Europe Artificial Intelligence In Medical Imaging Market Size, Share, Trends & Growth Forecast Report Segmented By Technology (Deep Learning, Natural Language Processing (NLP), Others), Modality, End Use, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe), Industry Analysis From 2026 To 2034

Europe Artificial Intelligence in Medical Imaging Market Size

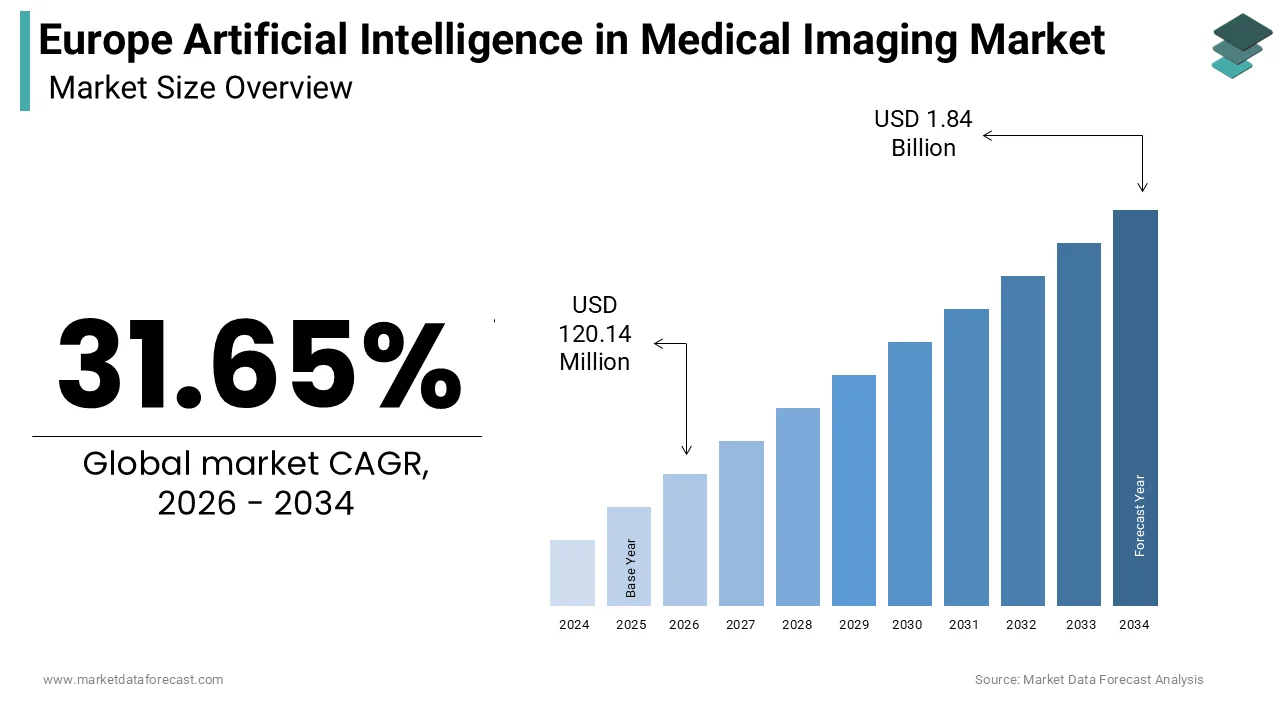

The Europe artificial intelligence in medical imaging market size was calculated to be USD 91.26 million in 2025 and is anticipated to be worth USD 1.84 billion by 2034, from USD 120.14 million in 2026, growing at a CAGR of 31.65% during the forecast period.

The artificial intelligence in medical imaging represents a transformative intersection of advanced computational algorithms and diagnostic radiology, designed to enhance the accuracy, speed, and efficiency of image interpretation. This sector integrates machine learning and deep learning models into modalities such as magnetic resonance imaging, computed tomography, and X-ray systems to assist radiologists in detecting anomalies with greater precision. The region is witnessing a paradigm shift towards value-based healthcare, where early and accurate diagnosis is paramount for improving patient outcomes and reducing long-term treatment costs. According to the World Health Organization, cancer remains a leading cause of death in Europe, accounting for approximately 1.3 million deaths in 2024. Furthermore, the European Commission has identified digital health as a priority area, aiming to create a European Health Data Space to facilitate secure data sharing and innovation. According to Eurostat, the proportion of the population aged 65 and over in the European Union reached 21.3% in 2023. The integration of artificial intelligence addresses the growing burden on healthcare systems by automating routine tasks and prioritizing urgent cases. Regulatory frameworks such as the Medical Device Regulation ensure that AI-driven solutions meet stringent safety and performance standards, fostering trust among healthcare providers. This technological evolution is reshaping clinical workflows, enabling personalized medicine and supporting the sustainability of European healthcare systems amidst demographic pressures.

