U.S. Soup Market Size, Share, Trends, and Growth Analysis Report, Segmented by Type, Distribution Channel, and Country – Industry Forecast From 2026 to 2034

U.S. Soup Market Report Summary

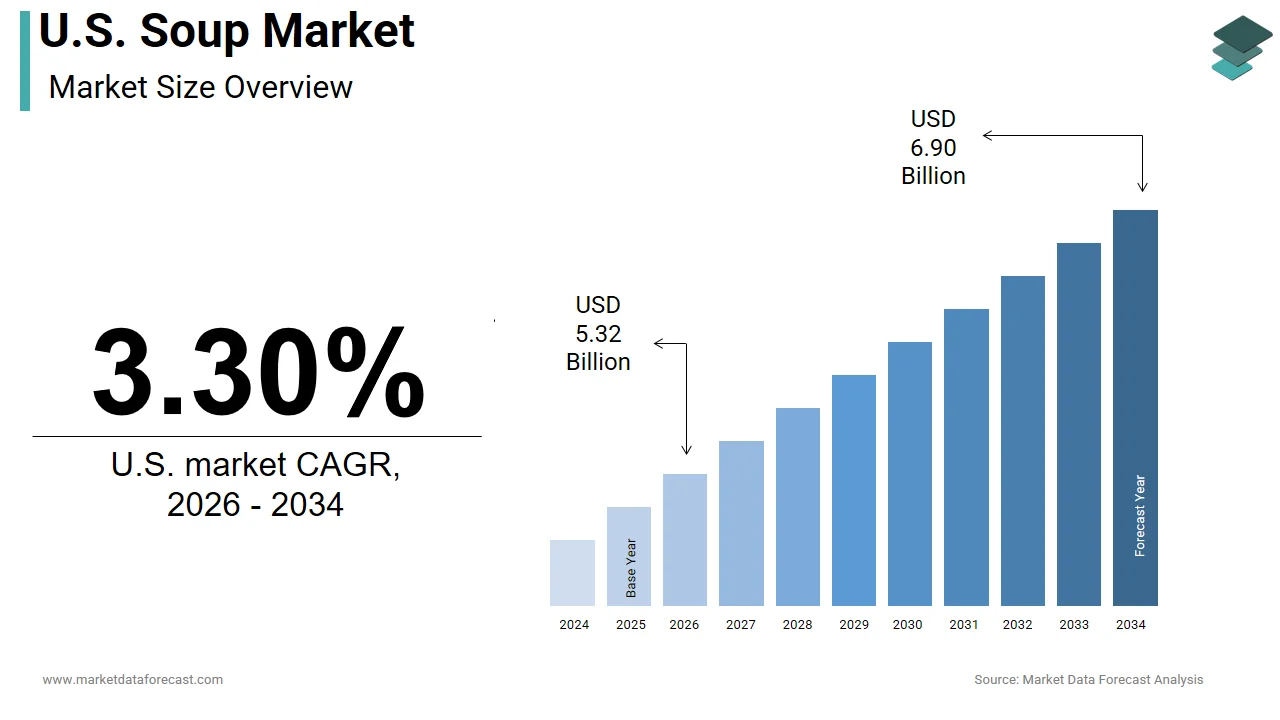

The U.S. soup market was valued at USD 5.15 billion in 2025, is estimated to reach USD 5.32 billion in 2026, and is projected to reach USD 6.90 billion by 2034, growing at a CAGR of 3.30% from 2026 to 2034. Market growth is driven by increasing demand for convenient, ready-to-eat meals and evolving consumer preferences toward healthier and premium soup options. The market benefits from strong retail distribution, product innovation, and the introduction of organic, low-sodium, and functional soups. However, changing dietary habits and competition from fresh and frozen alternatives slightly moderate growth.

Key Market Trends

- Rising demand for convenient and ready-to-eat food products.

- Growing interest in healthy, organic, and low-sodium soups.

- Expansion of premium and gourmet soup offerings.

- Strong presence of retail and supermarket distribution channels.

- Increasing focus on clean-label and functional ingredients.

Segmental Insights

- Based on type, the canned soup segment dominated the United States market in 2025, driven by its long shelf life and strong presence as a pantry staple.

- Based on distribution channel, the hypermarkets and supermarkets segment led the market in 2025, supported by wide product availability and consumer accessibility.

