Global Veterinary Software Market Size, Share, Trends & Growth Forecast Report By Type of Software, Delivery Model, Practice Type, End-Use and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Global Veterinary Software Market Report Summary

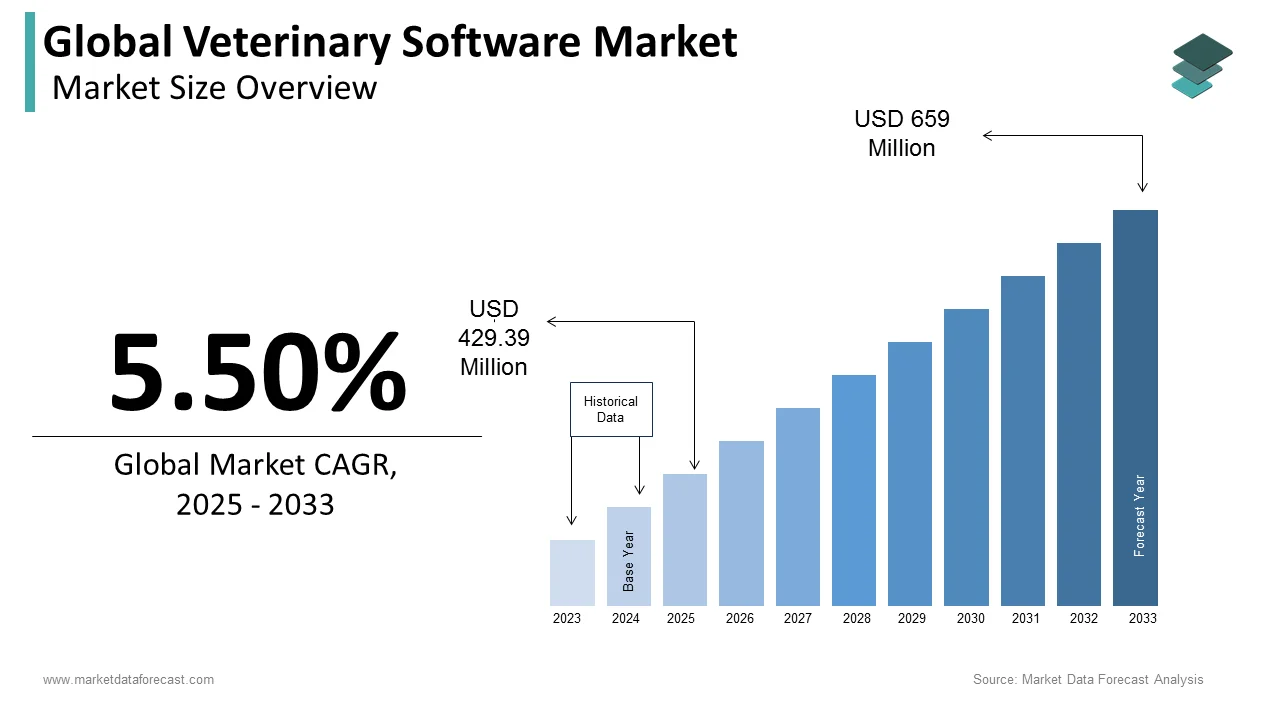

The global veterinary software market was valued at USD 429.39 million in 2025, is estimated to reach USD 453.01 million in 2026, and is projected to reach USD 695 million by 2034, growing at a CAGR of 5.50% from 2026 to 2034. Market growth is driven by the increasing adoption of digital solutions in veterinary practices, rising pet ownership, and growing demand for efficient clinic management systems. Veterinary software solutions help streamline operations, improve patient record management, and enhance clinical decision-making. The growing trend of treating pets as family members, coupled with advancements in cloud-based technologies, is further supporting market expansion globally.

Key Market Trends

- Increasing adoption of digital practice management solutions in veterinary clinics.

- Rising trend of pet humanization and increased spending on animal healthcare.

- Growing demand for cloud-based and web-enabled veterinary software.

- Expansion of data-driven decision-making and electronic health records.

- Increasing focus on regulatory compliance and animal health tracking.

