U.S. Toy Market Size, Share, Trends, and Growth Analysis Report, Segmented by Product Type, Age Group, Sales Channel, and Country – Industry Forecast From 2026 to 2034

U.S. Toy Market Report Summary

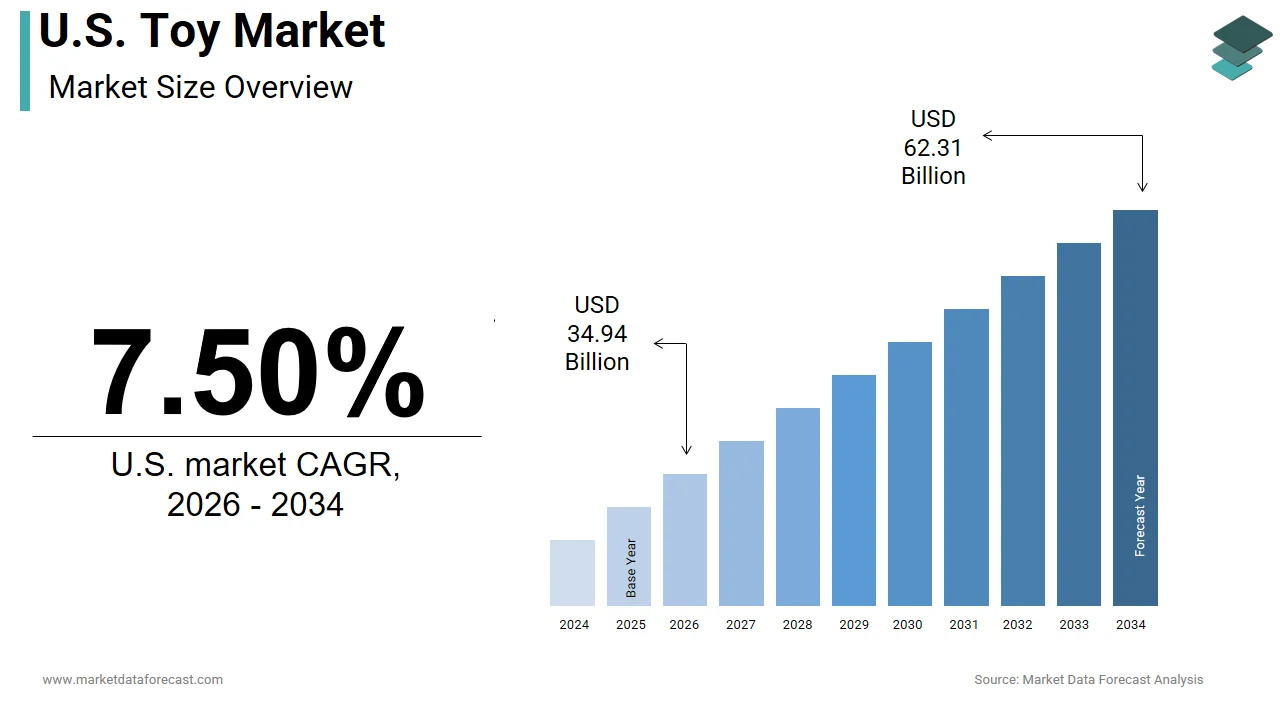

The U.S. toy market was valued at USD 32.50 billion in 2025, is estimated to reach USD 34.94 billion in 2026, and is projected to reach USD 62.31 billion by 2034, growing at a CAGR of 7.50% from 2026 to 2034. Market growth is driven by increasing demand for educational and interactive toys, rising influence of digital entertainment, and strong consumer spending on children’s products. The integration of technology such as augmented reality (AR), artificial intelligence (AI), and connected play experiences is reshaping the toy industry. Additionally, the growth of e-commerce and licensing partnerships with entertainment franchises is further boosting market expansion.

Key Market Trends

- Rising demand for educational and STEM-based toys.

- Increasing integration of digital and interactive technologies.

- Growth of licensed toys linked to movies and entertainment franchises.

- Expansion of e-commerce and online toy retailing.

- Increasing focus on innovative and experiential play.

