Europe Aviation Fuel Market Size, Share, Trends, and Growth Analysis Report, Segmented by Fuel Type, Aircraft Type, Application, and Country – Industry Forecast From 2026 to 2034

Europe Aviation Fuel Market Report Summary

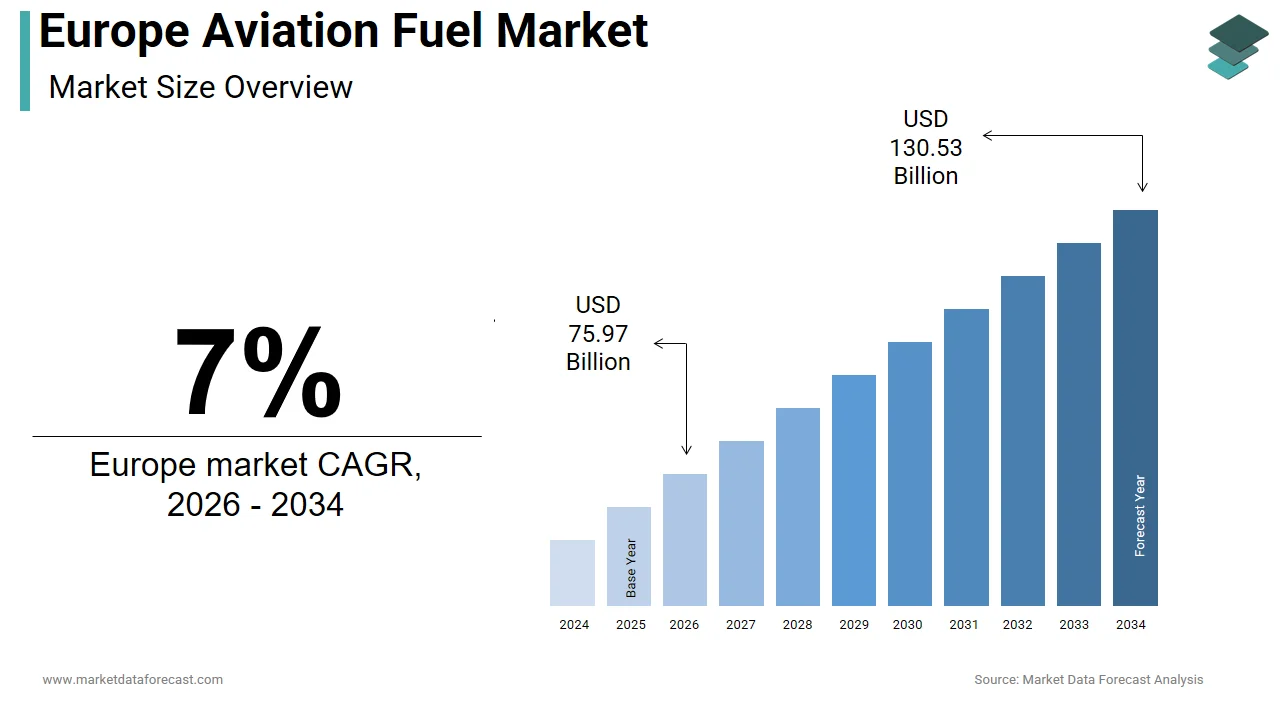

The Europe aviation fuel market was valued at USD 71.00 billion in 2025, is estimated to reach USD 75.97 billion in 2026, and is projected to reach USD 130.53 billion by 2034, growing at a CAGR of 7% from 2026 to 2034. Market growth is driven by the recovery of air travel post-pandemic, increasing passenger traffic, and expanding airline operations across Europe. Rising demand for sustainable aviation fuel (SAF) and stricter environmental regulations are also shaping market dynamics. Additionally, investments in airport infrastructure, fleet expansion, and growing tourism are contributing to increased fuel consumption across the region.

Key Market Trends

- Recovery and growth in air passenger traffic across Europe.

- Increasing adoption of sustainable aviation fuels (SAF).

- Rising focus on carbon emission reduction and environmental regulations.

- Expansion of low-cost carriers and regional airlines.

- Investments in airport infrastructure and fleet modernization.

Segmental Insights

- Based on fuel type, the conventional jet fuel segment dominated the Europe aviation fuel market in 2025, driven by its widespread use and established supply infrastructure.

- Based on aircraft type, the narrow-body aircraft segment led the market with 55.1% share in 2025, supported by the high frequency of short- and medium-haul flights.

- Based on application, the commercial airlines segment held the majority share in 2025 due to increasing passenger travel and airline operations.