Segmental Insights

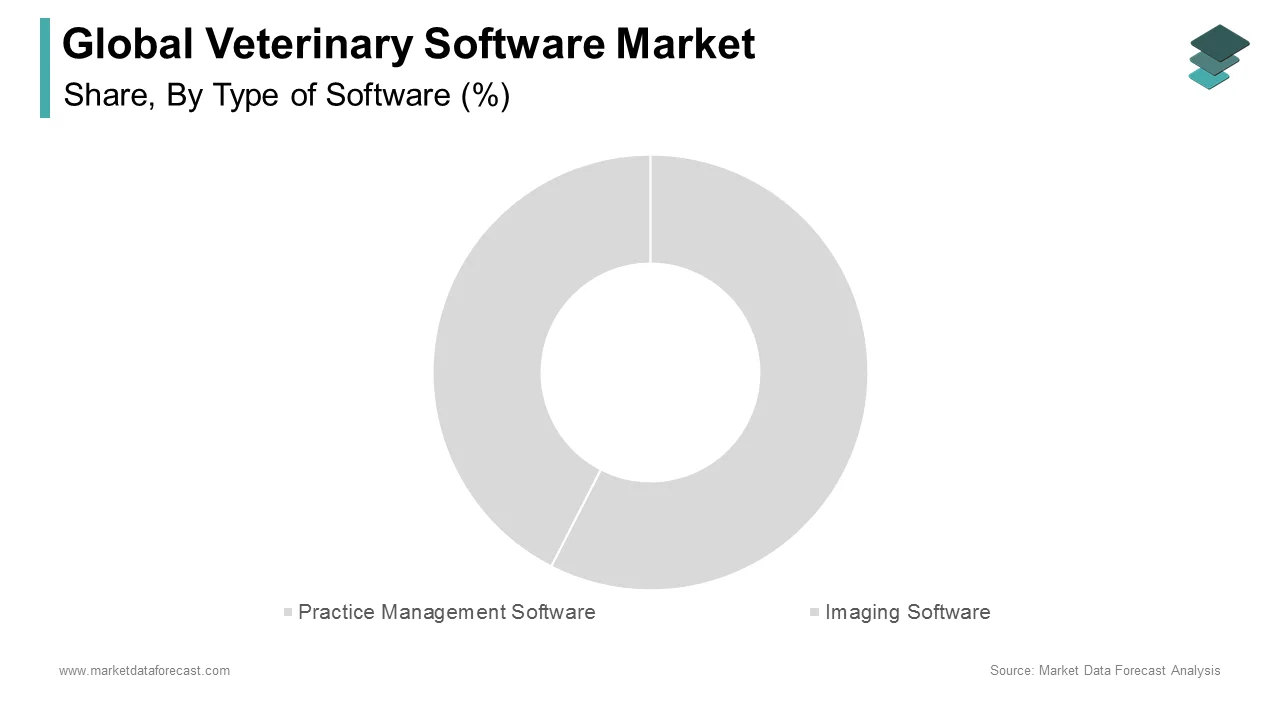

- Based on type of software, the practice management software segment held a significant share in the global veterinary software market in 2025, driven by its role in streamlining clinic operations.

- Based on delivery model, the cloud/web-based segment dominated the market in 2025 due to its scalability, accessibility, and cost efficiency.

- Based on end user, the hospitals segment led the market by capturing 58.4% share in 2025, supported by increasing adoption of digital systems in veterinary hospitals.

Regional Insights

The global veterinary software market is witnessing steady growth across regions due to increasing digitalization and pet healthcare demand.