Segmental Insights

- Based on product type, the building sets segment dominated the United States toy market in 2025, driven by strong demand for creative and educational play.

- Based on age group, the up to 5 years segment held the largest share in 2025, supported by high spending on early childhood development toys.

- Based on sales channel, the online stores segment led the market in 2025, driven by convenience, wide product selection, and competitive pricing.

Country-Level Insights

- The United States led the North American toy market by holding 40.5% share in 2025, supported by strong consumer demand, high disposable income, and a well-established retail ecosystem. The country continues to dominate due to its innovation-driven toy industry and growing adoption of digital play experiences.

Competitive Landscape

The U.S. toy market is highly competitive, with companies focusing on product innovation, brand collaborations, and expanding digital engagement. Licensing agreements with major entertainment brands and continuous product launches are key strategies.

Prominent companies operating in the U.S. toy market include The LEGO Group, Mattel, Hasbro, Bandai Namco Holdings Inc., Spin Master, Funko, MGA Entertainment Inc., and VTech Holdings Limited.

U.S. Toy Market Size

The U.S. toy market was valued at USD 32.50 billion in 2025, is estimated to reach USD 34.94 billion in 2026, and is projected to reach USD 62.31 billion by 2034, growing at a CAGR of 7.50% from 2026 to 2034.

A toy is generally defined as any object designed, manufactured, or marketed as a plaything for children. This market includes traditional categories such as dolls, action figures, and board games, alongside modern interactive electronics and construction sets. As per the US Census Bureau, there are approximately 73 million children under the age of 18 in the country, representing a substantial demographic base for consumer goods. The market is defined by seasonal volatility, with a significant portion of annual sales occurring during the fourth quarter holiday season. According to the Bureau of Labor Statistics and industry data, household expenditure on toys and games averages approximately $450 per year, though this rises to over $580 for households with children. The industry operates within a complex regulatory environment governed by the Consumer Product Safety Commission, which enforces strict standards for material safety and choking hazards. Consumer behavior is increasingly influenced by digital media franchises where movies and video games drive demand for associated physical merchandise. Research indicates that 95 percent of teenagers have access to smartphones, facilitating a hybrid play environment where digital and physical experiences intersect. The definition of this market now extends to include educational tools and STEM-related products as parents prioritize cognitive development. Understanding this landscape requires analyzing the interplay between licensing agreements, retail dynamics, and evolving parental preferences for sustainable and educational play options.

MARKET DRIVERS

Integration of Educational Value and STEM Learning

The increasing emphasis on educational value and STEM learning accelerates the growth of the United States toy market. This aligns with developmental goals. Parents and educators are prioritizing toys that foster critical thinking, problem-solving, and technical skills from an early age. As per the National Science Foundation, initiatives to promote science and mathematics education have led to a surge in demand for construction kits, coding robots, and scientific experiment sets. This trend is supported by data from the Department of Education, which highlights the growing importance of early exposure to technology and engineering concepts. According to a study, while educational toy sales are stable, they have recently been outpaced by the collectibles and "kidult" segments, which have become the dominant growth drivers in the U.S. toy industry. The integration of curriculum-aligned content into playthings allows manufacturers to appeal to both children and their guardians, who view these purchases as investments in future academic success. Schools and preschools also contribute to this demand by incorporating hands-on learning tools into their teaching methods. Furthermore, the rise of remote learning has accelerated the adoption of home-based educational resources, creating a sustained market for interactive and instructional toys. This convergence of entertainment and education ensures that STEM-focused products remain a dominant force in the industry, driving innovation and higher price points.

