U.S. Seafood Market Size, Share, Trends & Growth Forecast Report Segmented By Type ( Fish, Shrimps, Others ), Form, Distribution Channel and Country – Industry Analysis From 2026 to 2034

U.S. Seafood Market Report Summary

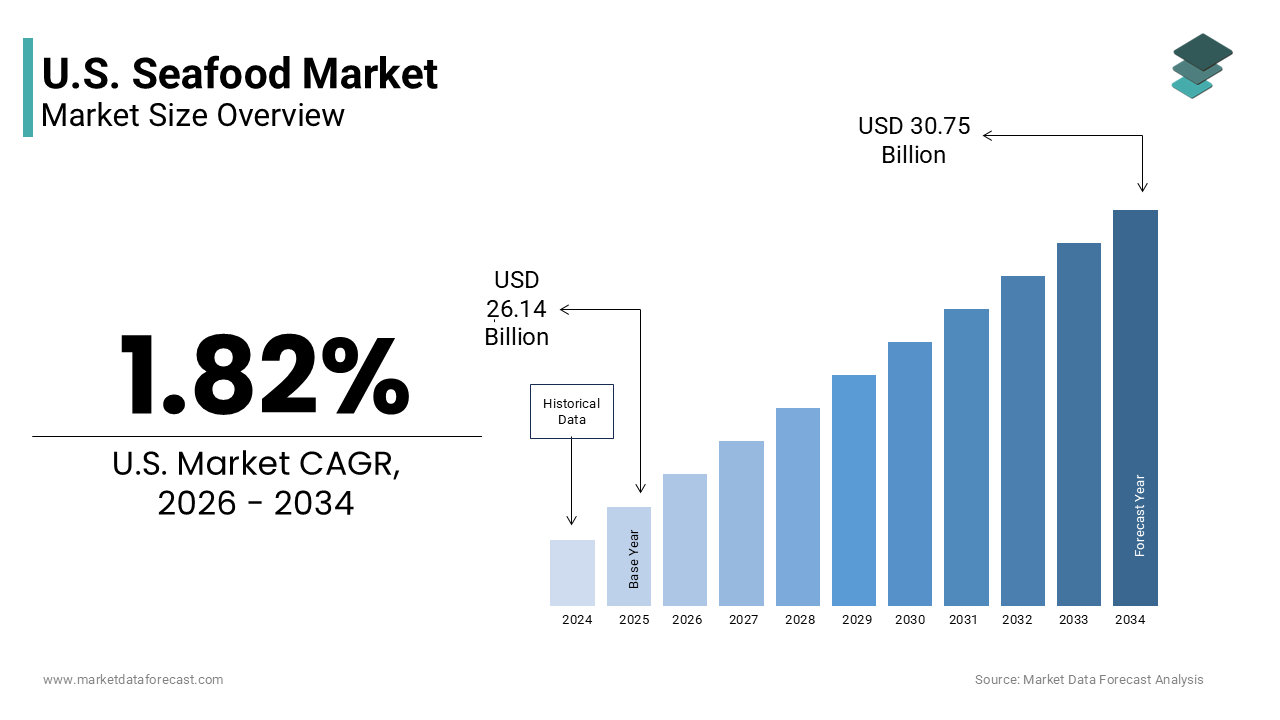

The U.S. seafood market was valued at USD 26.14 billion in 2025 and is estimated to reach USD 26.62 billion in 2026, and is projected to reach USD 30.75 billion by 2034, growing at a CAGR of 1.82% during the forecast period from 2026 to 2034. The growth of the U.S. seafood market is driven by increasing health consciousness, rising demand for high-protein diets, and growing preference for convenient ready-to-eat seafood products. However, the market is also shaped by heavy reliance on imports, sustainability concerns, and regulatory complexities, making it a dynamic and evolving sector.