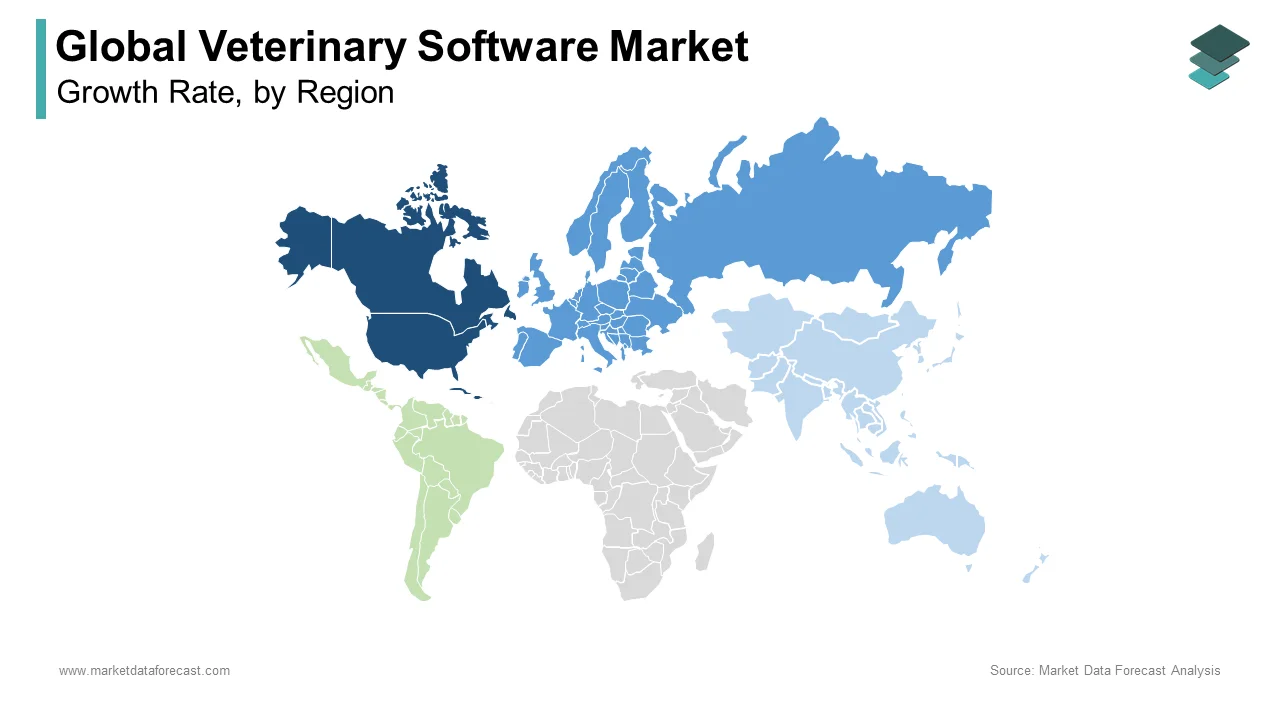

- North America led the market in 2025 with 42.3% share, supported by high pet ownership and advanced veterinary infrastructure.

- Europe is expected to witness steady growth driven by stringent regulatory requirements for animal health tracking and a high density of veterinary practices.

- Asia-Pacific is anticipated to grow significantly due to urbanization, rising disposable incomes, and increasing pet adoption trends.

Competitive Landscape

The global veterinary software market is moderately competitive, with the presence of specialized software providers and healthcare technology companies. Market players are focusing on enhancing software capabilities, expanding cloud-based offerings, and integrating advanced analytics. Strategic partnerships, product innovation, and expansion into emerging markets are shaping competitive dynamics across the industry.

Prominent companies operating in the global veterinary software market include Britton's Wise Computer, Inc., Firmcloud Corporation, Covetrus Inc., IDEXX Laboratories Inc., Timeless Veterinary Systems, Inc., Henry Schein One, ezyVet Limited, MedaNext Inc., and Animal Intelligence Software, Inc.

Global Veterinary Software Market Size

The size of the global veterinary software market was worth USD 429.39 million in 2025. The global market is anticipated to grow at a CAGR of 5.50% from 2026 to 2034 and be worth USD 695 million by 2034 from USD 453.01 million in 2026.

The veterinary software is a specialized suite of digital solutions designed to manage the operational, clinical, and administrative functions of animal healthcare facilities. These systems encompass practice management platforms, electronic health records, telemedicine interfaces, and inventory control tools tailored specifically for companion animals, livestock, and exotic species. The nature of these tools is the escalating volume of animal patients requiring care as pet ownership reaches historic highs globally. According to the American Pet Products Association, approximately 66% of households in the United States own a pet, which translates to roughly 85 million families seeking regular veterinary services. Furthermore, the European Commission indicates that over 260 million pets reside within the European Union, creating a massive demand for organized healthcare delivery systems. As per the World Organisation for Animal Health, the global push towards better animal welfare standards and disease surveillance necessitates robust digital record keeping to track vaccination histories and outbreak patterns. The definition of this market extends beyond simple data entry to include advanced analytics for population health management and regulatory compliance reporting. The increasing complexity of veterinary medicine, which now mirrors human healthcare in sophistication, drives the urgent need for integrated software solutions to handle diverse clinical scenarios efficiently.

MARKET DRIVERS

Surging Pet Ownership Rates and Humanization Trends Amplify Service Demand

The unprecedented rise in pet ownership, coupled with the deepening emotional bond between owners and their animals, is propelling the growth of the veterinary software market. Pets are increasingly viewed as family members, leading owners to seek higher-quality medical care, including advanced diagnostics, surgical procedures, and preventive wellness plans. These clinics are to handle higher patient volumes necessitating automated systems for appointment booking, reminder services, and client communication to maintain efficiency. The humanization trend also drives demand for detailed electronic health records that allow owners to access vaccination certificates, dietary plans, and treatment histories via mobile applications. Consequently, veterinary practices are compelled to upgrade from manual or legacy systems to modern cloud-based platforms that can manage complex billing, insurance claims, and loyalty programs. This surge in demand ensures that software providers continue to innovate features that enhance the client experience and optimize clinic throughput to accommodate the growing number of animal patients.