Influence of Media Franchises and Licensing Partnerships

The powerful influence of media franchises and licensing partnerships drives significant demand in the United States toy market. This creates emotional connections between consumers and characters. Movies, television series, and video games serve as marketing engines that generate hype and desire for associated physical products. As per the Motion Picture Association, box office successes often translate directly into spikes in toy sales, with blockbuster films launching extensive merchandise lines. This synergy allows manufacturers to leverage established brand equity and reduce the risk of new product introductions. According to a source, licensed properties account for a substantial portion of top-selling toys annually, demonstrating the effectiveness of cross-media promotion. Children are more likely to request toys featuring familiar characters from their favorite shows, creating pull-through demand at the retail level. Retailers capitalize on this by securing exclusive rights to popular licenses, thereby driving foot traffic and loyalty. The longevity of iconic franchises such as Star Wars and Marvel ensures a steady stream of revenue as new generations discover these stories. Additionally, the expansion of streaming platforms provides continuous content that keeps characters relevant and maintains consumer interest over time. This strategic alignment between entertainment and retail creates a robust ecosystem where narrative engagement fuels commercial success.

MARKET RESTRAINTS

Regulatory Compliance and Safety Standards

Strict regulatory compliance and safety standards act as a major restraint on the United States toy market. This increases production costs and limits design flexibility. Manufacturers must adhere to rigorous guidelines set by the Consumer Product Safety Commission regarding chemical content, small parts, and mechanical safety. As per the U.S. Consumer Product Safety Commission, non-compliance with safety standards can result in costly recalls and significant legal penalties, which increase time-to-market and regulatory burdens for manufacturers. The complexity of testing and certification processes requires significant investment in quality assurance and legal oversight. According to the Toy Industry Association, smaller companies often struggle to meet these requirements due to limited resources, leading to market consolidation among larger players. The need for third-party testing and documentation adds layers of administrative burden that slow down product launches. Additionally, evolving regulations regarding sustainability and environmental impact further complicate compliance efforts. Manufacturers must constantly monitor legislative changes to ensure their products remain legally viable in the domestic market. This regulatory landscape creates barriers to entry for new innovators and restricts the variety of materials and designs that can be used. So, the high cost of compliance constrains profit margins and limits the ability of companies to respond quickly to emerging trends.

Digital Substitution and Screen Time Competition

The proliferation of digital entertainment and increased screen time further limits the expansion of the United States toy market. These factors compete for children's attention and leisure hours. Video games, mobile apps, and streaming services offer immersive experiences that often replace traditional physical play. According to Common Sense Media, the average daily screen time for children has increased substantially, reducing the hours available for interacting with tangible toys. This shift in behavior alters consumption patterns as families allocate more budget toward digital subscriptions and hardware rather than physical playthings. According to the American Academy of Pediatrics, concerns about excessive screen use have led to debates, but the reality is that digital engagement remains high among youth demographics. The convenience and instant gratification of digital content make it a formidable competitor to toys that require assembly or imaginative effort. Parents may also perceive digital educational apps as more efficient learning tools compared to traditional toys. This substitution effect limits the growth potential of conventional toy categories and forces manufacturers to integrate digital components to remain relevant. The challenge lies in balancing physical play benefits with the allure of interactive media, which continues to dominate the entertainment landscape for younger generations.

MARKET OPPORTUNITIES

Expansion of Sustainable and Eco-Friendly Products

The growing consumer preference for sustainable and eco-friendly toys offers a significant opportunity for the United States toy market. This appeals to environmentally conscious parents. Buyers are increasingly seeking products made from renewable materials such as wood, bamboo, and recycled plastics that minimize environmental impact. The EPA's 'National Strategy to Prevent Plastic Pollution' (2024) outlines objectives to reduce plastic waste and improve circularity across industries, but it does not explicitly report that these initiatives have already heightened consumer awareness regarding the lifecycle of toys. Manufacturers can differentiate their offerings by obtaining certifications for sustainable sourcing and biodegradable packaging. This trend aligns with broader societal shifts toward circular economy principles, where durability and recyclability are valued over disposability. Companies that innovate with plant-based materials and non-toxic paints can capture market share from traditional plastic-based competitors. Additionally, the rise of second-hand toy markets and rental services offers new business models that extend product life cycles. By embracing sustainability, brands can build loyalty among millennial and Gen Z parents who prioritize ethical consumption. This strategic focus not only addresses environmental concerns but also opens new revenue streams through innovative material science and green marketing initiatives.

