U.S Stationery Market Size, Share, Trends & Growth Forecast Report - Segmented By Type, Application, Distribution Channel, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Stationery Market Report Summary

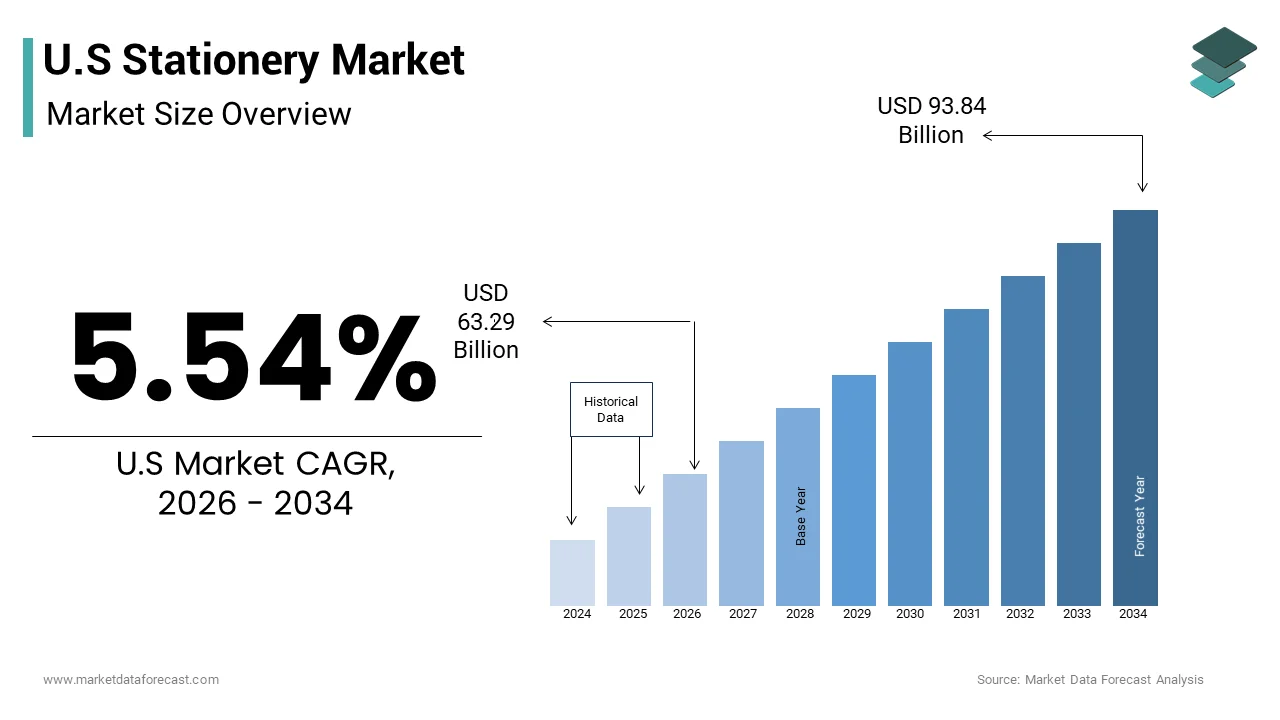

The U.S. stationery market was valued at USD 59.96 billion in 2025 and is projected to grow from USD 63.29 billion in 2026 to USD 93.84 billion by 2034, registering a CAGR of 5.54% during the forecast period from 2026 to 2034. The growth of the U.S. stationery market is driven by increasing demand for office and educational supplies, rising student enrollment, and the continued relevance of paper-based products across academic and professional environments. Additionally, growing interest in creative stationery, personalized products, and premium writing instruments is further supporting market expansion.

Key Market Trends

- Rising demand for eco-friendly and sustainable stationery products made from recycled and biodegradable materials.

- Increasing popularity of premium and designer stationery driven by gifting and personalization trends.

- Growth in home-office and remote working culture boosting demand for office supplies.