Regulatory Mandates for Animal Disease Tracking and Food Safety Compliance

The implementation of stringent government regulations regarding animal disease surveillance and food safety, particularly in the livestock and mixed animal sectors, is also escalating the growth of the veterinary software market. Authorities worldwide are enforcing rigorous documentation requirements to monitor zoonotic diseases, track medication usage, and ensure the safety of the food supply chain from farm to fork. According to the World Organisation for Animal Health, member countries are required to report specific notifiable diseases within 24 hours of confirmation, necessitating real-time digital reporting capabilities that only modern software can provide. The European Food Safety Authority mandates comprehensive traceability for all livestock movements and veterinary drug administrations within the European Union, forcing farmers and veterinarians to adopt compliant digital record-keeping systems. These regulatory pressures eliminate the viability of paper-based records, which are prone to errors and inefficiencies in reporting. Furthermore, the threat of emerging infectious diseases such as avian influenza and foot and mouth disease drives governments to subsidize digital infrastructure for early detection and rapid response. This regulatory landscape creates a non-negotiable demand for software solutions that offer secure data storage, automated reporting, and seamless integration with national animal health databases.

MARKET RESTRAINTS

High Implementation Costs and Financial Constraints of Small Practices

The substantial financial burden associated with acquiring, implementing, and maintaining advanced veterinary software systems for small independent clinics and rural practices is limiting the growth of the veterinary software market. The initial investment often includes licensing fees, hardware upgrades, data migration costs, and extensive staff training, which can strain the limited capital reserves of smaller businesses. As per the American Animal Hospital Association, nearly 30% of veterinary practices operate with profit margins below 5%, making large capital expenditures for technology prohibitive without external financing. As per the Bureau of Labor Statistics, the rising operational costs, including rent, utilities, and labor, have further squeezed budgets, leaving little room for technology investments in many regions. Additionally, the transition from legacy systems often results in temporary productivity losses as staff adapt to new interfaces, potentially impacting revenue during the critical implementation phase. These economic barriers force many practitioners to rely on outdated software or manual processes that lack the efficiency and features of modern solutions. The high total cost of ownership discourages widespread adoption, especially in developing markets where veterinary services are already price sensitive, limiting the overall market penetration of premium software products.

Shortage of Technologically Skilled Veterinary Staff and Resistance to Change

The scarcity of veterinary professionals proficient in digital technologies, coupled with inherent resistance to changing established workflows with the rapid adoption of new software solutions, is also degrading the growth of the veterinary software market. Many experienced veterinarians and technicians trained in traditional methods find it challenging to adapt to complex digital interfaces and automated processes, leading to frustration and reduced utilization of available features. According to the Association of American Veterinary Medical Colleges, there is a persistent gap in digital literacy training within veterinary curricula, leaving new graduates ill-prepared to maximize the potential of advanced practice management systems. As per a survey by the British Veterinary Association, many veterinary staff expressed anxiety regarding the introduction of new technology, citing fears of increased workload and technical glitches during patient consultations. This resistance is often compounded by poor user interface design in some software products, which fails to align with the fast-paced nature of clinical environments. The lack of dedicated IT support within most veterinary clinics means that even minor technical issues can halt operations entirely, discouraging further investment in digital tools.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence for Diagnostic Support and Predictive Analytics

The incorporation of artificial intelligence and machine learning algorithms into veterinary software to enhance diagnostic accuracy and enable predictive health monitoring for animal patients is expected to bolster new opportunities for the growth of the veterinary software market. AI-driven tools can analyze medical images such as X-rays and ultrasounds to detect abnormalities with speed and precision that surpasses human capability in certain scenarios. According to the Journal of the American Veterinary Medical Association, AI-assisted diagnostic tools have improved in identifying early-stage tumors and orthopedic issues in companion animals compared to traditional review methods. The potential for predictive analytics allows software to analyze historical patient data to forecast disease outbreaks or identify individuals at risk for chronic conditions like diabetes or kidney failure. As per McKinsey and Company, the application of AI in veterinary care could reduce diagnostic errors and optimize treatment plans, leading to better outcomes and lower long term costs for pet owners. Furthermore, AI-powered chatbots and virtual assistants integrated into practice management systems can handle routine client inquiries, appointment scheduling, and triage, freeing up staff to focus on critical care tasks. This technological evolution positions software vendors to offer premium value-added services that differentiate their products in a crowded market. The ability to provide data-driven insights transforms veterinary software from a mere administrative tool into a critical clinical partner, driving significant growth opportunities for innovators in the sector.