Growth of Direct-to-Consumer and Personalized Offerings

The expansion of direct-to-consumer DTC channels and personalized toy offerings offers a substantial opportunity for differentiation and customer engagement in the United States toy market. Online platforms allow manufacturers to bypass traditional retail intermediaries and build direct relationships with families. According to studies, the toy industry is experiencing flat sales or stabilization following the pandemic boom, with recent market activity driven primarily by adult collectors ('kidults') rather than the general ecommerce growth surge observed in previous years. Brands can leverage data analytics to offer customized products such as personalized dolls or bespoke building sets that enhance emotional value. According to Shopify and industry benchmarks (2025), the average ecommerce customer retention rate is approximately 30%, which remains lower than the ~63% retention rate seen in traditional retail, despite the use of tailored marketing to improve repeat purchase rates. The ability to control the brand narrative and customer experience enables companies to command higher margins and gather valuable insights into consumer preferences. Social media integration facilitates viral marketing campaigns and community building around specific product lines. Additionally, subscription boxes for toys provide recurring revenue streams and introduce customers to new products regularly. By investing in robust digital infrastructure, toy companies can expand their reach beyond geographical constraints. This shift empowers brands to offer unique value propositions and foster deeper loyalty in an increasingly competitive retail environment.

MARKET CHALLENGES

Supply Chain Volatility and Raw Material Costs

Supply chain volatility and fluctuating raw material costs are a persistent hindrance to the United States toy market. This disrupts production schedules and increases input expenses. The industry relies heavily on global manufacturing hubs, particularly in Asia, which are susceptible to geopolitical tensions and logistical bottlenecks. As per the Bureau of Labor Statistics, producer price indices for plastics and metals have experienced significant swings, affecting the cost structure for toy manufacturers. Dependence on imported components exposes companies to risks such as port congestion and labor shortages that delay shipments. According to the Institute for Supply Management, supply chain disruptions have led to extended lead times, forcing brands to hold higher inventory levels, which ties up capital. The rising cost of freight and energy further exacerbates these issues, squeezing profit margins for both manufacturers and retailers. Companies struggle to pass these costs onto consumers without risking demand erosion in a price-sensitive market. Additionally, the lack of domestic manufacturing capacity limits flexibility in responding to sudden changes in demand. This instability complicates long-term planning and inventory management, making it difficult for brands to maintain consistent product availability. Consequently, supply chain vulnerabilities act as a persistent drag on market efficiency and profitability.

Counterfeit Products and Intellectual Property Theft

The widespread presence of counterfeit toys and intellectual property theft poses a serious barrier to the United States toy market. This erodes brand integrity and causes revenue losses. Illicit manufacturers produce low-quality replicas of popular toys, which are sold through online marketplaces and unauthorized retailers. As per the OECD and EUIPO 2025 report on illicit trade, global trade in counterfeit goods reached $467 billion, with the toy category being a significant target, causing billions in annual losses and severe risks to brand reputation and consumer safety. Counterfeits often fail to meet safety standards, posing health risks to children and damaging consumer trust in legitimate brands. According to the Federal Trade Commission, enforcement against online counterfeiters remains challenging due to the anonymity and cross-border nature of these operations. The prevalence of fakes dilutes the exclusivity of licensed products, reducing the perceived value for collectors and enthusiasts. Brands must invest heavily in authentication technologies and legal actions to combat this issue, which increases operational costs. Furthermore, the ease of accessing counterfeits online erodes trust in secondary marketplaces where authenticity is paramount. This persistent threat forces companies to constantly adapt their security measures and monitoring strategies. Failure to effectively address counterfeiting can lead to long-term damage to brand equity and customer loyalty in a highly competitive landscape.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Age Group, Sales Channel, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | The LEGO Group, Mattel, Hasbro, Bandai Namco Holdings Inc., Spin Master, Funko, MGA Entertainment Inc., VTech Holdings Limited, and Others. |

