U.S. Pet Food Market Size, Share, Trends & Growth Forecast Report Segmented By Pet Food Product (Pet Food, Pet Treats & Snacks, Pet Nutraceuticals & Supplements, Veterinary Diets / Prescription Food), Pet Type, Distribution Channel and Country – Industry Analysis From 2026 to 2034

U.S. Pet Food Market Report Summary

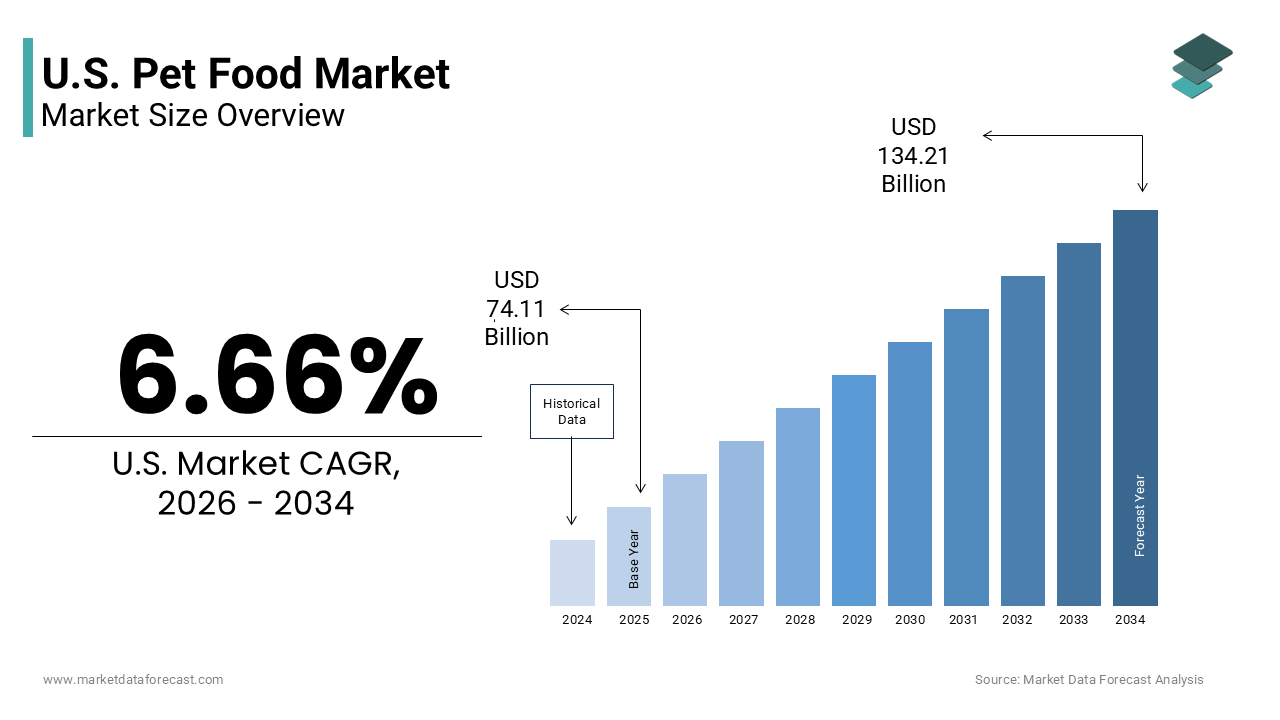

The U.S. pet food market was valued at USD 74.11 billion in 2025, is estimated to reach USD 79.05 billion in 2026, and is projected to reach USD 134.21 billion by 2034, growing at a CAGR of 6.66% during the forecast period from 2026 to 2034. The growth of the U.S. pet food market is driven by the increasing humanization of pets, rising pet ownership, and growing demand for premium and specialized nutrition products. The market has evolved significantly with trends such as organic, grain-free, and functional pet food, along with the rising adoption of personalized nutrition and sustainable sourcing practices.