MARKET DRIVERS

Escalating Radiologist Workforce Shortages Necessitate Automated Diagnostic Support

The persistent shortage of qualified radiologists across European healthcare systems is propelling the growth of the European artificial intelligence in medical imaging market. As per the European Society of Radiology, there is a significant disparity between the growing demand for imaging services and the available workforce, with many countries facing a deficit of specialized professionals. According to a 2023 survey by the German Radiological Society, the number of radiologists in Germany is not keeping pace with the demand for imaging services. This workforce gap leads to prolonged reporting times and potential diagnostic delays, adversely affecting patient care pathways. Artificial intelligence tools alleviate this burden by performing initial screenings and triaging urgent cases, thereby allowing radiologists to focus on complex diagnoses. According to a study published in The Lancet Digital Health, AI algorithms can reduce the time required for image interpretation by up to 30% and enhance overall departmental efficiency. The aging population further exacerbates this challenge because older individuals require more frequent diagnostic interventions for chronic conditions. As per the European Commission, the number of people aged 80 and above in the European Union is projected to reach approximately 13% by 2050. Consequently, healthcare providers are increasingly investing in AI-driven platforms to augment human capabilities, ensuring timely and accurate diagnoses despite staffing constraints. This strategic integration of technology not only mitigates workforce shortages but also improves job satisfaction among radiologists by reducing repetitive tasks and cognitive load.

Rising Prevalence of Chronic Diseases Drives Demand for Precision Diagnostics

The escalating prevalence of chronic diseases, particularly cancer and cardiovascular conditions, is further contributing to the European artificial intelligence in medical imaging market expansion. As per the World Health Organization, the European region recorded approximately 4 million new cancer cases in 2022. Traditional imaging methods often struggle with the subtle nuances of early-stage tumors, leading to missed diagnoses or false positives. Artificial intelligence algorithms trained on vast datasets excel in identifying minute abnormalities that may escape human observation, thereby enhancing diagnostic sensitivity and specificity. According to the European Heart Network, cardiovascular diseases account for approximately 42% of all deaths in Europe. AI-powered tools facilitate the quantitative analysis of cardiac images, providing detailed insights into heart function and structure that aid in personalized treatment planning. The European Society of Cardiology emphasizes the role of AI in improving risk stratification and monitoring disease progression, which is essential for managing chronic conditions effectively. Furthermore, the integration of AI in screening programs such as mammography for breast cancer has demonstrated improved detection rates and reduced recall rates, as noted by the European Breast Cancer Council. This technological advancement supports public health initiatives aimed at reducing mortality rates through early detection. Consequently, the rising incidence of chronic diseases creates a sustained demand for AI-enhanced imaging solutions, driving market growth and fostering innovation in diagnostic accuracy and patient care management.

MARKET RESTRAINTS

Stringent Data Privacy Regulations Impede Algorithm Training and Development

Rigorous data privacy regulations, particularly the General Data Protection Regulation, impose significant constraints on the growth of European AI in the medical imaging market. As per the European Data Protection Board, healthcare data is classified as sensitive personal data, which subjects it to strict processing conditions and consent requirements that complicate data-sharing initiatives. This regulatory landscape creates fragmentation across member states as varying interpretations of compliance standards hinder the creation of large-scale multinational databases essential for training high-performance AI models. According to a 2023 report by the European Union Agency for Cybersecurity, approximately 45% of healthcare organizations identified data privacy and complex regulations as a significant barrier to adopting new digital technologies. The requirement for explicit patient consent and anonymization processes adds layers of complexity and cost to data collection efforts, slowing down research and development cycles. Furthermore, the cross-border transfer of health data faces additional legal hurdles restricting collaboration between European institutions and global technology partners. The European Commission acknowledges these challenges and is working towards harmonizing data usage frameworks, yet implementation remains inconsistent. This regulatory uncertainty discourages investment in AI startups and limits the scalability of existing solutions. Consequently, developers must navigate a complex legal environment, often resulting in smaller, less representative training datasets that may compromise algorithm accuracy and generalizability. These constraints impede the rapid innovation and widespread adoption of AI in medical imaging, posing a substantial restraint to market growth.