Regional Insights

The Europe aviation fuel market is witnessing steady growth across major countries driven by tourism, connectivity, and airline expansion.

- The United Kingdom led the market in 2025 with 18.2% share, supported by high air traffic and major international airports.

- Germany followed with 15.8% share in 2025, driven by strong industrial travel demand and aviation infrastructure.

- France plays a key role in the market due to its strong tourism sector and strategic geographic position in Europe.

Competitive Landscape

The Europe aviation fuel market is highly competitive, with major oil and energy companies dominating supply and distribution. Market players are focusing on expanding sustainable fuel production, enhancing supply chain efficiency, and forming strategic partnerships with airlines and airports.

Prominent companies operating in the Europe aviation fuel market include BP plc, Royal Dutch Shell plc, TotalEnergies SE, Shell plc, Repsol SA, and Exxon Mobil Corp.

Europe Aviation Fuel Market Size

The Europe aviation fuel market was valued at USD 71 billion in 2025, is estimated to reach USD 75.97 billion in 2026, and is projected to reach USD 130.53 billion by 2034, growing at a CAGR of 7% from 2026 to 2034.

Aviation fuel is a specialized, highly refined petroleum-based or synthetic fuel engineered to power aircraft engines under extreme atmospheric conditions. It differs from automobile fuel by lacking ethanol and including additives to prevent freezing and explosion at high altitudes. This market is intrinsically linked to the operational viability of the airline industry, serving as a critical input for both domestic and international flights. The market is currently undergoing a significant transformation driven by regulatory mandates aimed at decarbonization and the gradual integration of sustainable aviation fuels. According to Eurostat, the total volume of air travel across the European Union has experienced a strong resurgence, with passenger counts nearing pre-pandemic levels as demand for international and domestic flights continues to rise. This resurgence directly correlates with increased consumption of conventional jet fuel despite efforts to improve fleet efficiency. The International Energy Agency notes that while aviation represents a specific portion of global energy-related carbon emissions, its faster-than-average growth rate compared to other transport sectors has led to increased regulatory focus on sustainable fuels and efficiency improvements. The European Union has implemented stringent policies such as the ReFuelEU Aviation initiative, which mandates minimum shares of sustainable aviation fuels at EU airports. These regulations are reshaping the supply chain dynamics and forcing stakeholders to adapt to new blending requirements. The infrastructure for fuel storage and distribution at major hubs like London Heathrow, Frankfurt, and Paris Charles de Gaulle remains highly developed, ensuring reliable access for carriers. However, the transition towards alternative energy sources introduces complexity in logistics and pricing structures. The interplay between traditional fossil-based jet fuel and emerging bio-based alternatives defines the current landscape of the Europe aviation fuel market.

MARKET DRIVERS

Resurgence in International and Domestic Air Travel Demand

The robust recovery in passenger and cargo air travel is a key force behind the growth of the European aviation fuel market. As a result, airlines are increasing flight frequencies to meet this pent-up demand. Following the stabilization of global health concerns, travelers have returned to both leisure and business trips, leading to a substantial rise in seat capacity and load factors. The International Air Transport Association shows that European passenger demand experienced double-digit growth in recent years, significantly outpacing previous annual increases and highlighting a powerful recovery in the region's travel market. This increase in flight operations directly translates to higher consumption of jet fuel as aircraft require significant energy resources for takeoff, cruising, and landing phases. As per Eurostat, the number of passengers carried by air transport in the European Union approached pre-pandemic levels, demonstrating the resilience of the aviation sector. The expansion of route networks by low-cost carriers and legacy airlines further amplifies fuel demand. Additionally, the growth in e-commerce has boosted air cargo volumes, requiring dedicated freighter flights that rely heavily on aviation fuel. The seasonal nature of travel in Europe, particularly during the summer months, creates peaks in fuel consumption that suppliers must manage efficiently. Airlines are optimizing their fleets, but the sheer volume of flights necessitates a steady and reliable supply of fuel. This sustained operational activity ensures that, despite efficiency gains, the absolute volume of aviation fuel consumed remains high, driving market activity and revenue for suppliers across the continent.