SEGMENTAL ANALYSIS

By Product Type Insights

The building sets segment led the U.S. toy market in 2025. This leading position is attributed to its enduring appeal across multiple age groups and its strong alignment with educational developmental goals. These products encourage spatial reasoning, creativity, and problem-solving skills, which resonate deeply with parents seeking constructive play options. As per sources, construction toys consistently rank among the top-selling categories due to their versatility and replay value. The dominance is further reinforced by powerful licensing partnerships with major entertainment franchises such as Star Wars, Marvel, and Harry Potter, which drive consistent consumer interest. The ability of these toys to scale in complexity allows them to grow with the child from simple blocks for toddlers to intricate mechanical models for teenagers. This longevity enhances the perceived value for money, encouraging repeat purchases within the same brand ecosystem. Additionally, the rise of adult fans of LEGO and similar brands has expanded the target demographic beyond children, creating a new revenue stream. The tactile satisfaction of assembling structures provides a screen-free alternative that appeals to families looking to balance digital consumption. This combination of educational benefit, cross-generational appeal, and strong brand loyalty solidifies building sets as the cornerstone of the US toy industry.

The games and puzzles segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 9.5% during the forecast period due to the increasing demand for social interaction and family bonding activities. The pandemic accelerated this trend as households sought indoor entertainment options that facilitated connection without screens. This segment benefits from the diversification of game types, ranging from traditional strategy games to cooperative narratives that appeal to diverse age groups. The rise of crowdfunding platforms has also enabled independent designers to launch innovative games that capture niche markets and drive overall category growth. Furthermore, the educational value of games in teaching logic, probability, and social skills makes them attractive to parents and educators. Retailers have responded by expanding shelf space for this category and hosting in-store events that foster community engagement. The low barrier to entry for new players and the endless variety of themes ensure sustained interest. This convergence of social utility, cognitive benefit, and creative innovation propels the games and puzzles segment ahead of others in terms of growth velocity.

By Age Group Insights

The up to 5-year age group segment dominated the U.S. toy market in 2025. This dominance of the segment is driven by the critical nature of early childhood development and the high frequency of gift-giving for infants and toddlers. Parents and relatives invest heavily in toys that stimulate sensory motor and cognitive skills during these formative years. This demographic drives demand for plush toys, rattles, shape sorters, and introductory building blocks, which are often replaced as children grow. The emotional connection formed through comfort items like stuffed animals ensures consistent sales volume. Additionally, the tradition of baby showers and first birthdays creates specific occasions for substantial toy purchases. Manufacturers focus on this segment by developing products that align with developmental milestones such as walking, talking, and recognizing colors. The influence of parental recommendations and pediatrician endorsements further guides purchasing decisions. This combination of developmental necessity, cultural gift traditions, and brand trust ensures that the up to 5 years segment remains the largest contributor to overall market revenue.

The above 10-year age group segment is expected to exhibit a noteworthy CAGR of 8.2% from 2026 to 2034, owing to the increasing complexity of interests and the influence of pop culture franchises. Pre-teens and teenagers seek toys that reflect their identity and social status, such as collectible figures, advanced robotics, and strategic board games. The blurring lines between toys and hobbies, such as model building and esports accessories, contribute to this growth. Licensing from video games and anime series drives significant demand for action figures and role-play items. Furthermore, the rise of social media influencers showcasing unboxing and review content creates viral trends that rapidly boost sales for specific products. Retailers cater to this segment by offering exclusive collector editions and limited releases that foster a sense of exclusivity. The higher disposable income of this age group through allowances and gifts allows for premium purchases. This shift toward sophisticated and culturally relevant playthings ensures rapid expansion of the above 10-year segment.

By Sales Channel Insights

The online stores segment was the largest segment in the United States toy market in 2025 because of the convenience of home delivery, extensive product selection, and competitive pricing available through digital platforms. E-commerce allows consumers to compare brands, read reviews, and access exclusive releases without geographical constraints, making it the preferred channel for busy parents. Major retailers and direct-to-consumer brands have invested heavily in user-friendly websites and apps that offer personalized recommendations and seamless checkout experiences. The ability to access global inventory and niche products that may not be available in local stores further enhances the appeal of online shopping. Additionally, flexible return policies and free shipping incentives reduce the perceived risk of buying toys without seeing them physically. The integration of social commerce features allows users to purchase directly from social media posts, streamlining the journey from discovery to purchase. This combination of convenience, variety, and technological innovation ensures that online stores remain the dominant distribution channel in the US toy market.