High Implementation Costs and Infrastructure Limitations Restrict Adoption

Substantial financial investments are required for implementing artificial intelligence solutions, coupled with inadequate existing infrastructure in many healthcare facilities, which is further impeding the regional market expansion. As per the European Hospital and Healthcare Federation, many hospitals operate under tight budget constraints, prioritizing immediate clinical needs over long-term technological upgrades. The initial costs associated with acquiring AI software, integrating it with existing picture archiving and communication systems, and training staff are prohibitive for smaller institutions. According to a report by the European Commission, healthcare spending as a share of GDP in several European countries remained stable or declined slightly in real terms during 2023. Additionally, legacy IT systems in many hospitals lack the computational power and storage capacity necessary to support data-intensive AI applications, necessitating costly infrastructure overhauls. The European Investment Bank highlights that rural and peripheral regions face greater challenges in accessing high-speed internet and advanced computing resources, exacerbating disparities in healthcare technology adoption. Furthermore, the ongoing maintenance and updates of AI systems require continuous financial commitment, which strains limited operational budgets. The lack of standardized reimbursement models for AI-assisted diagnostics further discourages investment because healthcare providers are uncertain about return on investment and hesitate to adopt new technologies. These financial and infrastructural barriers create an uneven landscape where only well-funded urban centers can leverage AI benefits, leaving many facilities behind. Consequently, the high entry costs and infrastructure gaps significantly restrain market expansion and equitable access to advanced diagnostic tools.

MARKET OPPORTUNITIES

Integration with Telemedicine Platforms Expands Remote Diagnostic Capabilities

The seamless integration of artificial intelligence with telemedicine platforms is a lucrative opportunity for the Europe artificial intelligence in medical imaging market by enabling remote diagnostic services and expanding access to specialized care in underserved areas. As per the European Commission, the use of digital health services, including telemedicine, increased significantly across Europe during 2023. AI algorithms can analyze medical images transmitted from remote locations, providing real-time support to general practitioners and specialists who lack immediate access to radiologists. This synergy enhances diagnostic accuracy and reduces referral times, particularly in rural regions where specialist availability is limited. According to Eurostat, approximately 26% of the European population lived in rural areas in 2022. AI-driven tele radiology solutions bridge this gap by offering preliminary assessments and triage recommendations, facilitating timely interventions. The European Commission’s Digital Europe Programme supports initiatives that integrate AI into digital health services, fostering innovation and interoperability. Furthermore, the ability to share AI-analyzed images securely across borders promotes collaborative care and second opinions, enhancing patient outcomes. This integration also supports continuous monitoring of chronic conditions, allowing for proactive management and reduced hospital admissions. As healthcare systems increasingly prioritize decentralized care models, the combination of AI and telemedicine offers a scalable solution to improve efficiency and accessibility. Consequently, this technological convergence creates new revenue streams for AI vendors and strengthens the overall resilience of European healthcare systems.

Advancements in Personalized Medicine Fuel Demand for AI-Driven Insights

The growing emphasis on personalized medicine in Europe is further generating significant opportunities for the regional market as AI tools provide detailed quantitative insights that tailor treatment plans to individual patient characteristics. As per the European Alliance for Personalized Medicine, healthcare systems are shifting towards precision therapies that consider genetic, environmental, and lifestyle factors, requiring advanced diagnostic capabilities. AI algorithms can extract complex features from medical images, such as tumor texture and volume changes, which are crucial for predicting treatment response and prognosis. According to the European Society for Medical Oncology, personalized medicine strategies have significantly improved clinical outcomes for patients with specific cancer types in recent years. AI enables the integration of imaging data with genomic and clinical records, creating comprehensive patient profiles that guide therapeutic decisions. This holistic approach supports the development of targeted therapies and minimizes adverse effects, aligning with the goals of value-based healthcare. The European Medicines Agency encourages the use of real-world data, including imaging biomarkers, to support drug development and regulatory approvals. Furthermore, AI-driven analytics facilitate the identification of patient subgroups that benefit most from specific interventions, optimizing resource allocation and improving clinical trial outcomes. As healthcare providers increasingly adopt personalized care pathways, the demand for AI tools that deliver actionable insights from medical images continues to grow. This trend not only enhances patient care but also drives innovation in diagnostic technologies, positioning AI as a cornerstone of modern personalized medicine in Europe.

MARKET CHALLENGES

Interoperability Issues Hinder Seamless Integration with Existing Systems

Significant interoperability challenges between artificial intelligence solutions and existing hospital information systems pose a major challenge to the Europe artificial intelligence in medical imaging market, impeding efficient data exchange and workflow integration. As per the European Commission, many healthcare facilities utilize disparate software platforms that lack standardized communication protocols, making it difficult to integrate AI tools seamlessly. This fragmentation results in data silos where valuable imaging information remains isolated and inaccessible to AI algorithms that require comprehensive datasets for accurate analysis. According to a report by the European Coordination Committee of the Radiological, Electromedical and Healthcare IT Industry, less than 50% of healthcare organizations in Europe have fully implemented interoperable digital health systems. The lack of universal standards for data formats and interfaces forces vendors to develop custom integration solutions for each institution, increasing costs and deployment times. Furthermore, inconsistencies in image quality and labeling across different scanners and institutions complicate the training and validation of AI models, affecting their performance and reliability. The European Commission has initiated efforts to promote interoperability through the European Health Data Space, but widespread adoption remains slow. These technical barriers hinder the scalability of AI solutions and limit their clinical utility as radiologists struggle with disjointed workflows and manual data entry. Consequently, addressing interoperability issues is critical for unlocking the full potential of AI in medical imaging, requiring collaborative efforts from stakeholders to establish common standards and facilitate seamless system integration.