Implementation of Mandatory Sustainable Aviation Fuel Blending Targets

European regulators have introduced mandatory sustainable aviation fuel blending targets, which are also propelling the expansion of the European aviation fuel market. These mandates are driving significant market evolution and investment in alternative fuel sources. The ReFuelEU Aviation initiative establishes a clear framework requiring fuel suppliers to blend increasing percentages of sustainable aviation fuel with conventional jet fuel at EU airports. Under the European Commission ReFuelEU Aviation framework, fuel suppliers are legally required to gradually increase the proportion of sustainable alternatives in their fuel mix, with targets set to accelerate significantly over the coming decades. This regulatory push compels fuel suppliers and airlines to secure long term contracts for sustainable aviation fuel, thereby stimulating production and infrastructure development. As per the European Environment Agency, the aviation sector is under pressure to reduce its carbon footprint, and sustainable aviation fuel offers a viable pathway to achieve immediate emission reductions without requiring new aircraft technologies. The certainty provided by these mandates encourages investment in production facilities using feedstocks such as used cooking oil, agricultural residues, and synthetic fuels. Fuel suppliers are adapting their logistics and storage systems to handle blended fuels, ensuring compliance with strict quality standards. This regulatory environment creates a guaranteed market for sustainable aviation fuel producers, fostering innovation and competition. The shift towards mandated blending not only drives the adoption of cleaner fuels but also reshapes the competitive landscape of the Europe aviation fuel market by prioritizing suppliers who can meet sustainability criteria.

MARKET RESTRAINTS

Volatility in Crude Oil Prices and Supply Chain Instability

Fluctuations in global crude oil prices are a serious obstacle for the European aviation fuel market. This is because jet fuel prices are closely correlated with crude oil benchmarks. Geopolitical tensions, conflicts, and production decisions by major oil-exporting nations can cause sudden and sharp increases in fuel costs, impacting airline profitability and operational planning. The International Energy Agency shows that benchmark crude prices have faced extreme fluctuations, at times exceeding triple digits per barrel due to major global conflicts and sudden shifts in export availability. As jet fuel is a refined product of crude oil, any instability in the upstream market directly affects the cost structure for airlines and fuel suppliers. High fuel prices force airlines to implement fuel surcharges, which can dampen demand for air travel, particularly among price-sensitive leisure travelers. Financial analysis from the International Air Transport Association indicates that fuel now constitutes the single largest operating expense for the global aviation industry, with its share of total spending rising significantly compared to pre-pandemic levels. This financial pressure limits the ability of airlines to invest in fleet modernization or expand routes. Furthermore, supply chain disruptions caused by logistical bottlenecks or refinery maintenance can lead to localized shortages affecting airport operations. The unpredictability of fuel costs complicates budgeting and strategic decision-making for industry stakeholders. This economic uncertainty acts as a brake on market growth as airlines seek to mitigate exposure through hedging strategies, which may not always be effective in extreme market conditions.

High Production Costs and Limited Availability of Sustainable Aviation Fuels

The high production costs and limited availability of sustainable aviation fuels pose a significant impediment to the broader adoption and market expansion of eco-friendly options in the European aviation fuel market. Currently, sustainable aviation fuel is produced at a much smaller scale than conventional jet fuel, resulting in premiums that can be two to five times higher than fossil-based alternatives. According to IATA's sustainability trackers, while the output of renewable jet fuel has doubled recently, it still represents a tiny fraction of the total fuel consumed by commercial airlines worldwide. In Europe, the lack of sufficient feedstock, such as waste oils and agricultural residues, limits the ability of producers to scale up operations efficiently. The European Commission notes that while the new ReFuelEU Aviation mandates have successfully triggered an expansion of regional manufacturing, the market remains highly concentrated within a small number of member states. This dependency on imports exposes the market to supply chain risks and currency fluctuations. The high cost of sustainable aviation fuel is often passed on to airlines and ultimately passengers, potentially reducing the competitiveness of European carriers against those in regions with less stringent regulations. Furthermore, the technical challenges associated with producing drop-in fuels that meet strict aviation safety standards require substantial research and development investments. These economic and logistical barriers slow down the transition process and constrain the overall growth potential of the sustainable segment within the Europe aviation fuel market.

MARKET OPPORTUNITIES

Expansion of Hydrogen and Electric Propulsion Research Initiatives

The growing investment in hydrogen and electric propulsion technologies is creating new opportunities for the expansion of the European aviation fuel market. This shift allows the industry to diversify and innovate beyond traditional liquid fuels. European governments and aerospace manufacturers are actively collaborating on research projects aimed at developing zero-emission aircraft that could eventually replace conventional jet engines. According to the European Union Aviation Safety Agency, several pilot projects and demonstration flights using hydrogen fuel cells and battery electric systems have been successfully conducted in recent years. These initiatives are supported by substantial funding from the Clean Sky Joint Undertaking, which aims to accelerate the development of green aviation technologies. The European Commission has established specialized alliances to accelerate the entry into service of hydrogen-powered aircraft, focusing primarily on the specific engineering requirements of short-range and regional flight paths. This shift creates opportunities for fuel suppliers to expand into hydrogen production, storage, and distribution infrastructure at airports. Companies that adapt early to these new energy vectors can position themselves as leaders in the future low-carbon aviation ecosystem. The development of hydrogen refueling stations and electric charging infrastructure requires new partnerships and business models offering fresh revenue streams. Widespread adoption of alternative propulsion fuels may take decades. However, being an early mover to establish supply chains provides a strategic opportunity. This technological evolution encourages collaboration between energy providers, aircraft manufacturers, and regulators, fostering a dynamic environment for innovation in the Europe aviation fuel market.

