U.S Spirits Market Size, Share, Trends & Growth Forecast Report - Segmented By Product, End-User, Distribution Channel, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Spirits Market Report Summary

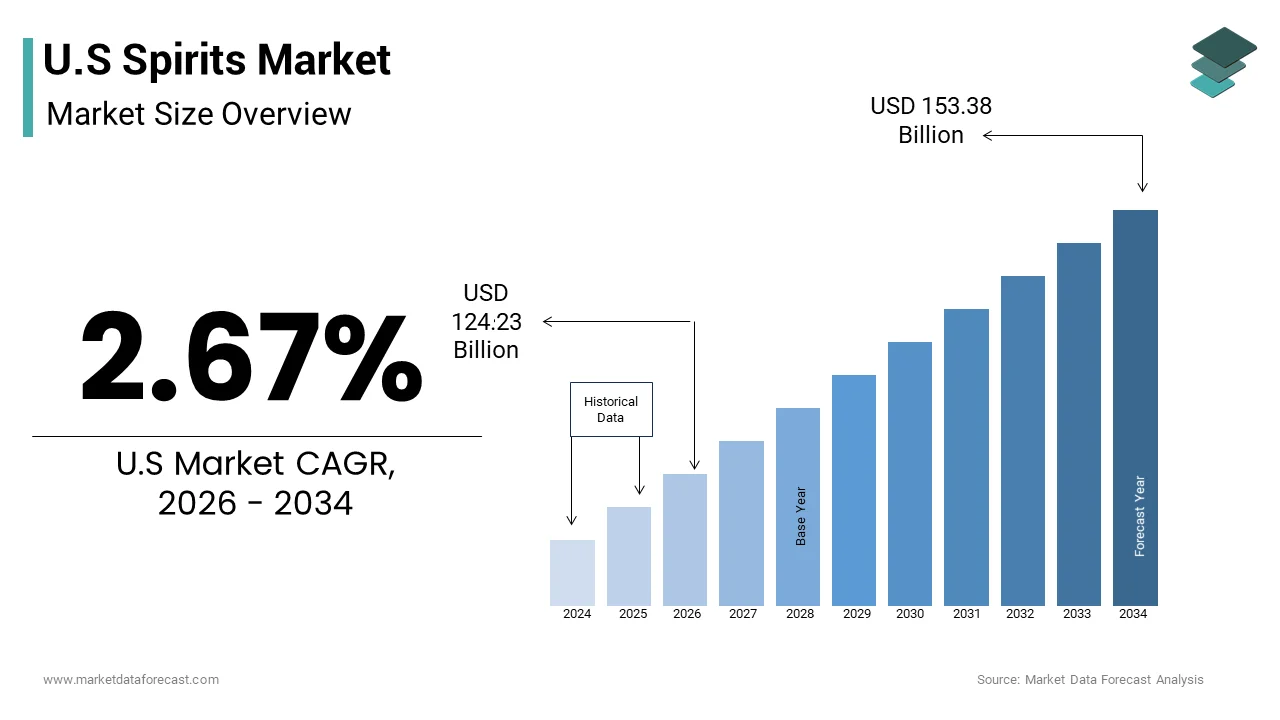

The United States spirits market was valued at USD 121 billion in 2025 and is projected to grow from USD 124.23 billion in 2026 to USD 153.38 billion by 2034, registering a CAGR of 2.67% during the forecast period from 2026 to 2034. The growth of the U.S. spirits market is driven by increasing consumer preference for premium and craft alcoholic beverages, rising demand for flavored and ready-to-drink (RTD) spirits, and evolving social drinking trends. Additionally, innovation in product offerings, expansion of distribution channels, and strong brand marketing strategies are supporting steady market expansion across the country.

Key Market Trends

- Growing demand for premium and super-premium spirits, especially among younger consumers seeking quality and unique taste profiles.

- Rising popularity of craft distilleries and artisanal spirits, driving innovation and localized production.

- Increasing consumption of ready-to-drink (RTD) cocktails and flavored spirits for convenience and variety.

- Expansion of e-commerce and direct-to-consumer alcohol sales channels enhancing accessibility.

- Shift toward healthier and low-alcohol options, including organic and sustainably produced spirits.

Segmental Insights

By Product

The whiskies segment dominated the U.S. spirits market in 2025, driven by strong consumer preference for bourbon, Scotch, and premium whiskey variants, along with growing interest in aged and small-batch products.