Limited Clinical Validation and Trust among Healthcare Professionals

The lack of extensive clinical validation and lingering skepticism among healthcare professionals regarding the reliability and safety of artificial intelligence algorithms present a significant challenge to the Europe artificial intelligence in medical imaging market. As per the European Society of Radiology, many radiologists remain cautious about relying on AI outputs due to concerns about algorithm transparency and potential errors. The black box nature of many deep learning models makes it difficult for clinicians to understand how decisions are made, undermining trust and acceptance. According to a survey by the Royal College of Radiologists, approximately 48% of radiologists in the UK reported that they were concerned about the clinical validation of AI tools. The absence of standardized clinical trials and long-term performance data further exacerbates these concerns as healthcare providers seek evidence of consistent accuracy and safety before adoption. The European Medicines Agency and other regulatory bodies are working to establish guidelines for clinical validation, but the process remains complex and time-consuming. Furthermore, the variability in AI performance across different patient populations and imaging equipment raises questions about generalizability and robustness. This uncertainty slows down adoption rates as hospitals prefer to wait for more conclusive evidence before investing in new technologies. Building trust requires transparent algorithm design, rigorous independent validation, and clear guidelines on clinical responsibility. Until these issues are addressed, the hesitation among healthcare professionals will continue to hinder the widespread integration of AI in medical imaging practices across Europe.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 31.65% |

| Segments Covered | By Technology, Modality, End Use, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Siemens Healthineers AG, GE HealthCare Technologies Inc., Koninklijke Philips N.V., Canon Medical Systems Corporation, IBM Corporation, NVIDIA Corporation, Fujifilm Holdings Corporation, Samsung Medison Co., Ltd., Agfa-Gevaert Group, Carestream Health Inc., Zebra Medical Vision Ltd., Aidoc Medical Ltd., Arterys Inc., Viz.ai Inc., Qure.ai Technologies Pvt. Ltd |