Country-Level Insights

- The United States dominated the North American soup market by holding 90.8% share in 2025, driven by high market maturity, extensive product diversity, and strong brand recognition. The country continues to lead due to its well-established food processing industry and evolving consumer preferences.

Competitive Landscape

The U.S. soup market is competitive, with major players focusing on product innovation, health-oriented offerings, and expanding distribution networks. Companies are introducing new flavors, clean-label products, and convenient packaging formats to attract consumers.

Prominent companies operating in the U.S. soup market include The Campbell Soup Company, Nestlé S.A., Baxters Food Group Limited, General Mills, Inc., Conagra Brands, Inc., Premier Foods Group Limited, The Kraft Heinz Company, Hindustan Unilever Limited, Ottogi Co., Ltd., and Associated British Foods plc.

U.S. Soup Market Size

The U.S. soup market stood at USD 5.15 billion in 2025, is projected to reach USD 5.32 billion in 2026, and is estimated to grow to USD 6.90 billion by 2034, expanding at a CAGR of 3.30% from 2026 to 2034.

Soup is defined as a primarily liquid food generally served warm or hot, made by combining ingredients such as meat and vegetables with stock, juice, water, or another liquid. This sector serves as a staple in American households due to its convenience, affordability, and perceived nutritional value. According to the USDA Economic Research Service (2025), per capita availability of processing vegetables stood at 95.6 pounds in 2024, down 8 percent from the previous year. This reflects a long-term downward trend in processed vegetable consumption, which now accounts for approximately 25% of total U.S. vegetable availability. The market is characterized by a shift from traditional high-sodium canned options toward healthier, clean-label, and premium alternatives. As per the National Association of Convenience Stores (2024), foodservice and prepared foods have become primary growth drivers for the industry, though high-impulse purchases remain dominated by snack and beverage categories rather than specific meal solutions like soup. Consumer preferences are increasingly influenced by dietary trends such as gluten-free, organic, and plant-based diets. The industry faces pressure to reduce sodium content while maintaining flavor profiles that appeal to diverse palates. Innovation in packaging formats such as microwavable bowls and single-serve cups has enhanced product accessibility. The market also benefits from the versatility of soup as both a standalone meal and a complementary side dish. Seasonal fluctuations influence sales volumes, with higher demand observed during colder months. This dynamic landscape requires manufacturers to balance tradition with innovation to meet changing consumer expectations.

MARKET DRIVERS

Increasing Demand for Convenient and Ready-to-Eat Meals

The increasing demand for convenient and ready-to-eat meals serves as a key growth enabler for the United States soup market. Consumers are actively seeking these time-saving solutions for daily nutrition. Busy lifestyles and dual-income households have reduced the time available for meal preparation, leading to a reliance on quick and easy food options. According to the Bureau of Labor Statistics (2025), the average American aged 15 and older spends 40 minutes per day on food preparation and cleanup, a figure that has risen from approximately 34 minutes per day a decade ago. Soup offers a complete meal solution that requires minimal effort, often needing only heating before consumption. The availability of microwavable containers and single-serve portions further enhances convenience for workers and students. Retailers have expanded their ready-to-eat sections to include a wider variety of soup flavors and types, catering to diverse dietary preferences. The rise of remote work has also influenced eating habits, with individuals seeking quick lunch options that can be prepared at home. Soup brands are responding by launching products with bold flavors and premium ingredients to attract discerning consumers. This trend toward convenience ensures that soup remains a relevant and popular choice for modern Americans seeking efficient meal solutions.

Growing Health Consciousness and Functional Food Trends

Increasing health consciousness and the trend toward functional foods significantly drive the United States soup market. This growth encourages consumers to choose nutritious and beneficial options. Shoppers are increasingly aware of the importance of diet in maintaining overall health, leading to a preference for soups rich in vegetables, lean proteins, and essential nutrients. According to the International Food Information Council, a majority of consumers are actively trying to consume more vegetables and fruits, which are primary ingredients in many soup varieties. As per the Centers for Disease Control and Prevention, chronic diseases such as heart disease and diabetes are linked to poor dietary habits, prompting individuals to seek healthier alternatives to processed foods. Soup brands are reformulating products to reduce sodium, eliminate artificial preservatives, and incorporate organic ingredients to meet these health demands. The inclusion of functional ingredients such as turmeric, ginger, and probiotics appeals to consumers seeking immune support and digestive health benefits. Plant-based and vegan soups are gaining popularity among those adopting flexible or strictly plant-based diets. Retailers are highlighting health claims on packaging to attract attention from wellness-oriented shoppers. The perception of soup as a comforting yet healthy meal option supports its continued growth. This alignment with health and wellness trends ensures that the soup market remains vibrant and responsive to consumer needs.