Key Market Trends

- Rising demand for premium and human-grade pet food products

- Growing popularity of fresh, refrigerated, and minimally processed pet food

- Increasing focus on functional ingredients and health-focused nutrition

- Expansion of online and subscription-based pet food delivery models

- Strong emphasis on sustainability, transparency, and clean-label products

Segmental Insights

- Based on pet food product, the pet food segment was the largest and held a significant share of the U.S. pet food market in 2025. The segment’s dominance is attributed to its essential nature as a daily requirement for pet nutrition, ensuring consistent and high-volume demand across households.

- Based on pet type, the dog segment accounted for the largest share of the U.S. pet food market in 2025. This is driven by the high population of dogs, greater food consumption compared to other pets, and increased spending on premium dog nutrition products.

- Based on distribution channel, the supermarkets and hypermarkets segment was the largest, occupying a prominent share of the U.S. pet food market in 2025. The dominance of this segment stems from the convenience, wide product availability, and competitive pricing offered by large retail chains.

Regional Insights

- The United States dominates the North American pet food market due to its high pet ownership rates, strong consumer spending, and well-established pet care ecosystem. The market benefits from continuous innovation, advanced supply chains, and increasing demand for premium and health-oriented pet food products, making it a global leader in pet nutrition trends.

Competitive Landscape

The U.S. pet food market is characterized by intense competition among global corporations and niche premium brands, focusing on product innovation, quality, and brand differentiation. Companies are increasingly investing in digital platforms, personalized nutrition, and sustainable practices to gain a competitive edge. Prominent players in the U.S. pet food market include Mars, Incorporated, Nestlé Purina PetCare, Hill’s Pet Nutrition, Inc., The J.M. Smucker Company, General Mills, Inc., Diamond Pet Foods, WellPet LLC, Blue Buffalo Company, Ltd., and Freshpet, Inc.

U.S. Pet Food Market Size

The U.S. Pet Food Market size was valued at USD 74.11 billion in 2025 and is anticipated to reach USD 79.05 billion in 2026 from USD 134.21 billion by 2034, growing at a CAGR of 6.66% during the forecast period from 2026 to 2034.

Pet food is specialized animal feed intended for domesticated pets, formulated to meet their daily nutritional needs. Sold in dry (kibble), wet (canned), and raw formats, it combines proteins, cereals, fats, vitamins, and minerals. This market has evolved from providing basic sustenance to offering specialized dietary solutions that mirror human food trends including organic grain free and raw options. As per the American Pet Products Association (APPA), approximately 63 percent of U.S. households own a pet, which translates to roughly 82 million homes, demonstrating the deep integration of animals into family structures. The market definition extends beyond dry kibble to include wet food freeze dried treats and functional supplements designed to address specific health concerns such as joint mobility and digestive health. According to the US Department of Agriculture the value of livestock slaughter byproducts which serve as key ingredients in pet food remains substantial indicating the industry's reliance on agricultural supply chains. Consumer behavior is increasingly driven by the humanization of pets where owners view their animals as children and prioritize premium quality ingredients. Data from the Bureau of Labor Statistics shows that expenditure on veterinary care and pet supplies has risen consistently outpacing general inflation rates. The regulatory landscape is governed by the Association of American Feed Control Officials which sets standards for labeling and ingredient definitions ensuring safety and transparency. Understanding this market requires analyzing the shift toward personalized nutrition and the growing demand for sustainable sourcing practices that appeal to environmentally conscious consumers.