SEGMENTAL ANALYSIS

By Technology Insights

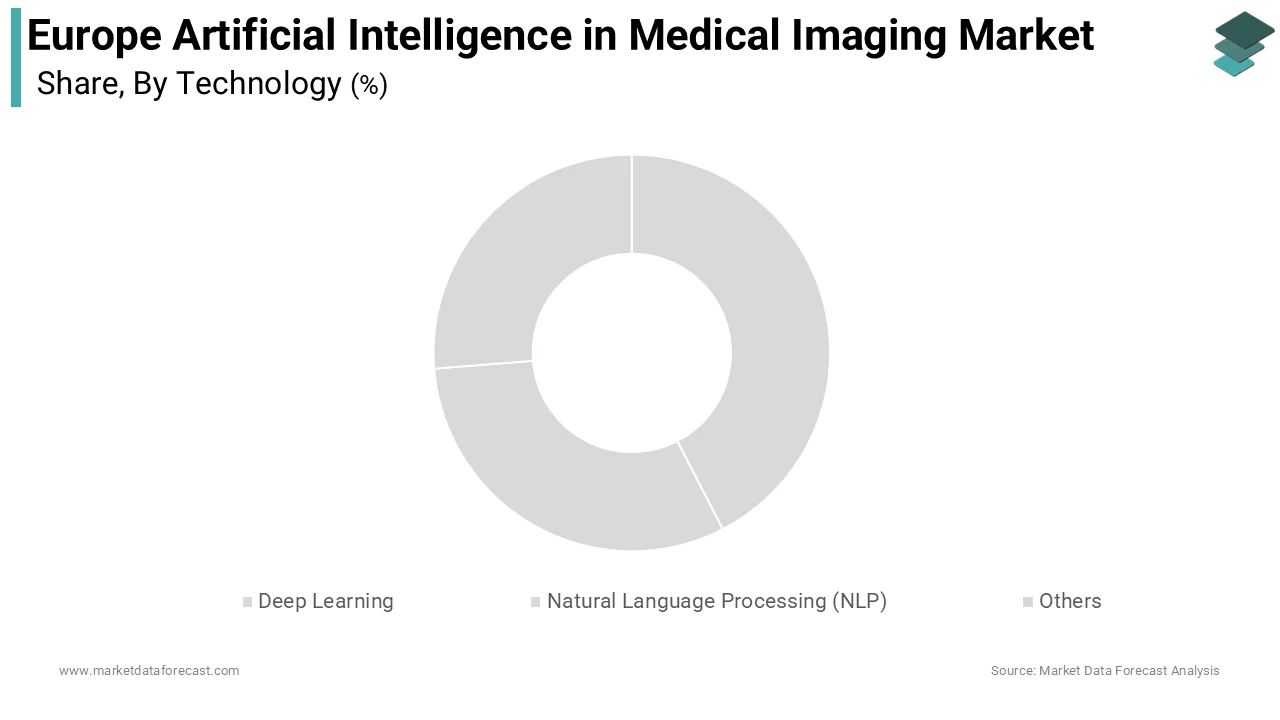

The deep learning segment led the market by capturing 61.6% of the European market share in 2025. The dominating position of the deep learning segment in the regional market is primarily attributed to the exceptional ability of deep learning algorithms, particularly convolutional neural networks, to process and analyze complex visual data with high accuracy. As per the European Society of Radiology, deep learning models have demonstrated diagnostic performance comparable to that of human radiologists in detecting conditions such as lung nodules and breast cancer. The technology’s capacity to learn from vast datasets without explicit programming allows it to identify subtle patterns and anomalies that may be overlooked by traditional methods. According to a study published in Scientific Reports, deep learning systems demonstrated high sensitivity and specificity in detecting various clinical conditions in medical imaging. The widespread availability of large-scale annotated imaging datasets in Europe further accelerates the development and refinement of these algorithms. Healthcare institutions are increasingly integrating deep learning solutions into their workflows to enhance diagnostic precision and reduce interpretation time. The European Commission’s support for AI research through initiatives like Horizon Europe provides substantial funding for advancing deep learning applications in healthcare. This technological superiority, combined with robust regulatory frameworks and increasing clinical validation, solidifies deep learning as the cornerstone of AI-driven medical imaging in Europe, driving its extensive adoption across various diagnostic modalities.

On the other hand, the NLP segment is estimated to record the fastest CAGR of 23.2% over the forecast period in this regional market, owing to the urgent need to extract valuable insights from unstructured clinical data. As per the European Federation for Medical Informatics, a large majority of healthcare data exists in unstructured formats, such as physician notes and radiology reports. NLP technologies enable the conversion of this text into structured data that can be analyzed alongside imaging results, providing a more comprehensive view of patient health. According to a report in the Journal of Biomedical Informatics, NLP algorithms can extract clinical information from medical texts with accuracy rates reaching over 90% for specific clinical entities. This capability is particularly valuable for retrospective studies and population health management, where large volumes of historical data need to be processed efficiently. The European Health Data Space initiative aims to leverage such technologies to improve data interoperability and reuse across member states. By linking textual information with imaging findings, NLP enhances the contextuality of diagnoses, leading to more personalized treatment plans. Healthcare providers are increasingly adopting NLP solutions to automate administrative tasks such as coding and billing, which reduces operational burdens and costs. The ability of NLP to interpret complex medical terminology and contextual nuances makes it an indispensable tool for modernizing healthcare information systems. Consequently, the growing recognition of unstructured data as a valuable asset drives the rapid expansion of the NLP segment in the European AI medical imaging market.

By Modality Insights

The CT scan segment commanded a major share of 36.1% of the regional market in 2025. The growth of the CT scan segment in the European market is attributed to extensive use of CT scans in oncology, trauma, and cardiovascular diagnostics, where rapid and accurate image interpretation is critical. As per the European Society of Oncologic Imaging, CT scans are the primary modality for staging and monitoring cancer in Europe. AI algorithms enhance the detection of small lesions and characterize tumor morphology, improving diagnostic confidence and treatment planning. According to the European Commission, approximately 22 million CT exams were performed in Germany alone during 2021. The ability of AI to reconstruct images from lower dose acquisitions also addresses radiation safety concerns, making CT scans safer for repeated use. The European Commission’s Beating Cancer Plan emphasizes the role of advanced imaging in early detection, driving investment in AI-enhanced CT technologies. Hospitals are increasingly adopting AI solutions to manage the high volume of CT data, reducing radiologists' workload and improving throughput. The standardization of CT protocols across institutions facilitates the development and validation of robust AI models, further accelerating adoption. This combination of high clinical utility, safety improvements, and operational efficiency solidifies the CT Scan segment’s leading position in the European market.

On the other hand, the MRI segment is expected to grow at the fastest CAGR of 22.9% over the forecast period in the European market due to the rising prevalence of neurological disorders and the superior soft tissue contrast provided by MRI. As per the European Brain Council, brain disorders affect approximately 179 million people in Europe. AI algorithms enhance the analysis of MRI data by automating the segmentation of brain structures and detecting abnormalities such as tumors, multiple sclerosis plaques, and Alzheimer ’s-related atrophy. According to a study in Scientific Reports, AI-assisted MRI analysis demonstrated significant accuracy in classifying neurological conditions. The complexity of MRI data requires sophisticated processing techniques where AI excels in reducing noise and accelerating image reconstruction. The European Society of Neuroradiology emphasizes the role of AI in standardizing interpretations and reducing interobserver variability. Furthermore, AI enables quantitative biomarker extraction, which is crucial for monitoring disease progression and treatment response in clinical trials. The increasing availability of high-field MRI scanners and advanced sequences further expands the potential for AI applications. Healthcare providers are investing in AI solutions to handle the growing volume of neurological MRI scans, improving diagnostic efficiency and patient care. This strong clinical demand, coupled with technological advancements, positions MRI as the fastest-growing segment in the European AI medical imaging market.

