U.S Tea Market Size, Share, Trends & Growth Forecast Report - Segmented By Type, Packaging, End-user, Distributional Channel, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Tea Market Report Summary

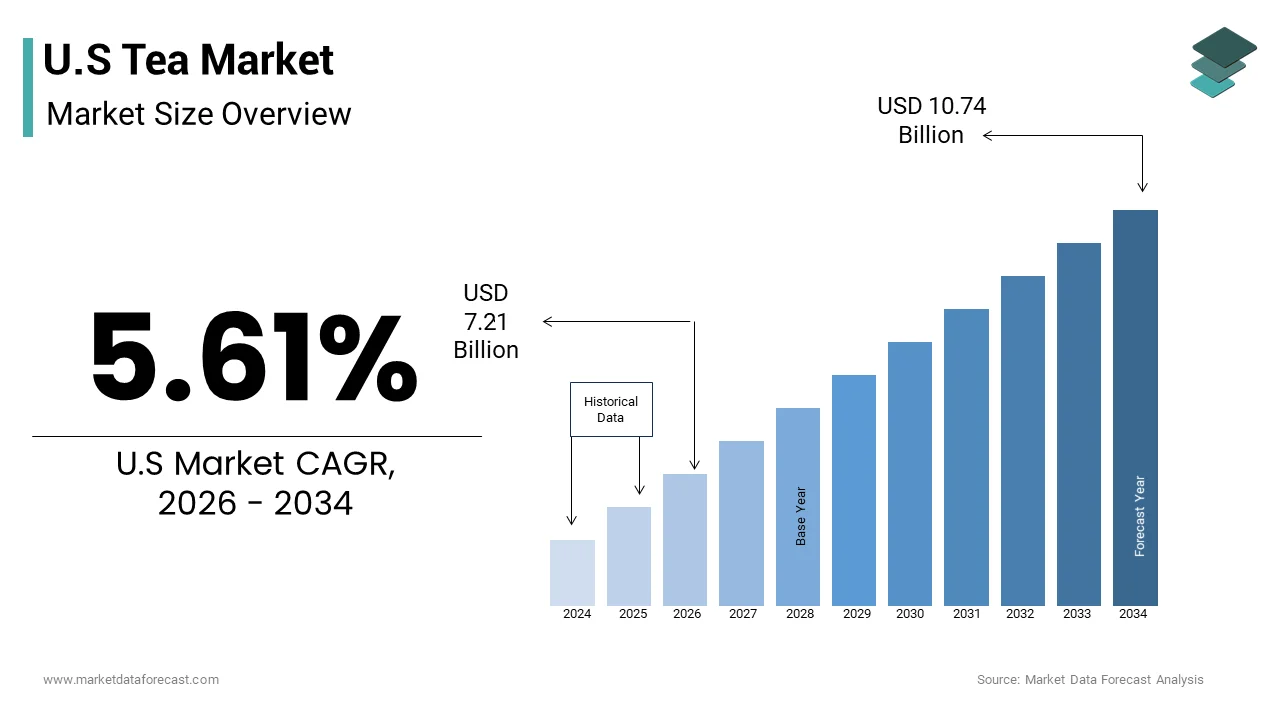

The U.S. tea market was valued at USD 6.83 billion in 2025 and is projected to grow from USD 7.21 billion in 2026 to USD 10.72 billion by 2034, registering a CAGR of 5.64% during the forecast period from 2026 to 2034. The growth of the U.S. tea market is driven by rising health consciousness among consumers, increasing demand for functional and herbal teas, and the growing popularity of ready-to-drink (RTD) tea beverages. Additionally, expanding product innovations, premium tea offerings, and the influence of wellness trends are further accelerating market expansion across the country.

Key Market Trends

- Increasing demand for herbal, green, and functional teas driven by health and wellness awareness.

- Rising popularity of ready-to-drink (RTD) tea beverages offering convenience and diverse flavor options.

- Growing consumer preference for premium and organic tea products with natural ingredients.

- Expansion of specialty tea brands and artisanal blends catering to niche consumer segments.

- Increasing adoption of sustainable packaging and ethically sourced tea products.

Segmental Insights

By Type

The black tea segment dominated the U.S. tea market in 2025, supported by its widespread consumption, strong flavor profile, and established presence across both traditional and modern tea consumers.

By Packaging

The tea bags segment held a 31.5% share of the market in 2025, driven by convenience, ease of use, and affordability, making it the preferred choice for daily consumption.

By End User

The residential segment accounted for the largest share at 61.9% in 2025, fueled by high at-home consumption trends and increasing preference for tea as a daily beverage.