By End User

The men segment accounted for the largest share of the U.S. spirits market in 2025, supported by higher consumption rates and brand loyalty within this demographic, although female consumer participation is steadily increasing.

By Distribution Channel

The off-trade segment held the leading share in 2025, driven by strong retail sales through liquor stores, supermarkets, and online platforms, offering convenience and a wide product selection.

Regional Insights

The United States dominated the North American spirits market, accounting for an 85.5% share in 2025. Market growth is supported by a well-established alcohol industry, high consumer spending on premium beverages, and a strong presence of domestic and international brands. Urban regions and metropolitan areas continue to drive demand, while evolving consumer lifestyles and regulatory support for online alcohol sales further contribute to market expansion.

Competitive Landscape

The U.S. spirits market is highly competitive and characterized by the presence of global leaders and regional craft producers focusing on innovation, premiumization, and brand differentiation. Key players are investing in product diversification, strategic acquisitions, and digital marketing to strengthen their market position. Prominent companies operating in the market include Diageo PLC, Suntory Holdings Limited, Bacardi Limited, Pernod Ricard SA, Sazerac Company Inc., Constellation Brands, Inc., Brown-Forman Corporation, E. & J. Gallo Winery, Heaven Hill Distilleries, Inc., Davide Campari-Milano N.V., William Grant & Sons Ltd., Rémy Cointreau S.A., Becle, S.A.B. de C.V., Fifth Generation, Inc., MGP Ingredients Inc., The Asahi Group Holdings, Ltd., Castle & Key Distillery, LLC, Stoli Group, Ole Smoky Distillery LLC, and The Boston Beer Company, Inc..

U.S Spirits Market Size

The United States spirits market size was valued at USD 121 billion in 2025 and is anticipated to reach USD 124.23 billion in 2026 to reach USD 153.38 billion by 2034, growing at a CAGR of 2.67% during the forecast period from 2026 to 2034.

Current Market Overview and Definition

Spirits (often called "hard liquor" or simply "liquor") are high-alcohol beverages created through distillation. This sector is characterized by a complex regulatory framework involving federal and state level controls that govern manufacturing, taxation, and sales. According to the Distilled Spirits Council of the United States (2025 Annual Economic Briefing), the industry supports over 1.7 million jobs and contributes approximately $250 billion to the national economy annually. The market has evolved from traditional consumption patterns toward a more sophisticated landscape where consumers prioritize quality, authenticity, and unique flavor profiles. As per the National Institute on Alcohol Abuse and Alcoholism, alcohol consumption patterns vary significantly across demographics, with spirits maintaining a strong presence among adult drinkers. The rise of craft distilleries has diversified the product offerings, introducing small batch and artisanal options that appeal to discerning palates. Consumer trends indicate a shift toward premiumization, where individuals are willing to pay higher prices for superior quality and brand heritage. The integration of spirits into mixology and cocktail culture further drives demand, particularly in urban centers with vibrant nightlife scenes. Regulatory changes regarding direct to consumer shipping and tasting room operations have also influenced market dynamics. This environment requires stakeholders to navigate legal complexities while adapting to evolving consumer preferences for transparency and sustainability. The market continues to demonstrate resilience despite economic fluctuations, underpinned by the deep rooted social role of spirits in American culture.

MARKET DRIVERS

Premiumization and Demand for High Quality Craft Spirits

The trend toward premiumization and the increasing demand for high quality craft spirits are the driving force behind the expansion of the United States spirits market. Consumers are shifting away from value oriented brands toward premium and super premium categories that offer superior taste, craftsmanship, and brand storytelling. According to the Distilled Spirits Council of the United States (DISCUS), the trend of premiumization paused in 2024, with sales of super premium spirits softening as consumers faced economic pressures and shifted toward more affordable, lower-priced categories. As per a study, widely reported in 2025, inflation-driven price increases have dampened consumer spending power, leading to a decline in spirit sales volumes and a shift toward value-oriented products rather than elevated premium options. This shift is driven by a growing appreciation for the art of distillation, aging processes, and unique botanical profiles. Craft distilleries have played a pivotal role in this movement by offering limited edition releases and locally sourced ingredients that resonate with authenticity seeking buyers. The influence of mixology and cocktail culture has further amplified this trend, as bartenders and enthusiasts seek specific high quality spirits to create complex drinks. Social media platforms facilitate the discovery of niche brands, enabling smaller producers to reach national audiences. The desire for exclusivity and differentiation motivates consumers to explore diverse spirit types such as aged rye whiskey or small batch gin. This cultural evolution toward sophistication ensures that the premium segment continues to expand, driving overall market growth and profitability for brands that emphasize quality and heritage.