Key Market Trends

- Rising demand for healthy protein sources rich in omega-3 fatty acids

- Increasing popularity of ready-to-eat and convenience seafood products

- Growing adoption of sustainable aquaculture and certified seafood sourcing

- Expansion of online grocery and cold-chain logistics infrastructure

- Increasing focus on traceability and transparency through digital technologies

Segmental Insights

- Based on type, the fish segment was the largest and held a significant share of the U.S. seafood market in 2025. The segment’s dominance is attributed to the high consumption of salmon and tuna, supported by their nutritional benefits, versatility, and year-round availability.

- Based on form, the frozen and canned segment accounted for a major share of the U.S. seafood market in 2025. This is driven by the extended shelf life, reduced food waste, and convenience offered by preserved seafood formats.

- Based on distribution channel, the off-trade segment was the largest, occupying a prominent share of the U.S. seafood market in 2025. The dominance of this segment stems from the strong presence of supermarkets, retail chains, and online grocery platforms that provide accessibility and variety to consumers.

Regional Insights

The United States remains a key player in the global seafood market, supported by its large consumer base, strong retail infrastructure, and increasing demand for nutritious food options. Coastal states such as California, Washington, and Oregon play a significant role in domestic production, while the country continues to rely heavily on imports to meet consumption demand.

Competitive Landscape

The U.S. seafood market is highly competitive and fragmented, with the presence of large multinational companies and regional processors competing on product quality, sustainability, and pricing strategies. Companies are increasingly focusing on value-added products, sustainable sourcing, and digital traceability solutions to strengthen their market position. Prominent players in the U.S. seafood market include Trident Seafoods, American Seafoods Group, Bumble Bee Foods, Chicken of the Sea, StarKist Co., High Liner Foods, Pacific Seafood, Phillips Foods, Inc., Beaver Street Fisheries, and Sysco Corporation.

U.S. Seafood Market Size

The U.S. Seafood Market size was valued at USD 26.14 billion in 2025 and is anticipated to reach USD 26.62 billion in 2026 from USD 30.75 billion by 2034, growing at a CAGR of 1.82% during the forecast period from 2026 to 2034.

The seafood is a complex and vital component of the national food system by encompassing the harvesting, processing, distribution, and consumption of marine and freshwater organisms. The significant disparity between domestic production and consumer demand, necessitating heavy reliance on international imports to satisfy dietary preferences. As per the National Oceanic and Atmospheric Administration, the United States imported approximately 79% of its seafood supply in 2023, highlighting a substantial trade deficit in this commodity category . Domestic commercial fisheries landed about 9.6 billion pounds of fish and shellfish, valued at 5.9 billion U.S. dollars, reflecting the economic importance of coastal communities and fishing industries . The market includes diverse species ranging from shrimp and salmon to tuna and crab, each with distinct supply chain dynamics and consumer appeal. Regulatory frameworks established by agencies such as the Food and Drug Administration and the Department of Commerce ensure safety standards and sustainable harvesting practices. Consumer trends indicate a growing preference for convenient, ready to eat seafood products, driven by busy lifestyles and health consciousness. The industry faces ongoing challenges related to sustainability certifications, labor practices, and environmental impacts. Despite these hurdles, the market remains robust due to the recognized nutritional benefits of seafood, including high protein content and omega 3 fatty acids. The integration of aquaculture into the domestic supply chain is gradually expanding, offering potential pathways to reduce import dependency. This dynamic landscape requires stakeholders to navigate regulatory, environmental, and economic factors to maintain competitiveness and meet evolving consumer expectations.

MARKET DRIVERS

Increasing Health Consciousness and Nutritional Awareness

The increasing health consciousness and nutritional awareness, as consumers actively seek protein sources that offer superior health benefits compared to red meats is majorly fuelling the growth of the United States seafood market. Seafood is widely recognized for its rich content of omega 3 fatty acids, high quality proteins, vitamins, and minerals, which are associated with reduced risks of cardiovascular diseases and improved cognitive function. As per the Dietary Guidelines for Americans issued by the Department of Health and Human Services, adults are recommended to consume at least 8 ounces of seafood per week to achieve optimal health outcomes. This official guidance has significantly influenced consumer behavior, leading to a steady increase in seafood consumption among health oriented demographics. Surveys conducted by the International Food Information Council indicate that over 60% of Americans consider seafood a healthy protein option, driving regular purchase habits. The aging population in the United States further amplifies this trend, as older adults prioritize heart healthy diets to manage chronic conditions. Additionally, the rise of fitness cultures and plant flexible diets has expanded the consumer base for seafood, attracting individuals who view it as a lean and nutritious alternative. Marketing campaigns by industry associations emphasizing these health benefits have reinforced positive perceptions. The availability of fortified and value added seafood products also caters to specific nutritional needs, enhancing accessibility.

