U.S. Piano Market Size, Share, Trends & Growth Forecast Report Segmented By Distribution Channel (Offline, Online), Product, End-User and Country – Industry Analysis From 2026 to 2034

U.S. Piano Market Report Summary

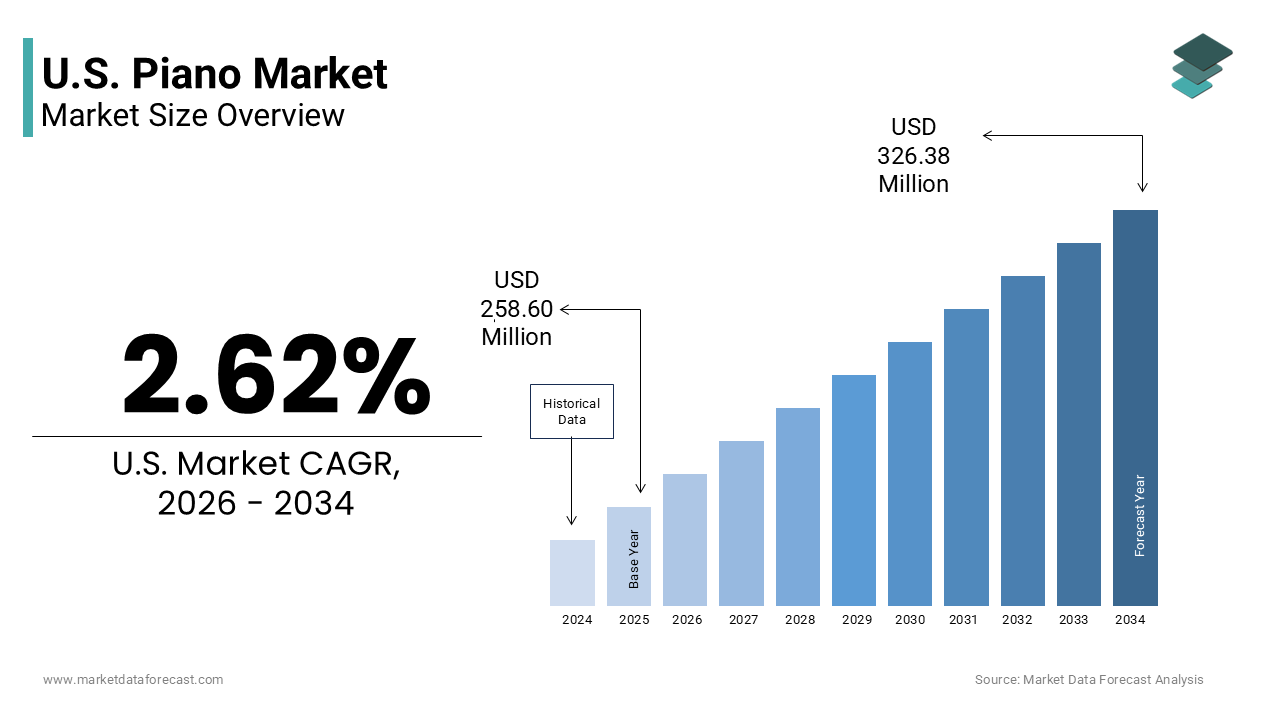

The U.S. piano market was valued at USD 258.60 million in 2025, is estimated to reach USD 265.38 million in 2026, and is projected to reach USD 326.38 million by 2034, growing at a CAGR of 2.62% during the forecast period from 2026 to 2034. The growth of the U.S. piano market is driven by the resurgence of home-based entertainment, increasing interest in music as a hobby, and steady demand from educational institutions. Additionally, the integration of digital technologies and hybrid instruments is reshaping consumer preferences and expanding market accessibility.

Key Market Trends

- Rising interest in home-based hobbies and creative activities

- Growing adoption of digital and hybrid pianos with smart features

- Increasing use of online learning platforms and music education apps

- Expansion of direct-to-consumer and online sales channels

- Demand for compact and space-efficient instruments in urban households

Segmental Insights

- Based on product, the digital piano segment was the largest and held a significant share of the U.S. piano market in 2025. The segment’s dominance is attributed to its affordability, low maintenance, compact design, and compatibility with digital learning tools.