Expansion of Ready to Drink Cocktail Categories

The expansion of ready to drink (RTD) cocktail categories significantly boosts the growth of the United States spirits market. This offers convenience and consistency to modern consumers. RTD cocktails combine high quality spirits with mixers in pre packaged formats, appealing to individuals who seek ease of preparation without compromising on taste. According to the Beverage Information Group, the RTD category has experienced double digit growth rates in recent years, outperforming many traditional spirit segments. As per sources, sales of canned cocktails have surged, particularly among younger demographics who value portability and portion control. The convenience of RTDs aligns with busy lifestyles and the trend toward outdoor socializing, such as picnics and festivals, where glass bottles are often prohibited. Major spirit companies have entered this space by launching their own RTD lines, leveraging established brand equity to capture market share. The variety of flavors and alcohol strengths available caters to diverse preferences, from light and refreshing spritzers to bold and complex old fashioneds. Retailers have expanded shelf space for RTDs, recognizing their potential for impulse purchases and high turnover. The regulatory acceptance of malt based and spirit based RTDs in various states has further facilitated market penetration. This innovation in format and packaging ensures that spirits remain accessible and relevant to a broader audience, driving volume growth and attracting new consumers to the category.

MARKET RESTRAINTS

Stringent Regulatory Frameworks and Taxation Policies

Stringent regulatory frameworks and high taxation policies hinder the growth of the United States spirits market. This increases operational costs and limits market access. The alcohol industry is subject to a complex web of federal, state, and local regulations that govern production, labeling, advertising, and distribution. According to the Alcohol and Tobacco Tax and Trade Bureau, excise taxes on distilled spirits are significantly higher than those on beer and wine, impacting pricing strategies and profit margins. As per the National Conference of State Legislatures, varying state laws regarding direct to consumer shipping and retail hours create logistical challenges for manufacturers and distributors. The three tier system, which mandates separation between producers, distributors, and retailers, adds layers of complexity and cost to the supply chain. Compliance with these regulations requires substantial legal and administrative resources, particularly for small craft distilleries with limited budgets. High taxes are often passed on to consumers, potentially dampening demand among price sensitive segments. Additionally, restrictions on advertising and marketing limit the ability of brands to reach potential customers effectively. The inconsistency in regulations across different jurisdictions hinders national expansion efforts for emerging brands. These regulatory burdens create barriers to entry and growth, forcing companies to navigate a fragmented and often restrictive legal landscape. Reforms need to simplify these processes. Until then, the industry will continue to face significant operational headwinds.

Health Consciousness and Changing Social Attitudes

Health consciousness and changing social attitudes toward alcohol consumption pose major obstacles for the United States spirits market. A growing segment of the population is reducing or eliminating alcohol intake due to concerns about health risks, calorie content, and mental well being. According to the Centers for Disease Control and Prevention, alcohol use is linked to numerous health issues including cancer, prompting updated public health guidance that emphasizes "drinking less is better" for health rather than simply encouraging moderation, as recent data indicates even moderate consumption carries risks. As per Gallup polls, the percentage of Americans who abstain from alcohol has increased in recent years, particularly among younger generations such as Millennials and Gen Z. This shift is driven by the wellness movement, which prioritizes physical fitness and mental clarity over traditional social drinking habits. The rise of the sober curious movement has led to increased demand for non alcoholic alternatives, diverting spending away from traditional spirits. Bars and restaurants are responding by expanding their mocktail menus, further normalizing non alcoholic consumption. Marketing restrictions and negative perceptions of alcohol related harms also influence consumer behavior. While moderate drinking remains socially acceptable, the stigma associated with heavy consumption is growing. This cultural shift challenges the spirits industry to adapt by promoting responsible drinking and exploring lower alcohol or non alcoholic product lines. The long term impact of these changing attitudes may result in stagnant or declining volume growth for traditional spirit categories.

