U.S. Healthcare Market Size, Share, Trends, and Growth Analysis Report, Segmented By End-User, Service, Type, Payer Type, & Country (U.S.), Industry Forecast From 2026 to 2034

U.S. Healthcare Market Size

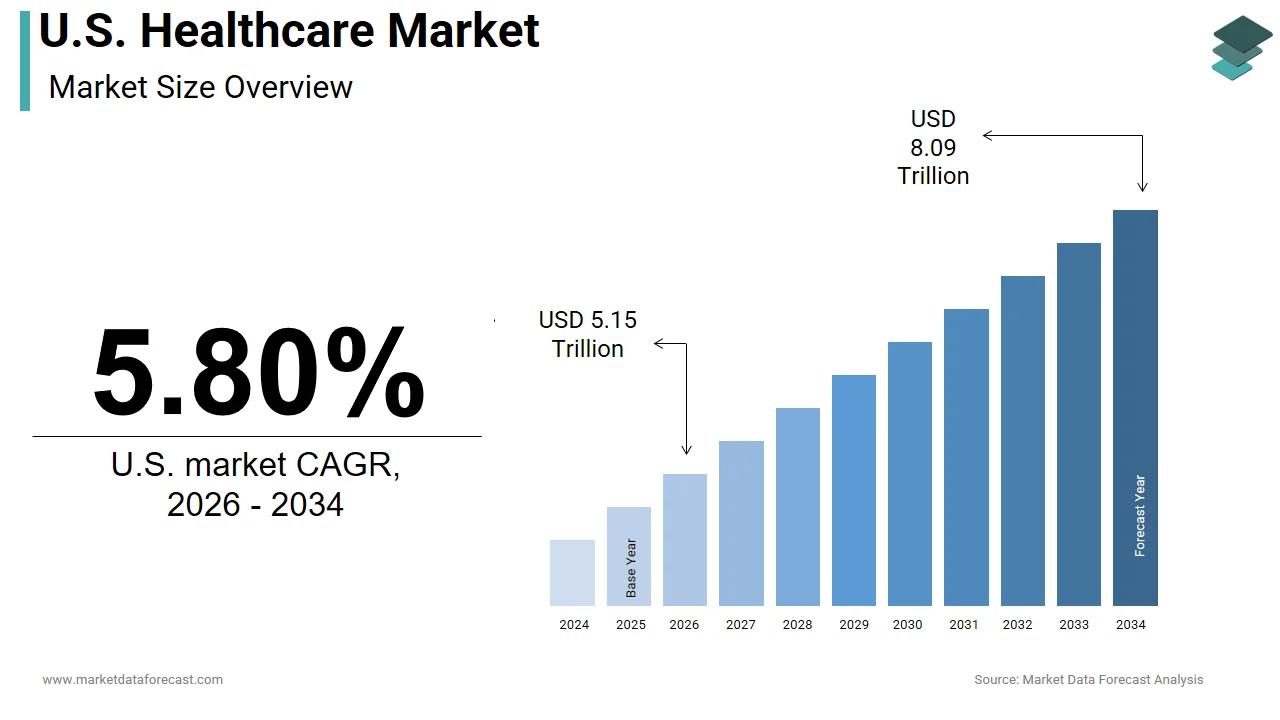

The U.S. healthcare market was valued at USD 4.87 trillion in 2025, is estimated to reach USD 5.15 trillion in 2026, and is projected to reach USD 8.09 trillion by 2034, growing at a CAGR of 5.80% from 2026 to 2034.

Healthcare is a vast, multi-layered ecosystem encompassing providers, payers, pharmaceutical innovators, and technology enablers, functioning not merely as a service industry but as a socio-economic infrastructure. According to the Centers for Disease Control and Prevention, over 1.2 million licensed physicians and 15.7 million allied health professionals operate across 6,093 hospitals and 1.2 million ambulatory clinics nationwide.

MARKET DRIVERS

Chronic Disease Prevalence Fueling Sustained Care Demand

The inexorable rise in chronic conditions, particularly diabetes, cardiovascular disease, and obesity-related comorbidities, is driving the growth of the U.S. Healthcare Market. According to the Centers for Disease Control and Prevention, 6 in 10 U.S. adults now live with at least one chronic disease, and 4 in 10 have two or more, driving 90% of the nation’s $4.3 trillion annual healthcare expenditure. The American Heart Association documents that cardiovascular disease alone accounts for 875,000 hospitalizations annually, with average treatment costs exceeding $21,000 per admission.

Aging Population Intensifying Utilization Pressure

Demographic aging is increasing the utilization intensity in post-acute, pharmaceutical, and chronic care domains, which is escalating the growth of the U.S. Healthcare Market. As per the U.S. Census Bureau’s 2023 National Population Projections, adults aged 65 and older will comprise 22% of the U.S. population by 2030. According to the Centers for Medicare & Medicaid Services, over 85 consume 3.2 times more inpatient days and 4.1 times more home health visits than those aged 65–74.