Development of Advanced Biofuel Production Facilities

The establishment of advanced biofuel production facilities utilizing non-food biomass and synthetic pathways offers an attractive prospect for growth in the Europe aviation fuel market. Technological advancements in gasification and Fischer-Tropsch synthesis allow for the conversion of municipal solid waste, forestry residues, and agricultural waste into high-quality, sustainable aviation fuel. According to the European Bioplastics Association, the capacity for advanced biofuel production in Europe is expanding as investors recognize the long-term potential of the sector. The European Waste-based & Advanced Biofuels Association shows a significant increase in capital investment for biorefineries, driven by legislative mandates that prioritize the scaling of non-food-based renewable energy sources. The European Union’s support through subsidies and grants encourages the construction of large-scale biorefineries capable of meeting the rising demand for sustainable aviation fuel. Companies that invest in these facilities can secure long-term supply contracts with airlines committed to decarbonization goals. Furthermore, the integration ofpower-to-liquidd technologies, which use renewable electricity to produce synthetic fuels, provides a pathway to fully carbon-neutral aviation fuel. This diversification of feedstock sources reduces reliance on limited waste oil supplies and enhances energy security. The development of a robust domestic production base for advanced biofuels strengthens the resilience of the Europe aviation fuel market and aligns with broader circular economy objectives, creating substantial growth opportunities for innovative players.

MARKET CHALLENGES

Infrastructure Constraints for Sustainable Aviation Fuel Distribution

The lack of adequate infrastructure for the storage, handling, and distribution of sustainable aviation fuels poses a major challenge to the Europe aviation fuel market. Most existing airport fuel farms and pipeline systems were designed for conventional jet fuel and may require significant modifications to handle blends with higher concentrations of sustainable aviation fuel or pure sustainable aviation fuel. According to the International Air Transport Association, the logistical complexity of introducing new fuel types requires rigorous testing and certification to ensure safety and compatibility with existing aircraft and ground equipment. The European Union Aviation Safety Agency explains that while renewable fuels utilize existing airport fuel hydrants, smaller regional hubs face higher delivery costs due to their distance from the primary refineries and blending facilities where these fuels are produced. The segregation of sustainable aviation fuel from conventional fuel during transport and storage is essential to maintain integrity and traceability, which adds operational complexity and cost. Furthermore, the limited number of production sites means that sustainable aviation fuel often needs to be transported over long distances, increasing the risk of supply disruptions. Upgrading infrastructure requires substantial capital investment and coordination among multiple stakeholders, including airports, fuel suppliers, and regulators. Without timely improvements in infrastructure, the ability to meet blending mandates and scale up sustainable aviation fuel usage will be hindered. This infrastructural gap represents a critical barrier that must be addressed to facilitate the smooth transition towards a more sustainable aviation fuel ecosystem in Europe.

Regulatory Fragmentation and Compliance Complexity

The fragmentation of regulatory frameworks across different regional countries creates significant compliance issues for participants in the Europe aviation fuel market. While the European Union sets overarching targets through initiatives like ReFuelEU, individual member states may implement additional national laws, taxes, or incentives that vary widely. The European Commission has implemented standardized regulations across member states to ensure that all fuel suppliers and airlines follow the same sustainability reporting and compliance rules, thereby preventing competitive disadvantages within the internal market. As per the International Air Transport Association, airlines operating across multiple jurisdictions must navigate a complex web of regulations that increase administrative burdens and operational costs. The uncertainty regarding future regulatory changes makes long-term planning difficult for investors and fuel producers. For instance, differences in the definition of eligible feedstocks or sustainability criteria can complicate the sourcing and certification of sustainable aviation fuel. This regulatory ambiguity can delay investment decisions and hinder the development of a unified European market for aviation fuels. Furthermore, the need for continuous monitoring and reporting to demonstrate compliance with evolving standards requires sophisticated data management systems. The complexity of navigating these diverse regulatory landscapes acts as a drag on market efficiency and slows down the adoption of innovative fuel solutions. Harmonizing regulations across the continent remains a critical challenge that needs to be addressed to unlock the full potential of the Europe aviation fuel market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Fuel Type, Aircraft Type, Application, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | BP plc, Royal Dutch Shell plc, TotalEnergies SE, Shell plc, Repsol SA, Exxon Mobil Corp., and Others. |

