Europe Directed Energy Weapons Market Size, Share, Trends & Growth Forecast Report Segmented By Product Type (Lethal, Non-Lethal), Technology, Platform, Application, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe), Industry Analysis From 2026 To 2034

Europe Directed Energy Weapons Market Report Summary

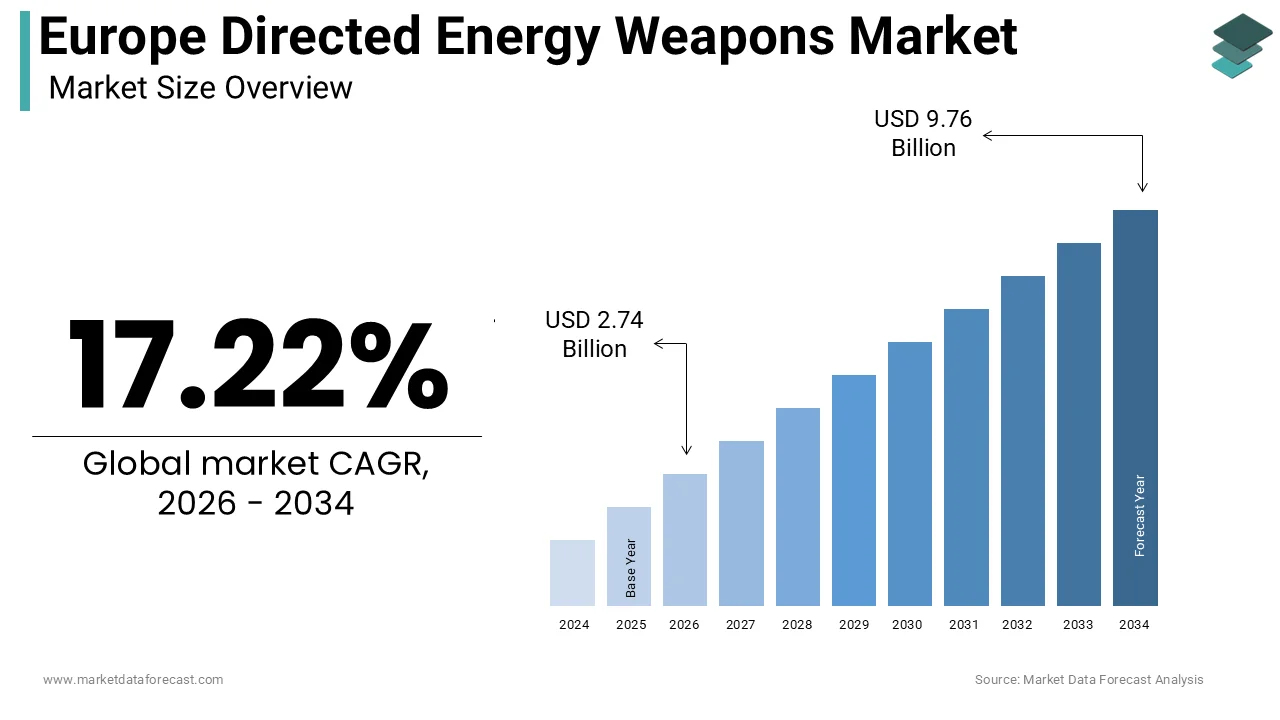

The Europe directed energy weapons market was valued at USD 2.34 billion in 2025 and is projected to reach USD 9.76 billion by 2034, growing from USD 2.74 billion in 2026 at a CAGR of 17.22% during the forecast period. Market growth is driven by increasing defense modernization programs, rising geopolitical tensions, and growing investments in advanced military technologies. Directed energy weapons (DEWs), including laser and microwave systems, are gaining traction due to their precision targeting, reduced operational costs, and ability to counter emerging threats such as drones and missiles.