MARKET OPPORTUNITIES

Growth of Non-Alcoholic and Low Alcohol Spirits

The growth of non-alcoholic and low alcohol spirits offers new pathways for the United States spirits market. This caters to health-conscious consumers and the sober curious demographic. Innovations in distillation and flavor extraction technologies have enabled the creation of sophisticated non alcoholic spirits that mimic the complexity and taste profiles of traditional counterparts. According to the Adult Non-Alcoholic Beverage Association (ANBA), sales of non-alcoholic beverages have grown substantially, with spirits alternatives emerging as a key category. As per research, consumers are seeking ways to participate in social rituals without the effects of alcohol, driving demand for high quality substitutes. Major spirit brands are launching non alcoholic versions of their flagship products, leveraging brand recognition to attract new customers. These products appeal to individuals who wish to reduce alcohol intake for health, religious, or personal reasons. The versatility of non alcoholic spirits in mixology allows bartenders to create intricate mocktails that rival traditional cocktails. Retailers are dedicating shelf space to these products, recognizing their potential for growth and higher margins. Marketing campaigns that emphasize inclusivity and wellness resonate with modern consumers who value choice and balance. The expansion of this segment allows spirit companies to diversify their portfolios and maintain relevance in a changing cultural landscape. The market can capture new revenue streams by embracing this trend. In doing so, it will build loyalty among health-focused buyers.

Direct to Consumer Sales and E Commerce Expansion

The expansion of direct to consumer (DTC) sales and e commerce platforms provides a promising prospect for the United States spirits market. This enables brands to bypass traditional distribution channels and connect directly with buyers. Recent regulatory changes in several states have allowed for the online sale and shipping of spirits, opening new avenues for growth. According to the American Distilling Institute (ADI), DTC sales have become an increasingly important revenue stream for craft distillers, helping to offset losses from traditional channels. As per studies, online alcohol sales have continued to grow, driven by the convenience of home delivery and the ability to access a wider variety of products. E commerce platforms allow brands to share their stories, educate consumers, and build communities through digital engagement. Subscription services and curated boxes provide recurring revenue opportunities and encourage exploration of new flavors. Data collected from online interactions enables companies to personalize marketing efforts and improve customer retention. The ability to reach consumers in remote areas or those with limited access to specialty stores expands market reach. Brands are investing in user friendly websites and secure payment systems to enhance the shopping experience. This digital transformation empowers producers to control their brand narrative and gather valuable insights into consumer preferences. The spirits market can enhance profitability by leveraging DTC channels. This approach also fosters deeper connections with its audience.

MARKET CHALLENGES

Supply Chain Disruptions and Raw Material Shortages

Supply chain disruptions and raw material shortages are serious inhibition to the United States spirits market. This affects production consistency and increases costs. The spirits industry relies on agricultural inputs such as grains, sugarcane, and botanicals, which are vulnerable to weather events, climate change, and geopolitical instability. According to the USDA Economic Research Service, fluctuations in crop yields due to droughts or floods can lead to scarcity and price volatility for key ingredients. As per the Bureau of Labor Statistics, transportation and logistics costs have risen significantly, impacting the efficiency of distribution networks. Shortages of glass bottles and aluminum cans have also constrained production capabilities, forcing manufacturers to delay launches or limit output. The reliance on global sourcing for certain materials adds complexity and risk to supply chain management. Labor shortages in manufacturing and logistics sectors further exacerbate these challenges, leading to delays and increased operational expenses. Companies must invest in redundant supply chains and alternative sourcing strategies to mitigate these risks, which requires significant capital. The unpredictability of supply conditions makes long term planning difficult and affects inventory management. These disruptions can lead to product shortages on shelves, frustrating consumers and damaging brand loyalty. Addressing these supply chain vulnerabilities requires collaboration across the industry and investment in resilient infrastructure.

Counterfeit Products and Brand Integrity Issues

Counterfeit products and brand integrity issues hold back the expansion of the United States spirits market. This undermines consumer trust and causes financial losses. The high value of premium and luxury spirits makes them attractive targets for counterfeiting, where fake products are sold as genuine articles. According to the International Trademark Association, counterfeit alcohol poses serious health risks due to unregulated production methods and potentially toxic ingredients. As per the Federal Bureau of Investigation, intellectual property theft in the alcohol industry results in billions of dollars in lost revenue annually. Counterfeit products damage brand reputation and erode consumer confidence, as buyers may associate poor quality or safety issues with the authentic brand. Detecting and combating counterfeiting requires significant investment in security features, legal action, and consumer education. The proliferation of online marketplaces complicates enforcement efforts, as fake products can be sold anonymously to a wide audience. Small craft distilleries are particularly vulnerable as they lack the resources to protect their intellectual property effectively. The presence of counterfeit goods distorts market data and undermines fair competition. Industry groups are collaborating with law enforcement and technology providers to develop tracking and authentication solutions. However, the persistent threat of counterfeiting remains a critical challenge that requires ongoing vigilance and strategic intervention to protect brand integrity and consumer safety.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 2.67% |