SEGMENTAL ANALYSIS

By Fuel Type Insights

The conventional jet fuel segment maintained dominance in the Europe aviation fuel market by accounting for a substantial share in 2025. This dominance of the segment is supported by the established infrastructure and the sheer volume of commercial air traffic that relies on kerosene-based fuels for daily operations. One of the major factors fueling this leadership is the extensive network of short-haul and medium-haul flights operated by narrow-body aircraft, which constitute the backbone of European aviation. Eurostat shows that air passenger traffic in the European Union has now fully recovered, with recent annual totals exceeding pre-pandemic records and signaling a total resurgence in travel demand. This high frequency of departures and arrivals necessitates a continuous and massive supply of conventional jet fuel to keep fleets airborne. As per the International Air Transport Association, jet fuel remains the most cost-effective and energy-dense option available for current aircraft technologies, ensuring its continued preference over emerging alternatives. The existing refining capacity across Europe is optimized for producing Jet A1 fuel, allowing for efficient distribution to major hubs such as London Heathrow and Frankfurt Airport. Furthermore, the lack of scalable alternatives means that airlines have no immediate choice but to rely on fossil-based fuels for the majority of their operations. The integration of sustainable aviation fuel is still in its infancy and constitutes a negligible fraction of total volume. Consequently, the operational reality of modern aviation ensures that conventional jet fuel remains the undisputed leader in the market.

The sustainable aviation fuel segment is estimated to register the fastest CAGR of 45.2% from 2026 to 2034 due to stringent regulatory mandates and corporate decarbonization commitments. This rapid growth is also attributed to the European Union’s ReFuelEU Aviation initiative, which legally requires fuel suppliers to blend increasing shares of sustainable aviation fuel with conventional jet fuel. According to the European Commission, the mandate begins with a 2 percent blending requirement in 2025 and escalates significantly in subsequent years, creating a guaranteed and expanding market for SAF. As per the International Air Transport Association, airlines are actively signing long-term off-take agreements with producers to secure supply and meet their own net-zero targets. The development of new production facilities using feedstocks such as used cooking oil and agricultural residues is accelerating across the continent. Governments are providing subsidies and incentives to lower the production cost gap between SAF and conventional fuel, making it more economically viable for airlines. The growing consumer awareness regarding environmental impact also pressures airlines to adopt greener fuel options to maintain brand reputation. Technological advancements in power-to-liquid processes are further expanding the potential supply base. Although the current volume is low, the regulatory push ensures that SAF will experience exponential growth rates compared to other fuel types. This segment represents the future trajectory of the Europe aviation fuel market as the industry transitions towards sustainability.

By Aircraft Type Insights

The narrow-body segment led the Europe aviation fuel market by holding a 55.1% share in 2025 because of the high frequency of short-haul and domestic flights that connect major European cities and serve as feeders for long-haul international routes. A key aspect propelling this leadership is the operational model of low-cost carriers and legacy airlines, which rely heavily on fuel-efficient narrow-body aircraft such as the Airbus A320 family and Boeing 737 series. Data from Airlines for Europe (A4E) and Eurocontrol confirm that low-fare airlines now provide nearly half of all scheduled seats in the European market, making them a primary driver of regional jet fuel consumption. These aircraft operate multiple flights per day, resulting in high cumulative fuel consumption despite lower per-flight usage compared to wide-body jets. Eurostat indicates that flights between member states represent the single largest segment of European air travel, necessitating extensive refueling infrastructure across both hub and regional airports. The dense population and economic integration of the European Union facilitate robust business and leisure travel on these routes. The reliability and versatility of narrow-body aircraft make them the preferred choice for airlines operating in a competitive market. Consequently, the sheer number of flights operated by this aircraft type ensures that it remains the largest consumer of aviation fuel in the region.

The Cargo and Freighters segment is anticipated to witness the fastest CAGR of 6.8% during the forecast period, owing to the sustained expansion of e-commerce and global supply chain dynamics. This swift expansion growth is further propelled by the increasing demand for fast and reliable delivery of goods, which relies heavily on air freight capabilities. The International Air Transport Association notes that following a period of post-pandemic adjustment, European air freight volumes have entered a new phase of expansion driven by the specific logistics requirements of e-commerce and global supply chains. The shift towards online shopping has created a structural increase in the volume of parcels transported by air, requiring dedicated freighter aircraft that consume significant amounts of jet fuel. As per Eurostat, the value of goods transported by air in the European Union continues to rise, reflecting the importance of air cargo in high value trade. The expansion of logistics hubs and the introduction of new freighter routes further amplify fuel consumption. Additionally, the need for just in time delivery in industries such as pharmaceuticals and electronics supports the growth of this segment. Unlike passenger traffic, which can be seasonal, cargo demand remains relatively stable throughout the year. The modernization of freighter fleets with larger and more efficient aircraft also contributes to increased fuel uptake. This segment’s growth is underpinned by fundamental changes in consumer behavior and global trade patterns.