MARKET RESTRAINTS

High Sodium Content and Health Concerns

High sodium content in traditional soup products acts as a major restraint on the United States soup market. This is because health-conscious consumers seek to limit their salt intake. Excessive sodium consumption is linked to high blood pressure and cardiovascular issues, leading to increased scrutiny of processed food labels. According to the American Heart Association (2024), while the recommended daily limit is 2,300 mg (with an ideal limit of 1,500 mg for most adults), a single serving of many popular canned soups contains approximately 800 mg to 900 mg of sodium, accounting for nearly 40% of the daily maximum. As per the FDA, sodium reduction is a key public health goal, and manufacturers face pressure to reformulate products to meet lower sodium standards. However, reducing salt can impact flavor and preservation, posing technical challenges for producers. Consumers often perceive canned soups as unhealthy due to their high sodium levels, leading them to choose fresh or homemade alternatives. The presence of warning labels or negative media coverage regarding processed food health risks further dampens demand. While low-sodium options are available, they often command higher prices and may not match the taste profile of traditional varieties. This health concern restricts the market potential for standard canned soups, forcing companies to invest in research and development to create healthier formulations. Sodium levels must be significantly reduced without compromising quality. Until then, this restraint will continue to impact consumer purchasing decisions.

Perception of Processed Foods and Clean Label Demands

The negative perception of processed foods and the growing demand for clean label products constrain the United States soup market. This shifts consumer preference toward fresh and minimally processed alternatives. Many shoppers associate canned and dried soups with artificial additives, preservatives, and lower nutritional value compared to fresh options. According to the Clean Label Project, consumers are increasingly scrutinizing ingredient lists for recognizable and natural components, avoiding products with long lists of chemical additives. Soup manufacturers face the challenge of removing artificial ingredients while maintaining shelf stability and flavor consistency. The rise of fresh soup bars and refrigerated soup sections in grocery stores offers a perceived healthier alternative, drawing customers away from shelf-stable products. The cost of producing clean-label soups is often higher, which can result in increased retail prices that deter price-sensitive consumers. Marketing efforts to educate consumers about the safety and quality of preserved soups have had limited success in changing deep-seated perceptions. This shift toward fresh and natural foods limits the growth potential of conventional soup categories, requiring industry participants to innovate and adapt to changing consumer values.

MARKET OPPORTUNITIES

Expansion of Plant-Based and Vegan Soup Varieties

The expansion of plant-based and vegan soup varieties creates a major opportunity for the United States soup market. This caters to the growing number of consumers adopting flexible or strict plant-based diets. The demand for meat-free options is driven by health, environmental, and ethical concerns, creating a robust market for vegetable, legume, and grain-based soups. According to the Plant Based Foods Association (2024), while the plant-based food market reached $8.1 billion in sales, growth is primarily driven by the milk and meat categories; plant-based soups currently represent a smaller, niche segment within the broader "prepared meals" category. As per sources, menu items featuring plant-based ingredients are increasing in popularity across foodservice channels, influencing retail trends. Manufacturers are developing innovative recipes that use ingredients such as lentils, chickpeas, and quinoa to provide protein and texture without animal products. The versatility of plant-based soups allows for diverse flavor profiles ranging from spicy Asian inspired broths to hearty Mediterranean stews. Retailers are dedicating more shelf space to vegan options, recognizing their potential for growth. Marketing campaigns that highlight the sustainability and health benefits of plant-based diets further drive consumer interest. The ability to appeal to both vegans and flexitarians expands the target audience for these products. By investing in plant-based innovation, soup brands can capture new market share and differentiate themselves in a competitive landscape. This trend aligns with broader societal shifts toward sustainable and humane food consumption.