MARKET DRIVERS

Humanization of Pets and Premiumization Trends

The profound emotional bond between owners and their pets drives the demand for premium and human grade pet food products in the United States pet food market. Consumers increasingly perceive their pets as family members leading to a willingness to spend more on high quality nutrition that parallels their own dietary preferences. As per the American Pet Products Association spending on pet food and treats reached record highs with owners prioritizing natural and organic ingredients over conventional options. This trend is evident in the rising sales of fresh and refrigerated pet meals which offer perceived health benefits and higher palatability. According to Packaged Facts, surveys indicate that over 50 percent of pet owners actively seek out products with clear label claims such as no artificial preservatives or non-GMO verification. The desire to extend pet longevity and improve quality of life motivates purchases of functional foods enriched with vitamins probiotics and antioxidants. Retailers respond by expanding shelf space for premium brands and introducing private label lines that cater to these discerning buyers. The influence of social media also plays a role as owners share feeding routines and product recommendations creating viral demand for niche brands. This cultural shift ensures that price sensitivity decreases among core consumer segments who view premium pet food as an essential investment in their companion's well being rather than a discretionary expense.

Increasing Pet Ownership and Population Growth

The steady growth in pet ownership rates and the overall population of companion animals contributes to the expansion of the United States pet food market. This expands the base of regular consumers. The adoption of pets surged during recent years and many new owners have retained their animals leading to sustained demand for daily nutrition. As per the American Veterinary Medical Association (AVMA), the number of households owning dogs and cats has stabilized following a historic surge, with the total pet population now growing at a more moderate pace. This demographic expansion creates a consistent need for staple food products regardless of economic fluctuations. According to the US Census Bureau the rise in single person households and delayed parenthood has contributed to higher pet adoption rates as individuals seek companionship and emotional support. Each new pet represents a long term customer who requires daily feeding for potentially 10 to 15 years ensuring recurring revenue for manufacturers. The diversity of pet types including small breeds and senior animals further segments the market allowing for targeted product development. Multi pet households are also common with many families owning both dogs and cats which doubles the consumption volume per home. This structural growth in the pet population provides a stable foundation for market expansion as manufacturers innovate to meet the varying nutritional needs of different life stages and breeds.

MARKET RESTRAINTS

Volatility in Raw Material Costs and Supply Chain Disruptions

The fluctuation in prices for key ingredients, such as meat, poultry, grains, and vegetables, slows down the growth of the United States pet food market. This impacts production costs and profit margins. Manufacturers rely on agricultural commodities that are subject to weather conditions disease outbreaks and global trade policies which can cause sudden price spikes. As per the US Department of Agriculture indices for feed grains and protein meals have experienced considerable volatility affecting the cost structure for pet food producers. These increases often force companies to raise retail prices which can deter price sensitive consumers and lead to trading down to cheaper alternatives. According to the Bureau of Labor Statistics the producer price index for animal food manufacturing has risen sharply reflecting the pressure on input costs. Supply chain disruptions further complicate procurement with delays in sourcing specific ingredients like novel proteins or specialized additives. The reliance on imported materials exposes the industry to geopolitical tensions and logistical bottlenecks that can halt production lines. Smaller brands with less purchasing power struggle to absorb these costs making it difficult to compete with larger corporations that can hedge against price risks. Consequently, the instability in raw material availability and pricing constrains the ability of manufacturers to maintain consistent product quality and affordability limiting market growth potential.

Regulatory Complexity and Labeling Standards

Strict regulatory requirements and evolving labeling standards act as a major restraint on the United States pet food market. Thie increases compliance costs and limits marketing flexibility. The Association of American Feed Control Officials and the Food and Drug Administration enforce rigorous guidelines regarding ingredient definitions nutritional adequacy and claim substantiation. As per AAFCO standards (upheld by the FDA), regulations prohibit misleading claims such as "human grade" unless every ingredient and the manufacturing facility meet human food production standards, which restricts how brands communicate quality. Navigating these rules requires significant legal and technical resources particularly for companies introducing innovative ingredients or novel processing methods. According to industry associations the lack of uniformity in state level regulations creates a fragmented compliance landscape that complicates national distribution strategies. Missteps in labeling can result in costly recalls and reputational damage eroding consumer trust. The scrutiny on terms like natural and holistic forces manufacturers to provide extensive documentation proving the origin and processing of ingredients. Additionally, emerging concerns about contaminants such as heavy metals in pet food have led to tighter testing protocols and reporting requirements. These regulatory burdens slow down product launches and increase operational expenses for all market participants. Companies must balance innovation with compliance ensuring that new formulations meet all safety standards before reaching shelves. This cautious environment can stifle creativity and delay the introduction of beneficial new products to the market.