| Segments Covered | By Product, End-User, Distribution Channel, and Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | US, Canada, and the Rest of North America |

| Market Leaders Profiled | Diageo PLC, Suntory Holdings Limited, Bacardi Limited, Pernod Ricard SA, Sazerac Company Inc., Constellation Brands, Inc., Brown-Forman Corporation, E. & J. Gallo Winery, Heaven Hill Distilleries, Inc., Davide Campari-Milano N.V., William Grant & Sons Ltd., Rémy Cointreau S.A., Becle, S.A.B. de C.V. (Proximo Spirits), Fifth Generation, Inc., MGP Ingredients Inc., The Asahi Group Holdings, Ltd., Castle & Key Distillery, LLC, Stoli Group, Ole Smoky Distillery LLC, The Boston Beer Company, Inc. (Truly Spirits) |

SEGMENTAL ANALYSIS

By Product Insights

The whiskies segment was the largest segment in the United States spirits market in 2025. This prominence of the segment is supported by its deep cultural roots and the ongoing trend toward premiumization. American whiskey, particularly bourbon and rye, is protected by federal standards of identity which mandates that it be produced in the United States, fostering a strong sense of national pride and authenticity. The versatility of whiskey in both neat consumption and classic cocktails such as the Old Fashioned and Manhattan ensures its broad appeal across demographics. Craft distilleries have further enriched the market by offering small batch and single barrel options that attract connoisseurs seeking unique flavor profiles. The aging process and craftsmanship associated with whiskey production justify higher price points, encouraging consumers to trade up from standard brands. Marketing efforts emphasizing heritage, tradition, and artisanal methods resonate strongly with buyers who value storytelling and provenance. This combination of cultural significance and quality elevation solidifies whiskey as the leading product type in the US spirits landscape. The versatility of whiskey in mixology and its prominence in on premise establishments significantly drive its market domination. Whiskey serves as the base for numerous popular cocktails, making it a staple in bars, restaurants, and lounges across the country. This exposure introduces consumers to new brands and styles, driving retail sales as enthusiasts seek to replicate bar experiences at home. The availability of diverse whiskey types including Scotch Irish Canadian and American variants allows for extensive experimentation and pairing opportunities. Retailers support this trend by expanding their whiskey selections and offering tasting events that educate consumers. The social aspect of whiskey consumption, often associated with networking and celebration, reinforces its position as a preferred choice for group settings. The ability of whiskey to adapt to seasonal trends such as warm weather highballs or winter sippers ensures year round relevance. This dynamic presence in both social and private settings sustains its leadership in the spirits market.

The tequila and mezcal segment is estimated to register the fastest CAGR in the US spirits market during the forecast period owing to surging popularity among Millennials and Generation Z consumers. These demographics are drawn to the authentic production methods and cultural heritage associated with agave spirits. The perception of tequila as a cleaner and more natural spirit compared to grain based alcohols appeals to health conscious drinkers who prioritize ingredient transparency. Social media platforms play a crucial role in this growth, with influencers showcasing tequila based cocktails and lifestyle content that resonates with younger audiences. The expansion of mezcal, known for its smoky flavor and artisanal production, adds depth to the category and attracts adventurous palates. Brands are responding by launching sustainable and ethically sourced products that align with the values of these consumers. The versatility of tequila in both traditional shots and modern mixology ensures broad appeal. This demographic shift and cultural alignment ensure that tequila and mezcal continue to experience robust growth. Premiumization and innovation in craft agave spirits are key drivers accelerating the growth of the tequila and mezcal segment. Consumers are increasingly willing to pay for high quality 100 percent agave tequilas and small batch mezcals that offer complex flavor profiles. Distillers are experimenting with different agave varieties and fermentation techniques to create distinct tastes that differentiate their products. The rise of celebrity owned tequila brands has also brought mainstream attention to the category, leveraging star power to drive trial and adoption. Retailers are dedicating more shelf space to premium agave spirits, recognizing their high margin potential. The educational aspect of agave production, including the regions of Jalisco and Oaxaca, enhances consumer appreciation and loyalty. Collaborations with mixologists and chefs further elevate the status of these spirits in culinary contexts. This focus on quality and craftsmanship ensures that the tequila and mezcal segment remains dynamic and rapidly expanding.