- Expansion of e-commerce platforms enhancing product accessibility and variety.

- Continued relevance of traditional paper products despite increasing digitalization.

Segmental Insights

By Type

The paper products segment dominated the U.S. stationery market in 2025, supported by consistent demand for notebooks, printing paper, and educational materials across schools and offices.

By Application

The residential segment held the largest share in 2025, driven by increased usage of stationery products in home settings for education, remote work, and personal organization.

By Distribution Channel

The offline distribution channel led the market in 2025, owing to strong sales through supermarkets, specialty stores, and office supply retailers offering immediate product availability.

Regional Insights

The United States accounted for an 85.6% share of the stationery market in 2025, maintaining its position as a leading contributor. Market growth is supported by a well-established retail network, high demand from educational institutions and businesses, and increasing consumer spending on quality stationery products.

Competitive Landscape

The U.S. stationery market is highly competitive, with key players focusing on product innovation, sustainability, and brand differentiation to strengthen their market presence. Companies are introducing eco-friendly materials, expanding premium product lines, and leveraging digital sales channels to reach a broader audience. Prominent players in the market include Faber-Castell, Kokuyo Camlin Ltd., Bic Group, STAEDTLER SE, Rifle Paper Co., Newell Brands, Schwan-STABILO, ITC Limited, Navneet Education Limited, Ryohin Keikaku Co., Ltd., and 3M Company.

U.S Stationery Market Size

The U.S stationery market size was valued at USD 59.96 billion in 2025 and is anticipated to reach USD 63.29 billion in 2026 to reach USD 93.84 billion by 2034, growing at a CAGR of 5.54% during the forecast period from 2026 to 2034.

Current Market Overview and Definition

Stationery refers to the collective range of materials used for writing, printing, or office work. This market includes items such as notebooks pens pencils folders and planners that facilitate communication record keeping and creative expression. As per the National Center for Education Statistics approximately 50 million students are enrolled in public schools annually creating a consistent baseline demand for essential school supplies. The market definition extends beyond functional utility to include aesthetic and lifestyle components, where design and brand identity influence consumer choices. According to the Bureau of Labor Statistics employment in office and administrative support roles remains significant with millions of workers requiring daily access to stationary items for professional tasks. Consumer behavior is increasingly shaped by the trend toward analog mindfulness where individuals use physical writing tools to disconnect from digital screens and enhance mental well being. Surveys from the US Postal Service (USPS) Household Diary Study indicate that while personal letter volumes have declined, a majority of Americans (often cited around 73-81% in industry interpretations) still report a high preference for receiving handwritten notes over digital alternatives, valuing the tangible connection. The industry operates within a supply chain that relies on pulp and paper manufacturing which faces evolving environmental regulations. Understanding this landscape requires analyzing the interplay between digital transformation which reduces some traditional uses and the resurgence of artisanal and premium stationery as luxury or hobbyist goods. The market is characterized by seasonal peaks particularly during back to school periods and holiday gifting seasons which drive significant volume fluctuations.

MARKET DRIVERS

Resurgence of Analog Mindfulness and Journaling

The growing trend toward analog mindfulness and journaling is a key driver for the United States stationery market. This growth encourages consumers to adopt physical writing practices for mental health and creativity. In an increasingly digital world individuals are seeking tactile experiences that promote relaxation focus and self reflection through handwriting and drawing. Studies published in journals such as Psychological Science and Frontiers in Psychology suggest that handwriting activates different neural pathways than typing, such as the parietal and central brain regions, leading to improved memory retention and learning. This psychological benefit drives demand for high quality journals planners and fountain pens that enhance the writing experience. According to multiple studies, sales of journals and planners have grown as consumers, particularly Gen Z and Millennials, increasingly view these items as tools for mindfulness and mental wellness. The popularity of bullet journaling and artistic lettering on social media platforms further amplifies this trend by showcasing aesthetically pleasing layouts and techniques that inspire participation. Retailers respond by offering curated collections of papers inks and accessories that cater to hobbyists and enthusiasts. The desire to reduce screen time and engage in slow living practices motivates purchases of durable and beautifully designed stationery products. This cultural shift ensures steady growth in the premium segment as users invest in tools that support their wellness routines and creative pursuits.