Expansion of Retail Convenience and Ready to Eat Formats

The expansion of retail convenience and ready to eat seafood formats, addressing the time constraints of modern consumers is additionally escalating the growth of United States seafood market. Busy lifestyles and dual income households have increased the demand for meal solutions that require minimal preparation time, while maintaining nutritional value. Retailers and food service providers have responded by introducing a wide array of pre marinated, pre cooked, and packaged seafood products that simplify cooking processes. Products, such as seasoned salmon fillets, breaded shrimp, and sushi kits have become staples in supermarket aisles by appealing to consumers seeking quick and easy dinner options. The proliferation of online grocery shopping and home delivery services has further enhanced accessibility by allowing customers to purchase fresh and frozen seafood with ease. Major retail chains have invested in improved cold chain logistics to ensure product quality and freshness, building consumer trust in packaged offerings. Additionally, the influence of social media and culinary trends has popularized diverse seafood recipes, encouraging experimentation with convenient formats. The availability of single serve portions also aligns with the growing number of smaller households.

MARKET RESTRAINTS

High Perishability and Cold Chain Logistics Costs

The high perishability and the associated costs of maintaining cold chain logistics are impacting both profitability and accessibility, which is hindering the growth of United States seafood market. Seafood is highly susceptible to spoilage and bacterial growth if not kept at precise temperatures throughout the supply chain, from harvest to retail display. As per the Food and Agriculture Organization, approximately 35% of global fish production is lost or wasted due to inadequate handling and storage infrastructure. In the United States, the requirement for continuous refrigeration increases operational expenses for distributors, retailers, and restaurants, often resulting in higher retail prices that can deter price sensitive consumers. Maintaining strict temperature controls during transportation, especially for imported seafood traveling long distances, requires specialized equipment and monitoring systems, adding to the overall cost structure. Any breach in the cold chain can lead to product rejection and financial losses, creating risk aversion among suppliers. Furthermore, energy costs associated with refrigeration contribute to the carbon footprint of seafood products, raising environmental concerns. Small and medium sized enterprises often struggle to afford advanced cold chain technologies, limiting their market reach and competitiveness. The complexity of managing perishable inventory also leads to shrinkage and waste at the retail level, affecting profit margins. These logistical challenges restrict the geographic distribution of fresh seafood, particularly in inland regions, and limit the variety of species available to consumers.

Consumer Concerns Regarding Contaminants and Safety

The consumer concerns regarding contaminants and safety issues, influencing purchasing decisions and limiting consumption frequency is also degrading the growth of United States seafood market. Reports of mercury accumulation in certain fish species, such as tuna and swordfish, have raised health alarms, particularly among pregnant women and young children. As per the Environmental Protection Agency, advisories regarding mercury levels in fish have led to cautious consumption patterns among vulnerable populations. Additionally, incidents of seafood fraud, where cheaper species are mislabeled as premium varieties, have eroded consumer trust in product authenticity and quality. Concerns about antibiotic residues in farmed seafood and microplastic contamination also contribute to consumer hesitation. The lack of transparent sourcing information makes it difficult for buyers to verify the safety and origin of their purchases. Negative media coverage of pollution and unsafe farming practices further exacerbates these fears, leading some consumers to substitute seafood with other protein sources. Regulatory efforts to improve labeling and inspection protocols are ongoing, but perception gaps persist. The fear of foodborne illnesses from raw or undercooked seafood, such as oysters and sushi, also limits market potential in certain segments. Addressing these safety concerns through rigorous testing, clear labeling, and education is essential to rebuilding consumer confidence and removing this restraint on market growth.

