U.S. Used Cars Market Size, Share, Trends & Growth Forecast Report By Vehicle Type, By Sales Channel Type, By Fuel Type, By Distribution Channel, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Used Cars Market Size

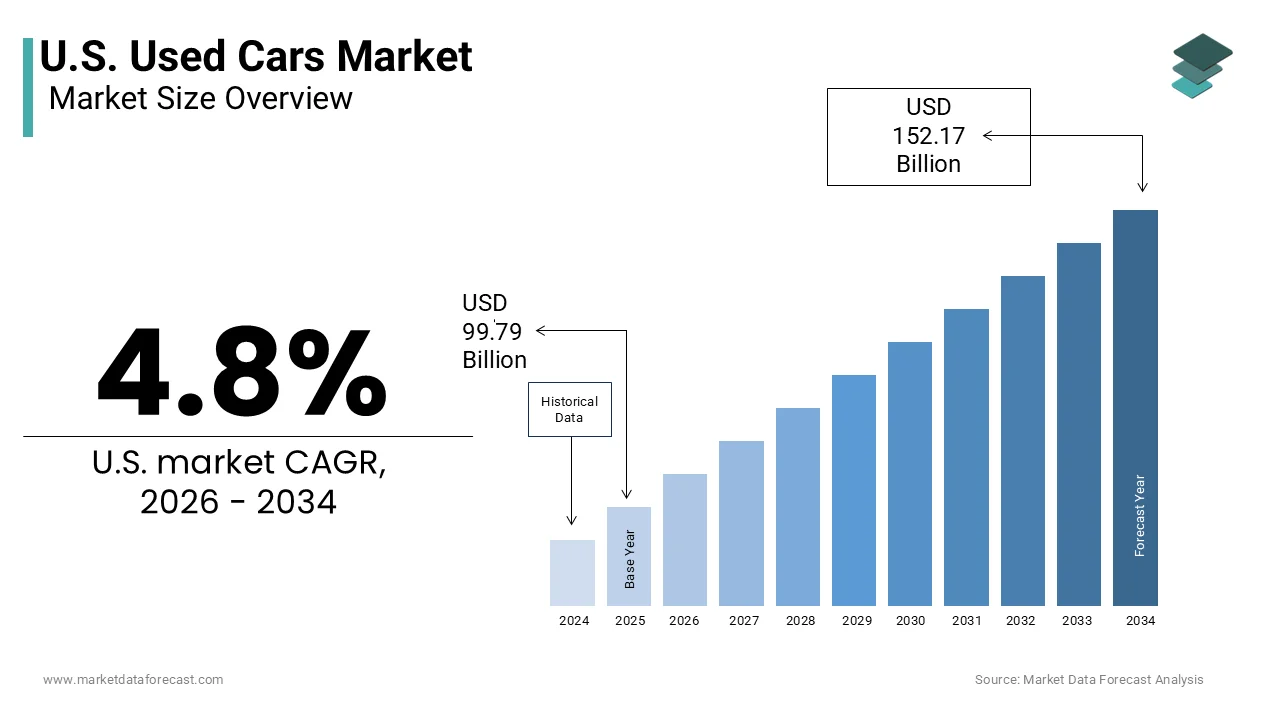

The U.S. Used Cars Market was valued at USD 99.79 billion in 2025, is estimated to reach USD 104.58 billion in 2026, and is projected to reach USD 152.17 billion by 2034, growing at a CAGR of 4.8% from 2026 to 2034.

According to data from S&P Global Mobility, the average age of light vehicles in the U.S. reached 12.6 years in 2024, and this indicates a growing inventory of older cars available for secondary transactions. The ecosystem is supported by robust financing options and certification programs that enhance consumer confidence in purchasing pre-owned assets. According to Cox Automotive, approximately 35.9 million used vehicles were sold in the U.S. in 2023, significantly outnumbering new car sales,s which reached approximately 15.5 million units. This disparity underscores the market's importance in providing mobility solutions to a diverse demographic range. The shift towards online retailing has further transformed the landscape, with digital tools enabling transparent pricing and virtual inspections. According to the Bureau of Transportation Statistics, household expenditure on vehicle purchases remains a substantial component of personal consumption, reflecting the enduring demand for automotive transport. The market operates within a complex regulatory framework involving title transfers, emissions standards, and consumer protection laws. These factors collectively shape the operational environment for dealers and private sellers alike. The integration of advanced diagnostics and vehicle history reports has standardized quality assessments, reducing information asymmetry between buyers and sellers. This evolution ensures that the used car sector remains a resilient and essential pillar of the American transportation infrastructure.