By Distribution Channel

The supermarkets and hypermarkets segment led the market with a 44.7% share in 2025, supported by strong retail presence, product variety, and easy accessibility for consumers.

Regional Insights

The United States accounted for a 14.2% share of the global tea market in 2025, making it one of the leading contributors worldwide. Market growth is supported by increasing consumer awareness of tea’s health benefits, strong retail infrastructure, and rising demand for innovative and premium tea products. Urban consumers and younger demographics are playing a key role in driving market expansion through evolving consumption habits.

Competitive Landscape

The U.S. tea market is highly competitive, with key players focusing on product innovation, premiumization, and sustainable sourcing to strengthen their market position. Companies are expanding their portfolios with functional teas, RTD beverages, and organic variants while leveraging strong distribution networks and digital marketing strategies. Major players operating in the market include PepsiCo, Yorkshire Tea, Tata Consumer Products Limited, Ito En Ltd, Starbucks Coffee Company, Dilmah Ceylon Tea Company PLC, Bigelow Tea, Caraway Tea, Harris Freeman, The Republic of Tea, Twinings and Company Limited, and Unilever.

U.S Tea Market Size

The U.S tea market size was valued at USD 6.83 billion in 2025 and is anticipated to reach USD 7.21 billion in 2026 to reach USD 10.72 billion by 2034, growing at a CAGR of 5.64% during the forecast period from 2026 to 2034.

Current Market Overview and Definition

Tea is a drink made by steeping the leaves of the Camellia sinensis plant in hot or boiling water. This sector has evolved significantly from a commodity driven industry to a diverse landscape characterized by premiumization, functional benefits, and varied preparation methods. Tea is consumed in multiple formats including hot bagged tea, loose leaf, ready to drink bottled varieties, and concentrated liquid extracts. According to the Tea Association of the USA, tea is found in about 80 percent of U.S. households, and approximately 159 million Americans drink tea on any given day, indicating its widespread popularity. The market is distinguished by a strong preference for iced tea, which accounts for a substantial majority of total volume consumption due to the country's warm climate and cultural affinity for cold beverages. As per U.S. Census Bureau and USDA trade data (2024), the United States imports nearly 100% of its tea, relying heavily on sources such as Argentina, China, India, and Japan. Consumer trends indicate a shift toward health conscious choices with increased demand for organic, non GMO, and functional teas that offer specific wellness benefits. The regulatory environment ensures strict labeling standards regarding caffeine content and ingredient sourcing. The industry also faces growing scrutiny regarding sustainability practices in sourcing and packaging. This dynamic market requires stakeholders to balance traditional consumption patterns with innovative product developments that appeal to younger demographics seeking convenience and transparency.

MARKET DRIVERS

Rising Health Consciousness and Functional Benefits

The rising health consciousness among American consumers drives the growth of the United States tea market. Individuals are increasingly seeking natural beverages with proven wellness benefits. Tea is rich in antioxidants, particularly polyphenols, which are associated with reduced risks of chronic diseases and improved cardiovascular health. According to the National Institutes of Health, regular consumption of green and black tea has been linked to lower levels of inflammation and improved metabolic function. As per the 2024 International Food Information Council (IFIC) Food & Health Survey, 66% of consumers are trying to limit or avoid sugars to improve their diet, primarily choosing water and low-calorie beverages. The popularity of herbal teas such as chamomile, peppermint, and ginger has surged due to their perceived ability to aid digestion, reduce stress, and improve sleep quality. Functional teas infused with adaptogens, probiotics, and vitamins are gaining traction among health enthusiasts who view beverages as a vehicle for nutritional supplementation. Retailers respond by expanding their offerings of organic and clean label teas that align with these wellness trends. Marketing campaigns emphasize the natural origins and health promoting properties of tea, resonating with educated shoppers. This shift toward preventive healthcare and holistic wellness ensures that tea remains a preferred choice for consumers seeking both hydration and functional benefits.

Convenience and Growth of Ready to Drink Formats

The demand for convenience and the rapid growth of ready to drink (RTD) tea formats contributed to the expansion of the United States tea market. Busy lifestyles and the need for on the go hydration have led consumers to prefer pre packaged beverages that require no preparation. According to the Beverage Marketing Corporation (2025), while RTD tea retail dollars have grown, sales volumes declined in both 2023 and 2024, lagging behind faster-growing segments like bottled water and energy drinks. As per sources, single serve bottles and cans of iced tea are popular purchases in convenience stores and vending machines, appealing to students, workers, and travelers. The variety of flavors and formulations available in RTD teas, including sparkling teas and tea lemonades, attracts younger demographics who seek novel taste experiences. Brands are innovating with reduced sugar options and natural sweeteners to address health concerns while maintaining convenience. The portability of RTD teas makes them ideal for outdoor activities, sports, and social gatherings where brewing facilities are unavailable. Retailers dedicate prominent shelf space to these products, recognizing their high turnover rates and impulse purchase potential. The integration of RTD teas into meal kits and subscription services further enhances accessibility. This focus on ease of use and immediate consumption ensures that the RTD segment continues to expand, driving overall market growth.