Innovation in Premium and Artisanal Soup Products

Innovation in premium and artisanal soup products offers a lucrative potential for the United States soup market. Such offerings appeal directly to consumers looking for high-quality, unique culinary experiences. There is a rising interest in gourmet flavors, exotic ingredients, and small-batch production methods that distinguish premium soups from mass market offerings. According to the Specialty Food Association, specialty foods, including artisanal soups, continue to outpace general food sales in terms of value growth. Brands are launching limited-edition flavors and regional specialties to attract food enthusiasts and explorers. Packaging innovations such as glass jars and eco-friendly materials enhance the perceived value of these products. Collaborations with celebrity chefs and local farmers create storytelling opportunities that resonate with buyers seeking authenticity. The rise of e-commerce platforms allows niche brands to reach national audiences without relying on traditional retail distribution. Subscription services for gourmet soup deliveries provide recurring revenue streams and build customer loyalty. By focusing on quality and uniqueness, manufacturers can command higher margins and build strong brand identities. This premiumization trend ensures that the soup market remains dynamic and responsive to evolving culinary preferences.

MARKET CHALLENGES

Supply Chain Volatility and Ingredient Cost Fluctuations

Supply chain volatility and ingredient cost fluctuations are a serious limitation to the United States soup market. This impacts production costs and pricing stability. The soup industry relies on a wide range of agricultural inputs, including vegetables, grains, and meats, which are subject to price variations due to weather conditions, labor shortages, and geopolitical events. According to the USDA Economic Research Service, food price inflation has remained elevated in recent years, driven by increased costs for raw materials and transportation. As per the Bureau of Labor Statistics, the producer price index for processed foods has risen significantly, squeezing profit margins for manufacturers. These cost pressures often force companies to raise retail prices, which can dampen consumer demand, particularly among budget-conscious shoppers. Disruptions in the supply chain can also lead to shortages of key ingredients, affecting product availability and consistency. The reliance on global sourcing for certain spices and additives adds complexity and risk to procurement processes. Manufacturers must navigate these uncertainties by diversifying suppliers and implementing hedging strategies, which require significant resources. The inability to fully pass on cost increases to consumers limits profitability and investment in innovation. This economic instability creates a challenging environment for sustained growth and operational efficiency in the soup market.

Intense Competition and Private Label Growth

Intense competition and the growth of private-label brands are significant challenges to the United States soup market. They erode brand loyalty and pressure pricing strategies. The market is saturated with numerous national brands and store brands offering similar products, making it difficult for individual companies to differentiate themselves. According to research, private label sales in the soup category have grown steadily as retailers enhance the quality and variety of their own-brand offerings, capturing increased market share from budget-conscious consumers. This trend forces national brands to invest heavily in marketing and promotion to maintain market share, increasing operational costs. The ease of entry for new artisanal and niche brands further fragments the market, diluting the dominance of established players. Retailers leverage their shelf space to promote private label products, often placing them alongside or instead of national brands. The pressure to compete on price while maintaining quality margins is a constant struggle for manufacturers. Brand loyalty is declining as consumers become more willing to switch brands based on price and convenience. This competitive landscape requires continuous innovation and strategic positioning to sustain relevance and profitability in a crowded marketplace.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Distribution Channel, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled |

|

SEGMENTAL ANALYSIS

By Type Insights

The canned soup segment dominated the United States soup market in 2025. Its exceptional shelf stability and entrenched status as a pantry staple in American households support the dominance of this segment. The ability of canned soups to remain safe and edible for extended periods without refrigeration makes them an essential component of emergency preparedness and long-term food storage. According to FMI – The Food Industry Association (2024), shelf-stable canned goods remain a foundational purchase during economic uncertainty, providing a consistent baseline of demand as consumers prioritize long shelf life and value. The durability of metal packaging protects the product from light and oxygen, preserving nutritional value and flavor integrity over time. This reliability appeals to budget-conscious consumers who prioritize minimizing food waste and maximizing value. Retailers benefit from the low logistical costs associated with storing non-perishable goods, allowing for widespread distribution even in remote areas. The convenience of having a ready-to-heat meal available at all times supports the busy lifestyles of modern families. Furthermore, the wide variety of flavors available in canned formats ensures that there is an option for every taste preference. This combination of practicality, affordability, and availability solidifies canned soup as the leading segment in the market. The cost efficiency and broad retail accessibility of canned soup significantly drive its market domination by making it an affordable meal option for diverse demographic groups. Canned soups are generally priced lower than fresh or frozen alternatives due to economies of scale in production and lower transportation costs. According to the Bureau of Labor Statistics, the price per serving of canned soup remains competitive compared to other prepared meals, attracting price-sensitive shoppers. The widespread presence of canned soups in various retail channels, including grocery stores, discount retailers, and convenience stores, ensures that consumers can easily access these products. Major brands invest heavily in supply chain optimization to keep costs low while maintaining consistent quality. The ability to purchase in bulk during promotional periods allows households to stock up and save money. This economic advantage is particularly important for students from low-income families and individuals seeking quick meal solutions without breaking the bank. The standardized packaging also facilitates efficient shelving and inventory management for retailers. These factors combine to make canned soup a ubiquitous and indispensable part of the American diet.