- Based on distribution channel, the offline segment accounted for a major share of the U.S. piano market in 2025. This is driven by the need for physical interaction, sound testing, and expert consultation before purchasing high-value instruments.

- Based on end-user, the amateur musicians segment was the largest, driven by the widespread participation in music as a hobby, supported by online tutorials and increasing interest in personal creative expression.

Regional Insights

The United States represents a mature and culturally significant piano market, supported by a strong ecosystem of music education programs, retail networks, and performance venues. States such as California, New York, and Washington play a key role due to their high population density, cultural diversity, and strong demand for musical instruments.

Competitive Landscape

The U.S. piano market is characterized by competition between global digital instrument manufacturers and premium acoustic piano makers. Companies are focusing on product innovation, hybrid technology integration, and enhanced customer experiences to remain competitive. Prominent players in the U.S. piano market include Yamaha Corporation, Kawai Musical Instruments Manufacturing Co., Ltd., Steinway & Sons, Baldwin Piano Company, Casio Computer Co., Ltd., Korg Inc., Roland Corporation, Samick Musical Instruments Co., Ltd., and Young Chang.

U.S. Piano Market Size

The U.S. Piano Market size was valued at USD 258.60 million in 2025 and is anticipated to reach USD 265.38 million in 2026 from USD 326.38 million by 2034, growing at a CAGR of 2.62% during the forecast period from 2026 to 2034.

A piano is primarily known as a large acoustic musical instrument that produces sound by striking metal strings with felt-covered hammers, controlled by a keyboard. This market is characterized by a dichotomy between traditional craftsmanship and modern technological integration where high end acoustic instruments coexist with versatile digital alternatives. As per the National Association of Music Merchants participation in music making remains a significant cultural activity with millions of Americans engaging in keyboard based instruments annually. The market definition extends beyond mere hardware sales to include maintenance tuning services and educational software that support the instrument lifecycle. According to the U.S. Census Bureau and the Bureau of Economic Analysis (BEA), household expenditure for recreational equipment, including musical instruments, has softened recently as consumers prioritize services and experiences over the purchase of durable goods. The industry relies heavily on a network of independent dealerships and specialized retailers who provide essential trial experiences and after sales support. Consumer behavior is increasingly influenced by space constraints in urban living environments which drives demand for compact digital models and silent acoustic systems. Data from the National Center for Education Statistics (NCES) shows that while a vast majority of public schools offer music education, actual enrollment in instrumental programs has faced stagnation, with industry groups noting a shift toward digital keyboard labs to manage rising equipment and maintenance costs. The market also faces evolving trends in home entertainment where self taught learning via apps complements traditional instruction. Understanding this landscape requires analyzing the interplay between demographic shifts housing trends and the enduring cultural value placed on musical proficiency and artistic expression in American society.

MARKET DRIVERS

Resurgence of Home Based Entertainment and Hobbyist Engagement

The shift toward home-centric lifestyles has significantly boosted the growth of the United States piano market. Consumers are seeking meaningful offline activities and creative outlets within their living spaces. The pandemic accelerated this trend but the habit of investing in home entertainment infrastructure has persisted driving sustained interest in musical instruments. As per the National Endowment for the Arts surveys indicate that personal participation in music creation has remained robust with keyboard instruments being among the most popular choices for adults and children alike. This cultural shift encourages households to allocate budget for high quality instruments that serve both educational and recreational purposes. According to the Bureau of Labor Statistics (BLS), time spent on hobbies and leisure at home has stabilized at pre-pandemic levels following a temporary surge, creating a more competitive environment for time-intensive activities such as piano practice. The desire for mental stimulation and stress relief through music making appeals to diverse age groups from young learners to retirees. Digital pianos with headphone capabilities allow for quiet practice in apartments making them accessible to urban dwellers who previously lacked space or noise tolerance for acoustic models. Furthermore, the rise of online learning platforms and tutorial apps lowers the barrier to entry for self taught musicians expanding the potential customer base. This convergence of lifestyle changes technological accessibility and psychological benefits sustains strong demand for pianos as central pieces of home cultural life.