MARKET RESTRAINTS

Competition from Coffee and Other Beverages

Intense competition from coffee and other alternative beverages restricts the growth of the United States tea market. This limits its potential for volume growth. Coffee culture remains deeply entrenched in American society, with many consumers preferring the higher caffeine content and robust flavor profile of coffee for morning routines. According to the National Coffee Association, daily coffee consumption rates exceed those of tea, particularly among working adults who rely on coffee for energy and focus. A study confirms the specialty coffee sector generates significantly higher revenue per capita than the tea sector in the U.S., driven by the proliferation of coffee shops, which maintain a dominant share of the out-of-home hot drinks market. Additionally, the rise of energy drinks, sparkling waters, and functional sodas offers alternative hydration options that appeal to similar health conscious and convenience seeking demographics. These beverages often feature bold marketing campaigns and innovative flavors that capture the attention of younger consumers. The perception of tea as a less stimulating or less exciting beverage compared to coffee or energy drinks can hinder its adoption among certain groups. Retail shelf space is limited, and tea brands must compete fiercely for visibility against established coffee and soda giants. This saturated beverage environment requires tea manufacturers to differentiate their products through unique value propositions, which can be challenging and costly. The dominance of coffee and other alternatives thus constrains the expansion of the tea market.

Perception of Lower Quality in Mass Market Products

The perception of lower quality in mass market tea products constrains the expansion of the United States tea market. This discourages premiumization and limits consumer engagement. Many Americans associate tea with inexpensive tea bags containing dust and fannings, which are viewed as inferior to loose leaf or whole leaf varieties. Market experts and the Tea Association of the U.S.A. note that the dominance of commodity-grade tea bags in retail channels presents a significant challenge to premiumization, as it anchors consumer price expectations and limits exposure to specialty tea's diverse flavor profiles. As per research, the price gap between tea and coffee is largely driven by coffee's positioning as a high-value functional energy beverage, whereas tea is often perceived as a low-cost, at-home wellness staple, limiting consumer willingness to pay premium prices in foodservice settings. This perception is reinforced by the widespread availability of flavored teas with artificial ingredients and high sugar content, which detract from the natural appeal of the beverage. The lack of standardization in grading and labeling further confuses shoppers, making it difficult for them to distinguish between high and low quality options. Consequently, many consumers remain loyal to basic brands without exploring the broader spectrum of tea varieties. Efforts by artisanal brands to elevate the image of tea face an uphill battle against entrenched stereotypes. The market must shift consumer perceptions toward quality and authenticity. Until then, the market will struggle to achieve the same level of prestige and pricing power as the coffee sector.

MARKET OPPORTUNITIES

Expansion of Premium and Specialty Tea Segments

The proliferation of premium and specialty tea segments opens new doors for the growth of the United States tea market. This caters to discerning consumers seeking unique and high quality experiences. There is a growing interest in single origin teas, rare varietals, and artisanal blends that offer distinct flavor profiles and storytelling elements. According to the Specialty Food Association, sales of specialty teas have outpaced general market growth, driven by consumers willing to pay for authenticity and craftsmanship. As per the Tea Association of the USA, interest in specialty and loose leaf tea is growing, largely driven by the health and wellness trend, sustainability concerns, and a shift toward premium at-home consumption. Retailers are responding by creating dedicated tea sections with knowledgeable staff who can guide customers through selections. Online platforms enable niche brands to reach national audiences, offering subscription boxes and curated sets that encourage exploration. The rise of tea ceremonies and tasting events fosters community and deepens appreciation for the cultural heritage of tea. Brands that emphasize sustainable sourcing, fair trade practices, and direct relationships with farmers resonate with ethically conscious buyers. The opportunity to position tea as a luxury lifestyle product allows for higher margins and brand loyalty. The market can attract affluent consumers by focusing on quality and exclusivity. Consequently, this will elevate the overall perception of tea in the market.