Key Market Trends

- Rising adoption of laser-based defense systems

- Increasing investments in next-generation military technologies

- Growing demand for counter-drone and missile defense solutions

- Integration of DEWs into land, naval, and airborne platforms

- Expansion of collaborative defense programs across Europe

Segmental Insights

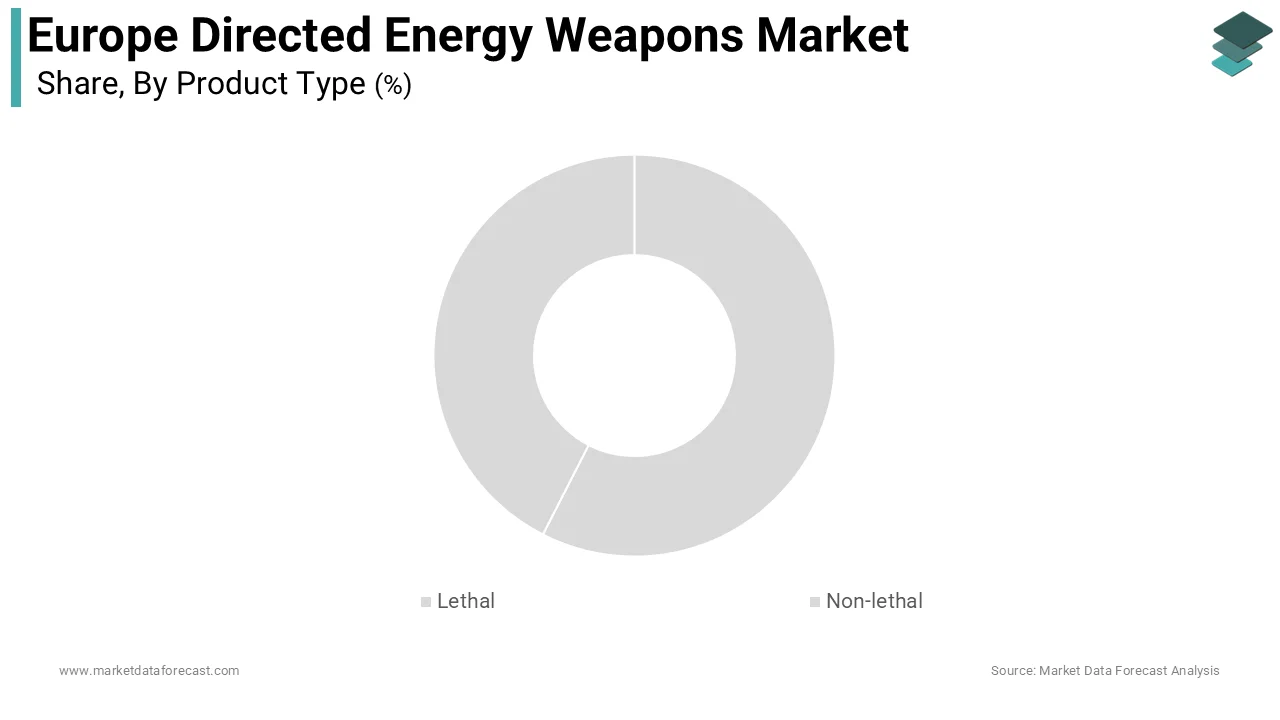

- Based on product type, the lethal segment dominated the Europe directed energy weapons market in 2025 by accounting for 65.4% of the regional market share, driven by increasing demand for high-power defense systems

- Based on the platform, the land-based segment led the market in 2025 by capturing 50.4% of the regional market share, supported by deployment in ground-based defense systems.

- Based on end use, the military and defense segment held the largest share in 2025, driven by increasing government investments in advanced weapon systems.

Regional Insights

- Germany led the Europe directed energy weapons market in 2025 by holding 25.7% of the regional market share, supported by strong defense manufacturing capabilities.

- United Kingdom ranked second with 18.2% share, driven by advanced research programs and defense innovation.

- France is expected to witness significant growth, supported by its industrial base and focus on technological independence.

- Italy is projected to grow steadily due to naval defense investments and European defense collaboration.s

- Sweden is anticipated to expand, supported by technological expertise and a strong domestic defenseindustryt.ry

Competitive Landscape

- The Europe directed energy weapons market is highly competitive, with leading defense contractors focusing on advanced laser technologies, high-energy systems, and integrated defense solutions. Companies are investing heavily in R&D and strategic collaborations to strengthen their technological capabilities.