By End User Insights

The men segment captured the majority share of the United States spirits market in 2025. This leading position of the segment is credited to traditional consumption patterns and generally higher volume intake of alcoholic beverages. Historical and cultural norms have long associated spirits consumption with masculinity, influencing drinking habits and preferences. This demographic drives significant volume sales in categories such as whiskey and bourbon, which are often marketed with themes of strength and heritage. The prevalence of male dominated social clubs and networking events where spirits are served further reinforces this trend. Marketing campaigns targeting men often emphasize ruggedness and tradition, resonating with established consumer identities. Retailers tailor promotions and displays to appeal to male shoppers, who tend to make larger bulk purchases. The loyalty of male consumers to specific brands ensures steady repeat business. While trends are shifting, the entrenched habits of male drinkers continue to underpin their dominance in the spirits market. The influence of men in on premise and business settings significantly contributes to their leading position in the spirits market. Men frequently dominate decision making in corporate entertainment and social gatherings where spirits are the preferred beverage. The role of men as primary purchasers for household alcohol stocks also impacts retail sales, as they often select spirits for personal use and guest entertainment. Brand loyalty among male consumers is strong, with many sticking to familiar labels that convey status and reliability. The visibility of spirits in male oriented media and sports sponsorships further cements this connection. Retailers and distributors prioritize relationships with male dominated venues and events to maximize reach. This structural advantage in both social and professional spheres ensures that men remain the primary drivers of spirits consumption.

The women segment is anticipated to witness the fastest CAGR in the US spirits market from 2026 to 2034 due to a shift toward premium and flavor forward spirits that align with evolving tastes. Female consumers are increasingly exploring diverse spirit categories beyond traditional wine and beer, seeking sophisticated and enjoyable drinking experiences. The trend toward moderation and quality over quantity encourages women to choose higher end products that provide satisfaction in smaller servings. Marketing efforts that emphasize elegance, wellness, and social connection resonate strongly with female audiences. Brands are launching products with lower sugar content and natural ingredients to meet health conscious demands. The rise of female led distilleries and brands creates representation and fosters community among women drinkers. This cultural shift and product innovation ensure that the female segment continues to expand rapidly. Increased social independence and purchasing power among women accelerate their growth in the spirits market. Women are taking greater control of their leisure activities and spending decisions, leading to higher engagement in nightlife and social drinking scenarios. The emergence of women focused social groups and clubs centered around spirits tasting and education fosters a supportive environment for exploration. Retailers are responding by creating welcoming spaces and marketing campaigns that appeal to female consumers. The ability of women to influence household purchasing decisions also boosts retail sales of spirits. This empowerment and economic strength ensure that women remain a dynamic and rapidly growing segment in the spirits industry.

By Distribution Channel Insights

The off-trade channel led the United States spirits market in 2025. This leading position of the segment is attributed to the convenience it offers and the growing trend of home consumption. Consumers prefer purchasing spirits from liquor stores supermarkets and online retailers for the ease of access and wider selection. The comfort of consuming alcohol at home, particularly after the pandemic, has sustained high off trade demand. Retailers offer competitive pricing and promotions that attract budget conscious shoppers. The availability of diverse brands and niche products in large retail formats allows consumers to explore new options without leaving home. The integration of curbside pickup and delivery services further enhances convenience. This accessibility and flexibility ensure that the off trade channel remains the primary source for spirits purchases. Regulatory ease and pricing advantages significantly contribute to the dominance of the off trade channel. Unlike on premise establishments, off trade retailers face fewer restrictions on operating hours and sales volumes in many states. Taxes and markups are often lower in off trade settings, resulting in better deals for buyers. The ability to purchase spirits alongside other groceries simplifies shopping trips and encourages larger basket sizes. Retailers leverage loyalty programs and digital coupons to drive repeat business. The stability of off trade sales provides a reliable revenue stream for producers and distributors. This economic and regulatory environment ensures that the off trade channel maintains its leading position.