MARKET OPPORTUNITIES

Growth of Sustainable Aquaculture and Domestic Production

The growth of sustainable aquaculture and domestic production to reduce import dependency and enhance supply security is certainly creating new opportunities for the growth of United States seafood market. Aquaculture, or fish farming, offers a controlled environment for producing seafood with consistent quality and reduced environmental impact compared to wild capture fisheries. As per the National Oceanic and Atmospheric Administration, the United States has vast potential for expanding offshore aquaculture, which could significantly boost domestic supply [[9]. Recent regulatory reforms and investment incentives aim to streamline permitting processes for offshore fish farms, encouraging private sector participation. Technologies such as recirculating aquaculture systems allow for land based farming with minimal water usage and waste discharge, addressing environmental concerns. Consumers are increasingly willing to pay a premium for locally sourced and sustainably certified seafood, creating a lucrative niche for domestic producers. Partnerships between technology firms and aquaculture operators are driving innovation in feed efficiency and disease management, improving productivity and profitability. The development of species such as cobia, yellowtail, and salmon in US waters diversifies the product offering and reduces pressure on wild stocks. This shift towards domestic production not only enhances food security but also aligns with consumer preferences for transparency and sustainability, offering a robust pathway for market expansion.

Integration of Blockchain for Supply Chain Transparency

The integration of blockchain technology for supply chain transparency to build consumer trust and combat fraud is also to enhance the growth of United States seafood market. Blockchain enables the creation of immutable digital records that track seafood from harvest to plate, providing verifiable information on origin, handling, and sustainability certifications. As per IBM Food Trust, pilot programs using blockchain have demonstrated significant improvements in traceability and reduced time required to identify source of contamination issues. Retailers and brands leveraging this technology can differentiate their products by offering proof of ethical sourcing and quality assurance, appealing to conscientious consumers. This transparency helps mitigate concerns regarding seafood fraud and illegal fishing, enhancing brand reputation and loyalty. Digital labels and QR codes allow customers to access detailed information about the journey of their seafood, fostering engagement and confidence. Regulatory bodies are increasingly supporting digital traceability initiatives to enforce compliance with safety and sustainability standards. The adoption of blockchain also streamlines logistics and reduces administrative burdens by automating documentation and verification processes. As technology costs decrease and interoperability improves, wider adoption becomes feasible for small and medium sized enterprises.

MARKET CHALLENGES

Impact of Climate Change on Fish Stocks and Habitat

The impact of climate change on fish stocks and habitat by threatening the stability and sustainability of wild capture fisheries is one of the key challenges for the growth of United States seafood market. Rising ocean temperatures, acidification, and changing current patterns are altering the distribution and abundance of marine species, disrupting traditional fishing grounds. As per the National Climate Assessment, many commercially important fish species are shifting northward or to deeper waters, making them less accessible to existing fleets . This migration affects catch volumes and economic viability for fishing communities, leading to uncertainty in supply chains. Extreme weather events, such as hurricanes and heatwaves, further damage coastal habitats like coral reefs and mangroves, which serve as critical nurseries for many species. The decline in biodiversity reduces the resilience of ecosystems by making them more vulnerable to overfishing and disease. Fisheries management strategies must adapt to these dynamic conditions, requiring updated scientific data and flexible regulatory frameworks. However, the pace of environmental change often outstrips the ability of management systems to respond effectively. The unpredictability of stock assessments complicates long term planning for processors and retailers. Additionally, the economic costs associated with adapting fishing practices and equipment to new conditions burden industry participants.