Strong Institutional Demand from Educational Sector

The educational sector remains a key accelerator for the United States piano market. This is due to mandatory and elective music programs in schools colleges and universities that require reliable instruments for instruction. Institutions regularly purchase and replace pianos to maintain standards for student training performances and examinations ensuring a consistent baseline of commercial demand. As per the National Center for Education Statistics thousands of public and private schools across the country maintain music departments that rely on acoustic and digital pianos for curriculum delivery. This institutional procurement provides stability for manufacturers even when consumer discretionary spending fluctuates. According to the National Center for Education Statistics (NCES), music-related degree programs continue to graduate approximately 25,000 students annually, necessitating the maintenance of practice rooms, though the focus is increasingly shifting toward digital and hybrid instrumentation. Universities often invest in concert grand pianos for recital halls and performance venues enhancing their prestige and attracting talent. Additionally, community music schools and private studios contribute to demand by purchasing entry level and intermediate models for student use. The longevity of these institutions ensures long term relationships with suppliers who provide maintenance and tuning services alongside sales. Government grants and private donations occasionally fund music program expansions further stimulating purchases. This structural reliance on formal education creates a predictable revenue stream for the industry anchored in the societal value placed on musical literacy and artistic development.

MARKET RESTRAINTS

High Cost of Ownership and Maintenance Burdens

The substantial financial commitment required for acquiring and maintaining acoustic pianos remains an obstacle for the United States market. This limits accessibility for middle and lower income households. High end grand and upright pianos often cost several thousand dollars with additional recurring expenses for tuning regulation and potential repairs. As per the Piano Technicians Guild recommended tuning frequency is at least twice a year with each session costing between 100 and 200 dollars creating a significant ongoing burden for owners. This total cost of ownership discourages casual buyers who may prefer lower maintenance alternatives such as digital keyboards. According to the Bureau of Labor Statistics inflationary pressures on household budgets have led consumers to prioritize essential spending over luxury items like premium musical instruments. The complexity of moving and installing heavy acoustic pianos also adds logistical costs and risks deterring renters or those in transient living situations. Furthermore, the depreciation of used pianos can be steep making them less attractive as investment pieces compared to other assets. Potential buyers often hesitate due to fear of hidden repair costs associated with older instruments such as soundboard cracks or action issues. This financial barrier restricts market growth to affluent segments or dedicated enthusiasts while excluding broader demographics who might otherwise engage with the instrument. Thus, the high entry and maintenance costs constrain volume sales and limit the expansion of the acoustic piano segment.

Space Constraints in Urban Living Environments

The increasing prevalence of compact living spaces in urban areas inhibits the expansion of the United States piano market. This is particularly true for large acoustic instruments that require substantial floor area. Modern apartments and condominiums often lack the square footage necessary to accommodate grand pianos or even large uprights without compromising living comfort. As per the U.S. Census Bureau and industry data, the average size of new rental units in major metropolitan areas has hit record lows, dropping to roughly 890 square feet in 2025, which significantly limits the available space for bulky furniture like acoustic pianos. This spatial limitation forces consumers to opt for smaller digital alternatives or forego piano ownership entirely. According to real estate data from Zillow urban housing trends show a preference for multifunctional rooms where large fixed items are impractical. The weight of acoustic pianos also presents structural challenges in older buildings with floor load restrictions requiring professional assessment and reinforcement which adds to the cost and complexity of ownership. Noise transmission concerns in multi unit dwellings further discourage the use of acoustic instruments due to potential conflicts with neighbors. While silent systems and digital options mitigate some issues they do not fully replicate the aesthetic and tactile experience of traditional pianos. This physical constraint reduces the addressable market for high end acoustic models and shifts demand toward compact portable solutions thereby limiting revenue potential for manufacturers specializing in large traditional instruments.

MARKET OPPORTUNITIES

Integration of Smart Technology and Hybrid Instruments

The integration of smart technology into pianos paves the way for the growth of the United States market. This shift appeals to tech savvy consumers and modernizes the learning experience. Hybrid and silent pianos that combine acoustic actions with digital connectivity allow users to practice quietly record performances and access interactive learning apps. As per the Consumer Technology Association the adoption of connected home devices continues to rise indicating a receptive audience for smart musical instruments. These technologies enable features such as automatic accompaniment lesson feedback and remote instruction which enhance engagement and retention for students. Manufacturers can differentiate their offerings by partnering with educational platforms to provide bundled subscriptions that add recurring revenue streams. The ability to update firmware and add new features over the air extends product lifecycle and value proposition. Additionally, silent systems allow acoustic piano owners to practice with headphones addressing noise concerns in urban environments and expanding the usability of the instrument. This convergence of tradition and technology attracts younger demographics who value connectivity and versatility. Piano makers can leverage Internet of Things capabilities to turn static instruments into interactive hubs for musical exploration. These connected pianos allow companies to capture value in the digital wellness and education sectors.