The on trade channel segment is likely to experience the fastest CAGR in the US spirits market over the forecast period. This rapid expansion of the segment is propelled by the rebound in hospitality and social dining following pandemic restrictions. Consumers are eager to return to bars restaurants and clubs for social interaction and experiential drinking. The role of bartenders as mixologists has elevated the status of on trade consumption, attracting enthusiasts seeking expertly crafted drinks. Events and festivals featuring spirits tastings have also boosted on trade visibility. The social atmosphere and immediate gratification of on premise drinking cannot be replicated at home, driving sustained growth. This resurgence in social activity ensures that the on trade channel continues to expand rapidly. Experiential marketing and brand engagement accelerate the growth of the on trade channel. Spirits brands invest heavily in on premise activations such as sponsored events bartender training and exclusive launches to build loyalty. The immersive nature of on trade experiences allows brands to tell their stories and connect emotionally with customers. Bars and restaurants serve as showcases for premium and limited edition spirits, encouraging upselling and exploration. The integration of digital menus and interactive displays enhances engagement. This strategic focus on experience ensures that the on trade channel remains a dynamic and high growth area.

COUNTRY ANALYSIS

Market Position and Status

United States Spirits Market Analysis

The United States remained dominant in the North American spirits market and accounted for a 85.5% share in 2025. High maturity, extensive product diversity, and strong brand recognition are the main reasons behind the dominance of the US market. According to the Distilled Spirits Council of the United States, the country is one of the largest spirits markets globally, driven by a culture of social drinking and premiumization. The market benefits from a well-developed distribution network and robust regulatory framework that ensures product safety and quality. Market data from the Distilled Spirits Council of the United States (DISCUS) indicates that while volume has remained resilient, consumer trends are shifting toward higher quality and craft options (premiumization). Conversely, the National Institute on Alcohol Abuse and Alcoholism (NIAAA) focuses on health outcomes, reporting that alcohol use disorder (AUD) affects approximately 27.1 million adults (10.3% of the age group) based on the most recent national survey data. The presence of major multinational companies fosters innovation and competition, driving continuous improvement in product offerings. Consumer preferences are influenced by health consciousness and sustainability, prompting brands to adapt their strategies. The United States leads in trends such as ready to drink cocktails and non alcoholic spirits, influencing global market dynamics. Investment in digital marketing and e commerce enhances reach and engagement. The strong economic foundation and high disposable income support demand for premium and luxury spirits. This combination of scale, innovation, and consumer sophistication ensures that the United States remains the central pillar of the global spirits industry.

COMPETITIVE LANDSCAPE

The competition in the United States spirits market is intense and characterized by the presence of large multinational corporations alongside a growing number of craft distilleries. Major players compete on the basis of brand heritage product quality innovation and marketing effectiveness to secure shelf space and consumer loyalty. The market sees continuous innovation as companies launch new flavors formats and premium expressions to differentiate their offerings. Craft distilleries contribute to market diversity by offering unique and locally sourced products that appeal to niche segments. Private label brands pose a challenge by providing affordable alternatives that attract budget conscious shoppers. Regulatory complexities and varying state laws influence distribution strategies and market access. The rise of health consciousness drives demand for low alcohol and non alcoholic options prompting reformulation efforts. Digital marketing and e commerce platforms enable direct engagement with consumers and bypass traditional distribution channels. Consolidation through mergers and acquisitions is common as larger firms seek to expand their reach and achieve economies of scale. This dynamic landscape requires agility and strategic foresight to navigate changing trends and maintain market relevance effectively.

KEY MARKET PLAYERS

A few of the market players that are dominating the U.S spirits market are

- Diageo PLC

- Suntory Holdings Limited

- Bacardi Limited

- Pernod Ricard SA

- Beam Suntory Inc

- Sazerac Company Inc.

- Constellation Brands, Inc.

- Brown-Forman Corporation

- E. & J. Gallo Winery

- Heaven Hill Distilleries, Inc.

- Davide Campari-Milano N.V.

- William Grant & Sons Ltd.

- Rémy Cointreau S.A.

- Becle, S.A.B. de C.V. (Proximo Spirits)

- Fifth Generation, Inc.

- MGP Ingredients Inc.

- The Asahi Group Holdings, Ltd.