By End Use Insights

The hospitals segment dominated the market by holding the highest share of 59.4% of the regional market in 2025 due to the centralized nature of hospital care, where high patient volumes and diverse diagnostic needs create a strong demand for efficient imaging solutions. As per the European Hospital and Healthcare Federation, hospitals perform the majority of complex diagnostic procedures, requiring robust AI support to manage workflow and ensure accuracy. The integration of AI in hospital settings facilitates multidisciplinary collaboration, allowing radiologists, oncologists, and surgeons to access and analyze images seamlessly. According to a report by the European Commission, over 75% of hospitals in the EU have implemented at least one digital healthcare solution. The availability of substantial financial resources and IT infrastructure in large hospital networks supports the adoption of advanced AI technologies. Furthermore, hospitals serve as training grounds for medical professionals, fostering a culture of innovation and continuous learning. The European Commission’s initiatives to digitize healthcare systems prioritize hospital implementation,s providing funding and regulatory support. This conducive environment enables hospitals to lead the adoption of AI in medical imaging, setting standards for clinical practice and driving market growth. The critical role of hospitals in emergency and specialized care further reinforces their position as the primary users of AI-driven imaging solutions.

However, the diagnostic imaging centers segment is estimated to register a promising CAGR of 24.4% during the forecast period in the European market due to the shifting healthcare landscape towards outpatient care and specialized diagnostic services. As per the European Commission, the number of specialized diagnostic centers in many European countries has increased as part of efforts to improve healthcare access. These centers often specialize in specific modalities or body parts, allowing for focused expertise and efficient workflows. AI technologies enable these smaller entities to compete with larger hospitals by enhancing diagnostic accuracy and reducing reporting times. According to a 2023 report by the European Coordination Committee of the Radiological, Electromedical and Healthcare IT Industry, independent imaging providers are increasingly adopting AI to improve productivity. The lower overhead costs and flexible operational models of imaging centers facilitate quicker adoption of new technologies compared to large hospital bureaucracies. Furthermore, partnerships with teleradiology providers allow imaging centers to access remote expert opinions supported by AI, enhancing service quality. The European Commission’s support for private sector participation in healthcare delivery encourages the growth of these centers. As patients increasingly seek faster and more personalized diagnostic experiences, the demand for AI-enhanced services in diagnostic imaging centers continues to rise, driving the segment’s rapid expansion.

REGIONAL ANALYSIS

Germany AI in Medical Imaging Market Analysis

Germany occupied the major share of 23.6% of the European AI in the medical imaging market in 2025. The dominance of Germany in the European market is driven by its robust healthcare infrastructure, strong technological base, and significant investment in digital health initiatives. The country is home to leading medical device manufacturers and research institutions that pioneer AI developments in radiology. As per the German Federal Ministry of Health, the Digital Healthcare Act facilitates the reimbursement of digital health applications, encouraging the adoption of AI tools in clinical practice. The presence of major university hospitals and research clusters fosters innovation and clinical validation of AI algorithms. According to a survey by the German Radiological Society, approximately 52% of radiologists in Germany use AI tools in their daily practice as of 2023. The country’s strong data protection framework, aligned with GDPR, ensures secure handling of patient data, building trust among stakeholders. Furthermore, the government-funded projects promote the integration of AI into healthcare workflows. The aging population and high prevalence of chronic diseases in Germany create sustained demand for advanced diagnostic services. This combination of regulatory support, technological expertise, and clinical need positions Germany as the leading market for AI in medical imaging in Europe, driving continuous innovation and adoption.

United Kingdom AI in Medical Imaging Market Analysis

The United Kingdom held a significant position in the Europe artificial intelligence in medical imaging market in 2025 with 18.4% of the regional market share. The growth of the UK in the European market can be credited to its National Health Service’s commitment to digital transformation and AI adoption. The NHS Long Term Plan prioritizes the integration of AI to improve diagnostic accuracy and reduce waiting time,s creating a favorable environment for market growth. As per the UK Government, the NHS AI Lab has supported numerous projects to integrate AI into clinical settings. The UK is home to a vibrant AI startup ecosystem supported by government initiatives that fund the development and deployment of innovative solutions. According to a 2023 report by the Royal College of Radiologists, approximately 40% of NHS trusts are currently using AI for image analysis. The country’s strong regulatory framework, overseen by the Medicines and Healthcare products Regulatory Agency, ensures the safety and efficacy of AI medical devices. Furthermore, collaborations between academia, industry, and the NHS facilitate the translation of research into clinical practice. The high burden of cancer and cardiovascular diseases in the UK drives demand for advanced imaging technologies. This strategic alignment of policy innovation and clinical need sustains the UK’s prominent role in the European AI medical imaging landscape.