MARKET OPPORTUNITIES

Expansion of Fresh and Refrigerated Food Segments

The growing demand for fresh and refrigerated pet food offers a significant opportunity for the United States market. This trend appeals to owners seeking minimally processed and highly palatable options. These products offer superior nutritional value and freshness compared to traditional dry kibble aligning with human food trends toward clean eating and whole ingredients. As per Packaged Facts, the fresh pet food segment is projected to grow at a compound annual growth rate of approximately 23.5% through 2030, driven by increased consumer awareness of health benefits and the convenience of subscription models. Major retailers are expanding their cold chain infrastructure to accommodate these perishable items making them more accessible to mainstream shoppers. According to research, sales of fresh dog and cat food have outpaced other categories in terms of year-over-year dollar growth, indicating strong consumer acceptance and willingness to pay a premium. Subscription based delivery models further enhance convenience allowing owners to receive regular shipments of portioned meals tailored to their pet's specific needs. This direct to consumer approach builds loyalty and provides valuable data for personalized marketing. Partnerships with veterinary clinics and pet wellness centers also offer channels for educating consumers about the benefits of fresh diets. By investing in cold chain logistics and marketing education manufacturers can capture value from this high growth segment. The opportunity extends to developing sustainable packaging solutions that address environmental concerns associated with refrigerated goods. This convergence of convenience health and sustainability positions fresh food as a key driver of future market expansion.

Integration of Functional Ingredients and Personalized Nutrition

The integration of functional ingredients and personalized nutrition solutions creates up new chances for the United States pet food market. Consumers are increasingly interested in preventive health care for their pets seeking foods that address specific issues such as anxiety weight management and skin health. As per the American Veterinary Medical Association there is rising interest in therapeutic diets that support overall wellness through targeted nutrient profiles. Manufacturers can leverage advancements in nutritional science to formulate products with added probiotics omega fatty acids and joint supporting supplements. According to research, the global pet nutraceuticals landscape is expanding rapidly reflecting the demand for health enhancing food options. Personalization technologies allow companies to create custom meal plans based on a pet's breed age activity level and health status providing a tailored experience that commands higher prices. Digital platforms facilitate this process by collecting user data and generating recommendations that optimize pet health outcomes. Collaborations with veterinarians and nutritionists enhance credibility and ensure that formulations are scientifically sound. This approach transforms pet food from a commodity into a specialized health product fostering deeper brand engagement. By focusing on individual needs manufacturers can build loyal customer bases that value expertise and customization. The opportunity lies in combining scientific innovation with digital tools to deliver precise nutritional solutions that improve pet longevity and quality of life.

MARKET CHALLENGES

Prevalence of Private Label and Generic Brands

The widespread availability of private label and generic pet food brands is a major hurdle to established manufacturers in the United States pet food market. This intensifies price competition and erodes brand loyalty. Retailers such as Walmart Costco and Amazon develop their own exclusive lines that offer comparable quality at lower prices attracting cost conscious consumers. As per a study, private label pet food sales have grown significantly, capturing market share from national brands particularly during periods of economic uncertainty as consumers seek value. These store brands benefit from lower marketing costs and direct shelf placement allowing them to undercut branded competitors on price. According to sources, shoppers are increasingly willing to switch to private labels when they perceive little difference in quality between options. This trend pressures mainstream manufacturers to reduce prices or increase promotional spending which squeezes profit margins. The perception that private labels have improved in quality due to better sourcing and manufacturing standards further strengthens their competitive position. Established brands must invest heavily in differentiation through unique ingredients storytelling and customer engagement to justify premium pricing. However, the sheer volume and accessibility of generic options make it difficult to retain price sensitive segments. This dynamic creates a constant battle for shelf space and consumer attention forcing companies to continuously innovate while managing costs. The challenge lies in maintaining brand equity and perceived value in a market where affordable alternatives are readily available and widely promoted.