Innovation in Functional and Adaptogenic Blends

Innovation in functional and adaptogenic blends provides big chances for the expansion of the United States tea market. These innovations align with the wellness trend and demand for personalized nutrition. Consumers are increasingly seeking beverages that provide specific health benefits such as stress relief, immune support, and enhanced focus. According to the Global Wellness Institute, the global wellness economy reached $6.8 trillion in 2024, with functional teas representing a growing product segment within the Healthy Eating, Nutrition, & Weight Loss sector. As per a study, launches of teas containing functional ingredients like ashwagandha, turmeric, and adaptogens have increased significantly, appealing to health-conscious individuals seeking immunity and stress-relief benefits. These blends offer a natural alternative to supplements and pharmaceuticals, fitting seamlessly into daily routines. Brands are collaborating with nutritionists and herbalists to develop scientifically backed formulations that deliver tangible benefits. Packaging innovations such as pyramid bags and biodegradable materials enhance the premium feel and environmental appeal of these products. Retailers are highlighting functional claims on shelves, attracting shoppers looking for targeted solutions. The versatility of herbal and botanical ingredients allows for continuous innovation and flavor experimentation. By positioning tea as a functional tool for well being, manufacturers can tap into new revenue streams and differentiate themselves in a crowded market. This trend ensures sustained growth and relevance in the evolving health landscape.

MARKET CHALLENGES

Supply Chain Vulnerabilities and Climate Change

Supply chain vulnerabilities and the impacts of climate change challenge the growth of the United States tea market. This threatens the stability and quality of raw material supplies. Since the US relies entirely on imports, any disruption in producing countries directly affects availability and pricing. According to the Food and Agriculture Organization of the United Nations, changing weather patterns including droughts and excessive rainfall are reducing yields in key tea growing regions such as India and Kenya. As per the Intergovernmental Panel on Climate Change, rising temperatures are altering the chemical composition of tea leaves, potentially affecting flavor and antioxidant levels. These environmental stressors increase the risk of crop failures and price volatility, making it difficult for manufacturers to maintain consistent product quality and cost structures. Political instability and labor issues in producing countries further exacerbate supply chain risks. The reliance on long distance transportation also exposes the industry to logistical bottlenecks and fuel cost fluctuations. Companies must invest in diversified sourcing strategies and sustainable farming initiatives to mitigate these risks, which requires significant capital and coordination. The uncertainty surrounding future supply conditions challenges long term planning and investment. Addressing these environmental and logistical issues is critical for ensuring the resilience and continuity of the tea market.

Regulatory Complexity and Labeling Standards

Regulatory complexity and inconsistent labeling standards slow down the expansion of the United States tea market. This creates compliance burdens and consumer confusion. The classification of tea as either a food or a dietary supplement depends on its intended use and claims, leading to varying regulatory requirements. According to the Food and Drug Administration, making health claims on tea packaging requires rigorous scientific substantiation and approval, which can be costly and time consuming for manufacturers. As per the Federal Trade Commission, advertising standards for natural and organic claims are strictly enforced, requiring precise documentation and certification. The lack of uniform definitions for terms such as herbal, botanical, and functional creates ambiguity for consumers and regulators alike. Small businesses often struggle to navigate these complex regulations, limiting their ability to innovate and market effectively. Additionally, varying state laws regarding labeling and sales add another layer of complexity for national distribution. The threat of litigation over misleading labels or unsubstantiated claims poses a financial risk to companies. Ensuring compliance while maintaining clear and appealing messaging requires careful legal oversight and strategic planning. This regulatory landscape acts as a barrier to entry and growth, particularly for smaller and emerging brands seeking to establish themselves in the competitive market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.64% |

| Segments Covered | By Type, Packaging, End-user, Distributional Channel, and Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | California, Washington, Oregon, New York & Rest of the United States |

| Market Leaders Profiled | PepsiCo, Yorkshire Tea, Tata Consumer Products Limited, Ito En Ltd, Starbucks Coffee Company, Dilmah Ceylon Tea Company PLC, Bigelow Tea, Caraway Tea, Harris Freeman, The Republic of Tea, Twinings and Company Limited, Unilever. |