Persistent Demand from Educational Institutions

The continuous enrollment in educational institutions from kindergarten through higher education sustains a robust demand for basic stationery items in the United States stationary market. Schools and universities require vast quantities of notebooks writing utensils and organizational supplies for student use creating a predictable and recurring revenue stream for manufacturers. As per the National Center for Education Statistics (NCES), public school enrollment has declined from pre-pandemic levels (approx. 49.6 million in Fall 2022 vs. 50.8 million in Fall 2019), while retail bodies like the NRF track the billions spent annually by families on replenishing supplies. This institutional demand is reinforced by state and district mandates that specify required materials for various grade levels ensuring consistent purchase volumes. According to the National Retail Federation (NRF), household spending on school supplies peaks during the summer months, with recent surveys indicating families start shopping as early as July to prepare for the academic year. Teachers also contribute significantly to this demand by purchasing classroom materials often out of pocket or through school budgets to support instructional activities. The shift toward hybrid learning models has not eliminated the need for physical tools as students still rely on paper for note taking testing and creative projects. Additionally, the rise of early childhood education programs emphasizes fine motor skill development through writing and drawing further driving consumption among younger demographics. This structural reliance on educational systems provides a stable foundation for the stationery market mitigating the impact of digital substitution in other sectors.

MARKET RESTRAINTS

Digitalization of Communication and Record Keeping

The widespread adoption of digital technologies for communication documentation and organization is a major restraint on the United States stationery market. This reduces the necessity for physical paper products. Email cloud storage and productivity software have replaced many traditional uses of stationery such as letter writing file management and note taking in professional and personal contexts. As per a study, the vast majority of Americans now use digital platforms for news and social interaction, while USPS data indicates a long-term decline in First-Class Mail volume due to the shift toward electronic communication. This shift significantly impacts sales of envelopes letterheads and standard office paper which were once staple items. According to research, the transition to remote work has shifted demand, increasing sales of home office equipment and supplies, while the Bureau of Labor Statistics reports that telework remains a significant component of the U.S. labor landscape. Educational institutions are also integrating tablets and laptops into curricula which reduces the volume of notebooks and textbooks required for daily lessons. The convenience and searchability of digital records make them more attractive for long term storage compared to physical files. Consequently, the overall per capita consumption of traditional stationery items has decreased as consumers and organizations prioritize efficiency and sustainability through digitization. This structural change limits market growth and forces manufacturers to innovate beyond basic functional products.

Environmental Concerns and Paper Waste Awareness

Increasing awareness of environmental issues and the negative impact of paper waste further hinders the expansion of the United States stationery market. This influences consumer preferences and regulatory policies. The production of paper involves deforestation water consumption and chemical usage which raises concerns among eco conscious buyers who seek to minimize their ecological footprint. As per the Environmental Protection Agency paper and paperboard materials constitute a large portion of municipal solid waste prompting efforts to reduce consumption and increase recycling rates. Consumers are increasingly opting for digital alternatives or reusable options to avoid generating disposable waste from single use stationery items. According to a survey, a growing percentage of shoppers consider sustainability credentials when making purchasing decisions often avoiding products with excessive packaging or non recyclable components. Regulatory pressures such as stricter forestry standards and waste management laws add compliance costs for manufacturers who must source responsible materials and implement cleaner production processes. The perception of paper products as environmentally harmful discourages impulse buys and encourages minimalism in office and school supplies. Brands face challenges in convincing consumers that their products are sustainable despite the inherent resource intensity of paper manufacturing. This environmental scrutiny constrains market expansion and drives a shift toward durable or digital solutions over traditional disposable stationery.