Regulatory Complexity and Compliance Burdens

The regulatory complexity and compliance burdens by imposing costly and time consuming requirements on industry participants is also to impede the growth of United States seafood market. Federal, state, and local regulations govern various aspects of seafood production, including harvesting limits, safety standards, labeling requirements, and environmental protections. As per the Small Business Administration, small fishing businesses often struggle to navigate the intricate web of regulations, facing high compliance costs and administrative hurdles. The Seafood Import Monitoring Program, designed to prevent illegal, unreported, and unregulated fishing, requires extensive data collection and reporting from importers, increasing operational overhead. Changes in trade policies and tariffs further complicate international supply chains, affecting pricing and availability. Compliance with food safety regulations enforced by the Food and Drug Administration necessitates rigorous testing and documentation, particularly for imported products. The lack of harmonization between different regulatory jurisdictions creates inconsistencies and inefficiencies, hindering market access for smaller players. Additionally, evolving sustainability certifications and eco labeling schemes add another layer of complexity, requiring continuous monitoring and verification. These regulatory pressures can stifle innovation and discourage new entrants, limiting market dynamism. Industry stakeholders advocate for streamlined processes and greater clarity in regulations to reduce burdens while maintaining safety and sustainability goals.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 1.82% |

| Segments Covered | By Type, Form, Distribution Channel and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, and the Rest of the United States. |

| Key Market Players | Trident Seafoods, American Seafoods Group, Bumble Bee Foods, Chicken of the Sea, StarKist Co., High Liner Foods, Pacific Seafood, Phillips Foods, Inc., Beaver Street Fisheries, and Sysco Corporation. |

SEGMENTAL ANALYSIS

By Type Insights

The fish segment was the largest by holding 23.4% of the United States seafood market share in 2025 with the immense popularity of salmon and tuna among American consumers. These species are favored for their versatility, mild flavor profiles, and recognized health benefits, particularly their high omega 3 fatty acid content. As per the National Oceanic and Atmospheric Administration, salmon remained the most consumed seafood item in the United States in 2024, with per capita consumption reaching approximately 2.9 pounds. This consistent demand is supported by widespread availability in both fresh and frozen forms across retail and food service channels. Tuna follows closely, benefiting from its staple status in canned formats and growing popularity in sushi and sashimi preparations. The Dietary Guidelines for Americans emphasize the importance of varying protein sources, encouraging regular fish consumption to reduce heart disease risk. This nutritional endorsement reinforces consumer preference for fish over other seafood types. Additionally, the expansion of aquaculture has stabilized the supply of Atlantic salmon, ensuring year round availability and price stability. Retailers prioritize shelf space for popular fish varieties, further cementing their market dominance. The cultural integration of fish into diverse cuisines, from Mediterranean to Asian, broadens its appeal across demographic groups.

The shrimps segment is likely to grow at an anticipated CAGR of 12.4% from 2025 to 2034 with the rising popularity of convenience foods and snacking culture. Shrimp is perceived as an easy to prepare protein that cooks quickly and pairs well with various flavors, making it ideal for busy households. The proliferation of pre peeled, deveined, and cooked shrimp in retail stores has lowered the barrier to entry for consumers, who may find whole shrimp intimidating to prepare. Snackable shrimp formats, such as shrimp chips and dried shrimp snacks, are gaining traction among health conscious individuals seeking low calorie, high protein alternatives to traditional snacks. Social media trends showcasing quick shrimp recipes have further amplified interest, encouraging trial and repeat purchases. The versatility of shrimp in appetizers, salads, and main courses allows it to fit seamlessly into diverse meal occasions. Additionally, the growth of ethnic cuisines, particularly Thai, Vietnamese, and Cajun, which heavily feature shrimp, has expanded its consumer base. Retail promotions and bundle offers often highlight shrimp as a premium yet accessible option, driving volume growth.