- Prominent players in the Europe directed energy weapons market include Lockheed Martin Corporation, Raytheon Technologies Corporation, Northrop Grumman Corporation, BAE Systems plc, Leonardo S.p.A, Thales Group, Rheinmetall AG, MBDA, Elbit Systems Ltd, and L3Harris Technologies, Inc.

Europe Directed Energy Weapons Market Size

The Europe directed energy weapons market size was calculated to be USD 2.34 billion in 2025 and is anticipated to be worth USD 9.76 billion by 2034, from USD 2.74 billion in 2026, growing at a CAGR of 17.22% during the forecast period.

The directed energy weapons are advanced military systems that utilize concentrated electromagnetic energy or subatomic particles to disable, damage, or destroy targets. These technologies primarily include high-energy lasers, high-power microwaves, and particle beam weapons, which offer distinct advantages over conventional kinetic interceptors, such as speed of light engagement and low cost per shot. The strategic imperative for these systems has intensified due to the evolving nature of asymmetric threats, including unmanned aerial systems and swarm tactics. According to the European Defence Agency, member states have increasingly prioritized research into disruptive technologies, with collaborative projects receiving substantial funding under the Permanent Structured Cooperation framework. The North Atlantic Treaty Organization has also identified directed energy as a critical capability gap requiring urgent attention to ensure collective defense resilience. Furthermore, the European Commission’s Preparatory Action on Defence Research has allocated millions of Euros specifically for next-generation weapon systems.

MARKET DRIVERS

Escalating Threats from Unmanned Aerial Systems Drive Demand

The escalating threat posed by unmanned aerial systems, low-cost drones, and swarm tactics that overwhelm traditional air defense networks is fuelling the growth of Europe's directed energy weapons market. Conventional missile interceptors are often prohibitively expensive when used against cheap commercial drones, creating an unsustainable cost exchange ratio for defenders. Directed energy weapons offer a solution with a cost per engagement estimated at less than 10 Euros compared to hundreds of thousands for missiles. According to the research, the use of drones in recent conflicts has demonstrated their ability to disrupt military operations and inflict significant damage on critical infrastructure. This reality has prompted European nations to accelerate the development of laser-based counter-drone systems. As per the German Federal Ministry of Defence, the Bundeswehr has actively tested high-energy laser prototypes to protect forward operating bases and naval vessels from aerial threats. The ability of directed energy systems to engage multiple targets rapidly and with precision makes them ideal for countering swarm attacks. Furthermore, the unlimited magazine depth of laser systems, provided they have a power source, ensures sustained defensive capability during prolonged engagements. The European Defence Agency has launched several collaborative projects to address this specific vulnerability, emphasizing the need for indigenous solutions.

Strategic Shift Towards Cost-Effective Defense Mechanisms Accelerates Adoption

The strategic shift towards cost-effective defense mechanisms, as nations seek to optimize limited defense budgets, is also to leverage the growth of Europe directed energy weapons market. Traditional kinetic interceptors, such as surface-to-air missiles, are not only expensive but also limited in number, posing logistical challenges in high-intensity conflict scenarios. Directed energy weapons provide a compelling alternative by offering a low marginal cost per shot, primarily determined by electricity consumption. According to the International Institute for Strategic Studies, the average cost of a short-range air defense missile can exceed 100000 United States Dollars, whereas a laser engagement costs a fraction of that amount. This economic advantage allows military forces to maintain robust defense postures without depleting finite stockpiles. The ability to scale power output allows these systems to address a wide range of threats from small drones to larger missiles, providing versatile defense capabilities. Additionally, the reduced collateral damage associated with precise energy beams makes them suitable for urban environments and sensitive areas. The European Union’s Strategic Compass emphasizes the need for innovative and affordable defense solutions, further supporting this trend. Consequently, defense planners are increasingly integrating directed energy concepts into future procurement plans to achieve greater fiscal efficiency and operational effectiveness.