MARKET OPPORTUNITIES

Expansion of Premium and Artisanal Product Lines

The development of premium and artisanal stationery products offers a significant opportunity for the United States market. This development appeals to consumers who value craftsmanship aesthetics and exclusivity. High end items such as leather bound journals handcrafted pens and bespoke paper goods cater to niche segments willing to pay for quality and design excellence. As per sources, the luxury goods sector including personal accessories and lifestyle items has shown resilience with consumers trading up for products that offer emotional value and status. This trend is driven by the desire for unique personalized items that reflect individual taste and serve as meaningful gifts. According to studies sales of premium writing instruments and limited edition notebooks have grown as buyers seek tangible connections to heritage brands and artisanal makers. Social media platforms facilitate the discovery of independent stationery studios allowing small businesses to reach global audiences without extensive retail infrastructure. Collaborations with artists and designers create buzz and differentiate products in a crowded market. The gifting culture around holidays and special occasions further boosts demand for beautifully packaged and high quality stationery sets. By focusing on superior materials intricate details and storytelling brands can command higher margins and build loyal customer bases. This strategy transforms stationery from a commodity into a collectible or luxury item thereby unlocking new revenue streams.

Integration of Smart and Hybrid Stationery Solutions

The integration of smart technology into traditional stationery paves the way for innovation and growth in the United States stationary market. This integration bridges the gap between analog and digital workflows. Smart notebooks and pens allow users to write by hand while simultaneously digitizing their notes for easy storage and sharing via mobile apps. As per the Consumer Technology Association the adoption of connected devices and smart home office solutions is rising indicating a receptive audience for hybrid tools that enhance productivity. These products appeal to professionals and students who prefer the cognitive benefits of handwriting but require the convenience of digital organization. According to resaerch companies like Rocketbook and Moleskine have successfully launched smart notebook systems that sync with cloud services demonstrating strong consumer interest. The ability to erase and reuse pages in smart notebooks also addresses environmental concerns by reducing paper waste. Manufacturers can leverage partnerships with software developers to create seamless ecosystems that integrate with popular productivity platforms. Marketing these solutions as efficiency tools for modern workflows attracts tech savvy users who value innovation. Additionally, the data collected from smart pen usage can provide insights into user habits enabling personalized features and improvements. This convergence of tradition and technology positions smart stationery as a dynamic growth area in the evolving office supply landscape.

MARKET CHALLENGES

Intense Competition from Private Label Brands

The prevalence of private label and store brand stationery products poses a critical challenge to established manufacturers in the United States stationary market. This drives price competition and erodes brand loyalty. Retailers such as Walmart Target and Amazon offer exclusive lines of notebooks pens and organizers at lower prices than national brands attracting cost conscious consumers. As per sources, private label sales in the office supplies category have grown significantly capturing market share from legacy manufacturers who struggle to justify premium pricing. These store brands benefit from reduced marketing costs and direct shelf placement allowing them to undercut competitors on price while maintaining acceptable quality standards. According to studies, shoppers are increasingly willing to switch to private labels for basic stationery items where brand differentiation is perceived as minimal. This trend pressures mainstream brands to reduce prices or increase promotional spending which squeezes profit margins and limits investment in innovation. The perception that private labels have improved in quality due to better sourcing and manufacturing further strengthens their competitive position. Established companies must invest heavily in branding product differentiation and customer engagement to retain market share. However, the sheer volume and accessibility of generic options make it difficult to maintain loyalty among price sensitive segments. This dynamic creates a constant battle for shelf space and consumer attention forcing companies to continuously adapt their strategies.