- Castle & Key Distillery, LLC

- Stoli Group

- Ole Smoky Distillery LLC

- The Boston Beer Company, Inc. (Truly Spirits)

Top Players In The Market

- Diageo plc is a global leader in the spirits industry with a vast portfolio of premium brands including Johnnie Walker and Smirnoff. The company operates in over one hundred and eighty countries and drives innovation through sustainable practices and digital engagement. Recent actions include significant investments in distillery expansions and the acquisition of niche craft brands to diversify its offerings. Diageo focuses on premiumization strategies to capture high value consumers and enhance brand loyalty. The company also prioritizes environmental sustainability by reducing carbon emissions and water usage in production facilities. These initiatives strengthen its market position by aligning with modern consumer values and ensuring long term operational resilience. Diageo continues to leverage data analytics to optimize supply chain efficiency and marketing effectiveness. Diageo maintains a strong focus on quality and brand heritage. As a result, it remains a dominant force in the global spirits landscape.

- Pernod Ricard SA is a major international player in the spirits and wine sector known for iconic brands such as Absolut Vodka and Jameson Irish Whiskey. The company emphasizes creativity and entrepreneurship to drive growth and connect with diverse consumer bases globally. Recent actions involve strategic acquisitions of premium tequila and mezcal brands to capitalize on emerging trends. Pernod Ricard invests heavily in responsible drinking campaigns and sustainability initiatives to enhance corporate reputation. The company also expands its presence in key growth markets through localized marketing and distribution partnerships. These efforts strengthen its market position by fostering brand affinity and operational agility. Pernod Ricard leverages digital platforms to engage directly with consumers and provide personalized experiences. Pernod Ricard maintains its competitive edge in the dynamic global spirits industry. They achieve this by focusing on innovation and cultural relevance.

- Beam Suntory Inc is a leading producer of premium spirits with a strong portfolio including Jim Beam and Maker s Mark. The company combines American bourbon heritage with Japanese craftsmanship to offer unique and high quality products. Recent actions include expanding production capacity in Kentucky and investing in sustainable agriculture practices. Beam Suntory focuses on premiumization and innovation by launching limited edition releases and flavored variants. The company also enhances its digital capabilities to improve customer engagement and e commerce operations. These strategies strengthen its market position by appealing to discerning consumers and adapting to changing preferences. Beam Suntory prioritizes diversity and inclusion within its workforce and community initiatives. Beam Suntory leverages its global network and brand equity. This allows the company to continue growing its influence in the international spirits market.

Top Strategies Used By Key Market Participants

Key players in the United States spirits market employ several major strategies to maintain competitiveness and drive growth. Premiumization is central to these efforts with companies focusing on high end and super premium brands to capture value conscious consumers. Strategic acquisitions allow firms to expand their portfolios and access niche categories such as craft tequila and artisanal gin. Sustainability initiatives including eco friendly packaging and responsible sourcing enhance brand reputation and meet regulatory expectations. Digital transformation enables direct to consumer sales and personalized marketing campaigns that build loyalty. Innovation in ready to drink formats appeals to younger demographics seeking convenience and variety. Partnerships with hospitality venues ensure prominent placement and visibility in on trade channels. These combined strategies allow participants to adapt to evolving consumer preferences and sustain long term profitability in a highly competitive environment.

MARKET SEGMENTATION

This research report on the U.S spirits market is segmented and sub-segmented into the following categories.

By Product Type

- Brandy and Cognac

- Liqueur

- Rum

- Tequila and Mezcal

- Whiskies

- White Spirits

- Other Spirit Types

By End User

- Men

- Women

By Distribution Channel

- On-Trade

- Off-Trade

- Specialty/Liquor Stores

- Others Off Trade Channels

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

What is currently driving growth in the United States spirits market?

Rising demand for premium alcoholic beverages and craft spirits is driving market growth.

Why are spirits becoming more popular among consumers in the United States?

Consumers are seeking unique flavors and high-quality drinking experiences.

How would you explain spirits in simple terms?

They are distilled alcoholic beverages such as whiskey, vodka, and rum.

Where are spirits most commonly consumed in the United States?

They are widely consumed in homes, bars, restaurants, and social events.

What makes spirits important in the beverage industry?

They offer product diversity and premiumization opportunities.

From a consumer perspective, are premium spirits worth the higher price?

Yes, many consumers value quality, taste, and brand experience.

What challenges are affecting the United States spirits market?

Regulatory restrictions and changing consumer preferences are key challenges.

How is consumer lifestyle influencing spirits consumption?

Shifts toward social drinking and premium products are boosting demand.

Which spirit categories contribute the most to market demand?

Whiskey, vodka, tequila, and rum are major contributors.

Is the United States spirits market growing steadily?

Yes, it is expanding with increasing demand for premium and craft products.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com