MARKET RESTRAINTS

Administrative Fragmentation Inflating Systemic Costs

The U.S. healthcare system’s operational inefficiency stems from its fragmented payer-provider-administrator architecture, which imposes disproportionate overhead. According to the Journal of the American Medical Association’s 2023 cost decomposition analysis, administrative expenses consume 34% of total hospital revenue, nearly double the Canadian benchmark. The Medical Group Management Association documents that U.S. physician practices spend an average of $102,000 annually per full-time physician on billing and insurance verification alone.

Workforce Shortages Constricting Access and Capacity

A deficit in clinical and support personnel is throttling care delivery capacity, particularly in primary care, mental health, and rural settings. As per the Association of American Medical Colleges, the U.S. will face a shortage of up to 124,000 physicians by 2034, with primary care accounting for 48% of the gap. The Health Resources and Services Administration designates 7,400 geographic areas as Primary Care Health Professional Shortage Areas, affecting 85 million Americans. Compounding this, the American Nurses Association projects a deficit of 1.1 million registered nurses by 2030, exacerbated by 31% of current RNs planning retirement within five years. These shortages force extended wait times, provider burnout, and care migration to higher-cost settings, undermining both access and affordability.

MARKET OPPORTUNITIES

Value-Based Care Models Unlocking Systemic Efficiency

The migration from fee-for-service to outcome-aligned reimbursement creates structural incentives for preventive care, care coordination, and cost containment is creating new opportunities for the growth of the U.S. Healthcare Market. According to the Centers for Medicare & Medicaid Services, 40% of traditional Medicare payments were tied to alternative payment models in 2023, with accountable care organizations reducing hospital admissions by 8.3% and saving $2.3 billion annually. The National Committee for Quality Assurance reports that value-based contracts covering 150 million Americans now mandate standardized quality metrics, driving adoption of remote monitoring and chronic disease registries. Simultaneously, the Bipartisan Policy Center documents that bundled payment programs for joint replacements reduced episode costs by 21% without compromising outcomes.

Digital Therapeutics and AI-Enabled Diagnostics Scaling Precision Care

The integration of regulatory approval pathways and clinical validation is enabling software-based interventions to function as reimbursable medical tools, which is expected to escalate the growth of the U.S. Healthcare Market. As per the Food and Drug Administration’s Digital Health Center of Excellence, 67 prescription digital therapeutics received authorization in 2023. Simultaneously, the Centers for Medicare & Medicaid Services expanded coverage for remote therapeutic monitoring in 2023, enabling reimbursement for software tracking medication adherence and musculoskeletal therapy.

MARKET CHALLENGES

Health Equity Gaps Undermining Systemic Outcomes

Persistent disparities in access, quality, and outcomes across racial, socioeconomic, and geographic lines corrode system performance and inflate long-term costs, which is a majorly challenge to the growth of the U.S. Healthcare Market. According to the Agency for Healthcare Research and Quality’s 2023 National Healthcare Quality and Disparities Report, Black and Native American patients experience 40% higher preventable hospitalization rates for diabetes and hypertension than their white peers. The Commonwealth Fund documents that rural residents face 67% longer travel times to Level I trauma centers and 38% fewer mental health providers per capita. Simultaneously, the Kaiser Family Foundation confirms Medicaid enrollees are 3.2 times more likely to report difficulty accessing specialists than privately insured patients.

Drug Pricing Volatility and Supply Chain Fragility

The pharmaceutical cost instability and manufacturing concentration expose the system to therapeutic disruption and budgetary shock is also degrading the growth of the U.S. Healthcare Market. As per the U.S. Government Accountability Office, 47% of essential generic drugs experienced at least one shortage in 2023, with 82% of active pharmaceutical ingredients sourced from only three countries: China, India, and Italy.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By End User, Service, Type, and Country. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | U.S |

| Market Leaders Profiled | Apollo Hospitals Enterprise Ltd, athenahealth Inc., Community Health Systems Inc., CVS Health Corp., DaVita Inc., Dr Lal PathLabs Ltd, Expedient Healthcare Marketing Pvt. Ltd., Fresenius Medical Care AG and Co. KGaA, Genesis Healthcare Inc., iHealth Labs Inc., Max Healthcare Institute Ltd, Mayo Foundation for Medical Education and Research, McKesson Corp., OMH HealthEdge Holdings LLC, Optum Inc., Quest Diagnostics Inc., Sonic Healthcare Ltd, Universal Health Services Inc., West Suffolk NHS Foundation Trust. |

SEGMENTAL ANALYSIS

By End-User Insights

The adult care segment, which includes individuals aged 19 to 64, held 58.2% of the U.S. healthcare market share in 2024, with the increasing chronic disease burden and workforce-linked insurance coverage. The Centers for Disease Control and Prevention confirms that 119 million working-age adults manage at least one chronic condition, driving 76% of all prescription fills and 63% of outpatient visits. The Agency for Healthcare Research and Quality reports that this cohort accounts for 82% of all emergency department visits for preventable conditions, which is a reflection of fragmented primary care access and delayed intervention.