Supply Chain Disruptions and Raw Material Volatility

Supply chain disruptions and volatility in raw material costs impede the growth of the United States stationery market. This affects production stability and profitability. The industry relies on pulp paper plastics and metals which are subject to global commodity price fluctuations and logistical bottlenecks. As per the Bureau of Labor Statistics producer price indices for paper and related products have experienced significant swings due to factors such as energy costs transportation delays and trade policies. These increases force manufacturers to raise prices which can deter consumers and lead to trading down to cheaper alternatives. According to the Institute for Supply Management supply chain constraints have led to extended lead times for imported components complicating inventory management for retailers. The dependence on overseas manufacturing for many stationery items exposes the industry to geopolitical risks and labor issues that can halt production. Smaller brands with less purchasing power struggle to absorb these costs making it difficult to compete with larger corporations that can hedge against price risks. Additionally, the scarcity of specific materials such as high quality wood pulp affects the availability of premium products. This instability complicates long term planning and pricing strategies creating uncertainty for both suppliers and buyers. Navigating these logistical and financial pressures requires agile operations and diversified sourcing which remain difficult to achieve in a globalized market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.54% |

| Segments Covered | By Type, Application, Distribution Channel, and Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | California, Washington, Oregon, New York & Rest of the United States |

| Market Leaders Profiled | Faber Castell (Germany), Kokuyo Camlin Ltd. (India), Bic Group, STAEDTLER SE (Germany), Rifle Paper Co. (U.S.), Newell Brands (U.S.), Schwan Stabilo (Germany), ITC Limited (India), Navneet Education Limited (India), Ryohin Keikaku Co., Ltd. (MUJI) (Japan), 3M Company (U.S.) |

SEGMENTAL ANALYSIS

By Type Insights

The paper products segment maintained dominance in the United States stationery market in 2025. Its fundamental role in educational administrative and personal organizational activities drives this dominance of the segment. This category includes notebooks loose leaf paper sticky notes and planners which are essential consumables for students and office workers. As per the National Center for Education Statistics approximately 50 million students enroll in public schools annually creating a massive recurring demand for writing pads and composition books. The sheer volume of consumption in academic settings ensures that paper products remain the backbone of the industry despite digital alternatives. According to the Environmental Protection Agency paper and paperboard constitute a significant portion of municipal solid waste indicating the high turnover rate of these items. The versatility of paper allows it to serve multiple functions from note taking to artistic expression making it indispensable across various demographics. Furthermore, the back to school season generates a concentrated spike in sales as families purchase bulk supplies for the academic year. Retailers prioritize shelf space for paper goods due to their fast moving nature and broad appeal. The continued reliance on physical documents for legal contracts tests and creative projects sustains this dominance. Manufacturers benefit from economies of scale in production which keeps prices competitive and accessible. This combination of institutional necessity habitual use and low cost solidifies paper products as the primary revenue generator in the US stationery landscape.

The calligraphy related tools and materials segment is predicted to witness the highest CAGR of 8.5% from 2026 to 2034 due to the rising popularity of hand lettering as a hobby and professional skill. Social media platforms have amplified interest in artistic writing styles encouraging individuals to invest in specialized pens brushes and high quality practice papers. As per Etsy trend reports searches for calligraphy supplies and hand lettering kits have increased significantly reflecting a surge in DIY craft activities among millennials and Gen Z consumers. This creative outlet offers a mindful escape from digital screens appealing to those seeking tangible artistic experiences. According to a study, sales of premium fountain pens, brush markers, and ink sets have outpaced general writing instrument categories, with a projected growth rate exceeding 7.6% as users prioritize aesthetic appeal and "slow writing" craftsmanship. Online tutorials and workshops further fuel this trend by providing accessible learning resources that lower the barrier to entry for beginners. The customization aspect of calligraphy also drives demand for personalized stationery gifts such as wedding invitations and greeting cards. Brands respond by launching curated kits that include guides and diverse nib options to cater to varying skill levels. This convergence of artistic expression social influence and mental wellness positions calligraphy tools as a dynamic and rapidly expanding niche within the broader stationery market.