Expansion of Telemedicine and Remote Monitoring Capabilities

The rapid growth of telemedicine and remote patient monitoring technologies for veterinary software developers to extend care beyond the physical confines of the clinic is expected to fuel the opportunities for the growth of the veterinary software market. The pandemic accelerated the acceptance of virtual consultations, and clients now expect flexible options for follow-up visits, behavioral counseling, and nutritional advice via digital platforms. According to the American Telemedicine Association, the volume of veterinary telehealth consultations increased by 150% between 2022 and 2025, indicating a permanent shift in how care is delivered. Software platforms that seamlessly integrate video conferencing, secure messaging, and remote data ingestion from wearable devices are poised to capture this expanding market segment. As per the Federation of Veterinarians of Europe, new guidelines formally recognizing telemedicine as a valid component of veterinary practice have opened regulatory pathways for broader adoption across member states. The integration of Internet of Things devices, such as smart collars and activity monitors, allows software to track vital signs, movement patterns, and sleep quality in real time, enabling proactive interventions. This capability is particularly valuable for managing chronic conditions in elderly pets or monitoring livestock health in remote locations.

MARKET CHALLENGES

Critical Issues Regarding Data Interoperability and Fragmented Ecosystems

The lack of standardized data formats and seamless interoperability between different veterinary software systems for the efficient exchange of patient information is one of the challenges for the growth of the veterinary software market. Veterinary practices often utilize a mix of specialized tools for imaging, laboratory results, and practice management, which frequently fail to communicate effectively, leading to data silos and fragmented patient records. According to the Health Level Seven International organization, the absence of a universally adopted data standard like HL7 FHIR in veterinary medicine results in significant manual effort to transfer records between clinics and specialists. As per the European Commission, the fragmentation of the market with hundreds of small software vendors each using proprietary databases complicates efforts to create a unified national or regional animal health network. This incompatibility hinders the ability to conduct large-scale epidemiological studies and track disease trends effectively across borders. Furthermore, the difficulty in migrating data when switching providers locks practices into suboptimal systems due to the fear of data loss or corruption.

Escalating Cybersecurity Threats and Data Privacy Concerns

The increasing frequency of cyberattacks targeting veterinary clinics and the sensitive data that threatens the integrity and trustworthiness of veterinary software systems is also inhibiting the growth of the veterinary software market. Veterinary practices store vast amounts of personally identifiable information about pet owners, along with detailed medical records and financial data, making them attractive targets for ransomware and phishing schemes. The European Data Protection Board emphasizes that veterinary clinics must comply with strict GDPR regarding the protection of client data, facing severe fines for any breaches or negligence. The reliance on cloud-based solutions introduces additional vulnerabilities if providers do not implement state of the art encryption and access controls. Furthermore, the lack of cybersecurity awareness among veterinary staff often leads to accidental data leaks through weak passwords or unsecured devices. Addressing these security challenges requires continuous investment in advanced threat detection and regular staff training, which can be resource-intensive for software vendors and clinics alike.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type of Software, Delivery Model, Practice Type, End-User, & Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Britton's Wise Computer, Inc. (U.S.), Firmcloud Corporation (U.S.), Timeless Veterinary Systems, Inc. (Canada), ezyVET Limited (New Zealand), MedaNext Inc. (U.S.), and Animal Intelligence Software, Inc. (U.S.).

|

SEGMENTAL ANALYSIS

By Type of Software Insights

The practice management software segment accounted for a significant share of the global veterinary software market in 2025. The growth of the segment is likely to be driven by the need for integrated billing, scheduling, and inventory control systems that reduce operational overhead and prevent revenue leakage. According to the American Animal Hospital Association, practices utilizing comprehensive management software experience an increase in collected revenue due to automated invoicing and reduced missed appointments compared to manual systems. The regulatory pressure to maintain detailed electronic health records for compliance with animal welfare and drug dispensing laws is also influencing the growth of the segment. As per the European Commission, veterinarians across the European Union are mandated to keep digital records of all prescription medications for food-producing animals for at least five years, forcing a widespread migration from paper logs to digital platforms. These systems serve as the central hub for all clinic data, making them indispensable for daily operations.

The imaging software segment is projected to register the fastest CAGR of 14.2% during the forecast period, driven by the rapid adoption of advanced diagnostic modalities and the need for specialized image analysis tools. This rapid expansion is fueled by the increasing availability of high-resolution digital radiography, ultrasound, and computed tomography systems in veterinary practices, which require sophisticated software for image storage and interpretation. The integration of artificial intelligence algorithms that assist veterinarians in detecting fractures, tumors, and soft tissue abnormalities with greater accuracy is contributing to the growth of the segment. The rising demand for teleradiology services, which allows general practitioners to send complex images to specialists for remote interpretation necessitating secure cloud-based imaging platforms.