The chilled soup segment is on the rise and is expected to be the fastest-growing segment in the market due to increasing consumer demand for freshness and premium quality perceptions. Shoppers are increasingly wary of preservatives and artificial additives commonly found in canned varieties, leading them to seek refrigerated options that offer cleaner labels. According to the Specialty Food Association, sales of fresh and chilled foods have outpaced those of shelf-stable counterparts, reflecting a shift toward perceived healthier choices. The use of fresh vegetables, herbs, and high-quality proteins in chilled soups appeals to health-conscious individuals who prioritize nutrition and flavor. Retailers have expanded their refrigerated sections to accommodate a wider variety of chilled soup brands, enhancing visibility and accessibility. The shorter shelf life of chilled soups implies fresher ingredients and less processing, which resonates with the clean eating movement. Marketing campaigns emphasize the farm-to-table aspect of these products, building trust and loyalty among discerning buyers. The growth of meal kit services has also familiarized consumers with fresh prepared meals, encouraging trial of chilled soups. This trend toward premiumization and freshness ensures that the chilled segment continues to expand rapidly. The convenience of ready-to-eat formats is a key driver accelerating the growth of the chilled soup segment. Unlike canned soups that often require heating and preparation, chilled soups are frequently designed to be consumed cold or warmed quickly in microwavable containers. According to the National Restaurant Association, the demand for grab-and-go meals has surged, with chilled soups fitting seamlessly into this category. The packaging innovations, such as leak-proof lids and ergonomic designs, enhance portability and ease of consumption. Retailers place chilled soups near deli counters and salad bars, creating convenient meal bundles for shoppers. The ability to enjoy a nutritious meal without the hassle of cooking aligns with the busy lifestyles of urban consumers. Foodservice providers are also incorporating chilled soups into their menus, offering them as healthy sides or light mains. The versatility of chilled soups in both retail and foodservice channels supports their rapid adoption. This focus on convenience and immediacy ensures that chilled soups remain a dynamic and high-growth segment in the market.

By Distribution Channel Insights

The hypermarkets and supermarkets led the US soup market in 2025. This leading position of the segment is attributed to the one-stop shopping convenience and wide product assortment they offer. Consumers prefer these large-format stores for their ability to purchase groceries, household items, and fresh produce in a single trip. The ability to compare prices and flavors side by side enhances the shopping experience and encourages impulse buys. Promotional activities such as weekly discounts and loyalty programs drive traffic and volume sales. Supermarkets also offer private label options that compete effectively with national brands, providing value to budget-conscious shoppers. The strategic placement of soups in aisles near bread crackers and dairy products increases visibility and cross-category sales. The trust established through consistent quality and service reinforces customer loyalty. This comprehensive approach to retailing ensures that hypermarkets and supermarkets remain the dominant channel for soup distribution. The strong supply chain infrastructure and advanced inventory management capabilities of hypermarkets and supermarkets significantly contribute to their market leadership. These retailers have established robust logistics networks that ensure consistent stock levels and timely replenishment of soup products. This reliability builds consumer confidence and encourages repeat purchases. The ability to handle large volumes of goods allows supermarkets to negotiate favorable terms with suppliers, resulting in competitive pricing. Advanced warehousing and distribution centers enable rapid turnover of perishable chilled soups while maintaining quality standards. The integration of technology in store operations enhances the shopping experience through self-checkout and mobile apps. These operational efficiencies support the dominance of hypermarkets and supermarkets in the soup market. The capacity to manage complex product portfolios ensures that consumers have access to a diverse range of soup options year-round.