SEGMENTAL ANALYSIS

By Type Insights

In 2025, the black tea segment remained in the lead in the United States tea market and captured a substantial share. This leading position of the segment is attributed to its overwhelming dominance in the ready to drink and iced tea categories. The American preference for cold beverages drives the vast majority of tea consumption volume, with black tea serving as the base for most commercial iced teas. According to the Tea Association of the USA, approximately 80 percent of all tea consumed in the United States is iced, and black tea accounts for the largest share of this segment. As per NielsenIQ data, black tea based ready to drink products consistently top sales charts in the bottled beverage aisle, driven by brands that offer consistent flavor and affordability. The robust flavor profile of black tea stands up well to dilution with ice and sweeteners, making it ideal for mass market formulations. Its high caffeine content also appeals to consumers seeking an energy boost comparable to coffee but with a smoother delivery. The established supply chain for black tea ensures low costs and widespread availability, reinforcing its status as the default choice for households and foodservice operators. This entrenched position in the high volume iced tea sector ensures that black tea remains the undisputed leader in terms of total consumption volume across the country. The cultural entrenchment of black tea as a morning staple and its popularity in breakfast blends further drive its market domination. Many American consumers associate black tea with traditional morning routines, often consuming it with milk and sugar as a substitute for or complement to coffee. As per the Specialty Tea Institute, classic black tea varieties such as English Breakfast and Earl Grey remain the best selling loose leaf and bagged options in retail stores. The familiarity of these blends lowers the barrier to entry for new tea drinkers who may find green or herbal teas less approachable. Major tea brands heavily market black tea as a reliable and comforting option, leveraging decades of brand loyalty. The versatility of black tea in baking and cooking also contributes to its household penetration. Retailers allocate prime shelf space to black tea products, ensuring high visibility and easy access. This deep rooted habit and broad acceptance across age groups sustain the high volume sales that define the black tea segment’s leadership in the US market.

The green tea segment is estimated to register the fastest CAGR of 7.3% over the forecast period. This rapid growth of the segment is propelled by heightened health consciousness and the demand for antioxidant rich beverages. Consumers are increasingly aware of the potential health benefits of green tea, including weight management, improved heart health, and cancer prevention properties. According to the National Institutes of Health, green tea is rich in catechins, particularly epigallocatechin gallate, which are powerful antioxidants linked to various health improvements. As per the International Food Information Council, a growing number of Americans are actively seeking functional foods and beverages that support wellness goals, leading to increased adoption of green tea. The perception of green tea as a metabolism booster has made it popular among fitness enthusiasts and those following dietary plans. Retailers have expanded their green tea offerings to include matcha, sencha, and jasmine varieties, catering to diverse taste preferences. Marketing campaigns emphasize the natural and clean label aspects of green tea, appealing to health focused demographics. The rise of green tea based supplements and beauty products further reinforces its image as a holistic health solution. This strong association with wellness ensures that green tea continues to experience robust growth rates compared to other tea types. Innovation in matcha and premium green tea formats significantly accelerates the growth of this segment. Matcha, a powdered form of green tea, has gained immense popularity due to its vibrant color, unique flavor, and versatility in culinary applications. According to the Specialty Food Association, matcha has become a staple in cafes and restaurants, featured in lattes, smoothies, and desserts. The convenience of matcha powder allows for easy integration into daily routines, appealing to busy professionals. Premium green tea brands are also launching single origin and organic options that cater to discerning palates seeking authenticity and quality. The aesthetic appeal of matcha and high grade green teas makes them highly shareable on social media, driving organic marketing and trial. Retailers are dedicating more shelf space to premium green tea products, recognizing their higher margin potential. The continuous innovation in flavors and formats keeps the segment dynamic and engaging. This combination of culinary trendiness and premium positioning ensures that green tea remains the fastest growing category in the US tea market.

By Packaging Insights

The tea bags segment maintained dominance in the United States tea market and accounted for a 31.5% share in 2025. This dominance of the segment is driven by its unparalleled convenience and ease of preparation. The fast paced lifestyle of American consumers favors quick and mess free brewing methods, which tea bags provide efficiently. According to the Tea Association of the USA, tea bags account for the majority of hot tea sales in retail channels, reflecting the consumer preference for simplicity. The ability to brew a consistent cup of tea without measuring loose leaves or using specialized equipment appeals to casual drinkers and offices alike. Tea bags are also portable, making them ideal for travel and workplace consumption. Major brands have optimized tea bag designs to improve water flow and flavor extraction, addressing previous concerns about quality. The familiarity of tea bags reduces the learning curve for new tea consumers, encouraging trial and repeat purchases. Retailers benefit from the high turnover rate of tea boxes, ensuring steady revenue. This combination of practicality and accessibility solidifies tea bags as the leading packaging format in the market. The cost efficiency and mass market appeal of tea bags significantly contribute to their market leadership. Producing and packaging tea bags is generally less expensive than loose leaf or premium formats, allowing for competitive pricing that attracts budget conscious shoppers. The standardized nature of tea bags facilitates efficient manufacturing and distribution, reducing logistical costs for producers. This economic advantage enables major brands to invest in extensive marketing campaigns that reinforce brand loyalty. The wide variety of flavors available in tea bag format ensures that there is an option for every preference, from classic black to fruity herbal blends. Retail promotions often feature tea bags, driving volume sales during key shopping periods. The balance of low cost and acceptable quality ensures that tea bags remain the primary choice for the majority of American tea drinkers.