By Application Insights

The commercial airlines segment was the largest in the Europe aviation fuel market and occupied a substantial share in 2025. This supremacy of the segment is attributed to the vast scale of passenger and cargo operations conducted by scheduled airlines across the continent. A key reason behind this leadership is the recovery of international and domestic travel following global disruptions, which has led to a surge in flight frequencies and seat capacity. Commercial airlines operate large fleets of aircraft that require regular refueling to maintain their schedules and connectivity. The competitive nature of the airline industry encourages carriers to maximize aircraft utilization, leading to higher fuel usage. Legacy carriers and low-cost airlines alike contribute to this demand as they expand their route networks and offer affordable travel options. The reliance on fossil-based jet fuel for the majority of these operations ensures that commercial airlines remain the largest application segment. The economic importance of tourism and business travel further sustains this dominance.

The General and Business Aviation segment is likely to experience the fastest CAGR of 5.5% between 2026 and 2034. This growth of the segment is driven by the increasing preference for private travel among high-net-worth individuals and corporations. It is also supported by the desire for flexibility, privacy, and time efficiency, which private jets offer compared to commercial flights. The recovery of the global economy has boosted corporate profits, enabling greater spending on executive travel. General aviation also includes recreational flying and training, which contributes to fuel demand, although to a lesser extent than business jets. The ability of private aircraft to access smaller airports with less congestion appeals to busy executives and celebrities. Furthermore, the introduction of newer and more efficient business jets encourages owners to fly more frequently. While the absolute volume of fuel consumed is lower than that of commercial airlines, the growth rate is higher due to the niche nature and expanding user base of this segment. The segment benefits from less regulatory pressure on slot allocations, allowing for increased operational freedom.

COUNTRY LEVEL ANALYSIS

United Kingdom Aviation Fuel Market Analysis

The United Kingdom outperformed other countries in the Europe aviation fuel market and accounted for a 18.2% share in 2025. This prominence of the UK market is fuelled by its status as a global aviation hub. The country’s market status is characterized by high traffic volumes at major airports such as London Heathrow, Gatwick, and Manchester. A key driving factor is the strong demand for international long-haul flights, which connect the UK to destinations worldwide. The presence of major airlines such as British Airways and easyJet ensures consistent demand for jet fuel. The UK government’s commitment to net zero emissions is influencing the adoption of sustainable aviation fuel, although conventional fuel remains dominant. The strategic location of the UK makes it a key transit point for transatlantic and European flights. Infrastructure investments at airports are enhancing capacity to handle growing passenger numbers. The regulatory framework is aligning with international standards to promote sustainability while maintaining competitiveness. The UK’s robust aviation ecosystem ensures its leading position in the European aviation fuel market.

Germany Aviation Fuel Market Analysis

Germany was the second largest country in the Europe aviation fuel market and captured a 15.8% share in 2025. This position of the German market is propelled by its central location and strong industrial base. The market status is defined by significant traffic at hubs such as Frankfurt, Munich, and Berlin, which serve as key connectors for European and global routes. A primary driving factor is the high volume of business travel associated with Germany’s powerful economy and export-oriented industries. Frankfurt Airport remains one of the busiest cargo hubs in Europe, driving substantial fuel demand from freighter operations. The presence of the Lufthansa Group as a major carrier ensures steady consumption of aviation fuel. Government policies are encouraging the development of green hydrogen and synthetic fuels for aviation. The country’s extensive rail network complements air travel but does not replace the need for long-distance flights. Germany’s commitment to environmental standards is shaping the future of its aviation fuel market. The combination of passenger and cargo traffic sustains its prominent position.

France Aviation Fuel Market Analysis

France plays a major role in the Europe aviation fuel market due to its tourism industry and strategic geographic location. The market status is characterized by high traffic at Paris Charles de Gaulle and Orly airports, which serve as major gateways to Europe and beyond. A key growth enabler is the popularity of France as a top tourist destination, attracting millions of visitors annually. The presence of Air France KLM as a major airline group drives significant demand for jet fuel. The country’s overseas territories also contribute to domestic flight volumes. France is investing in research and development for biofuels and hydrogen technologies to reduce aviation emissions. The regulatory environment is supportive of green initiatives while maintaining the competitiveness of the aviation sector. The diversity of flight types, including short-haul European routes and long-haul intercontinental flights,s ensures balanced fuel demand. France’s focus on sustainability positions it as a leader in the transition to cleaner aviation fuels.