MARKET DRIVERS

Economic Pressure and Affordability Constraints

Economic pressure and affordability constraints are propelling the expansion of the U.S. used cars market, which is compelling consumers to seek cost-effective alternatives to new vehicles. Rising inflation and higher interest rates have significantly increased the total cost of ownership for new automobiles, making them less accessible to average households. As per the Federal Reserve Bank of New York, the average monthly payment for a new car loan reached 735 U.S. dollars in the fourth quarter of 2023, prompting many buyers to pivot towards the pre-owned segment,nt where payments are substantially lower. The price gap between new and used vehicles has widened, with used cars offering similar utility at a fraction of the cost. Data from Kelley Blue Book indicates that the average transaction price for a used light vehicle was approximately 28,000 U.S. dollars in 2024, compared to over 48,000 U.S. dollars for new models. This significant differential drives demand among budget-conscious consumers, first-time buyers, and families managing tight financial budgets. Additionally, the depreciation curve of new cars means that buyers can acquire relatively recent models with low mileage at reduced prices. The lingering effects of supply chain disruptions from previous years have also kept new vehicle inventories constrained, further pushing demand toward the used market. According to recent consumer surveys, financial prudence has become a dominant factor in purchasing decisions, with nearly 60% of car shoppers considering used vehicles due to economic uncertainty. This trend ensures sustained volume in the used car sector as consumers prioritize value and affordability in their transportation choices.

Expansion of Digital Retailing and Online Platforms

The expansion of digital retailing and online platforms has revolutionized the U.S. used cars market by enhancing transparency, convenience, and consumer trust, which is another major market driver. Traditional barriers such as opaque pricing and high-pressure sales tactics are being dismantled by e-commerce-enabled dealerships and dedicated online marketplaces. As per industry data, over 40% of used car buyers now begin their search online, utilizing digital tools to compare prices, view vehicle history reports, and even complete financing applications remotely. Companies like Carvana and Vroom have pioneered the concept of buying cars entirely online, offering home delivery and return policies that mimic the ease of standard e-commerce transactions. This shift appeals to younger demographics who prefer digital interactions over physical dealership visits. The availability of comprehensive vehicle data, including accident history and maintenance records, reduces perceived risk and encourages purchase decisions. According to industry reports, dealerships that adopt digital retailing tools see higher conversion rates and customer satisfaction scores compared to those relying solely on traditional methods. Furthermore, the integration of artificial intelligence in pricing algorithms ensures competitive and fair market values, attracting both buyers and sellers. The convenience of browsing extensive inventories from anywhere at any time expands the potential customer base beyond local geographic limits. This digital transformation not only streamlines the buying process but also fosters a more efficient and transparent market environment. As technology continues to evolve, the reliance on online platforms will likely deepen, driving further growth and modernization in the used car sector.

MARKET RESTRAINTS

High Interest Rates and Financing Challenges

High interest rates and financing challenges are hampering the U.S. used cars market growth by increasing the cost of borrowing and reducing purchasing power for consumers. The Federal Reserve’s monetary policy adjustments to combat inflation have led to elevated interest rates for auto loans, particularly for subprime borrowers who frequently populate the used car market. As per Experian data, the average interest rate for used car loans reached approximately 11% in 2024, a notable increase from previous years. This rise in borrowing costs translates to higher monthly payments, discouraging potential buyers from entering the market or forcing them to choose cheaper, older vehicles with potentially higher maintenance risks. Lenders have also tightened credit standards, resulting in lower approval rates for applicants with less than perfect credit histories. According to the Federal Reserve Bank of Philadelphia, delinquency rates on auto loans have risen, prompting financial institutions to exercise greater caution in lending practices. This contraction in credit availability limits the pool of qualified buyers, thereby suppressing overall sales volume. Additionally, the combination of high vehicle prices and high interest rates creates an affordability crisis for many middle and lower-income households. Consumers may delay purchases or extend the life of their current vehicles, further dampening demand. The uncertainty surrounding future interest rate trajectories adds another layer of hesitation among buyers. Until financing conditions improve or vehicle prices adjust downward, these financial barriers will continue to constrain the growth potential of the used car market.