By Application Insights

The residential segment remained in the lead in the United States stationery market in 2025. This leading position of the segment is attributed to the widespread use of writing and organizational tools for personal education household management and creative hobbies. Consumers purchase stationery for childrens school needs home office setups and leisure activities such as journaling and scrapbooking. As per the Bureau of Labor Statistics time use surveys indicate that Americans spend significant hours on household activities and personal care which often involve planning and organizing using physical tools. The rise of remote work has blurred the lines between professional and personal spaces leading many individuals to equip their homes with comprehensive stationery supplies. According to the National Retail Federation, back-to-school spending reached record levels of $38.8 billion, with families allocating an average of $141.62 specifically to traditional school supplies like notebooks and pens, though electronics remains the top spending category. The emotional connection to handwritten letters and diaries further sustains demand in the personal sector as people seek meaningful ways to document their lives. Additionally, the popularity of home based crafts and DIY projects encourages the purchase of specialized papers and decorative items. Retailers target this segment through seasonal promotions and bundled offerings that appeal to budget conscious households. The sheer number of households engaging in these activities ensures a consistent and high volume of sales. This broad based consumer engagement makes the residential application the primary pillar of the stationery industry.

The commercial segment is estimated to register the fastest CAGR of 6.2% during the forecast period owing to the need for branded corporate identity and efficient office organization. Businesses invest in high quality stationery for client communications internal documentation and promotional purposes to maintain a professional image. As per the Institute for Supply Management procurement indices show that companies are prioritizing supplier relationships that offer customized and sustainable office solutions. The return to office policies has revitalized demand for physical supplies as employees restock their workspaces with personalized items. According to research, the corporate sector is increasingly adopting eco friendly stationery options to align with sustainability goals driving sales of recycled paper and biodegradable pens. Branding opportunities through custom printed notebooks and folders allow companies to reinforce their identity and enhance employee engagement. The need for efficient record keeping in regulated industries also sustains demand for specialized filing and organizational products. Additionally, the hospitality and events sectors utilize premium stationery for invitations menus and signage contributing to market growth. Manufacturers cater to this segment by offering bulk discounts and tailored design services. This focus on professionalism sustainability and branding ensures that the commercial segment expands steadily despite the overall shift toward digital workflows.

By Distribution Channel Insights

The offline distribution channel segment was the largest segment in the United States stationery market in 2025. This supremacy of the segment is credited to the immediate availability of products and the tactile experience of selecting items such as pens and paper. Consumers prefer to test the weight and feel of writing instruments and assess the quality of paper before purchasing which is difficult to achieve online. Specialty retailers and big box stores provide extensive assortments that cater to diverse needs from basic school supplies to premium office gear. The ability to purchase items instantly without waiting for shipping appeals to last minute shoppers and students preparing for exams. Additionally, local bookstores and gift shops contribute to sales by offering curated selections of artisanal and unique stationery products. The social aspect of shopping for school supplies with family members further reinforces the preference for physical retail environments. Retailers enhance this experience through interactive displays and knowledgeable staff who provide recommendations. This combination of sensory evaluation convenience and immediate gratification ensures that offline channels remain the primary destination for stationery purchases.

The online e commerce channel segment is anticipated to witness the fastest CAGR of 9.5% between 2026 and 2034. This rapid growth of the segment is fuelled by the convenience of home delivery and access to a wider variety of niche products. Digital platforms allow consumers to browse extensive catalogs read reviews and compare prices easily which enhances the shopping experience. The availability of subscription services for recurring needs such as printer paper and notebooks fosters customer loyalty and predictable revenue streams. In addition, the ability to access international brands and unique items not available in local stores drives traffic to online marketplaces. Detailed product descriptions and video demonstrations help buyers make informed decisions about quality and functionality. Additionally, competitive pricing and frequent online exclusives attract cost conscious consumers. The integration of mobile apps facilitates seamless purchasing and tracking enhancing user satisfaction. This digital transformation expands market reach and enables personalized shopping experiences that drive rapid growth in the online channel.