The specialty stores segment is predicted to witness the highest CAGR of 7.6% over the forecast period. This quick surge of the segment is propelled by the demand for curated experiences, expert advice, and unique product offerings. Consumers increasingly seek out independent toy shops and specialized retailers for high-quality educational and artisanal toys that are not available in mass market outlets. These stores often host events such as story times and demo days that create emotional connections with families. The focus on sustainable and locally sourced products also attracts environmentally conscious buyers. Specialty stores differentiate themselves by offering exclusive brands and limited edition items that appeal to collectors and enthusiasts. The tactile experience of testing products in store, combined with the trust built through face-to-face interactions, fosters strong customer loyalty. This blend of expertise, curation, and community focus positions specialty stores as a dynamic growth area in the competitive toy retail landscape.

COUNTRY LEVEL ANALYSIS

U.S. Toy Market Analysis

The United States was the top performer in the toy market in the North American region and occupied a 40.5% share in 2025. This supremacy of the US market is driven by its large population, high disposable income, and strong consumer culture. Its top position is further supported by a robust retail infrastructure and a deep-seated tradition of gift giving during holidays and special occasions. As per the Toy Association, the US toy industry generates billions in annual revenue, reflecting the central role of play in American family life. The market is characterized by a mature ecosystem where global brands coexist with innovative startups, driving continuous product development. According to the US Census Bureau, the presence of millions of children ensures a steady baseline demand for age-appropriate products. Consumer behavior in the US is marked by a high adoption of e-commerce and digital media influences, which shape purchasing decisions and brand loyalty. The prevalence of licensing agreements with Hollywood studios creates a synergistic relationship between entertainment and retail. Regulatory frameworks regarding safety and sustainability are strictly enforced, maintaining high-quality benchmarks for domestic and imported goods. High levels of urbanization and dual-income households drive demand for convenient and educational play options. This robust foundation ensures that the United States remains the central hub for toy innovation and consumption, influencing global trends and setting standards for quality and service in the industry.

COMPETITIVE LANDSCAPE

The competition in the United States toy market is intense and characterized by a mix of global conglomerates and agile niche brands vying for consumer attention. Major players compete on brand equity, innovation, and multimedia integration, while smaller companies differentiate themselves through unique designs and educational value. The rise of direct-to-consumer models has disrupted traditional retail channels, forcing established brands to enhance their digital presence and customer service quality. Price sensitivity varies across segments, with value-driven shoppers seeking affordability and collectors willing to pay premiums for exclusivity. Innovation in technology and sustainability provides competitive advantages for early adopters who can offer superior interactive or eco-friendly products. Regulatory compliance and safety standards also influence competitive dynamics as consumers demand transparency. Social media plays a pivotal role in shaping trends and driving viral demand for specific items. This complex landscape requires continuous adaptation and strategic investment to maintain market relevance and profitability in a saturated industry.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. toy market include

- The LEGO Group

- Mattel

- Hasbro

- Bandai Namco Holdings Inc.

- Spin Master

- Funko

- MGA Entertainment Inc.

- VTech Holdings Limited

TOP PLAYERS IN THE MARKET

- The LEGO Group remains a dominant force in the global toy industry, renowned for its iconic interlocking brick system that fosters creativity and learning. The company actively expands its portfolio through strategic partnerships with major entertainment franchises such as Disney and Nintendo to drive consumer engagement. Recent actions include significant investments in sustainable materials, aiming to produce bricks from recycled sources by 2032. LEGO strengthens its market position by enhancing digital integration through augmented reality apps and video games that complement physical play. The firm also focuses on educational initiatives, collaborating with schools to promote STEM learning. By prioritizing innovation in product design and sustainability, LEGO maintains its reputation for quality and timeless appeal. These efforts ensure continued growth and brand loyalty across diverse age groups globally while adapting to modern environmental standards and digital trends.