By Delivery Model Insights

The cloud/web-based segment was the largest by holding a dominant share of the veterinary software market in 2025 due to its flexibility, scalability, and lower upfront costs. This dominance is driven by the shifting preference of modern veterinary practices toward subscription-based models that eliminate the need for expensive on-site servers and dedicated IT staff. The ability of cloud solutions to provide seamless remote access to patient data enables veterinarians to work from multiple locations or offer telemedicine services effectively. According to the Veterinary Information Network, over 75% of new veterinary practices established in 2025 chose cloud-based systems specifically for their ability to support mobile workflows and remote monitoring capabilities. The automatic update mechanism inherent in cloud platforms, which ensures that all users always have the latest security patches and feature enhancements without manual intervention. As per the British Veterinary Association, the risk of data loss due to local hardware failure is significantly reduced with cloud hosting, where data is replicated across multiple secure data centers, providing peace of mind for clinic owners. The cost efficiency of paying a monthly fee rather than a large capital expenditure makes these solutions accessible to small and medium-sized clinics, further expanding their market penetration.

The cloud/web-based segment is anticipated to witness a CAGR of 13.8% from 2026 to 2034, owing to the aggressive migration of legacy on-premises systems to cloud infrastructure. The superior scalability of cloud architectures, which allows practices to instantly add users or storage capacity as they expand without costly hardware upgrades, is boosting the growth of the veterinary software market. According to research, the total cost of ownership for cloud-based veterinary software is 40% lower over a five year period compared to on-premises solutions when factoring in maintenance, energy, and upgrade costs. The second factor is the enhanced collaboration features of web-based platforms that facilitate real-time data sharing between veterinarians, specialists, and pet owners through secure portals. As per the Federation of Veterinarians of Europe, the ability to share live patient records across borders has become essential for treating traveling pets and managing transboundary diseases, driving rapid adoption in international clinics. The combination of economic advantages and operational resilience ensures that the cloud segment will continue to outpace all other delivery models in terms of growth velocity.

By End-User Insights

The hospitals segment accounted in holding 58.4% of the veterinary software market share in 2025. Veterinary hospitals handle a high volume of emergency cases, surgical procedures, and inpatient care, which necessitates robust software capable of managing intricate workflows and large datasets. According to the American College of Veterinary Emergency and Care, hospitals processing over 10000 cases annually rely on advanced software to reduce medical errors by 25% through automated drug interaction checks and dosage calculations. The requirement for detailed reporting and analytics to monitor key performance indicators, such as bed occupancy rates, surgical success rates, and client retention metrics. The sheer scale of operations and the critical nature of the services provided ensure that hospitals remain the primary consumers of high-end veterinary software solutions globally.

The reference laboratories segment is swiftly emerging at a fastest CAGR of 12.5% from 2026 to 2034, with the increasing outsourcing of diagnostic testing by general practitioners. As veterinary medicine becomes more specialized, small clinics are sending more samples to external labs for advanced pathology, microbiology, and genetic testing, driving demand for laboratory information management systems. The need for seamless digital integration between clinic practice management software and laboratory systems to ensure rapid turnaround of results is also driving the growth of the segment. The second factor is the implementation of automated result posting features that instantly upload lab data into the patient record, eliminating manual entry errors and speeding up treatment decisions. As per Idexx Laboratories, one of the leading providers of veterinary diagnostics, digital connectivity has reduced the average time to receive results from 24 hours to under 4 hours for tests. This efficiency gain encourages higher testing volumes and drives laboratories to invest in advanced software platforms that can handle massive throughput and complex data analytics.

REGIONAL ANALYSIS

North America Veterinary Software Market Analysis

North America was the top performer in the global veterinary software market by holding 42.3% of the share in 2025, with high pet ownership rates and advanced technological adoption. The region benefits from a mature healthcare infrastructure for animals, where practice management systems are considered essential rather than optional tools for clinic efficiency. According to the American Pet Products Association, over 70% of households in the United States own a pet, translating to a massive volume of patient visits that require sophisticated scheduling, billing, and electronic health record management. The presence of major software vendors like IDEXX Laboratories and Covetrus within the United States fosters a competitive environment that accelerates the development of cloud-based solutions and telemedicine platforms. As per the American Veterinary Medical Association, the average revenue per veterinary practice has increased significantly due to the implementation of integrated software that reduces administrative burdens and improves client communication. Furthermore, the high prevalence of pet insurance in North America necessitates software capable of seamless claims processing and real-time verification, which further entrenches the use of advanced digital systems. The strong regulatory framework regarding animal health data privacy also drives clinics to adopt secure, compliant software solutions.