COUNTRY LEVEL ANALYSIS

United States Stationery Market Analysis

The United States was the top performer in the stationery market and accounted for a 85.6% share in 2025. This position of the US market is supported by its large population robust educational system and strong consumer culture. High literacy rates and a deep seated tradition of valuing written communication and personal organization also strengthened its dominant position. As per the National Center for Education Statistics (NCES), 49.6 million students were enrolled in public elementary and secondary schools in Fall 2022, providing the demographic base that private industry analysts credit with driving demand for school supplies. The market is characterized by a mature ecosystem where global brands coexist with local artisans and private label retailers offering diverse choices to consumers. According to the Bureau of Labor Statistics (BLS) Employment Projections (2023–2033), employment in Office and Administrative Support occupations is projected to decline by 3.5% due to the adoption of automation and AI, rather than remaining high, while employment in Educational Instruction and Library occupations is projected to grow by 1.6%. Consumer behavior in the US is marked by a blend of practicality and aesthetic appreciation with shoppers seeking both functional efficiency and stylish designs. The presence of major retail chains and specialized online platforms ensures widespread accessibility and competitive pricing. Regulatory frameworks regarding environmental sustainability are increasingly influencing product development with a shift toward recycled materials and eco friendly packaging. High disposable income levels among American households enable sustained spending on premium and hobbyist stationery products. The diversity of the population drives varied preferences encouraging innovation in design and functionality. This robust foundation ensures that the United States remains the central hub for stationery consumption and trend setting in the region influencing global markets through its demand for quality and innovation.

COMPETITIVE LANDSCAPE

The competition in the United States stationery market is intense and characterized by a mix of established global brands and agile niche players vying for consumer attention. Major corporations compete on brand recognition distribution reach and product variety while smaller companies differentiate themselves through unique designs and sustainability practices. The rise of private label brands from major retailers has increased price pressure forcing national brands to innovate and justify premium pricing. Digital transformation has lowered barriers to entry allowing independent creators to sell directly to consumers through online platforms. Consumer preferences are shifting toward eco friendly and aesthetically pleasing products driving companies to invest in sustainable materials and creative collaborations. Seasonal demand spikes during back to school periods create fierce competition for shelf space and promotional visibility. Brand loyalty is increasingly influenced by social media trends and influencer endorsements rather than traditional advertising. This dynamic environment requires continuous adaptation and strategic investment in product development and marketing to maintain relevance and profitability in a saturated market.

KEY MARKET PLAYERS

A few of the market players that are dominating the U.S stationery market are

- Faber Castell (Germany)

- Kokuyo Camlin Ltd. (India)

- Bic Group

- STAEDTLER SE (Germany)

- Rifle Paper Co. (U.S.)

- Newell Brands (U.S.)

- Schwan Stabilo (Germany)

- ITC Limited (India)

- Navneet Education Limited (India)

- Ryohin Keikaku Co., Ltd. (MUJI) (Japan)

- 3M Company (U.S.)

Top Players In The Market

- Newell Brands Inc is a global leader in consumer and commercial products with a strong portfolio of stationery brands including Sharpie Paper Mate and EXPO. The company leverages its extensive distribution network to ensure widespread availability of writing instruments and organizational tools across retail channels. Recent actions include optimizing its supply chain to improve efficiency and reducing costs while investing in sustainable product innovations. Newell focuses on enhancing brand equity through strategic marketing campaigns that highlight product durability and creativity. The firm strengthens its market position by expanding its presence in the premium segment with high quality offerings that appeal to professional and artistic consumers. By prioritizing digital transformation and direct to consumer engagement Newell adapts to changing shopping behaviors. These efforts ensure sustained growth and competitiveness in the global stationery market through continuous innovation and operational excellence.

- Bic Group is a prominent global player known for its iconic writing instruments and disposable lighters with a significant presence in the stationery sector. The company offers a wide range of affordable and reliable pens pencils and markers that cater to diverse consumer needs worldwide. Recent strategies involve expanding its eco friendly product lines by introducing pens made from recycled materials to align with sustainability goals. Bic invests in digital marketing and social media collaborations to engage younger demographics and enhance brand relevance. The firm strengthens its market position through innovative packaging designs and limited edition collections that drive consumer interest. By leveraging its global manufacturing capabilities Bic ensures consistent product quality and availability. These initiatives enable the company to maintain its leadership in the mass market segment while adapting to evolving environmental standards and consumer preferences in the competitive stationery industry.