The online retail segment is the fastest-growing distribution channel in the US soup market, owing to the rapid expansion of e-commerce grocery services. The convenience of ordering groceries online and having them delivered to the doorstep has attracted a broad demographic, including busy professionals and elderly consumers. The ability to browse extensive selections, read reviews, and compare prices without leaving home enhances the shopping experience. Online platforms often provide detailed nutritional information and ingredient lists appealing to health-conscious shoppers. The integration of subscription services for regular deliveries of staple items like soup ensures consistent revenue streams for retailers. Mobile applications facilitate easy reordering and personalized recommendations, driving engagement and loyalty. The improvement in last-mile delivery logistics ensures that products arrive in good condition, building trust in online purchasing. This digital transformation allows retailers to reach customers beyond their geographic footprint, expanding market potential. Digital marketing and personalized recommendations are critical factors fueling the rapid growth of the online retail channel for soup. E-commerce platforms leverage data analytics to understand consumer preferences and tailor marketing efforts accordingly. Algorithms suggest complementary products, such as crackers or salads, enhancing basket size. The ability to offer exclusive online deals and bundles attracts price-sensitive shoppers. User-generated content, such as ratings and reviews, builds social proof and encourages trial of new brands. Online retailers also provide educational content such as recipes and cooking tips, engaging consumers and fostering brand loyalty. The seamless integration of payment and delivery options simplifies the purchasing process, reducing friction. These technological advantages create a superior shopping experience that traditional retail channels struggle to match. The continuous innovation in digital tools ensures that online retail remains a dynamic and rapidly expanding channel for soup sales.

COUNTRY LEVEL ANALYSIS

The United States outperformed other countries in the North American soup market and occupied a 90.8% share in 2025. This supremacy of the US market is driven by high maturity, extensive product diversity, and strong brand recognition. According to the USDA Economic Research Service (2025) and academic studies (2024), ultra-processed food staples, including canned and instant soups, dominate the U.S. diet and contribute to the country having one of the highest global intakes of ultra-processed foods, fueled by a consumer culture prioritizing convenience. The market benefits from a well-developed retail infrastructure and advanced supply chain capabilities that ensure widespread product availability. As per the National Association of Convenience Stores (2024-2025), foodservice has become the leading driver of inside-store growth and profit margins, with prepared and grab-and-go food options reflecting the American consumer's demand for immediate consumption and speed of service. Consumer preferences are shifting toward healthier and premium options, prompting manufacturers to innovate and reformulate products. The presence of major multinational food companies fosters intense competition and drives continuous improvement in quality and variety. Regulatory standards enforced by the FDA ensure food safety and labeling accuracy, maintaining consumer trust. The country also leads in trends such as plant-based and organic soups, influencing global market dynamics. Investment in sustainable packaging and sourcing practices addresses environmental concerns and enhances brand reputation. The robust economic foundation and high disposable income support demand for premium and artisanal soup products. This combination of scale innovation and consumer sophistication ensures that the United States remains the central pillar of the global soup industry.

COMPETITIVE LANDSCAPE

The competition in the United States soup market is intense and characterized by the dominance of established legacy brands alongside emerging niche players. Major companies compete based on brand recognition, product quality, price, and distribution efficiency to secure shelf space and consumer loyalty. The market sees frequent innovation as companies strive to differentiate their offerings through unique flavors, health benefits, and sustainable packaging. Private label brands pose a significant challenge to national brands by offering lower-priced alternatives that appeal to budget-conscious shoppers. Artisanal and organic soup makers contribute to market diversity by catering to niche segments seeking high-quality and authentic products. Consolidation through mergers and acquisitions is common as larger firms seek to expand their portfolios and achieve economies of scale. Regulatory compliance and food safety standards also influence competitive dynamics, requiring continuous investment in quality assurance. The rise of health and wellness trends drives demand for low-sodium and plant-based options, prompting reformulation efforts. This dynamic landscape requires agility and strategic foresight to navigate changing preferences and maintain market relevance effectively.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. soup market include

- The Campbell Soup Company

- Nestlé S.A

- Baxters Food Group Limited

- General Mills, Inc

- Conagra Brands, Inc.

- Premier Foods Group Limited

- The Kraft Heinz Company

- Hindustan Unilever Limited

- Ottogi Co., Ltd

- Associated British Foods plc

TOP PLAYERS IN THE MARKET

- The Campbell Soup Company is a global leader in the soup industry with a dominant presence in the United States market. The company offers a diverse portfolio of condensed, ready-to-eat, and broth products under iconic brands. Campbell leverages its extensive distribution network to ensure widespread availability across retail and foodservice channels. Recent actions include the divestiture of non-core assets to focus on core meal solutions and snacking categories. The company has invested heavily in product innovation, launching organic low-sodium and plant-based options to meet evolving consumer preferences. Campbell also emphasizes sustainability initiatives such as responsible sourcing and reduced packaging waste. These strategic moves strengthen its market position by enhancing brand relevance and operational efficiency. The organization continues to prioritize digital marketing and direct-to-consumer engagement to build loyalty. This comprehensive approach ensures Campbell remains a key influencer in the global soup landscape.