The geriatric care segment is likely to grow with an expected CAGR of 7.9% during the forecast period. As per the Centers for Medicare & Medicaid Services, beneficiaries aged 85+ consume 3.2 times more hospital days and 4.1 times more home health visits than those aged 65–74. The National Institute on Aging reports 80% of seniors manage at least one chronic condition, and 50% have three or more, necessitating polypharmacy and multidisciplinary coordination.

By Service Insights

The hospitals and clinics segment was the largest and held 42.3% of the U.S. Healthcare Market share in 2024. As per the Agency for Healthcare Research and Quality, 68% of all advanced imaging and 92% of surgical procedures occur within hospital systems, which is driven by regulatory mandates, technology concentration, and liability frameworks. Simultaneously, the Medicare Payment Advisory Commission reports that 73% of commercially insured patients receive initial cancer diagnosis and staging within hospital-affiliated oncology networks, anchoring downstream revenue. This institutional gravity persists despite cost pressures, as licensure, accreditation, and capital intensity create near-insurmountable barriers to substitution.

The home healthcare segment is growing lucratively with an expected CAGR of 11.2% during the forecast period. According to the National Association for Home Care & Hospice, there has been a 41% increase in home infusion and ventilator-dependent care since 2020, enabled by portable diagnostics and payer-aligned risk contracts. This segment’s expansion represents not convenience but systemic re-engineering, shifting acuity, cost, and accountability from institutions to households.

By Type Insights

The outpatient services segment accounted in holding 47.3% of the U.S. Healthcare Market share in 2024 due to technological enablement and payer-driven site-of-service optimization. The American Medical Association confirms that 89% of all physician encounters now occur in ambulatory settings, with same-day surgical volume growing 9.3% annually. The U.S. Government Accountability Office documents that Medicare’s site-neutral payment policy reduced hospital outpatient department growth by 14% while accelerating freestanding clinic expansion.

The telehealth segment is likely to grow with an expected CAGR of 23.6% during the forecast period, with the regulatory permanence and generational adoption. The Centers for Medicare & Medicaid Services made 250 telehealth services permanently reimbursable in 2023, covering 48 million beneficiaries. This is not a pandemic artifact but a systemic rewiring collapsing geography, redistributing workforce capacity, and embedding asynchronous care into chronic disease management.

REGIONAL ANALYSIS

The United States healthcare market is the largest contributor by occupying a dominant share with high investments in the expansion of the healthcare units. The U.S. National Institutes of Health funds 41% of global biomedical research, anchoring therapeutic innovation, while the Food and Drug Administration approves 62% of novel therapeutics worldwide. Unlike single-payer systems, the U.S. functions as a laboratory of payment models, digital adoption, and provider entrepreneurship, exporting clinical protocols and health tech while struggling with equity and efficiency.

COMPETITIVE LANDSCAPE

Competition in the U.S. healthcare market is defined not by facility count or insurance enrollment but by intellectual export, protocol standardization, and digital enablement across global care ecosystems. Players vie to embed their clinical workflows, data architectures, and reimbursement models into international systems in the Asia Pacific, where infrastructure expansion outpaces human capital development. Differentiation stems from licensable care pathways, AI-validated diagnostics, and governance frameworks that elevate quality while containing cost.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. healthcare market include

- Apollo Hospitals Enterprise Ltd

- athenahealth Inc.

- Community Health Systems Inc.

- CVS Health Corp.

- DaVita Inc.

- Dr Lal PathLabs Ltd.

- Expedient Healthcare Marketing Pvt. Ltd.

- Fresenius Medical Care AG and Co. KGaA

- Genesis Healthcare Inc.

- iHealth Labs Inc.

- Max Healthcare Institute Ltd

- Mayo Foundation for Medical Education and Research

- McKesson Corp.

- OMH HealthEdge Holdings LLC

- Optum Inc.

- Quest Diagnostics Inc.

- Sonic Healthcare Ltd.

- Universal Health Services Inc.

- West Suffolk NHS Foundation Trust

Top Strategies Used by Key Market Participants

Key players deploy clinical protocol licensing, digital care enablement platforms, regional training academies, value-based care infrastructure exports, and cross-border data interoperability frameworks to fortify market positioning. They embed U.S. diagnostic and treatment standards through physician certification and hospital management contracts. Digital consult platforms extend specialist reach without physical presence. Training institutes institutionalize American care models in local systems.