- Kokuyo Co Ltd is a leading Japanese manufacturer of stationery and office furniture with a growing global footprint in the writing and organizational products market. The company is renowned for its innovative design and high quality notebooks planners and filing systems that emphasize functionality and aesthetics. Recent actions include expanding its international distribution networks and launching digital tools that complement its physical products for enhanced productivity. Kokuyo focuses on sustainability by developing eco friendly materials and reducing plastic usage in its packaging. The firm strengthens its market position through collaborations with designers and artists to create unique and appealing product lines. By prioritizing user centric innovation Kokuyo addresses the evolving needs of modern workers and students. These strategic moves enable the company to capture value in the premium stationery segment and build a loyal customer base globally through superior design and practical solutions.

Top Strategies Used By Key Market Participants

Key players in the United States stationery market prioritize product innovation by developing eco friendly and sustainable items that appeal to environmentally conscious consumers. Companies focus on expanding their digital presence through e commerce platforms and social media marketing to reach younger demographics effectively. Strategic partnerships with influencers and artists help brands create hype and drive demand for limited edition collections. Manufacturers invest in supply chain optimization to reduce costs and improve efficiency amidst raw material volatility. Diversification into premium and artisanal segments allows firms to capture higher margins and differentiate from private label competitors. Enhancing customer experience through personalized services and subscription models fosters loyalty and recurring revenue. These combined approaches enable companies to navigate market challenges and sustain growth in a evolving retail landscape.

MARKET SEGMENTATION

This research report on the U.S stationery market is segmented and sub-segmented into the following categories.

By Type

- Paper Products

- Writing Instruments

- Pens

- Fountain Pens

- Ballpoint Pens

- Gel Pens

- Others

- Pencils

- Graphite Pencils

- Colored Pencils

- Others

- Calligraphy-related Tools & Materials

- Calligraphy Pens

- Dip Nibs

- Inks

- Gilding Supplies

- Calligraphy Pads, Paper,

- and Other Writing Surfaces

- Others

- Art & Craft

- Basic Materials/Supplies

- Marking Materials/Supplies

- Crayons

- Paint

- Watercolors

- Acrylic

- Oil Paints

- Others

- Markers

- General-purpose Markers

- Whiteboard Markers

- Permanent Markers

- Highlighters

- Artistic Markers

- Alcohol-based Markers

- Paint Markers

- Water-based Markers

- Chalk Markers

- Calligraphy & Brush Markers

- Acrylic Markers

- Watercolor Markers

- Fineliner Markers

- Specialized Markers

- Glass Markers

- Fabric Markers

- Retractable Markers

- Dry Erase Markers

- Others

By Application

- Residential

- Commercial

By Distribution Channel

- Offline

- Online/ E-commerce

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

What is currently driving growth in the United States stationery market?

Rising demand for educational supplies and office products is driving market growth.

Why is stationery still relevant in the digital age in the United States?

It supports learning, creativity, and everyday office tasks.

How would you explain stationery in simple terms?

It includes writing, paper, and office supplies used for work and study.

Where are stationery products most commonly used in the United States?

They are widely used in schools, offices, and homes.

What makes stationery important for education and work?

It enables writing, organization, and communication activities.

From a consumer perspective, is stationery a necessary purchase?

Yes, it remains essential for academic and professional use.

What challenges are affecting the United States stationery market?

Digital alternatives and declining paper usage are key challenges.

How is digitalization influencing stationery demand?

Increasing use of digital tools is reducing reliance on traditional products.

Which product segments contribute the most to stationery demand?

Writing instruments, notebooks, and office supplies are major contributors.

Is the United States stationery market growing steadily?

It is growing moderately with stable demand from education and offices.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com