MARKET RESTRAINTS

Technical Maturity and Power Generation Constraints Restrain Deployment

The technical immaturity of key components, particularly regarding power generation, storage, and thermal management, is limiting the growth of Europe's directed energy weapons market. High-energy lasers and microwave systems require substantial electrical power delivered in compact and lightweight packages, which remains a significant engineering challenge for mobile platforms. According to the European Organisation for Nuclear Research, developing efficient power conditioning units that can operate in harsh military environments involves complex trade-offs between size, weight, and performance. Current battery technologies and generators often lack the energy density required for sustained high-power operations, limiting the duty cycle of these weapons. As per the German Aerospace Center, thermal dissipation is another factor, as excess heat generated during operation can degrade optical components and reduce system reliability. The need for advanced cooling systems adds further weight and complexity to the platform, potentially compromising mobility and survivability. Additionally, the atmospheric attenuation of laser beams due to weather conditions such as fog, rain, and dust reduces effectiveness in certain operational theaters. These technical hurdles require extensive research and development before directed energy weapons can achieve full operational capability.

Regulatory Hurdles and Ethical Concerns Regarding Weaponization Limit Progress

The regulatory hurdles and ethical concerns, as governments navigate complex legal frameworks governing new weapon technologies, are additional factors hindering the growth of Europe's directed energy weapons market. The use of directed energy weapons raises questions about compliance with international humanitarian law, particularly regarding proportionality and distinction in combat situations. According to the International Committee of the Red Cross, any new weapon must undergo rigorous legal review to ensure it does not cause unnecessary suffering or indiscriminate harm. The potential for lasers to cause permanent blindness has led to specific prohibitions under Protocol IV of the Convention on Certain Conventional Weapons requiring strict safeguards in system design. As per the European Parliament Research Service, there is ongoing debate about the implications of integrating artificial intelligence with directed energy systems for autonomous target engagement. Furthermore, export controls on dual-use technologies such as high-power lasers and advanced optics can hinder international collaboration and commercialization. The lack of standardized testing and certification protocols across European nations creates fragmentation in development efforts. These regulatory and ethical complexities slow down the procurement process and increase compliance costs for manufacturers.

MARKET OPPORTUNITIES

Integration with Existing Air Defense Architectures Presents Significant Opportunities

The integration of directed energy weapons with existing air defense architectures is certainly to pose as a new opportunity for the growth of Europe's directed energy weapons market. Military forces are increasingly seeking layered defense solutions, where directed energy systems complement traditional kinetic interceptors to provide comprehensive protection. According to the North Atlantic Treaty Organization, interoperability is a key priority for allied forces, driving the development of open architecture systems that can communicate with various sensors and effectors. Directed energy weapons can be integrated into current command and control networks, allowing for coordinated engagement strategies that maximize resource efficiency. As per the Italian Ministry of Defence, recent exercises have demonstrated the feasibility of combining laser systems with radar-guided guns to create a hybrid defense shield. This approach leverages the strengths of each technology, using lasers for low-cost precision strikes and missiles for high-value targets. The modular design of many directed energy prototypes facilitates retrofitting onto existing vehicles, ships, and aircraft, reducing acquisition costs. Furthermore, the data generated by these systems can enhance situational awareness and threat assessment capabilities. Governments are investing in middleware and interface standards to ensure seamless connectivity.

Advancements in Beam Control and Adaptive Optics Create New Avenues

The advancements in beam control and adaptive optics by enhancing the precision and effectiveness of energy delivery are another factor likely to elevate the growth of Europe's directed energy weapons market. Atmospheric turbulence and platform vibration can distort laser beams, reducing their intensity at the target site. Recent breakthroughs in adaptive optics allow systems to compensate for these distortions in real time, maintaining focus and maximizing damage potential. According to the European Space Agency, technologies developed for astronomical telescopes are being adapted for military applications, enabling sharper and more stable beams over longer distances. These innovations extend the effective range of directed energy weapons, making them viable against faster and more distant threats. Additionally, improvements in beam combining techniques allow multiple lower-power lasers to be merged into a single high-energy beam, overcoming power scaling limitations. This scalability enables the development of modular systems that can be tailored to specific mission requirements. The commercial sector’s progress in fiber laser technology also contributes to cost reductions and reliability improvements.