- General Mills Inc is a major multinational food company with a significant footprint in the United States soup market through its Progresso and other brands. The company focuses on delivering high-quality, convenient meal solutions that cater to diverse dietary needs. General Mills utilizes its robust research and development capabilities to innovate flavors and formats that appeal to modern consumers. Recent actions involve expanding its portfolio of clean-label and organic soups to address health-conscious trends. The company has also enhanced its supply chain resilience to mitigate disruptions and ensure consistent product availability. General Mills prioritizes sustainable agriculture practices, supporting farmers who supply key ingredients. These efforts reinforce its reputation for quality and responsibility among suppliers and customers. The integration of advanced data analytics allows for better demand forecasting and inventory management. By focusing on innovation and sustainability, General Mills solidifies its competitive edge in the dynamic soup market.

- Conagra Brands Inc is a leading packaged food company with a strong presence in the United States soup sector through brands like Healthy Choice and Chef Boyardee. The company provides a wide range of frozen and shelf-stable soup options that emphasize convenience and nutrition. Conagra is known for its commitment to making food more accessible and affordable for consumers. Recent actions include the reformulation of products to reduce sodium and artificial ingredients, aligning with health trends. The company has invested in marketing campaigns that highlight the versatility and ease of preparation of its soup products. Conagra also focuses on digital transformation to enhance customer engagement and e-commerce capabilities. These initiatives strengthen its market position by improving brand perception and reaching new audiences. The organization continues to explore partnerships with retailers to expand shelf space and visibility. By prioritizing innovation and accessibility, Conagra maintains its status as a trusted partner in the global soup industry.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States soup market employ several major strategies to maintain competitiveness and drive growth. Product innovation is central to these efforts, with companies developing healthy, organic, and plant-based options to meet changing consumer preferences. Strategic acquisitions allow firms to expand their portfolios and access niche markets with high growth potential. Sustainability initiatives such as eco-friendly packaging and responsible sourcing enhance brand reputation and comply with regulatory standards. Digital marketing and e-commerce integration help companies reach direct consumers and gather valuable data on purchasing behavior. Partnerships with foodservice providers ensure steady demand through menu inclusion and promotional activities. Cost optimization through supply chain efficiency and automation improves margins and operational resilience. These combined strategies enable participants to adapt to market dynamics and sustain long-term profitability in a highly competitive environment.

MARKET SEGMENTATION

This research report on the U.S. soup market has been segmented and sub-segmented into the following categories.

By Type

- Instant

- Canned

- Dehydrated

- Chilled

- Others

By Distribution Channel

- Hypermarket/Supermarket

- Convenience Stores

- Online Retail

- Others

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

What is the U.S. soup market?

The U.S. soup market offers canned, ready-to-eat, and instant soups for quick meals, comfort food, and health-conscious consumers nationwide.

How does the U.S. soup market function?

The U.S. soup market functions through manufacturers, retailers, and brands distributing diverse soup products via grocery stores and online channels.

What drives growth in the U.S. soup market?

The U.S. soup market grows due to busy lifestyles, health awareness, and demand for convenient, nutritious meal solutions.

Which soup types lead the U.S. soup market?

The U.S. soup market is led by canned soups, ready-to-eat options, broths, and creamy varieties popular for everyday consumption.

What role do canned soups play in the U.S. soup market?

Canned soups dominate the U.S. soup market as affordable, shelf-stable choices for quick preparation and long storage.

How important are ready-to-eat soups in the U.S. soup market?

Ready-to-eat soups fuel the U.S. soup market by meeting demands for fast, heat-and-serve meals in time-pressed households.

What health trends shape the U.S. soup market?

The U.S. soup market adapts to health trends with low-sodium, organic, and clean-label options for wellness-focused buyers.

How does convenience influence the U.S. soup market?

Convenience drives the U.S. soup market as consumers seek instant, microwaveable soups for busy schedules and on-the-go eating.

What flavors define the U.S. soup market?

The U.S. soup market features chicken noodle, tomato, vegetable, and creamy varieties alongside innovative global flavors.

What channels serve the U.S. soup market?

The U.S. soup market reaches buyers through supermarkets, convenience stores, online platforms, and club retailers.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com