Counterfeit Products and Safety Concerns

The presence of counterfeit pet food products and ongoing safety concerns inhibits the expansion of the United States pet food market. This undermines consumer trust and poses health risks to animals. Illicit manufacturers produce fake versions of popular brands using substandard or harmful ingredients which can lead to severe health issues and even death in pets. As per the FDA reports of contaminated pet food containing elevated levels of toxins or undeclared substances periodically trigger recalls that damage industry reputation. These incidents create fear and hesitation among buyers who may question the safety of even legitimate products. According to the Pet Food Institute combating counterfeits requires extensive monitoring and enforcement efforts which are costly and complex given the global nature of supply chains. Online marketplaces exacerbate the problem by providing platforms for unauthorized sellers to distribute fake goods without adequate verification. Consumers who inadvertently purchase counterfeit items may blame the original brand leading to negative reviews and loss of loyalty. The difficulty in distinguishing authentic products from fakes especially in digital channels complicates the purchasing decision. Manufacturers must invest in anti counterfeit technologies such as holographic labels and blockchain tracking to ensure product integrity. However, these measures add to operational costs and may not fully eliminate the risk. Maintaining consumer confidence in the face of these threats requires transparent communication and rapid response to safety issues which remains a persistent operational burden.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.66% |

| Segments Covered | By Pet Food Product, Pet Type, Distribution Channel and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, and the Rest of the United States. |

| Key Market Players | Mars, Incorporated, Nestlé Purina PetCare, Hill’s Pet Nutrition, Inc., The J.M. Smucker Company, General Mills, Inc., Diamond Pet Foods, WellPet LLC, Blue Buffalo Company, Ltd., and Freshpet, Inc.. |

SEGMENTAL ANALYSIS

By Pet Food Product Insights

The pet food segment dominated the United States market in 2025. Its status as a daily essential necessity for pet survival and health drives the dominance of this segment. Unlike treats or supplements which are discretionary or supplemental main meals constitute the baseline expenditure for every pet owner ensuring consistent and high volume demand. As per the American Pet Products Association annual surveys indicate that pet food accounts for the largest portion of total pet care spending with billions of dollars allocated annually to staple diets. This dominance is reinforced by the biological requirement for regular feeding meaning that purchase frequency remains high regardless of economic conditions. According to Packaged Facts data shows that over 90 percent of dog and cat owners purchase commercial food regularly highlighting the deep market penetration of this category. The variety of formats including kibble canned and fresh options allows manufacturers to cater to diverse preferences and budgets ensuring broad accessibility. Furthermore, the transition toward premiumization within the food segment itself where owners upgrade from standard to natural or grain free varieties drives value growth even if volume remains stable. Retailers prioritize shelf space for core food brands due to their reliable turnover rates. The emotional bond between owners and pets ensures that nutrition is never compromised making this segment the financial backbone of the industry. Manufacturers focus on innovation in ingredient sourcing and formulation to retain loyalty in this competitive but stable category.

The pet nutraceuticals and supplements segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 8.5% over the forecast period due to the increasing focus on preventive healthcare and wellness for aging pets. Owners are proactively seeking solutions to manage chronic conditions such as arthritis anxiety and digestive issues through dietary additions rather than relying solely on veterinary pharmaceuticals. As per research the rising prevalence of obesity and age related ailments in pets has spurred demand for functional ingredients like glucosamine probiotics and omega 3 fatty acids. This trend aligns with the humanization of pets where owners apply their own health conscious behaviors to their companions. According to the American Holistic Veterinary Medical Association (AHVMA) and industry tracking, veterinarians increasingly incorporate supplements into integrative care plans, though the broader medical community emphasizes the need for quality-certified products (such as those with the NASC Seal) to ensure safety. The availability of these products in easy to administer formats such as chews and powders enhances compliance and convenience for owners. Social media and influencer marketing play a significant role in educating consumers about the benefits of specific supplements driving trial and repeat purchases. Additionally, the expansion of product lines by major pet food companies into the wellness space lends credibility and distribution advantages to this segment. The ability to address specific health concerns without prescription requirements makes supplements an accessible entry point for health focused pet care. This combination of medical validation consumer awareness and product innovation propels the rapid expansion of the nutraceuticals sector.