MARKET CHALLENGES

Atmospheric Interference and Weather Dependency Pose Operational Challenges

Atmospheric interference and weather dependency affect the operational reliability of laser-based systems, which also inhibits the growth of Europe directed energy weapons market. Laser beams are susceptible to scattering and absorption by water vapor aerosols and particulate matter, which significantly reduces their energy density at the target. This limitation restricts the all-weather capability of directed energy weapons, making them less reliable than kinetic alternatives in adverse conditions. As per the Royal Netherlands Meteorological Institute, variability in atmospheric transparency requires sophisticated sensing and prediction models to determine optimal engagement windows. Developing systems that can automatically adjust power levels or switch to backup kinetic weapons adds complexity and cost. Furthermore, thermal blooming caused by the heating of air along the beam path can defocus the laser, further reducing performance. These physical constraints necessitate extensive testing in diverse environmental conditions to validate operational effectiveness. Military planners must account for these limitations in doctrine and training, potentially reducing confidence in directed energy as a primary defense layer.

High Development Costs and Funding Uncertainties Hinder Program Continuity

The high development costs and funding uncertainties, as programs require sustained financial commitment over many years, also restrict the growth of Europe's directed energy weapons market. The research and development of high-energy lasers and microwave systems involves complex physics, engineering, and materials science, demanding substantial upfront investment. According to the European Defence Agency, collaborative defense projects often face budgetary constraints and competing priorities among member states, leading to delays or cancellations. As per the Stockholm International Peace Research Institute, fluctuations in national defense budgets can disrupt long-term procurement plans, affecting industry confidence and supply chain stability. The high-risk nature of directed energy technology means that failures in prototype stages can result in significant financial losses for contractors. Additionally, the lack of standardized funding mechanisms across European nations complicates joint development efforts. Small and medium-sized enterprises, which often drive innovation in niche technologies, may struggle to secure sufficient capital without government guarantees. The lengthy timeline from concept to deployment also increases the risk of technological obsolescence before systems become operational. These financial barriers can deter private investment and slow down the pace of innovation.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 17.22% |

| Segments Covered | By Product Type, Technology, Platform, Application, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Lockheed Martin Corporation, Raytheon Technologies Corporation, Northrop Grumman Corporation, BAE Systems plc, Leonardo S.p.A., Thales Group, Rheinmetall AG, MBDA, Elbit Systems Ltd., L3Harris Technologies, Inc. |

SEGMENTAL ANALYSIS

By Product Type Insights

The lethal segment was the largest by holding 65.4% of the Europe-directed energy weapons market share in 2025, with the need for effective countermeasures against increasingly sophisticated aerial threats, including cruise missiles, ballistic missiles, and unmanned aerial vehicles. According to the North Atlantic Treaty Organization, the alliance has identified air and missile defense as a top priority, with member states committing to enhancing their capabilities to protect populations and forces. Lethal directed energy systems such as high-energy lasers offer the ability to physically destroy targets at the speed of light, providing a decisive advantage in modern warfare. The cost-effectiveness of lethal lasers compared to expensive missile interceptors further drives adoption, allowing militaries to sustain defense operations during prolonged conflicts. The strategic imperative to maintain technological superiority and ensure national security against state and non-state actors ensures that lethal systems remain the primary focus of defense procurement budgets across Europe. Governments are prioritizing projects that deliver tangible combat capabilities, thereby sustaining the dominance of this segment in the regional market.

The non-lethal segment is likely to witness the fastest CAGR of 14.2% from 2026 to 2034, with the rising need for advanced crowd control and area denial technologies that minimize collateral damage and civilian casualties. Directed energy weapons such as active denial systems use millimeter waves to create a heating sensation on the skin, effectively dispersing crowds without causing permanent injury. As per the research, law enforcement agencies are actively exploring non-lethal directed energy tools to manage riots and secure critical infrastructure with greater precision and safety. The ethical advantages of non-lethal systems align with European values regarding human rights and proportionality in the use of force. Furthermore, the versatility of these systems allows for deployment in urban environments where kinetic weapons pose unacceptable risks. Government investments in homeland security and public order maintenance are driving the development and procurement of these technologies. The expanding application of non-lethal directed energy in both military and civilian contexts ensures robust growth for this segment in the coming years.