Spain Aviation Fuel Market Analysis

Spain grew steadily in the Europe aviation fuel market owing to its robust tourism sector. The market status is defined by high seasonal traffic at airports in Madrid, Barcelona, and coastal regions such as Malaga and Palma. A key force behind this growth is the influx of international tourists who rely on air travel to reach Spanish destinations. The presence of Iberia and Vueling as major carriers ensures consistent fuel consumption. Spain is also developing its capacity for sustainable aviation fuel production, leveraging its agricultural resources. The government is implementing measures to reduce emissions and promote green aviation. The geographic position of Spain makes it a key entry point for travelers from the Americas and Northern Europe. The seasonal nature of tourism creates peaks in fuel demand that suppliers must manage. Spain’s focus on sustainable tourism aligns with broader environmental goals in the aviation sector.

Netherlands Aviation Fuel Market Analysis

The Netherlands is likely to expand notably in the European market from 2026 to 2034 due to the strategic importance of Amsterdam Schiphol Airport. The market status is characterized by Schiphol’s role as a major European hub for both passenger and cargo traffic. A key driving factor is the airport’s connectivity, which facilitates a high volume of transfer passengers and freight. The presence of KLM as a major carrier drives significant fuel demand. The Netherlands is a leader in logistics and trade, making air cargo a vital component of its economy. The country is investing in innovative solutions such as synthetic fuels and hydrogen to decarbonize aviation. Regulatory measures are balancing growth with environmental protection. The efficient infrastructure at Schiphol supports high operational throughput. The Netherlands’ proactive approach to sustainability influences the broader European aviation fuel market.

COMPETITIVE LANDSCAPE

The competition in the Europe aviation fuel market is characterized by the presence of major integrated energy companies and specialized fuel suppliers. Market leaders compete based on supply reliability, product quality, and sustainability credentials. The transition towards sustainable aviation fuel creates new competitive dynamics as companies race to establish production capabilities and secure feedstock sources. Regulatory mandates such as ReFuelEU Aviation drive differentiation through compliance and green innovation. Price competitiveness remains important but is increasingly balanced with environmental performance metrics. Strategic alliances with airlines and airports strengthen market positions and ensure stable demand. The high barriers to entry due to infrastructure requirements and regulatory complexity limit new entrants. Established players leverage their existing networks and financial resources to maintain dominance. Innovation in biofuel technologies and synthetic fuels offers opportunities for differentiation. Companies that adapt quickly to sustainability trends gain a competitive advantage. The market sees continuous investment in low-carbon solutions and infrastructure upgrades. Overall, the competitive environment encourages collaboration and innovation, driving the evolution of the aviation fuel industry in Europe towards a more sustainable future.

KEY MARKET PLAYERS

The leading companies operating in the Europe aviation fuel market include:

- BP plc

- Royal Dutch Shell plc

- TotalEnergies SE

- Shell plc

- Repsol SA

- Exxon Mobil Corp.

TOP PLAYERS IN THE MARKET

- TotalEnergies is a major integrated energy company with a significant presence in the Europe aviation fuel market through its extensive refining and distribution network. The company supplies conventional jet fuel and sustainable aviation fuel to major airports across the continent. TotalEnergies is actively expanding its production capacity for sustainable aviation fuel by converting existing refineries and investing in new biofuel facilities. Recent actions include partnerships with airlines to secure long-term supply agreements for low-carbon fuels. The company leverages its global expertise to source diverse feedstocks such as used cooking oil and agricultural residues. TotalEnergies focuses on reducing the carbon footprint of its operations through innovation and technology. Their commitment to sustainability aligns with European regulatory requirements and customer expectations. By integrating sustainable solutions into its portfolio, TotalEnergies strengthens its market position. The company’s robust logistics infrastructure ensures reliable delivery to key aviation hubs. This strategic approach enhances their competitiveness in the evolving energy landscape.