By Pets Insights

The dog segment led the United States pet food market in 2025. This leading position of the segment is attributed to the large population of canine companions and their higher caloric needs compared to other pets which results in greater volume consumption. Dogs are the most popular pet in the US with millions of households owning at least one creating a massive base for food sales. As per the American Pet Products Association (APPA), dogs account for the highest share of pet ownership, with approximately 58 million U.S. households including a dog in their family. This widespread ownership translates into substantial recurring revenue for manufacturers as dogs require larger quantities of food daily. According to the US Department of Agriculture data on livestock usage indicates that a significant portion of meat byproducts is directed toward dog food production reflecting the scale of this segment. The diversity of dog breeds sizes and activity levels necessitates a wide range of specialized formulations from puppy to senior diets allowing for extensive product differentiation. Owners of large breed dogs particularly spend more on premium foods to support joint health and longevity. The social nature of dogs also leads to higher engagement in training and activities where treats and specialized diets are used as rewards. Furthermore, the emotional bond with dogs often drives owners to invest in higher quality nutrition to ensure their companions live longer healthier lives. This combination of population size consumption volume and willingness to spend solidifies the dog segment as the primary driver of the pet food industry.

The cat segment is expected to exhibit a noteworthy CAGR of 7.2% from 2026 to 2034 owing to changing lifestyle trends and the increasing popularity of cats among urban dwellers and younger generations. Cats are perceived as lower maintenance pets requiring less space and outdoor access making them ideal for apartment living and busy professionals. As per the American Veterinary Medical Association the number of households owning cats has risen steadily with many multi cat households contributing to increased per household spending. Cat owners are increasingly willing to pay for premium wet and raw food options which are often priced higher per ounce than dry dog food. According to Packaged Facts surveys indicate that cat owners are more likely to purchase specialized diets for hairball control urinary health and weight management driving demand for functional formulas. The rise of indoor only cats has also shifted focus toward nutrition that supports sedentary lifestyles and prevents obesity. Social media platforms have amplified the cultural presence of cats influencing owners to indulge their pets with high quality treats and meals. Additionally, the aging cat population requires senior specific nutrition which commands higher prices and fosters brand loyalty. Manufacturers are responding with innovative textures and flavors that appeal to the selective palates of cats. This shift toward high value specialized nutrition ensures that the cat segment outpaces others in revenue growth despite lower overall volume compared to dogs.

By Distribution Channel Insights

The supermarkets and hypermarkets segment held the majority share of the United States pet food market in 2025. This supremacy of the segment is credited to its convenience extensive product assortment and ability to offer competitive pricing through economies of scale. These retail giants allow consumers to purchase pet food alongside their regular grocery items simplifying shopping trips and encouraging impulse buys. The widespread geographic presence of these stores ensures accessibility for consumers in both urban and rural areas. Also, the ability to stock large volumes of heavy dry food bags reduces logistical costs for retailers and offers value packs that appeal to multi pet households. Private label brands offered by these retailers further attract budget conscious consumers who seek quality alternatives to national brands. The integration of pharmacy and pet care sections within superstores creates a one stop shop experience that enhances customer retention. Additionally, the trust associated with established grocery chains reassures buyers about product safety and freshness. This combination of convenience affordability and accessibility ensures that supermarkets remain the primary destination for routine pet food purchases despite the rise of online competitors.