Inventory Shortages and Supply Chain Disruptions

Inventory shortages and lingering supply chain disruptions remain persistent restraints on the U.S. used cars market, which is limiting the availability of desirable vehicles and sustaining elevated prices. The semiconductor chip shortage and other manufacturing delays that plagued the new car industry in recent years have had a cascading effect on the used car sector by reducing the flow of off-lease and trade-in vehicles. As per industry figures, the supply of used vehicles at auctions remained tight in early 2024, with inventory levels still below historical averages despite gradual improvements. This scarcity restricts the ability of dealers to stock diverse inventories, leading to fewer choices for consumers and prolonged search times. The reduced influx of late-model used cars forces buyers to consider older vehicles with higher mileage, which may not meet their preferences or reliability expectations. Furthermore, logistical challenges in transporting vehicles across the country continue to impact distribution efficiency and increase operational costs for dealers. According to the American Trucking Associations, freight capacity constraints have occasionally led to delays in vehicle delivery, exacerbating inventory imbalances in certain regions. The lack of sufficient supply prevents the market from reaching equilibrium, keeping prices artificially high and deterring price-sensitive buyers. Dealers face difficulties in acquiring quality stock at reasonable costs, squeezing margins, ins and limiting promotional activities. Until supply chains fully normalize and new vehicle production stabilizes, the used car market will continue to grapple with inventory limitations that hinder its full potential.

MARKET OPPORTUNITIES

Growth of Certified Pre-Owned Programs

The growth of certified pre-owned (CPO) programs presents a significant opportunity for the U.S. used cars market by bridging the gap between new and used vehicle purchases in terms of quality and warranty coverage. CPO vehicles undergo rigorous multi-point inspections and come with extended warranties, offering buyers peace of mind comparable to buying new. As per market tracking, sales of certified pre-owned vehicles have shown resilience and growth, with consumers increasingly valuing the added assurance of manufacturer-backed certifications. This segment appeals to buyers who desire newer models with low mileage but are deterred by the high cost of brand-new cars. Automakers and dealerships are expanding their CPO offerings to include a wider range of models, including electric vehicles, to capture this growing demand. The higher profit margins associated with CPO sales incentivize dealers to invest in reconditioning and marketing efforts. According to industry publications, CPO vehicles often sell faster and at higher prices than non-certified used cars, demonstrating strong consumer preference for verified quality. The expansion of digital tools allows buyers to easily identify and compare CPO options online, enhancing visibility and accessibility. Furthermore, the inclusion of complimentary maintenance packages and roadside assistance adds value to the purchase proposition. As consumer confidence in used vehicles grows through these structured programs, the CPO segment is poised for continued expansion. This opportunity allows market participants to differentiate themselves and capture value-conscious customers who prioritize reliability and warranty protection.

Integration of Electric Vehicles in the Used Market

The integration of electric vehicles (EVs) into the used car market offers a substantial opportunity for growth as early adopters upgrade and more EV models enter the secondary market. As electric vehicle adoption accelerates, a growing inventory of pre-owned EVs is becoming available, attracting environmentally conscious buyers and those seeking lower operating costs. As per recent reports, the number of used electric vehicles listed for sale has increased significantly, with prices becoming more competitive as battery technology improves and production scales up. Government incentives and tax credits for used EV purchases further stimulate demand, making these vehicles more affordable for a broader audience. The Inflation Reduction Act provides a tax credit of up to 4,000 U.S. dollars for qualifying used electric vehicles, enhancing their appeal to budget-conscious consumers. Dealers are investing in specialized training and equipment to inspect and service EVs, ensuring they can confidently offer these vehicles to customers. The lower maintenance requirements of electric vehicles, such as fewer moving parts and no oil changes, are attractive selling points for used car buyers. Additionally, the development of battery health assessment tools allows for accurate valuation and transparency regarding remaining range and longevity. As charging infrastructure expands and range anxiety diminishes, the demand for used EVs is expected to rise. This transition opens new revenue streams for dealers and provides consumers with sustainable mobility options. The evolving landscape of electric mobility presents a strategic avenue for market participants to diversify their inventories and align with future automotive trends.