- Shell plc is a leading global energy company that plays a crucial role in the Europe aviation fuel market by providing high-quality jet fuels and sustainable alternatives. The company operates a vast network of supply terminals and blending facilities at major European airports. Shell is investing heavily in the production of sustainable aviation fuel through advanced biofuel technologies and power-to-liquid processes. Recent initiatives include collaborations with waste management companies to secure consistent feedstock supplies. The company aims to become a net-zero emissions energy business by 2050, driving its focus on low-carbon solutions. Shell engages with airlines and airport authorities to develop efficient fueling infrastructure. Their expertise in trading and logistics enables them to manage supply chain complexities effectively. Shell’s commitment to innovation and sustainability strengthens its reputation among industry stakeholders. By offering tailored fuel solutions, NS Shell meets the diverse needs of commercial and cargo airlines. This customer-centric approach supports their continued growth in the European market.

- BP p.l.c. is a prominent international energy company with a strong footprint in the Europe aviation fuel market through its refining and marketing operations. The company supplies conventional jet fuel and is increasingly focusing on sustainable aviation fuel production. BP is transforming its business model to support the energy transition by investing in bioenergy and hydrogen technologies. Recent actions include the development of sustainable aviation fuel plants in Europe using waste-based feedstocks. The company partners with airlines to help them achieve their decarbonization goals through reliable fuel supplies. BP leverages its global trading capabilities to optimize fuel distribution and manage price volatility. Their strategic investments in low-carbon technologies position them as leaders in the green aviation sector. BP’s commitment to safety and operational excellence ensures consistent service quality. By adapting to changing market dynamics, BP maintains its competitive edge. The company’s proactive approach to sustainability drives innovation and long-term value creation in the European aviation fuel sector.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe aviation fuel market primarily focus on diversifying their product portfolios to include sustainable aviation fuels alongside conventional jet fuel. Companies invest heavily in research and development to improve production efficiency and reduce the costs of bio-based alternatives. Strategic partnerships with airlines and waste suppliers secure long-term feedstock availability and off-take agreements. Expansion of storage and distribution infrastructure at major airports ensures reliable supply chains. Compliance with environmental regulations drives the adoption of cleaner technologies and carbon reduction initiatives. Digitalization of logistics enhances operational transparency and efficiency. Marketing efforts emphasize sustainability credentials to attract eco-conscious customers. These strategies enable participants to navigate regulatory pressures and meet evolving customer demands while maintaining profitability in the European region.

MARKET SEGMENTATION

This research report on the Europe aviation fuel market has been segmented and sub-segmented into the following categories.

By Fuel Type

- Conventional Jet Fuel

- Sustainable Aviation Fuel (SAF)

- Avgas

By Aircraft Type

- Narrow-body

- Wide-body

- Regional Jets and Turboprops

- Cargo/Freighters

By Application

- Commercial Airlines

- Defense/Military Aviation

- General and Business Aviation

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe aviation fuel market?

The Europe aviation fuel market covers jet fuel and sustainable aviation fuel used by commercial, cargo, and defense aircraft. Demand is rising with air-travel recovery and decarbonization policy.

How does the Europe aviation fuel market function?

The Europe aviation fuel market functions through production, refining, storage, distribution, and aircraft refueling at airports. SAF supply is increasingly integrated into this chain.

What drives growth in the Europe aviation fuel market?

The Europe aviation fuel market grows on passenger traffic recovery, route expansion, and mandatory SAF blending. Airline ESG goals and public policy also support long-term demand.

Which countries lead the Europe aviation fuel market?

The Europe aviation fuel market is led by the UK, Germany, France, Spain, and the Netherlands. These countries combine strong airport hubs, airline demand, and fuel infrastructure.

What fuel types define the Europe aviation fuel market?

The Europe aviation fuel market includes conventional jet fuel, SAF, biojet fuel, and synthetic e-fuels. Conventional kerosene still dominates, but SAF is growing fastest.

What applications shape the Europe aviation fuel market?

The Europe aviation fuel market serves commercial aviation, cargo operations, general aviation, and defense flights. Commercial airlines account for the largest share of demand.

How does regulation influence the Europe aviation fuel market?

The Europe aviation fuel market is strongly shaped by ReFuelEU Aviation and related EU climate policy. Mandatory SAF shares are driving procurement, supply, and investment decisions.

What trends affect the Europe aviation fuel market?

The Europe aviation fuel market is seeing more SAF offtake deals, refinery upgrades, feedstock competition, and investment in alcohol-to-jet and power-to-liquid pathways.

What challenges face the Europe aviation fuel market?

The Europe aviation fuel market faces feedstock scarcity, high SAF costs, limited synthetic fuel capacity, and uneven airport infrastructure. These issues slow the pace of transition.

How does SAF impact the Europe aviation fuel market?

SAF is reshaping the Europe aviation fuel market by creating new demand for blended fuel, reducing emissions, and forcing suppliers to secure long-term supply contracts.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com