Rapid Growth of the Online Channel

The online distribution segment is predicted to witness the highest CAGR of 12.5% during the forecast period. This swift growth of the segment is fuelled by the convenience of home delivery subscription models and expanded product selection. Consumers increasingly prefer the ease of ordering heavy bags of food online and having them delivered directly to their doors eliminating the physical burden of transport. Subscription services offered by companies like Chewy and Amazon provide automatic replenishment and discounts fostering strong customer loyalty and predictable revenue streams. Detailed product descriptions customer reviews and virtual consultations help buyers make informed decisions about specialized diets. The integration of telehealth services and automated reorder reminders adds value beyond simple transaction processing. Mobile apps facilitate seamless shopping experiences allowing users to manage purchases on the go. The pandemic accelerated this shift by normalizing online grocery and pet supply shopping a habit that has persisted post pandemic. This digital transformation enables retailers to gather data on purchasing patterns and personalize marketing efforts further enhancing engagement. The combination of convenience customization and comprehensive inventory positions the online channel as the primary engine of future growth.

REGIONAL ANALYSIS

U.S. Pet Food Market Analysis

The United States led the pet food market in the North American region and captured a 80.7% share in 2025 because of its high pet ownership rates and substantial consumer spending power. Its dominant position is reinforced by a culture that deeply integrates pets into family life driving consistent demand for high quality nutrition. As per the American Pet Products Association the US pet industry generates billions of dollars annually with food representing the largest single category of expenditure. The market is characterized by a mature ecosystem where global manufacturers innovate continuously to meet evolving consumer preferences for natural and functional ingredients. According to the US Department of Agriculture the robust agricultural sector provides a stable supply of raw materials supporting domestic production capabilities. Consumer behavior in the US is marked by a high adoption of premium and specialized products with owners willing to pay for health benefits and sustainability. The presence of major industry associations and regulatory bodies ensures high standards for safety and labeling fostering consumer trust. High disposable income levels among American households enable sustained investment in pet wellness including advanced dietary solutions. The diversity of the population drives varied preferences encouraging a wide range of product offerings from budget friendly to luxury tiers. This robust foundation ensures that the United States remains the central hub for pet food innovation and consumption influencing global trends and setting benchmarks for quality and service in the industry.

COMPETITIVE LANDSCAPE

The competition in the United States pet food market is intense and characterized by a mix of multinational conglomerates and agile niche brands vying for consumer attention. Major players compete on product quality brand reputation and innovation while smaller companies differentiate themselves through specialized formulations and transparent sourcing practices. The rise of direct to consumer models has disrupted traditional retail channels forcing established brands to enhance their digital presence and customer engagement strategies. Price sensitivity among consumers drives promotional activities and private label growth particularly in the mass market segment. Premium and super premium categories see fierce competition based on ingredient quality and health benefits such as grain free or raw diets. Regulatory compliance and safety standards remain critical differentiators as recalls can severely damage brand trust. Innovation in packaging sustainability and personalized nutrition offers competitive advantages for early adopters. Retailers play a pivotal role by curating assortments that balance national brands with exclusive private labels. This dynamic environment requires continuous adaptation and strategic investment to maintain market relevance and profitability.

KEY MARKET PLAYERS

A few of the major companies in the U.S. Pet Food market include

- Mars, Incorporated

- Nestlé Purina PetCare

- Hill’s Pet Nutrition, Inc.

- The J.M. Smucker Company

- General Mills, Inc.

- Colgate-Palmolive Company

- Diamond Pet Foods

- WellPet LLC

- Blue Buffalo Company, Ltd.

- Freshpet, Inc.