Expansion of Online Sales and Direct to Consumer Models

The expansion of online sales channels and direct-to-consumer (DTC) models provide promising prospects for the United States piano market. These developments overcome geographical limitations and reduce retail overheads. Traditional piano buying has been confined to local dealerships but e commerce platforms enable buyers to compare specifications prices and reviews from a wider selection. As per sources, online sales of musical instruments have grown significantly with consumers becoming more comfortable purchasing high ticket items digitally. Brands that develop robust virtual trial experiences such as high fidelity audio samples and augmented reality placement tools can mitigate the inability to physically test instruments. According to Shopify data DTC brands in niche hobby categories often achieve higher customer loyalty through personalized service and community building. Manufacturers can leverage social media and influencer marketing to reach targeted audiences directly bypassing intermediaries and improving margins. The availability of flexible financing options and white glove delivery services addresses logistical concerns associated with shipping heavy instruments. Additionally, online platforms facilitate the sale of accessories bundles and maintenance packages enhancing average order value. This digital transformation allows smaller brands to compete with established giants by offering unique value propositions and transparent pricing. Omnichannel strategies allow piano companies to expand their reach and capture market share. These digital approaches overcome the traditional retail limitations of physical footprints and inventory constraints.

MARKET CHALLENGES

Decline in Formal Music Education Programs

The reduction in funding and participation in formal music education programs within public schools is a critical challenge to the United States piano market. This shrinks the pipeline of early stage learners. Budget cuts and shifting academic priorities have led many districts to reduce or eliminate music classes limiting exposure to pianos for young students. As per the National Endowment for the Arts data indicates a decline in school based arts instruction over the past decade affecting the number of children who develop foundational keyboard skills. This trend reduces the likelihood of students continuing piano lessons privately or purchasing instruments for home use. According to the National Center for Education Statistics (NCES) and NASM, a shift in the prior training of high school graduates toward digital production has altered enrollment profiles in higher education, ultimately influencing the institutional demand for traditional acoustic pianos. The lack of early exposure means fewer adults pursue piano as a hobby later in life constraining long term consumer demand. Private lesson costs have also risen making it inaccessible for many families further exacerbating the decline in new players. Manufacturers face a shrinking base of entry level customers forcing them to rely on replacement sales and upgrades from existing owners. This structural shift requires the industry to invest heavily in alternative marketing and community outreach to stimulate interest outside of traditional educational pathways. The market risks stagnation and reduced innovation without a steady influx of new learners. This decline is largely driven by diminishing user engagement.

Shortage of Skilled Technicians and Service Providers

The scarcity of qualified piano technicians and tuners is a persistent barrier to the United States piano market. This affects instrument maintenance and customer satisfaction. Proper care of acoustic pianos requires specialized skills that are in short supply as the workforce ages and fewer apprentices enter the field. As per the Piano Technicians Guild the average age of registered technicians is rising with insufficient new entrants to replace retiring professionals. This shortage leads to longer wait times for service and higher costs for consumers discouraging proper maintenance and potentially damaging instruments. According to industry reports inadequate tuning and regulation can result in poor performance causing owners to lose interest or blame the instrument rather than the lack of care. The complexity of modern hybrid and high end acoustic pianos requires advanced technical knowledge further narrowing the pool of capable service providers. Geographic disparities mean that rural areas often lack access to any qualified technicians leaving owners without support. This service gap undermines the value proposition of owning an acoustic piano and pushes consumers toward low maintenance digital alternatives that do not require regular tuning. Manufacturers and dealers struggle to provide comprehensive after sales support which is crucial for brand loyalty and reputation. Addressing this challenge requires investment in training programs and incentives to attract new talent to the trade ensuring the sustainability of the acoustic piano ecosystem.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 2.62% |

| Segments Covered | By Distribution Channel, Product, End-User and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, and the Rest of the United States. |

| Key Market Players | Yamaha Corporation, Kawai Musical Instruments Manufacturing Co., Ltd., Steinway & Sons, Baldwin Piano Company, Casio Computer Co., Ltd., Korg Inc., Roland Corporation, Samick Musical Instruments Co., Ltd., and Young Chang. |