The loose tea segment is anticipated to witness the fastest CAGR of 6.4% between 2026 and 2034 due to the trend toward premiumization and the appeal of artisanal products. Consumers are increasingly seeking high quality whole leaf teas that offer superior flavor and aroma compared to bagged alternatives. The ritual of brewing loose tea using infusers or teapots enhances the sensory experience, appealing to enthusiasts who value mindfulness and tradition. Specialty retailers and online platforms have made loose tea more accessible, offering detailed descriptions and brewing guides. The rise of tea shops and cafes that serve loose leaf beverages has also influenced home consumption habits. Brands emphasize sustainability and ethical sourcing in their loose tea offerings, resonating with conscientious buyers. This shift toward quality and experience ensures that the loose tea segment continues to expand rapidly. Environmental sustainability and the desire to reduce waste accelerate the growth of the loose tea segment. Many consumers are moving away from tea bags due to concerns about microplastics and non biodegradable materials used in their construction. Brands are responding by offering loose tea in glass jars, metal tins, and paper pouches that align with eco friendly values. The ability to reuse brewing equipment such as teapots and infusers further reduces environmental impact. Social media campaigns highlighting the ecological benefits of loose tea resonate with younger demographics who prioritize sustainability. Retailers are expanding their bulk bins and zero waste sections, facilitating loose tea purchases. This alignment with environmental ethics ensures that loose tea remains a dynamic and rapidly growing segment in the market.

By End Users Insights

The residential segment held the majority share of 61.9% of the United States tea market in 2025. This supremacy of the segment is credited to high household penetration and the establishment of tea drinking as a daily habit. A vast majority of American homes keep tea in stock for regular consumption, making it a staple pantry item. The affordability and ease of brewing tea at home make it an attractive option for families and individuals. The rise of remote work has further increased home consumption, as people seek comforting beverages during the day. Retailers offer a wide variety of tea products tailored to residential needs, from bulk boxes to specialty blends. The emotional connection to tea as a source of relaxation and warmth reinforces its presence in households. This consistent and widespread domestic demand ensures that the residential segment remains the dominant end user category. The ability to customize tea preparation to personal preference drives the dominance of the residential segment. At home, consumers have the freedom to adjust strength, sweetness, and additives such as milk or lemon to suit their tastes. The availability of specialized equipment such as electric kettles and infusers enhances the home brewing experience. Online communities and social media platforms provide recipes and tips that encourage experimentation and engagement. This level of control and personalization fosters a deeper connection to the product, leading to higher loyalty and repeat purchases. The residential setting allows for a more intimate and relaxed tea drinking experience, which appeals to many consumers. This flexibility and personal touch ensure that the residential segment continues to lead the market.

The food service segment is likely to experience the fastest CAGR of 4.8% during the forecast period owing to the expansion of cafe culture and the proliferation of specialty tea shops. Consumers are increasingly visiting establishments that offer high quality brewed teas and innovative tea based beverages. These establishments offer an experiential aspect that cannot be replicated at home, including professional brewing techniques and unique flavor combinations. The social atmosphere of tea shops encourages group visits and extended stays, boosting sales volume. Menu innovation in food service includes seasonal specials and limited time offers that create urgency and excitement. The visibility of tea in trendy urban centers influences consumer perceptions and encourages trial. This vibrant and evolving food service landscape ensures that the segment continues to grow rapidly. The integration of tea into restaurant menus and culinary trends accelerates the growth of the food service segment. Chefs and bartenders are incorporating tea into cocktails, desserts, and savory dishes, showcasing its versatility and complexity. Restaurants are educating staff about tea varieties to enhance service and recommendations. The inclusion of premium teas on beverage lists elevates the dining experience and attracts discerning customers. Collaborations between tea brands and restaurants create exclusive offerings that drive interest and sales. The trend toward healthy and natural ingredients in dining supports the adoption of tea based options. This culinary integration ensures that the food service segment remains a dynamic and high growth area in the tea market.