Top Players in the Market

Mars Pet Care Inc

Mars Pet Care Inc stands as a global leader in the pet nutrition industry with a diverse portfolio including premium brands like Royal Canin Pedigree and Whiskas. The company focuses on advancing veterinary care and personalized nutrition through scientific research and innovation. Recent actions include expanding its acquisition of specialized veterinary diet brands and investing in digital health platforms for pets. Mars leverages its extensive global distribution network to ensure product availability across various retail channels. The firm prioritizes sustainability by committing to responsible sourcing and reducing environmental impact in its supply chain. By integrating data driven insights into product development Mars creates tailored solutions for specific pet needs. These strategic initiatives enhance brand loyalty and drive growth in both companion animal food and healthcare sectors while maintaining a strong competitive edge in the global marketplace.

Nestlé Purina PetCare Company

Nestlé Purina PetCare Company is a dominant force in the global pet food market offering iconic brands such as Pro Plan Fancy Feast and Purina One. The company emphasizes science based nutrition and continuous innovation to meet evolving consumer demands for high quality pet food. Recent strategies involve expanding its presence in the premium and super premium segments through new product launches and facility upgrades. Purina invests heavily in research and development to create functional foods that address specific health concerns like weight management and digestive health. The firm strengthens its market position by engaging with pet owners through educational campaigns and community programs. By leveraging Nestlés global resources Purina ensures consistent quality and safety standards across its product lines. These efforts solidify its reputation as a trusted provider of nutritious and innovative pet care solutions worldwide.

General Mills Inc Blue Buffalo

General Mills Inc through its Blue Buffalo subsidiary plays a significant role in the global pet food market by focusing on natural and holistic nutrition options. The brand is renowned for its Life Protection Formula which features real meat whole grains and garden vegetables. Recent actions include expanding product lines to include grain free and limited ingredient diets catering to pets with sensitivities. General Mills leverages its robust supply chain and marketing expertise to enhance Blue Buffalos visibility in retail and online channels. The company prioritizes transparency in sourcing and manufacturing processes to build trust with health conscious consumers. By investing in sustainable packaging and community engagement initiatives General Mills strengthens its brand equity. These strategic moves enable Blue Buffalo to compete effectively in the premium segment while driving growth through innovation and customer centric approaches in the dynamic pet food industry.

Top Strategies Used by Key Market Participants

Key players in the United States pet food market prioritize product innovation by developing specialized formulas that address specific health needs such as digestive support and joint care. Companies focus on premiumization strategies by introducing natural organic and human grade ingredients to appeal to health conscious pet owners. Digital transformation is central to their approach with investments in e commerce platforms and subscription services enhancing customer convenience and retention. Brands leverage data analytics to personalize marketing campaigns and improve product recommendations for individual pets. Sustainability initiatives including eco friendly packaging and responsible sourcing are prominently featured to align with consumer values. Strategic acquisitions of niche brands allow major corporations to expand their portfolios and reach diverse demographic segments. Partnerships with veterinarians and pet influencers help build credibility and trust. These combined strategies enable firms to navigate competitive pressures and drive sustainable growth in a rapidly evolving market landscape.

MARKET SEGMENTATION

This research report on the U.S. Pet Food has been segmented based on the following categories.

By Pet Food Product

- Pet Food

- Dry Food (Kibble)

- Wet Food (Canned)

- Fresh & Frozen Food

- Dehydrated & Freeze-Dried Food

- Pet Treats & Snacks

- Biscuits & Crunchy Treats

- Soft & Chewy Treats

- Dental Treats

- Jerky & Meat-Based Treats

- Pet Nutraceuticals & Supplements

- Vitamins & Minerals

- Joint Health Supplements (Glucosamine, Chondroitin)

- Digestive Health (Probiotics & Prebiotics)

- Skin & Coat Care (Omega-3 Fatty Acids)

- Calming & Anxiety Relief Supplements

- Veterinary Diets / Prescription Food

- Weight Management Diets

- Gastrointestinal Diets

- Renal (Kidney) Diets

- Allergy & Hypoallergenic Diets

By Pets

- Cats

- Dogs

- Other Pets

By Distribution Channel

- Convenience Stores

- Online Channel

- Specialty Stores

- Supermarkets/Hypermarkets

- Other Channels

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com