SEGMENTAL ANALYSIS

By Distribution Channel Insights

The offline distribution channel segment held the majority share of the United States piano market in 2025. This supremacy of the segment is attributed to the tactile and auditory nature of the product which necessitates physical interaction before purchase. Consumers typically require the opportunity to test the touch sensitivity tonal quality and aesthetic appeal of a piano in person which cannot be fully replicated through digital means. As per the National Association of Music Merchants independent music product dealerships remain the primary point of sale for acoustic instruments with over 60 percent of high end piano transactions occurring in physical showrooms. This dominance is reinforced by the need for professional consultation regarding instrument maintenance delivery logistics and room acoustics which dealers provide as part of the sales process. According to industry data from Piano Buyers magazine the majority of grand piano buyers visit multiple stores to compare brands ensuring that brick and mortar locations serve as critical decision making hubs. The trust established through face to face interactions with knowledgeable staff further cements the preference for offline channels particularly for premium purchases. Additionally, institutional buyers such as schools and concert halls rely on direct relationships with local dealers for bulk procurement and service contracts. The immediate availability of inventory and the ability to negotiate trade ins for used instruments also favor physical retail environments. This combination of sensory evaluation expert guidance and logistical support ensures that offline channels remain the cornerstone of piano retailing despite the growth of digital alternatives.

The online distribution channel segment is estimated to register the fastest CAGR of 9.2% from 2026 to 2034. This swift growth of the segment is propelled by the increasing popularity of digital pianos and the convenience of e commerce platforms. The shift toward compact and portable keyboard instruments has lowered the barriers to online purchasing as these products are easier to ship and do not require complex installation. As per eMarketer sales of musical instruments online have surged with digital pianos accounting for a significant portion of this growth due to their standardized specifications and lower price points. Consumers are increasingly comfortable researching and buying entry level and mid range instruments online where competitive pricing and extensive user reviews facilitate decision making. According to Shopify data direct to consumer brands leverage social media marketing and virtual trial tools to reach younger demographics who prefer digital shopping experiences. The availability of flexible financing options and white glove delivery services mitigates concerns about shipping heavy items enhancing consumer confidence. Furthermore, the integration of augmented reality apps allows buyers to visualize how a piano fits in their space adding a layer of confidence to remote purchases. The expansion of online marketplaces like Amazon and Reverb provides access to a wider variety of brands and models than local stores can stock. This convenience accessibility and broader selection drive the rapid expansion of the online channel particularly for digital and hybrid instruments.

By Product Insights

The digital piano segment led the United States market in 2025. This leading position of the segment is credited to its affordability versatility and suitability for modern living environments. These instruments offer a compelling alternative to acoustic pianos by providing consistent tuning headphone connectivity for silent practice and a wide range of sounds without the maintenance burdens. The ability to integrate with learning apps and recording software appeals to self taught musicians and students who value technological features alongside musical performance. In addition, the compact design of slab style digital pianos fits easily into apartments and small homes addressing the space constraints faced by many urban dwellers. Additionally, the lower initial cost compared to acoustic instruments makes digital pianos accessible to a broader demographic including parents buying first instruments for children. The durability and portability of digital models also make them popular for gigging musicians and educators who require reliable transportable solutions. This combination of practicality technological integration and cost effectiveness solidifies the digital piano segment as the dominant force in the current market landscape.

The acoustic piano segment is experiencing steady growth due to demand for high end luxury instruments and the enduring prestige associated with traditional craftsmanship. Professional musicians serious students and affluent households continue to prefer the authentic touch and resonant sound of stringed instruments which digital models cannot fully replicate. The emotional connection to the acoustic experience drives loyalty among dedicated pianists who prioritize tonal complexity and dynamic range. Moreover, the restoration and refurbishment market for vintage acoustic pianos also contributes to segment growth as enthusiasts seek unique character and historical value. Additionally, the integration of silent systems into new acoustic models allows owners to enjoy traditional sound while practicing quietly expanding the appeal of these instruments in noise sensitive environments. This focus on quality authenticity and status ensures that the acoustic segment maintains a robust presence in the high end market despite lower overall unit volumes compared to digital counterparts.