By Form Insights

The frozen and canned form segment was accounted in holding a dominant share of the United States seafood market in 2025 due to its extended shelf life and ability to reduce food waste. Freezing and canning preserve the nutritional value and quality of seafood by allowing consumers to store products for long periods without spoilage. This format enables retailers to manage inventory more effectively, minimizing losses from perishability. Consumers appreciate the convenience of having seafood available on demand, regardless of seasonal availability or geographic location. Canned tuna and salmon remain pantry staples by offering affordable and nutritious meal options that require no refrigeration until opened. The development of advanced freezing technologies, such as flash freezing, ensures that texture and flavor are retained, addressing historical concerns about quality degradation. Emergency preparedness trends have also boosted demand for non-perishable seafood items, as households stockpile essentials. The consistency of supply for frozen and canned products allows manufacturers to plan production efficiently, maintaining stable prices. This reliability makes frozen and canned seafood a trusted choice for budget conscious families and institutions. The reduction in food waste aligns with sustainability goals by enhancing the appeal of these forms to environmentally aware consumers.

The processed seafood segment is esteemed to grow at an anticipated CAGR of 8.6% from 2026 to 2034 with the increasing demand for ready to eat and value-added products. Modern consumers prioritize convenience and time saving solutions, leading to higher sales of pre marinated, breaded, and fully cooked seafood items. Products such as crab cakes, fish sticks, and smoked salmon slices offer immediate consumption or minimal preparation, appealing to working professionals and families. Innovation in flavor profiles and packaging has enhanced the appeal of processed seafood, attracting younger demographics interested in global cuisines. The rise of meal kit services has also contributed to this growth, providing portion controlled and seasoned seafood ingredients that simplify cooking. Retailers are expanding their deli and prepared food sections to include high quality seafood options, catering to impulse buyers. Health focused processed products, such as low sodium canned fish and grilled chicken style tuna, address dietary concerns while offering convenience. The perception of processed seafood as a premium and sophisticated choice has shifted, with artisanal and gourmet options gaining popularity. This evolution in consumer preferences ensures that the processed segment continues to expand rapidly, capturing market share from traditional forms.

By Distribution Channel Insights

The off trade channel segment was the largest by holding 42.6% of the United States seafood market share in 2025 with the dominance of retail grocery and supermarket chains where consumers purchase seafood for home consumption. Major retailers such as Walmart, Kroger, and Costco offer extensive seafood selections, ranging from fresh counter service to frozen aisles, providing convenience and variety. The expansion of private label seafood brands has enhanced value propositions, attracting budget conscious shoppers. Retailers invest in improved display cases and staff training to ensure product quality and customer satisfaction. Loyalty programs and digital coupons incentivize repeat purchases, strengthening customer retention. The availability of online grocery shopping and curbside pickup options has further boosted off trade sales, allowing consumers to buy seafood with ease. Promotional events, such as seafood festivals and weekly specials, drive traffic and volume. The trust established by reputable retail brands assures consumers of safety and quality standards. Additionally, the integration of recipe ideas and cooking tips in store and online enhances the shopping experience, encouraging experimentation.

The on trade channel segment is expected to register a fastest CAGR of 9.2% from 2026 to 2034 with the robust recovery of the hospitality industry and renewed consumer interest in dining out. Restaurants, hotels, and catering services have seen a surge in patronage as social restrictions ease and consumers seek experiential dining. Consumers are willing to pay higher prices for professionally prepared seafood dishes, such as lobster tails and oyster platters, which are difficult to replicate at home. The rise of food tourism and culinary exploration encourages visits to specialized seafood establishments. Hotel buffets and banquet services have also rebounded, driving bulk purchases of seafood ingredients. The emphasis on fresh, high quality ingredients in menu descriptions attracts discerning diners. Chef driven concepts featuring sustainable and locally sourced seafood enhance the appeal of on trade venues. Marketing campaigns promoting date nights and group gatherings further stimulate demand. The integration of seafood into happy hour menus and appetizer offerings increases frequency of visits.