By Distribution Channel Insights

The supermarkets and hypermarkets segment was the largest segment in the United States tea market and occupied a share of 44.7% in 2025. This prominence of the segment is supported its wide accessibility and the convenience of one stop shopping. Most consumers purchase tea during their regular grocery trips, making these stores the primary source for tea products. The presence of national brands and private labels ensures competitive pricing and availability. Promotional activities such as discounts and displays drive impulse purchases and volume sales. The familiarity and trust associated with established grocery chains encourage repeat business. The ability to buy tea alongside other essentials simplifies the shopping process for busy families. This widespread presence and convenience solidify supermarkets and hypermarkets as the leading distribution channel. The established supply chains and efficient inventory management of supermarkets and hypermarkets significantly contribute to their market leadership. These retailers have robust logistics networks that ensure consistent stock levels and timely replenishment of tea products. The reliability builds consumer confidence and encourages loyal shopping habits. The ability to handle large volumes allows supermarkets to negotiate favorable terms with suppliers, resulting in competitive pricing. Advanced warehousing and distribution centers enable rapid turnover of perishable and seasonal tea items. The integration of technology in store operations enhances the shopping experience through self checkout and mobile apps. These operational efficiencies support the dominance of supermarkets and hypermarkets in the tea market.

The online stores segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 10.2% between 2026 and 2034. This swift growth is fuelled by the overall growth of e commerce and the rise of direct to consumer models. Consumers appreciate the convenience of ordering tea online and having it delivered to their doorstep. Subscription services provide recurring revenue streams and ensure consistent supply for regular drinkers. The ability to read reviews and compare products online enhances the shopping experience. Digital marketing and social media campaigns drive traffic to online stores, influencing purchasing decisions. The pandemic accelerated the shift to online shopping, a trend that has persisted post lockdown. This digital transformation allows retailers to reach customers beyond their geographic footprint, expanding market potential. Personalization and educational content available through online stores accelerate their growth in the tea market. E commerce platforms leverage data analytics to recommend products based on past purchases and preferences. Virtual tastings and live chats with tea experts enhance engagement and loyalty. The ability to curate custom boxes and samples allows customers to explore new varieties with low risk. Online communities and forums foster a sense of belonging among tea enthusiasts. The seamless integration of payment and delivery options simplifies the purchasing process. These features create a superior shopping experience that traditional retail channels struggle to match. The continuous innovation in digital tools ensures that online stores remain a dynamic and rapidly expanding channel.

COUNTRY ANALYSIS

United States Tea Market Analysis

The United States was the top performer in the global tea market and captured a 14.2% share in 2025. This dominance of the US market is driven by a heavy reliance on imports, as domestic production is minimal, and a strong preference for iced and ready to drink formats. According to the United States Department of Agriculture, the US imports nearly all of its tea supply, primarily from Argentina, China, and India, to meet domestic demand. As per the Tea Association of the USA, the country is one of the largest consumers of tea worldwide, driven by a culture of convenience and health consciousness. The market is influenced by trending wellness lifestyles, which fuel demand for herbal, green, and functional teas. Regulatory frameworks enforced by the Food and Drug Administration play a critical role in ensuring safety and labeling accuracy. The presence of major multinational beverage companies fosters intense competition and drives innovation in product formats. The country serves as a trendsetter for ready to drink innovations, influencing global market dynamics. Investment in sustainable sourcing and packaging practices addresses environmental concerns and enhances brand reputation. The mature retail infrastructure ensures widespread distribution, from supermarkets to specialty online stores. This combination of high import volume, diverse consumption habits, and regulatory oversight defines the unique status of the US tea market in the global landscape.

COMPETITIVE LANDSCAPE

The competition in the United States tea market is intense and characterized by a mix of large multinational corporations and specialized artisanal brands. Major players compete on the basis of brand recognition product quality price and distribution efficiency to secure shelf space and consumer loyalty. The market sees frequent innovation as companies strive to differentiate their offerings through unique flavors health benefits and sustainable packaging. Private label brands pose a significant challenge to national brands by offering lower priced alternatives that appeal to budget conscious shoppers. Artisanal and organic tea makers contribute to market diversity by catering to niche segments seeking high quality and authentic products. Consolidation through mergers and acquisitions is common as larger firms seek to expand their portfolios and achieve economies of scale. Regulatory compliance and food safety standards also influence competitive dynamics requiring continuous investment in quality assurance. The rise of health and wellness trends drives demand for functional and herbal options prompting reformulation efforts. This dynamic landscape requires agility and strategic foresight to navigate changing preferences and maintain market relevance effectively.