MARKET CHALLENGES

Vehicle Quality and Reliability Concerns

Vehicle quality and reliability concerns pose a major challenge to the U.S. used cars market, as buyers remain wary of purchasing vehicles with hidden defects or uncertain maintenance histories. Despite advancements in vehicle history reports, issues such as undisclosed accident damage, odometer fraud, and mechanical wear can still evade detection, leading to post-purchase dissatisfaction and financial burden for consumers. As per Consumer Reports, reliability varies significantly among different makes and models, with some used vehicles requiring frequent repairs shortly after purchase. This uncertainty erodes consumer trust and can deter potential buyers from entering the market. The complexity of modern vehicles, equipped with advanced electronics and software, further complicates diagnostic processes and increases repair costs. Independent mechanics may lack the specialized tools or knowledge to accurately assess these systems, leaving buyers vulnerable to unexpected expenses. According to the National Institute for Automotive Service Excellence, the shortage of skilled technicians exacerbates the problem, making it difficult to obtain timely and reliable inspections. Dealerships face the challenge of balancing reconditioning costs with competitive pricing, sometimes leading to compromises in quality control. Negative experiences shared through online reviews and social media can quickly damage reputations and reduce sales. Ensuring consistent quality and transparency requires significant investment in inspection technologies and staff training. Until these reliability concerns are adequately addressed, they will remain a persistent barrier to consumer confidence and market growth.

Regulatory Compliance and Consumer Protection Laws

Regulatory compliance and consumer protection laws present a complex challenge for participants in the U.S. used cars market, which requires strict adherence to varying state and federal regulations. Dealers must navigate a web of rules regarding disclosure of vehicle history, warranty obligations, and fair lending practices, which can differ significantly across jurisdictions. As per the Federal Trade Commission, the Used Car Rule mandates that dealers display a Buyers Guide on each used vehicle, outlining warranty coverage and known defects, and failure to comply can result in severe penalties. Additionally, state-level lemon laws and consumer protection statutes impose additional responsibilities on sellers to ensure vehicles meet certain standards. The evolving landscape of data privacy regulations also impacts how dealers collect and handle customer information during the sales and financing process. Compliance with these diverse requirements necessitates robust legal oversight and administrative resources, increasing operational costs for businesses. Small independent dealers may struggle to keep pace with changing regulations, facing heightened risk of litigation or fines. According to automotive industry associations, regulatory burdens are a top concern for dealers, impacting their ability to operate efficiently. Furthermore, scrutiny from consumer advocacy groups and regulatory bodies regarding predatory lending practices and unfair sales tactics adds pressure on the industry to maintain high ethical standards. Navigating this complex regulatory environment requires continuous monitoring and adaptation, posing a significant challenge to market participants aiming to maintain compliance while remaining competitive.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Vehicle Type, Sales Channel Type, Fuel Type, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | CarMax Inc., Carvana Co., AutoNation Inc., Asbury Automotive Group Inc., Lithia Motors Inc., Group 1 Automotive Inc., TrueCar Inc., CarGurus Inc., eBay Inc., Hendrick Automotive Group |