France AI in Medical Imaging Market Analysis

France is anticipated to hold a notable share of the Europe artificial intelligence in medical imaging market over the forecast period, owing to the strong government support for digital health and a thriving biomedical sector. The French government’s Health Innovation Strategy 2030 aims to position France as a leader in health technologies, including AI in medical imaging. As per the French Ministry of Economy, significant investments are being made in digital health as part of the France 2030 investment plan. The presence of major pharmaceutical and medical device companies in France fosters collaboration and innovation in AI-driven diagnostics. According to a 2024 report by the French Ministry of Health, the deployment of AI in healthcare is a strategic priority, with numerous pilot projects underway. The country’s robust data protection laws and ethical guidelines ensure responsible use of AI in healthcare. Furthermore, initiatives like the Health Data Hub facilitate secure data sharing for research and development purposes. The high quality of healthcare services and universal coverage create a stable demand for advanced diagnostic services. This supportive ecosystem of policy tourism and urban demand drives the growth of the automated retail market in France.

COMPETITION OVERVIEW

The competition in the Europe artificial intelligence in medical imaging market is characterized by intense rivalry among established medical device giants and innovative technology startups. Major players leverage their extensive distribution networks and brand recognition to dominate the landscape, while niche firms focus on specialized AI algorithms for specific clinical applications. The market exhibits high barriers to entry due to stringent regulatory requirements and the need for substantial clinical validation data. Companies differentiate themselves through technological superiority, ease of integration, and proven clinical outcomes. Strategic alliances between technology providers and healthcare institutions are common as they facilitate data access and algorithm refinement. The presence of robust intellectual property protections encourages continuous innovation but also leads to legal disputes over patent rights. Pricing pressure from public healthcare systems influences competitive dynamics, prompting firms to demonstrate clear value propositions through cost savings and efficiency gains. The rapid pace of technological advancement requires constant investment in research and development to stay ahead. Collaborative ecosystems involving academia, industry, and government bodies foster innovation and standardization. As demand for precision medicine grows, competition intensifies around personalized diagnostic solutions. Market participants must navigate complex reimbursement landscapes and varying national regulations across European countries. This dynamic environment drives consolidation as larger entities acquire smaller innovators to enhance their portfolios. Ultimately, the focus remains on improving patient outcomes through accurate and efficient diagnostic technologies.

KEY MARKET PLAYERS

A few major players of the Europe artificial intelligence in medical imaging market include

- Siemens Healthineers AG

- GE HealthCare Technologies Inc

- Koninklijke Philips N.V

- Canon Medical Systems Corporation

- IBM Corporation

- NVIDIA Corporation

- Fujifilm Holdings Corporation

- Samsung Medison Co. Ltd

- Agfa-Gevaert Group

- Carestream Health Inc

- Zebra Medical Vision Ltd

- Aidoc Medical Ltd

- Arterys Inc

- Viz.ai Inc

- Qure.ai Technologies Pvt. Ltd

Top Strategies Used by Key Market Participants

Key players in the Europe artificial intelligence in medical imaging market primarily focus on strategic collaborations and partnerships to expand their technological capabilities and market reach. Companies actively engage with academic institutions and healthcare providers to validate AI algorithms and ensure clinical relevance. Product innovation remains a central strategy with firms investing heavily in research and development to create advanced diagnostic tools. Integration of AI solutions with existing imaging hardware allows for seamless workflow adoption and enhanced user experience. Regulatory compliance is prioritized to navigate the complex European medical device regulations effectively. Market participants also pursue mergers and acquisitions to acquire specialized AI startups and broaden their product portfolios. Digital platform development enables remote monitoring and data sharing, which supports tele radiology services. Customer education and training programs are implemented to overcome resistance to change among healthcare professionals. Geographic expansion into emerging European markets helps companies tap into new revenue streams. Sustainability initiatives are increasingly incorporated to align with environmental goals and corporate social responsibility standards. These multifaceted strategies enable companies to maintain competitive advantages and drive long-term growth in the dynamic European healthcare landscape.

Leading Players in the Europe Artificial Intelligence in Medical Imaging Market

- Siemens Healthineers stands as a global leader in medical technology with a strong footprint in the European artificial intelligence in medical imaging sector. The company integrates its AI-powered solutions directly into imaging modalities such as MRI and CT scanners to enhance diagnostic precision and workflow efficiency. Its AI Rad Companion suite assists radiologists by automating routine tasks and providing quantitative insights for faster decision-making. Recently, the company expanded its digital ecosystem through strategic partnerships with healthcare providers across Germany and France to deploy advanced AI algorithms in clinical settings. Siemens Healthineers continues to invest heavily in research and development to refine its deep learning models for early disease detection. The organization also focuses on regulatory compliance within the European Union to ensure safe and effective deployment of its technologies. By combining hardware expertise with software innovation, the company strengthens its position as a key enabler of personalized medicine. These efforts support hospitals in managing increasing patient volumes while maintaining high standards of care. The continuous enhancement of its cloud-based platforms facilitates seamless data integration and collaboration among medical professionals throughout Europe.