KEY MARKET PLAYERS

A few of the market players that are dominating the U.S tea market are

- PepsiCo

- Yorkshire Tea

- Tata Consumer Products Limited

- Ito En Ltd

- Starbucks Coffee Company

- Dilmah Ceylon Tea Company PLC

- Bigelow Tea

- Caraway Tea

- Harris Freeman

- The Republic of Tea

- Twinings and Company Limited

- Unilever

Top Players In The Market

- The Unilever Group is a global consumer goods giant with a significant presence in the tea industry through its Lipton and Tazo brands. The company leverages its extensive distribution network to ensure widespread availability of tea products across retail and foodservice channels globally. Recent actions include the strategic partnership with CVC Capital Partners to form Ekaterra, which allows for focused innovation and agility in the tea sector. Unilever continues to emphasize sustainability by sourcing all tea from Rainforest Alliance Certified estates. This commitment enhances brand reputation and appeals to environmentally conscious consumers. The company invests heavily in digital marketing and product diversification to capture emerging trends such as herbal and functional teas. These initiatives strengthen its market position by maintaining relevance and driving growth in a competitive landscape.

- Tata Consumer Products Limited is a leading international tea company known for its iconic Tetley brand and strong foothold in the Indian market. The company operates globally with a diverse portfolio that includes green black and herbal teas. Tata Consumer focuses on premiumization and health oriented products to meet evolving consumer preferences. Recent actions involve acquiring specialty tea brands and expanding into ready to drink segments to broaden its appeal. The company prioritizes sustainable sourcing and community development programs to support tea growers. These efforts reinforce its commitment to ethical practices and quality assurance. Tata Consumer leverages its robust supply chain to maintain consistent product availability and competitive pricing. By fostering innovation and cultural relevance the company strengthens its global standing and drives long term value creation.

- Ito En Ltd is a prominent Japanese beverage company recognized as a global leader in green tea production and distribution. The company is renowned for its high quality oolong and green tea products sold under the Oi Ocha brand. Ito En operates vertically integrated facilities that ensure control over quality from leaf to bottle. Recent actions include expanding manufacturing capabilities in North America and Europe to meet rising international demand. The company emphasizes technological innovation in extraction and packaging to preserve freshness and flavor. Ito En also promotes the health benefits of green tea through educational campaigns and partnerships. These strategies enhance brand loyalty and attract health conscious consumers worldwide. By maintaining strict quality standards and pursuing global expansion Ito En solidifies its position as a key player in the international tea market.

Top Strategies Used By Key Market Participants

Key players in the United States tea market employ several major strategies to maintain competitiveness and drive growth. Product innovation is central to these efforts with companies developing functional herbal blends and ready to drink options to appeal to health conscious consumers. Sustainability initiatives such as ethical sourcing and eco friendly packaging enhance brand reputation and meet regulatory expectations. Strategic partnerships and acquisitions allow firms to expand their portfolios and access niche markets with high growth potential. Digital marketing and e commerce integration help companies reach direct consumers and gather valuable data on purchasing behavior. Premiumization strategies focus on high quality loose leaf and specialty teas to capture value driven segments. These combined strategies enable participants to adapt to market dynamics and sustain long term profitability in a highly competitive environment.

MARKET SEGMENTATION

This research report on the U.S tea market is segmented and sub-segmented into the following categories.

By Type

- Black Tea

- Green Tea

- Fruit/Herbal Tea

- Oolong Tea

- Others

By Packaging Type

- Loose Tea

- Paperboards

- Tea Bags

- Plastic Containers

- Aluminium Tins

By End-user

- Residential

- Food Service

- Institutional

By Price Point

- Economy

- Mid range

- Premium

- Luxury

By Distribution Channel

- Supermarkets/ Hypermarkets

- Specialty Stores

- Convenience Stores

- Online Stores

- Bulk Suppliers

- Others

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

What is currently driving growth in the United States tea market?

Rising health awareness and demand for functional beverages are driving market growth.

Why is tea consumption increasing in the United States?

Consumers are choosing healthier and low-calorie beverage options.

How would you explain the tea market in simple terms?

It involves the production and sale of tea products for consumption.

Where is tea most commonly consumed in the United States?

It is widely consumed at home, workplaces, and food service outlets.

What makes tea important in modern consumer lifestyles?

It offers health benefits and a variety of flavors for different preferences.

From a consumer perspective, is tea a preferred beverage choice?

Yes, many consumers prefer it for its health and refreshment value.

What challenges are affecting the United States tea market?

Competition from other beverages and fluctuating raw material prices are key challenges.

How is health awareness influencing tea consumption?

Consumers are increasingly choosing herbal and functional teas.

Which tea types contribute the most to market demand?

Black tea, green tea, and herbal tea are major contributors.

Is the United States tea market growing steadily?

Yes, it is expanding with increasing demand for premium and specialty teas.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com