SEGMENTAL ANALYSIS

By Vehicle Type Insights

The sport utility vehicles segment dominated the U.S. used cars market by accounting for the highest share of the U.S. market in 2025 due to their unparalleled versatility, spacious interiors, and perceived safety advantages, which align with the lifestyle needs of American families. As per data from industry analysts, SUVs accounted for approximately 55% of all used vehicle sales in 2024, reflecting a sustained shift away from traditional sedans. Consumers prioritize the higher seating position and all-wheel drive capabilities that many SUVs offer, providing confidence in diverse weather conditions and road types. The availability of three-row seating options in mid-size and full-size SUVs makes them ideal for growing families who require ample cargo space for daily activities and travel. This practical utility drives consistent demand in the secondary market, where buyers seek value without compromising on functionality. Furthermore, the robust resale value of popular SUV models encourages trade-ins, ensuring a steady supply of inventory for dealers. According to market researchers, consumer satisfaction scores for used SUVs remain high, particularly regarding comfort and technology features that were once exclusive to luxury segments. The widespread adoption of SUVs across various demographic groups, from young professionals to retirees, ensures broad market appeal. Manufacturers have responded by expanding their SUV lineups, resulting in a diverse range of pre-owned options at various price points. This abundance of choice reinforces the segment's leadership, as buyers can easily find models that fit their specific budget and feature requirements. The cultural preference for larger vehicles in the U.S. further cements the SUV's position as the dominant force in the used car landscape.

On the other hand, the hatchback segment is on the rise and is predicted to be the fastest-growing segment in the U.S. market during the forecast period, owing to the increasing urbanization and the demand for fuel-efficient compact vehicles. As more Americans move to cities where parking is scarce and streets are narrow, the compact dimensions of hatchbacks offer significant practical advantages. As per the U.S. Census Bureau, the urban population continues to grow, creating a larger base of consumers who prioritize maneuverability and ease of parking. Hatchbacks provide ample cargo space relative to their footprint, thanks to their versatile rear doors and foldable seats, making them ideal for city dwellers with active lifestyles. The superior fuel economy of hatchbacks compared to larger SUVs and trucks appeals to cost-conscious buyers facing fluctuating gas prices. According to the Environmental Protection Agency, many modern hatchbacks achieve over 35 miles per gallon in combined driving cycles, offering substantial savings on daily commutes. This economic benefit is a key driver for younger buyers and students entering the used car market for the first time. The availability of affordable pre-owned hatchbacks from reputable brands ensures that quality options are accessible to budget-constrained consumers. Additionally, the rise of ride-sharing services has increased the demand for reliable and efficient compact cars, further boosting the used hatchback segment. As urban living becomes more prevalent, the practicality and efficiency of hatchbacks will continue to drive their rapid growth in the secondary market.

By Sales Channel Type Insights

The offline segment led the market by capturing the leading share of the U.S. used cars market in 2025. The leading position of the offline segment in the U.S. used cars market is primarily because they allow consumers to physically inspect vehicles and conduct test drives before purchasing. This tactile experience is crucial for building trust and confidence, particularly for high-value transactions involving complex machinery. As per a survey by Cox Automotive, over 70% of used car buyers consider the ability to test drive a vehicle as a critical factor in their decision-making process. Physical inspections enable buyers to assess the condition of the interior, exterior, and mechanical components, reducing the perceived risk of purchasing a lemon. Dealerships provide professional reconditioning and certification, which adds a layer of assurance that private sellers or online-only platforms may lack. The presence of knowledgeable sales staff who can answer questions and provide immediate feedback enhances the customer experience. According to automotive dealer associations, dealership visits remain the primary method for finalizing used car purchases, with the majority of buyers visiting multiple lots before making a decision. The immediacy of taking possession of the vehicle upon completion of paperwork is another advantage of offline sales. For many consumers, the traditional dealership model offers a sense of security and accountability that digital alternatives have yet to fully replicate. This enduring preference for physical interaction ensures that offline channels continue to dominate the market landscape.

However, the online segment is growing at the fastest and is projected to grow at a promising CAGR in the U.S. market over the forecast period,d owing to the unparalleled convenience of browsing extensive inventories from home and the availability of home delivery services. Digital platforms allow consumers to compare thousands of vehicles based on price, mileage, and features without the time commitment of visiting multiple dealerships. As per industry consultants, the adoption of online automotive retailing has accelerated, with a significant portion of buyers now completing the entire purchase process digitally. The integration of high-resolution images, 360-degree virtual tours, and detailed vehicle history reports provides transparency that mitigates the lack of physical inspection. Companies like Carvana and Vroom have normalized the concept of buying a car online, offering seven-day return policies that reduce purchase anxiety. The ability to have the vehicle delivered directly to the buyer’s doorstep saves time and effort, appealing to busy professionals and tech-savvy consumers. According to industry forecasts, online used car sales are projected to grow at a compound annual growth rate of 12% over the next five years, outpacing traditional channels. This growth is supported by improvements in logistics and last-mile delivery networks. The seamless integration of digital financing and insurance tools further streamlines the experience. As consumer comfort with e-commerce continues to rise, the online channel is capturing an increasing share of the market, transforming how used cars are bought and sold.