COMPETITIVE LANDSCAPE

The competition in the United States seafood market is intense and fragmented characterized by a mix of large multinational corporations and regional processors vying for consumer attention. Major players leverage economies of scale and global sourcing networks to offer competitive pricing and consistent product availability. Brand recognition and trust play crucial roles as consumers increasingly prioritize sustainability and safety in their purchasing decisions. Private label brands from major retailers pose significant competition by offering lower priced alternatives that appeal to budget conscious shoppers. Innovation in product formats such as ready to cook meals and sustainable packaging helps companies differentiate themselves in crowded retail aisles. The rise of e commerce has intensified competition by enabling direct to consumer sales and broader market access for niche brands. Regulatory compliance regarding labeling and sourcing adds complexity requiring robust quality control systems. Companies must navigate fluctuating raw material costs and supply chain disruptions while maintaining profitability. Strategic alliances and vertical integration are common tactics to secure supply and reduce risks. The focus on health and wellness drives demand for premium and organic options creating opportunities for specialized producers. Adapting to changing consumer preferences and technological advancements is essential for sustaining competitive advantage in this dynamic industry.

KEY MARKET PLAYERS

A few of the major companies in the U.S. seafood market include

- Trident Seafoods

- American Seafoods Group

- Bumble Bee Foods

- Chicken of the Sea

- StarKist Co.

- High Liner Foods

- Pacific Seafood

- Phillips Foods, Inc.

- Beaver Street Fisheries

- Sysco Corporation

Top Players in the US Seafood Market

Thai Union Group PCL

Thai Union Group PCL operates as a global leader in sustainable seafood with a significant presence in the United States market through its diverse portfolio of brands. The company supplies canned tuna, shrimp, and value added products to major retailers and food service providers across North America. Recent actions include expanding its plant based seafood alternatives under the Plantish brand to cater to evolving consumer preferences for sustainable protein sources. Thai Union actively invests in digital traceability systems to enhance supply chain transparency and build consumer trust. The company strengthens its market position by partnering with local distributors and enhancing its cold chain logistics capabilities. Its commitment to environmental stewardship and social responsibility aligns with regulatory standards and consumer expectations. These strategic initiatives ensure consistent product quality and availability while reinforcing its reputation as a responsible industry leader in the competitive United States seafood landscape.

Maruha Nichiro Corporation

Maruha Nichiro Corporation is a prominent Japanese seafood conglomerate with extensive operations in the United States market focusing on processed and frozen seafood products. The company provides a wide range of items including surimi, canned fish, and ready to eat meals to retail and industrial clients. Recent strategies involve investing in advanced processing facilities in North America to improve efficiency and reduce lead times for domestic customers. Maruha Nichiro emphasizes innovation in product development by introducing health oriented seafood options that appeal to nutrition conscious consumers. The company leverages its global sourcing network to ensure stable supply and competitive pricing despite market volatility.

High Liner Foods Incorporated

High Liner Foods Incorporated stands as a leading processor and marketer of value added seafood products in North America with a strong footprint in the United States. The company offers a diverse array of frozen and fresh seafood items under well recognized brands such as Gorton’s and Fisher Boy. Recent actions include optimizing its manufacturing operations to enhance productivity and reduce environmental impact through energy efficient technologies. High Liner Foods focuses on expanding its portfolio of convenient and healthy seafood solutions to meet the demands of busy consumers. The company invests in marketing campaigns that highlight the nutritional benefits and culinary versatility of its products. Its dedication to sustainable sourcing and operational excellence ensures consistent quality and reliability for customers across the United States market.

Top Strategies Used by Key Market Participants

Key players in the United States seafood market primarily focus on sustainability and traceability to build consumer trust and comply with regulatory standards. Companies invest in certified sourcing programs and blockchain technology to ensure transparent supply chains from ocean to plate. Another major strategy involves product innovation particularly in value added and ready to eat formats to meet demand for convenience. Manufacturers expand their portfolios to include plant based alternatives and health focused options appealing to diverse dietary preferences. Strategic partnerships with retailers and food service providers enhance distribution networks and market reach. Investment in advanced processing technologies improves efficiency and reduces waste while maintaining product quality. These approaches help participants differentiate their offerings and capture value in a competitive and evolving marketplace.

MARKET SEGMENTATION

This research report on the U.S. seafood market has been segmented based on the following categories.

By Type

- Fish

- Shrimps

- Others

By Form

- Fresh/Chilled

- Frozen/Canned

- Processed

By Distribution Channel

- Off Trade

- On Trade

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com