By End-User Insights

The amateur musicians segment was the largest segment in the United States piano market in 2025 because of the widespread participation in music making as a hobby and recreational activity among the general population. Millions of Americans learn piano for personal enjoyment stress relief and cognitive benefits creating a large base of consumers who purchase instruments for home use. As per research, playing a musical instrument is one of the most common artistic activities among adults with keyboards being a preferred choice due to their accessibility. This broad engagement fuels demand for entry level and mid range instruments that balance quality with affordability. The rise of online learning platforms and tutorial apps has lowered the barrier to entry for self taught amateurs encouraging more individuals to start playing later in life. Parents also contribute significantly to this segment by purchasing pianos for their childrens education and extracurricular development. The desire for creative expression and mental wellness further motivates amateur purchases making this group the primary driver of market volume. Retailers cater to this segment by offering bundled packages with accessories and lessons enhancing the appeal for novice players. This vast and diverse user base ensures that amateur musicians remain the cornerstone of piano consumption in the US.

The professional musicians segment is likely to experience the fastest CAGR over the forecast period owing to the need for high performance instruments and specialized equipment for careers in performance education and composition. Professionals require instruments with superior touch response tonal accuracy and durability to meet the demands of concerts recordings and teaching. This segment drives demand for luxury grand pianos and advanced digital stage keyboards that offer extensive customization and connectivity options. The expansion of live music venues and educational institutions also creates opportunities for professionals to acquire new instruments for their studios and classrooms. Additionally, the rise of remote collaboration and home recording has led professionals to upgrade their home setups with high fidelity instruments and interfaces. This focus on quality and functionality ensures that while the professional segment is smaller in volume it contributes significantly to revenue growth through high value transactions. Manufacturers prioritize innovation in this segment to maintain credibility and attract influential users who shape market perceptions.

REGIONAL ANALYSIS

U.S. Piano Market Analysis

The United States dominated the piano market and accounted for a 40.8% share in 2025. This dominance of the country’s market is driven by its strong cultural emphasis on music education and high disposable income. A well-established network, comprising dealers, music schools, and performance venues, drives ongoing demand and secures their market dominance. As per the National Association of Music Merchants the US music products industry generates billions in annual revenue with pianos representing a significant portion of keyboard instrument sales. The market is characterized by a mature ecosystem where traditional acoustic brands coexist with innovative digital manufacturers driving continuous product development. According to the U.S. Census Bureau and the Bureau of Economic Analysis (BEA), real consumer spending on durable recreational goods, including musical instruments, has stabilized following a period of historic growth, as households shift discretionary allocations toward recreational services and experiences. Consumer behavior in the US is marked by a high adoption of digital technologies with many buyers preferring hybrid instruments that offer both acoustic feel and digital connectivity. The presence of major international manufacturers and domestic distributors ensures a wide variety of choices for consumers at all price points. Regulatory standards for safety and environmental compliance are strictly enforced maintaining high quality benchmarks for imported and domestic products. The diversity of the population drives varied musical tastes encouraging manufacturers to offer a broad range of styles and features. This robust foundation ensures that the United States remains the central hub for piano innovation and consumption influencing global trends and setting standards for quality and service in the industry.

COMPETITIVE LANDSCAPE

The competition in the United States piano market is characterized by a distinct segmentation between mass market digital manufacturers and niche luxury acoustic builders. Major multinational corporations dominate the entry and mid level sectors through economies of scale and widespread distribution networks while specialized artisans cater to the high end segment with bespoke craftsmanship. Digital piano brands compete fiercely on technological features such as key action realism sound library depth and connectivity options often leveraging price advantages to capture volume. Acoustic manufacturers differentiate themselves through heritage brand equity tonal quality and resale value appealing to purists and institutions. The rise of hybrid instruments has blurred these lines creating new competitive dynamics where companies must excel in both mechanical engineering and digital signal processing. Independent dealers play a crucial role in this landscape by providing personalized service and maintenance that online retailers cannot match. Price sensitivity varies significantly across segments with amateur buyers seeking value and professionals prioritizing performance. Regulatory compliance and environmental standards also influence competitive positioning as consumers increasingly favor sustainable practices. This complex environment requires strategic agility and continuous innovation to maintain relevance.