By Fuel Type Insights

The petrol-fueled vehicles segment dominated the market by holding the largest share of the U.S. used cars market in 2025. The dominance of the petrol segment is attributed to the extensive refueling infrastructure and consumer familiarity with internal combustion engine technology. Gas stations are ubiquitous across the country, ensuring that petrol vehicle owners have convenient access to fuel regardless of their location. As per the Energy Information Administration, there are over 145,000 fueling stations in the U.S., providing a reliable network that supports the vast majority of vehicles on the road. This accessibility eliminates range anxiety, a common concern associated with alternative fuel vehicles. Consumers are accustomed to the performance characteristics and maintenance requirements of petrol engines, making them a safe and predictable choice in the used market. The widespread availability of mechanics trained to service petrol vehicles ensures that repairs are affordable and accessible. According to the Bureau of Transportation Statistics, petrol continues to account for the overwhelming majority of light-duty vehicle fuel consumption, reflecting its entrenched position in the transportation sector. The large existing inventory of petrol vehicles provides buyers with a wide selection of makes, models, and price points. This abundance ensures that consumers can find vehicles that meet their specific needs and budgets. The reliability and proven track record of petrol engines further reinforce their dominance. Until alternative fuel infrastructure reaches comparable levels of maturity, petrol vehicles will remain the default choice for most used car buyers.

However, the electric vehicles segment is gaining traction and is estimated to register a prominent CAGR in the U.S. used cars market during the forecast period, owing to government incentives and increasing environmental awareness among consumers. Federal and state tax credits for used electric vehicles make them more affordable and attractive to buyers. As per the Internal Revenue Service, eligible buyers can claim a tax credit of up to 4,000 U.S. dollars for qualifying used electric vehicles, significantly reducing the effective purchase price. This financial incentive lowers the barrier to entry for consumers interested in sustainable transportation. Growing concern about climate change and air pollution is also motivating buyers to switch to zero-emission vehicles. As per the Pew Research Center, a majority of Americans express support for expanding electric vehicle adoption to reduce environmental impact. This shift in consumer values is reflected in the rising demand for used EVs. Automakers are introducing more electric models, increasing the supply of pre-owned options as early adopters upgrade to newer versions. The improving public perception of electric vehicles as viable and desirable transportation options further fuels growth. Educational campaigns and community initiatives promote the benefits of electric mobility, encouraging broader acceptance. As environmental regulations tighten and societal norms evolve, the demand for used electric vehicles will continue to accelerate. This trend represents a significant transformation in the automotive landscape, positioning electric vehicles as a key growth area in the used car market.

By Distribution Channel Insights

The franchised dealers segment held the leading position in the U.S. used cars market in 2025 due to their ability to offer certified pre-owned programs and the inherent trust associated with established automotive brands. These dealerships sell vehicles that have undergone rigorous multi-point inspections and come with manufacturer-backed warranties, providing buyers with peace of mind. As per industry evaluations, certified pre-owned vehicles sold at franchised dealers command higher prices and sell faster than non-certified units, reflecting consumer preference for verified quality. The association with reputable brands such as Toyota, Ford, and Honda enhances credibility and attracts loyal customers. Franchised dealers have access to original equipment manufacturer parts and trained technicians, ensuring that vehicles are reconditioned to high standards. This quality assurance reduces the risk of post-purchase issues and builds long-term customer relationships. According to the National Automobile Dealers Association, franchised dealers account for a major portion of used car sales by volume, leveraging their extensive networks and resources. The ability to offer trade-in allowances for new vehicle purchases creates a seamless upgrade path for customers. Financing options are often more competitive at franchised dealers due to relationships with captive finance arms. These advantages create a compelling value proposition that independent dealers and private sellers struggle to match. Consequently, franchised dealers maintain their dominance through quality, trust, and comprehensive service offerings.