Europe Veterinary Software Market Analysis

Europe veterinary software market growth is likely to be driven by the stringent regulatory requirements for animal health tracking and a high density of veterinary practices. The region operates under strict European Union mandates regarding the traceability of livestock and the prescription of veterinary medicines, which forces clinics to adopt digital record-keeping systems over manual logs. The growing preference for cloud-based platforms that facilitate cross-border data exchange and compliance with the General Data Protection Regulation for client information is also prompting the growth of the market. As per Eurostat, the number of pets in the European Union exceeds 300 million, with dogs and cats representing the largest segments driving demand for companion animal management tools. Countries like Germany, France, and the United Kingdom lead the regional adoption due to their robust healthcare spending and early integration of digital health records. The increasing focus on One Health initiatives, which link animal, human, and environmental health, also encourages the use of software capable of epidemiological surveillance and reporting.

Asia-Pacific Veterinary Software Market Analysis

The Asia-Pacific veterinary software market is likely to grow with the rapid urbanization, rising disposable incomes, and a cultural shift towards viewing pets as family members. Countries such as China, India, Japan, and Australia are witnessing an unprecedented expansion in the number of veterinary clinics and hospitals to cater to a burgeoning middle class that prioritizes animal welfare. The region is seeing a surge in the adoption of mobile-first software solutions since smartphone penetration is significantly higher than desktop usage, allowing veterinarians to manage clinics remotely and engage clients via apps. As per the Japanese Veterinary Medical Association, the aging population in Japan has led to increased spending on pet healthcare, including advanced diagnostics and chronic disease management, which requires robust data tracking capabilities. Furthermore, the growth of the livestock sector in countries like China and India drives demand for specialized herd management software to ensure food safety and productivity. Government initiatives to digitize agricultural records and control zoonotic diseases further accelerate market penetration.

Latin America Veterinary Software Market Analysis

Latin America veterinary software market growth is likely to grow with the modernization of veterinary practices and the increasing professionalization of the animal health sector in key economies. According to the Pan American Health Organization, the awareness of zoonotic diseases and the importance of vaccination programs has led governments to encourage digital record-keeping for better disease surveillance and control. The growing influence of international veterinary chains entering the Latin American market brings with it standardized software protocols that raise the bar for local competitors. Additionally, the rising trend of pet humanization in urban centers like São Paulo and Buenos Aires drives demand for client engagement features such as appointment reminders and teleconsultations.

Middle East and Africa Veterinary Software Market Analysis

The Middle East and Africa veterinary software market growth is likely to grow with a dichotomy between advanced healthcare systems in the Gulf Cooperation Council nations and developing infrastructure in sub-Saharan Africa. The Gulf states, including the United Arab Emirates and Saudi Arabia, are aggressively investing in world-class veterinary hospitals and specialty centers to serve their affluent populations and expatriate communities, driving demand for premium practice management software. According to the Gulf Cooperation Council Health Ministers Council, regional spending on animal health is projected to grow significantly as part of broader food security and public health strategies. In contrast, sub-Saharan Africa faces challenges related to limited resources, yet there is a growing recognition of the role of veterinary services in livelihoods and disease prevention, leading to the gradual adoption of basic digital tools. As per the World Organisation for Animal Health, initiatives to strengthen veterinary systems in Africa include training programs that introduce digital record-keeping to improve disease reporting and trade compliance. The rise of pet ownership in urban centers across Egypt, South Africa, and Kenya is also creating a nascent market for companion animal software solutions. Furthermore, the expansion of commercial livestock farming in the region necessitates software for inventory management and production tracking to meet export standards.

COMPETITIVE LANDSCAPE

The competition in the veterinary software market is characterized by intense rivalry between established industry giants and agile specialized startups striving to capture market share through innovation and superior user experience. Leading companies differentiate themselves by offering fully integrated ecosystems that combine practice management with diagnostics, inventory control, and client communication tools into a single seamless platform. The market sees frequent consolidation as larger entities acquire niche developers to fill functional gaps and eliminate potential competitors while expanding their technological capabilities. Price competition remains moderate as buyers prioritize system reliability, data security, and customer support over initial cost savings, given the critical nature of clinical operations. Regulatory compliance acts as a significant barrier to entry, ensuring that only firms with robust quality assurance processes can compete effectively in regulated regions. The presence of high switching costs due to data migration complexities further consolidates the position of incumbent players against new entrants.

KEY MARKET PLAYERS

Some of the other promising companies leading the global veterinary software market profiled in this report are

- Britton's Wise Computer, Inc. (U.S.)

- Firmcloud Corporation (U.S.)

- Covetrus Inc

- IDEXX Laboratories Inc

- Timeless Veterinary Systems, Inc. (Canada)

- Henry Schein One

- ezyVET Limited (New Zealand)

- MedaNext Inc. (U.S.)

- Animal Intelligence Software, Inc. (U.S.)