- Mattel Inc is a leading global toy company with a diverse portfolio featuring iconic brands such as Barbie, Hot Wheels, and Fisher-Price. The company leverages its strong intellectual property to create multimedia content, including films and series that reinforce brand relevance. Recent strategies involve transforming Barbie into a cultural phenomenon through successful movie releases and inclusive product lines. Mattel focuses on direct-to-consumer expansion by enhancing its e-commerce platforms and personalized shopping experiences. The firm invests in sustainability initiatives aiming for fully recyclable packaging and responsible sourcing practices. By integrating digital play experiences with physical toys, Mattel appeals to tech-savvy younger generations. These actions strengthen its competitive edge by balancing heritage brands with modern innovation and social responsibility in the dynamic global toy market.

- Hasbro Inc is a major global player known for its powerful brands, including Transformers, Nerf, and Magic: The Gathering. The company combines toy manufacturing with entertainment production, creating a synergistic ecosystem that drives long-term engagement. Recent actions include expanding its licensing agreements and developing new content for streaming platforms to keep franchises relevant. Hasbro focuses on digital transformation by launching interactive apps and online gaming communities that enhance player interaction. The firm strengthens its market position through strategic acquisitions of complementary brands and technologies. By prioritizing community engagement and immersive storytelling, Hasbro builds deep connections with fans. These efforts enable the company to maintain leadership in both traditional tabletop gaming and action figure segments while adapting to evolving consumer preferences for integrated play experiences.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States toy market prioritize intellectual property leverage by integrating toys with movies, games, and digital content to create immersive brand ecosystems. Companies focus on sustainability initiatives by adopting eco-friendly materials and recyclable packaging to meet growing consumer demand for responsible products. Direct-to-consumer channels are expanded through enhanced e-commerce platforms offering personalized experiences and exclusive releases. Strategic partnerships with technology firms enable the integration of augmented reality and interactive features into physical toys. Manufacturers invest in inclusive product lines reflecting diverse cultures and abilities to broaden market appeal. Data analytics drive targeted marketing campaigns that optimize inventory and enhance customer engagement. These combined approaches allow firms to navigate competitive pressures and sustain growth in a rapidly evolving retail landscape.

MARKET SEGMENTATION

This research report on the U.S. toy market has been segmented and sub-segmented into the following categories.

By Product Type

- Action Figures

- Building Sets

- Dolls

- Games and Puzzles

- Sports and Outdoor Toys

- Plush

- Others

By Age Group

- Up to 5 Years

- 5 to 10 Years

- Above 10 Years

By Sales Channel

- Supermarkets and Hypermarkets

- Specialty Stores

- Department Stores

- Online Stores

- Others

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

What is the U.S. toy market?

The U.S. toy market encompasses sales of dolls, games, action figures, and educational products for children through retail, online, and specialty channels.

How does the U.S. toy market function?

The U.S. toy market operates via manufacturers, distributors, retailers, and e-commerce platforms that supply toys tied to trends and licensing deals.

What drives growth in the U.S. toy market?

The U.S. toy market grows from licensed products, educational demand, media tie-ins, and parental focus on developmental play experiences.

Which toy categories lead the U.S. toy market?

The U.S. toy market is led by games, puzzles, building sets, action figures, dolls, and youth electronics popular among kids.

What role do licensed toys play in the U.S. toy market?

Licensed toys dominate the U.S. toy market through movie, game, and character merchandise that appeals to fans and collectors.

How important are educational toys in the U.S. toy market?

Educational toys shape the U.S. toy market as parents seek STEM, learning, and skill-building options for child development.

What channels serve the U.S. toy market?

The U.S. toy market reaches consumers via toy stores, big-box retailers, online platforms, and direct brand sales.

How does e-commerce impact the U.S. toy market?

E-commerce expands the U.S. toy market by offering convenience, variety, and direct access to trending and specialty toys.

What trends affect the U.S. toy market?

The U.S. toy market follows digital integration, nostalgia revivals, smart toys, and interactive play linked to media content.

What challenges face the U.S. toy market?

The U.S. toy market deals with competition, shifting trends, inventory management, and screen time competition from digital devices.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com