KEY MARKET PLAYERS

A few of the major companies in the U.S. Piano Market include

- Yamaha Corporation

- Kawai Musical Instruments Manufacturing Co., Ltd.

- Steinway & Sons

- Baldwin Piano Company

- Casio Computer Co., Ltd.

- Korg Inc.

- Roland Corporation

- Samick Musical Instruments Co., Ltd.

- Young Chang

Top Players in the Market

Yamaha Corporation

Yamaha Corporation stands as a global leader in the musical instrument industry with a comprehensive portfolio spanning acoustic and digital pianos. The company leverages its vertical integration to control every aspect of production from timber sourcing to final assembly ensuring consistent quality. Recent actions include expanding its Silent Piano technology and integrating advanced sampling methods into Clavinova models to enhance realism. Yamaha strengthens its market position through extensive educational initiatives and artist partnerships that build brand loyalty among students and professionals. The firm invests heavily in research and development to create hybrid instruments that bridge the gap between traditional and digital experiences. By maintaining a strong presence in both entry level and concert grand segments Yamaha ensures broad market coverage. Its commitment to sustainability and craftsmanship reinforces its reputation for reliability and excellence in the global piano market.

Kawai Musical Instruments Manufacturing Co Ltd

Kawai Musical Instruments Manufacturing Co Ltd is renowned for its innovation in acoustic piano action design and high quality digital instruments. The company utilizes proprietary materials such as ABS Carbon in its mechanisms to provide stability and responsiveness regardless of humidity changes. Recent strategies involve enhancing its Novus NV series which combines acoustic actions with digital sound engines to offer silent practice capabilities. Kawai focuses on strengthening relationships with independent dealers and educational institutions to maintain a strong retail network. The firm emphasizes craftsmanship in its Shigeru Kawai line appealing to discerning artists who demand concert level performance. By prioritizing technological advancement and traditional woodworking skills Kawai differentiates itself in a competitive landscape. These efforts ensure sustained growth and recognition for producing instruments that meet the rigorous demands of professional musicians worldwide.

Steinway & Sons

Steinway & Sons represents the pinnacle of luxury piano manufacturing with a heritage of crafting hand built concert grand pianos for over a century. The company maintains its elite status by adhering to strict artisanal standards and selecting premium materials for each instrument. Recent actions include expanding its Spirio high resolution player piano system which allows for precise playback and remote performances. Steinway strengthens its market position through exclusive partnerships with concert halls and renowned pianists who endorse its brand globally. The firm offers comprehensive restoration services for vintage instruments preserving their value and historical significance. By focusing on exclusivity and superior tonal quality Steinway appeals to affluent consumers and institutions seeking prestige. These strategic initiatives reinforce its position as the most recognized and respected name in the high end segment of the global piano industry.

Top Strategies Used by Key Market Participants

Key players in the United States piano market prioritize product innovation by developing hybrid instruments that combine acoustic actions with digital sound technologies for versatile use. Companies focus on enhancing customer experience through virtual trial tools and augmented reality applications that allow buyers to visualize instruments in their homes. Strategic partnerships with music educators and online learning platforms help brands engage directly with students and amateur musicians effectively. Manufacturers emphasize sustainability by sourcing responsibly harvested woods and implementing eco friendly production processes to appeal to conscious consumers. Expansion of direct to consumer sales channels complements traditional dealership networks to reach broader audiences efficiently. Investment in artist relations and endorsements builds brand credibility and influences purchasing decisions among serious musicians. These combined approaches enable firms to navigate market shifts and maintain competitiveness in a evolving industry landscape.

MARKET SEGMENTATION

This research report on the U.S. Piano Market has been segmented based on the following categories.

By Distribution channel

- Offline

- Online

By Product

- Acoustic piano

- Digital piano

By End-user

- Amateur musicians

- Professional musicians

- Others

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com