TOP PLAYERS IN THE MARKET

- IDEXX Laboratories Inc stands as a global leader providing comprehensive practice management software and diagnostic solutions for veterinary professionals worldwide. The company integrates its sophisticated software platforms with advanced diagnostic hardware to create seamless workflows for clinics and hospitals. IDEXX recently strengthened its market position by expanding its cloud-based connectivity features, which allow real-time data synchronization between practice management systems and reference laboratories. Their strategic focus involves acquiring innovative tech startups to enhance artificial intelligence capabilities within their imaging and diagnostic tools. The firm continues to invest heavily in developing user-friendly mobile applications that enable veterinarians to access patient records and communicate with pet owners remotely. These initiatives demonstrate their commitment to digitizing veterinary care and maintaining a dominant presence through integrated ecosystem solutions.

- Covetrus Inc is a prominent technology company dedicated to transforming animal health through its unified cloud-based practice management platform and extensive marketplace of third-party applications. The company serves a diverse global customer base ranging from small companion animal clinics to large mixed animal practices with scalable digital solutions. Covetrus has recently bolstered its offerings by launching advanced telemedicine modules and client engagement tools that facilitate remote consultations and automated appointment reminders. They have also expanded their international footprint by localizing software interfaces to support multiple languages and regional regulatory requirements. Their dedication to interoperability is evident through partnerships with major diagnostic providers, ensuring seamless data flow across different systems.

- Henry Schein One plays a significant role in the veterinary software market by offering robust practice management solutions tailored specifically for animal health professionals under the Animal Health brand. The company leverages its vast distribution network to provide integrated software that connects clinical management with supply chain logistics and purchasing. Henry Schein One has recently focused on enhancing its cloud infrastructure to offer greater data security and reliability for veterinary businesses of all sizes. They have formed strategic alliances with insurance providers and financial institutions to embed payment processing and financing options directly into their software platforms. The firm is also investing in analytics tools that help practice owners optimize inventory levels and track key performance metrics effectively. These efforts highlight their determination to lead in operational efficiency and provide holistic business management solutions for the global veterinary community.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the veterinary software market primarily employ strategic acquisitions and mergers to rapidly expand their product portfolios and integrate complementary technologies such as telemedicine and artificial intelligence. Companies consistently invest in research and development to transition legacy on-premises systems to flexible cloud-based architectures that offer remote accessibility and scalability. Another prevalent strategy involves forming exclusive partnerships with diagnostic laboratories and medical device manufacturers to create interconnected ecosystems that streamline data exchange and workflow efficiency. Market participants also focus on geographic expansion by localizing software features to meet specific regional regulatory requirements and language preferences in emerging markets.

MARKET SEGMENTATION

This market research report on the global veterinary software market has been segmented and sub-segmented based on the type of software, delivery model, practice type, end-user, and region.

By Type of Software

- Practice Management Software

- Imaging Software

By Delivery Model

- On-Premises

- Cloud/Web-based

By Practice Type

- Small Animal

- Mixed

- Large Animal

- Equine

By End-User

- Hospitals

- Reference Laboratories

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What is the global veterinary software market?

The global veterinary software market refers to digital systems designed to help veterinary practices manage clinical, administrative, and financial tasks efficiently worldwide

2. What drives growth in the global veterinary software market?

Growth is driven by rising pet ownership, demand for efficient practice management, adoption of cloud-based platforms, telemedicine, and AI diagnostics enhancements in the global veterinary software market

3. Which regions dominate the global veterinary software market?

North America leads due to advanced infrastructure and pet ownership, followed by Europe and the rapidly growing Asia Pacific region impacting the global veterinary software market significantly

4. What are the main segments in the global veterinary software market?

Segments include small animal, mixed animals, and large animal practices, with small animal practices holding the largest share in the global veterinary software market

5. How does cloud-based software affect the global veterinary software market?

Cloud-based solutions increase accessibility, scalability, and integration, propelling adoption and innovation within the global veterinary software market

6. Why is telemedicine important for the global veterinary software market?

Telemedicine enhances remote care capabilities, improves client communication, and expands service reach, boosting the global veterinary software market growth

7. What role does AI play in the global veterinary software market?

AI supports diagnostics, workflow automation, and data analysis, driving technological advancement and efficiency in the global veterinary software market

8. Who are the primary end-users in the global veterinary software market?

Veterinary hospitals, clinics, and reference laboratories are key end-users relying on the global veterinary software market for practice management and diagnostic needs

9. How does the global veterinary software market support regulatory compliance?

Software solutions help clinics track animals, maintain electronic health records, and comply with regional regulations, ensuring standardization across the global veterinary software market

10. What are the challenges in the global veterinary software market?

Challenges include integration complexity, data security concerns, and varying regional adoption rates in the global veterinary software market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com