- GE HealthCare Technologies maintains a prominent position in the Europe artificial intelligence in medical imaging market by offering comprehensive digital solutions that transform diagnostic imaging workflows. The company’s Edison platform integrates artificial intelligence and analytics into medical devices to improve operational efficiency and clinical outcomes. In Europe, GE HealthCare collaborates with leading hospitals to implement AI-driven tools for cardiac and neurological imaging applications. Recent initiatives include the launch of new AI-enabled ultrasound systems that provide real-time guidance to clinicians during procedures. The company actively engages in partnerships with academic institutions to validate its algorithms and accelerate regulatory approvals under European standards. GE HealthCare also emphasizes sustainability by developing energy-efficient imaging technologies supported by AI optimization. Its focus on interoperability ensures that AI solutions seamlessly connect with existing hospital information systems. By leveraging its extensive global network, the company brings innovative technologies to diverse healthcare settings across the continent. These strategic moves enhance its reputation as a trusted partner in digital health transformation. The commitment to advancing precision care through intelligent imaging solutions drives sustained growth and adoption in the European market.

- Canon Medical Systems Corporation is a significant contributor to the Europe artificial intelligence in medical imaging market, known for its innovative imaging technologies and patient-centric solutions. The company integrates AI into its CT and MRI systems to reduce radiation doses and improve image quality for better diagnostic confidence. In Europe, Canon Medical has strengthened its presence by collaborating with healthcare providers to deploy AI-assisted diagnostic tools in routine clinical practice. Recent actions include the introduction of advanced AI reconstruction techniques that significantly shorten scan times and enhance patient comfort. The company also invests in training programs for radiologists to facilitate the effective use of AI technologies. Canon Medical focuses on developing specialized applications for oncology and cardiovascular diseases, which are prevalent in the European population. Its commitment to regulatory adherence ensures that all AI solutions meet stringent safety requirements set by European authorities. By prioritizing user-friendly interfaces and seamless integration, the company enhances adoption rates among healthcare professionals. These efforts position Canon Medical as a key player in driving the digital transformation of medical imaging. The continuous innovation in AI capabilities supports the delivery of high-quality healthcare services across the region.

MARKET SEGMENTATION

This research report on the European artificial intelligence in medical imaging market has been segmented and sub-segmented based on technology, modality, end use & region.

By Technology

- Deep Learning

- Natural Language Processing (NLP)

- Others

By Modality

- CT Scan

- MRI

- Ultrasound

- X-rays

- Nuclear Imaging

By End Use

- Hospitals

- Diagnostic Imaging Centers

- Others

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What are the key factors driving the growth of AI in medical imaging in Europe?

Key drivers include the rising prevalence of chronic diseases, growing demand for early diagnosis, shortage of radiologists, and increasing adoption of automation in healthcare.

2. Which imaging modalities are most commonly integrated with AI technologies?

AI is widely used in modalities such as X-ray, CT scans, MRI, ultrasound, and mammography to enhance image analysis and interpretation.

3. How is AI improving diagnostic accuracy in medical imaging?

AI algorithms can detect subtle patterns and abnormalities in images, reducing human error and enabling earlier and more precise diagnosis.

4. What role does deep learning play in medical imaging applications?

Deep learning enables systems to learn from large datasets, improving image recognition, segmentation, and predictive analytics in medical imaging.

5. What are the major challenges faced by this market?

Challenges include data privacy concerns, high implementation costs, lack of standardization, and regulatory complexities.

6. How are regulatory policies impacting AI adoption in healthcare imaging?

Strict regulatory frameworks ensure patient safety and data protection but can slow down product approvals and market entry.

7. Who are the major players operating in the Europe AI in medical imaging market?

Major players include Siemens Healthineers, GE HealthCare, Philips, Canon Medical Systems, IBM, and several emerging AI startups.

8. What are the key applications of AI in radiology?

AI is used for image reconstruction, anomaly detection, workflow automation, clinical decision support, and disease classification.

9. What is the impact of AI on workflow efficiency in hospitals and diagnostic centers?

AI automates routine tasks, reduces reporting time, prioritizes urgent cases, and enhances overall operational efficiency.

10. What are the future trends shaping the Europe AI in medical imaging market?

Future trends include integration with cloud platforms, expansion of AI in personalized medicine, increased use of real-time analytics, and wider adoption across healthcare facilities.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com