Top Players in the Market

- In the U.S. healthcare market, UnitedHealth Group leverages its Optum platform to export integrated care delivery and data analytics capabilities across Asia Pacific. In 2023, it partnered with Thailand’s Bumrungrad International Hospital to deploy AI-driven chronic care pathways for diabetes and hypertension. Early 2024 saw Optum launch a regional value-based care accelerator in Singapore, training 42 hospital systems in risk-sharing contract design. It also integrated its claims adjudication engine with Japan’s Tokio Marine to streamline cross-border employer health plans. These moves position UnitedHealth not as an insurer but as an operational architect by embedding its care coordination and payment innovation into Asia’s evolving universal coverage frameworks.

- Mayo Clinic extends U.S. clinical excellence into the Asia Pacific through knowledge licensing and physician training rather than physical expansion. In late 2023, it signed a 10-year clinical governance agreement with India’s Apollo Hospitals, standardizing oncology and cardiology protocols across 73 facilities. In Q1 2024, it launched “Mayo Expert Advisor,” a real-time consult platform for Southeast Asian clinicians managing complex cases. Simultaneously, it co-developed a telepathology validation system with Singapore General Hospital, enabling remote biopsy interpretation compliant with U.S. CAP standards. These initiatives embed Mayo’s diagnostic rigor and care protocols without brick-and-mortar investment, transforming its brand into a licensable clinical operating system across high-growth Asian markets.

- Cleveland Clinic exports its integrated physician-led model and specialty care protocols to Asia Pacific through management contracts and digital academies. In 2023, it assumed operational control of Abu Dhabi’s Sheikh Shakhbout Medical City’s cardiology and transplant services — a gateway to South Asian referral networks. In February 2024, it launched the “Global Care Pathway Institute” in Manila, certifying 280 Asian hospital administrators in U.S.-style care coordination and revenue cycle optimization. It also partnered with South Korea’s Asan Medical Center to co-validate AI algorithms for early sepsis detection.

MARKET SEGMENTATION

This research report on the U.S. healthcare market has been segmented and sub-segmented into the following categories.

By End-user

- Adult care

- Geriatric care

- Pediatric care

By Service

- Hospitals and clinics

- Primary care services

- Long-term care services

- Home healthcare

- Others

By Type

- Inpatient Services

- Outpatient Services

- Diagnostic Services

- Telehealth

By Payer Type

- Public Insurance

- Private Insurance

- Out-of-Pocket

By Country

- U.S

Frequently Asked Questions

1. What is the U.S. Healthcare Market?

The U.S. Healthcare Market includes services, providers, payers, technology, pharmaceuticals, insurance, and regulatory bodies that make up the country's vast healthcare ecosystem

2. What are the main trends in the U.S. Healthcare Market for 2025?

Trends include digital health adoption, telemedicine growth, value-based care models, increased healthcare IT investments, precision medicine, and regulatory changes post-2024 elections

3. Which sectors drive the U.S. Healthcare Market growth?

Major sectors include hospital care, outpatient and ambulatory services, pharmacy, health insurance, digital health platforms, and pharmaceuticals

4. How is digital health impacting the U.S. Healthcare Market?

Digital health ncluding telehealth, cloud platforms, and remote monitoring—is driving scalable, efficient, and personalized care, improving population health management and chronic disease outcomes

5. Who are the top players in the U.S. Healthcare Market?

Major organizations include HHS, CMS, UnitedHealth Group, Anthem, Aetna, Epic Systems, Cerner, and leading hospital systems and pharmacy chains

6. What role does telehealth play in the U.S. Healthcare Market?

Telehealth services support remote and rural care delivery, increasing access, enhancing patient satisfaction, and reducing unnecessary hospital visits

7. How is AI transforming the U.S. Healthcare Market?

AI is used in diagnostics, surgery assistance, data analytics, workflow automation, and personalized medicine, supporting faster, more accurate, and cost-effective healthcare

8. How do regulatory changes affect the U.S. Healthcare Market in 2025?

Shifts in federal, state, and local policy following the 2024 elections will alter reimbursement, coverage, health equity initiatives, and regulatory compliance strategies for providers and insurers

9. What challenges exist in the U.S. Healthcare Market?

Ongoing challenges include rising costs, workforce shortages, health equality gaps, regulatory complexity, cybersecurity risks, and pandemic after-effects

10. How is value-based care being adopted in the U.S. Healthcare Market?

Value-based care ties provider reimbursement to patient outcomes and cost efficiency, expanding through Medicare/Medicaid and private payer initiatives

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com