On the other hand, the independent dealers segment is the fastest-growing segment in the U.S. used cars market and is predicted to showcase a healthy CAGR during the forecast period, owing to their flexibility in inventory sourcing and competitive pricing strategies. Unlike franchised dealers, independent dealers are not restricted to specific brands, allowing them to offer a diverse range of vehicles from various manufacturers. As per industry observations, independent dealers can quickly adapt to market trends by stocking popular models regardless of brand affiliation. This agility enables them to meet changing consumer demands and capitalize on niche markets. Independent dealers often operate with lower overhead costs than franchised counterparts, allowing them to offer more competitive prices. This affordability appeals to budget-conscious buyers seeking value. The ability to negotiate prices directly with owners provides a personalized shopping experience that some consumers prefer. According to industry analysis, independent dealers have expanded their presence in suburban and rural areas where franchised dealerships are less accessible. This geographic expansion increases their market reach and customer base. The use of digital marketing and online listings has also helped independent dealers gain visibility and attract younger buyers. Their focus on customer service and community engagement fosters loyalty and repeat business. As consumers seek alternatives to traditional dealerships, independent dealers are capturing a growing share of the market through flexibility and value.

COUNTRY LEVEL ANALYSIS

United States Used Cars Market Analysis

The U.S. is likely to see continued growth in the pre-owned vehicle sector for the next few years as high interest rates and vehicle prices sustain demand for secondary market alternatives. The U.S. holds the largest share of the global used cars market, accounting for approximately 35% of worldwide used vehicle transactions, reflecting its massive automotive culture and high vehicle ownership rates. As per Statista, the U.S. used car market is valued at over 500 billion U.S. dollars, demonstrating its significant economic impact. The market status is characterized by high liquidity, diverse inventory, and advanced retailing methods. The U.S. serves as a benchmark for global used car trends, with innovations in digital retailing and certified pre-owned programs often originating here. The mature automotive infrastructure supports a robust secondary market, with well-established channels for vehicle acquisition, reconditioning, and resale. Regulatory frameworks vary by state but generally support consumer protection and fair trade practices. The presence of major auction houses and logistics networks facilitates the fficient distribution of vehicles across the country. According to the Bureau of Economic Analysis, motor vehicle and parts dealers contribute significantly to retail sales, highlighting the sector's importance to the national economy. The U.S. market is also a leader in adopting electric vehicles in the used segment, driven by policy incentives and technological advancements. The high average age of vehicles on U.S. roads ensures a steady supply of used cars, sustaining market volume. This dominant position allows the U.S. to influence global pricing and standards in the used automotive sector. The U.S. used cars market is driven by several key factors, including economic pressures, digital transformation, and demographic shifts. High new car prices and interest rates push consumers toward affordable used alternatives, with used vehicle sales outnumbering new sales by a ratio of roughly 2.5 to 1. The expansion of online retailing has enhanced convenience and transparency, with digital sales growing at a double-digit annual rate. An aging vehicle fleet, with an average age of 12.6 years, ensures a consistent supply of trade-ins and off-lease vehicles. Government incentives for electric vehicles are stimulating growth in the used EV segment, with tax credits making these cars more accessible. The strong resale value of SUVs and trucks maintains high demand for these segments, which dominate sales volume. Consumer preference for certified pre-owned programs at franchised dealers builds trust and drives premium sales. Independent dealers are gaining ground.

COMPETITIVE LANDSCAPE

The competition in the U.S. used cars market is intense and characterized by a mix of traditional franchised dealerships, independent lots,s and emerging digital retailers. Large national chains leverage economies of scale to offer competitive pricing and extensive inventory, es while local dealers focus on personalized service and community relationships. Digital native companies have disrupted the traditional model by offering transparent pricing and home delivery services appealing to tech-savvy consumers. Franchised dealers maintain an advantage through certified pre-owned programs and manufacturer support, which builds consumer trust. Independent dealers compete on flexibility and price, often serving niche markets or budget-conscious buyers. The rise of online marketplaces has increased price transparency, forcing all participants to improve value propositions. Regulatory compliance and consumer protection standards add complexity, requiring robust operational frameworks. Technological adoption is now a key differentiator,r with companies investing in artificial intelligence for pricing and inventory management. Customer experience remains central to competitive strategy as buyers demand convenience and reliability. The market continues to evolve with consolidation activities and strategic partnerships shaping the landscape. Participants must continuously innovate to retain market share and adapt to shifting economic conditions and consumer behaviors in this highly fragmented yet dynamic sector.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. Used Cars Market include

- CarMax Inc.

- Carvana Co.

- AutoNation Inc.

- Asbury Automotive Group Inc.

- Lithia Motors Inc.

- Group 1 Automotive Inc.

- TrueCar Inc.

- CarGurus Inc.

- eBay Inc.

- Hendrick Automotive Group

TOP LEADING PLAYERS IN THE MARKET

- CarMax Incorporated stands as a pioneering force in the U.S. used car retail sector by establishing the superstore model that prioritizes transparency and customer experience. The company operates numerous locations nationwide, offering no-haggle pricing and comprehensive vehicle inspections to build consumer trust. Recent actions include significant investments in digital infrastructure to enhance online browsing and home delivery capabilities. CarMax has expanded its reconditioning centers to improve inventory turnover and quality consistency across its network. The firm actively integrates advanced data analytics to optimize pricing strategies and manage inventory levels efficiently. By focusing on customer satisfaction and operational excellence, CarMax strengthens its brand reputation globally. Its innovative approach to used car retailing sets industry standards for service and reliability. The company continues to invest in technology to streamline the buying process and maintain its competitive edge in a rapidly evolving market landscape.

- AutoNation Incorporated serves as a leading automotive retailer in the U.S. with a robust presence in both new and used vehicle segments. The company leverages its extensive dealership network to offer a wide variety of pre-owned cars backed by rigorous certification processes. Recent strategies involve enhancing its digital retail platform to provide seamless online purchasing options and virtual appraisals. AutoNation has invested heavily in logistics and distribution networks to optimize inventory management across its locations. The company focuses on expanding its certified pre-owned offerings to attract quality-conscious buyers seeking warranty protection. By integrating customer relationship management tools, AutoNation improves personalized service and retention rates. Its commitment to sustainability and community engagement further enhances its corporate image. These initiatives allow AutoNation to maintain strong customer loyalty and operational efficiency. The company continues to adapt to market trends by embracing technological innovations and diversifying its service portfolio to meet evolving consumer demands.

- Lithia Motors Incorporated has grown into a major automotive retailer in the U.S. through aggressive acquisitions and organic expansion strategies. The company operates a diverse portfolio of dealerships offering a broad selection of used vehicles to various customer segments. Recent actions include the integration of acquired dealerships into its unified operational framework to maximize synergies and efficiency. Lithia has invested significantly in its digital storefronts and mobile applications to facilitate remote transactions and home deliveries. The company emphasizes speed and convenience in its service models, appealing to modern consumers. By leveraging scale, Lithia negotiates favorable terms with manufacturers and lenders,s enhancing its value proposition. Its focus on employee training and development ensures high service standards across all locations. These efforts strengthen its market position and drive sustainable growth. Lithia continues to explore innovative retail formats and partnerships to expand its reach and improve customer accessibility in the competitive used car landscape.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the U.S. used cars market primarily focus on digital transformation to enhance customer convenience and operational efficiency. Companies invest heavily in online platforms that allow buyers to browse inventory,ry schedule test drives, and complete purchases remotely. Another major strategy involves expanding certified pre-owned programs to build trust and justify premium pricing through rigorous inspections and warranties. Retailers are also optimizing supply chain logistics to improve inventory turnover and reduce holding costs. Strategic acquisitions enable larger firms to consolidate market presence and achieve economies of scale. Personalization through data analytics helps dealers tailor marketing efforts and improve customer retention. These approaches help participants adapt to changing consumer preferences and maintain competitiveness in a dynamic industry landscape.

MARKET SEGMENTATION

This research report on the U.S. used cars market is segmented and sub-segmented into the following categories.

By Vehicle Type

- Sport Utility Vehicles (SUVs)

- Hatchbacks

By Sales Channel Type

- Offline

- Online

By Fuel Type

- Petrol

- Electric Vehicles

By Distribution Channel

- Franchised Dealers

- Independent Dealers

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com