By Technology Insights

The high-energy laser segment accounted in holding 55.4% of the Europe directed energy weapons market share in 2025, with extensive research and development efforts dedicated to laser technologies, which have reached a higher level of maturity compared to other directed energy forms. High-energy lasers are effective against unmanned aerial systems, which pose a significant threat to military bases and critical infrastructure. According to the Royal United Services Institute, laser weapons have demonstrated successful engagements against drones in various test scenarios, validating their operational viability. The ability of lasers to provide precise engagement with minimal collateral damage makes them ideal for complex battlefields. Furthermore, the scalability of laser power allows for adaptation to different platform sizes from trucks to ships. The presence of key industrial players in Europe specializing in optics and photonics supports the supply chain for laser components. Government funding continues to prioritize laser programs due to their immediate applicability and potential for near-term deployment.

The high-power radio frequency segment is expected to witness the fastest CAGR of 16.5% from 2026 to 2034, with the unique ability of high-power microwaves to disrupt or destroy electronic circuits, making them highly effective against drone swarms and guided missiles. According to the European Defence Agency, research into high-power microwave technologies has intensified as a countermeasure to saturation attacks involving numerous low-cost drones. As per the studies, experiments have shown that microwave pulses can incapacitate unmanned vehicles by frying their internal electronics without physical destruction. This capability addresses a gap in current air defense architectures, which struggle with volume fires. The technology is also applicable for protecting critical infrastructure such as power grids and communication networks from electromagnetic pulse attacks. Governments are increasing investment in this sector, recognizing its strategic importance for future warfare. The development of compact and mobile high-power microwave systems is advancing rapidly, enabling deployment on various platforms.

By Platform Insights

The land-based segment accounted in holding 50.4% of the Europe directed energy weapons market share in 2025, with the ease of integrating directed energy systems onto ground vehicles and static installations, which provide stable platforms for power generation and cooling. Land-based systems are crucial for protecting forward operating bases, airfields, and command centers from aerial threats. As per the British Army, recent trials have demonstrated the effectiveness of truck-mounted lasers in engaging drones and mortars in realistic combat scenarios. The modular nature of land-based platforms allows for rapid relocation and deployment in diverse terrains. Furthermore, the power requirements for high-energy lasers are easier to meet on large ground vehicles compared to smaller airborne or naval platforms. The strategic need to secure land borders and military installations against asymmetric threats drives continuous investment in this segment. Collaborative projects among European nations often focus on land-based prototypes due to lower logistical complexity.

The naval segment is likely to grow at the fastest CAGR of 15.8% from 2026 to 2034, owing to the increasing integration of directed energy weapons on naval vessels to provide an additional layer of defense against anti-ship missiles and drones. Ships offer ample space and power generation capacity, making them ideal platforms for high-energy laser systems. The threat environment at sea is evolving with adversaries deploying advanced anti-ship capabilities that require rapid and cost-effective countermeasures. Directed energy weapons provide ships with an unlimited magazine depth, reducing reliance on finite missile stocks. The ability to engage multiple threats simultaneously enhances the defensive posture of naval task forces. European navies are collaborating on technology development to share costs and accelerate deployment.

By Application Insights

The military and defense segment was the largest by holding a significant share of the Europe directed energy weapons market in 2025 owing to the imperative for nations to maintain superior defense capabilities against evolving threats, including ballistic missiles, hypersonic weapons, and unmanned systems. Directed energy weapons are viewed as a transformative technology that can alter the balance of power by providing cost-effective and scalable defense solutions. As per the North Atlantic Treaty Organization, allied nations are prioritizing the development of disruptive technologies to maintain a technological edge over potential adversaries. The integration of directed energy systems into existing military architectures enhances overall combat effectiveness and operational flexibility. Government funding for defense research and development is substantial, with specific allocations for directed energy projects. The strategic autonomy agenda of the European Union also promotes indigenous development of defense technologies. The involvement of major defense contractors and government laboratories ensures a steady pipeline of innovation and procurement.

The homeland security segment is projected to register the fastest CAGR of 13.5% from 2026 to 2034, owing to the increasing need to protect critical infrastructure such as airports, power plants, and government buildings from terrorist attacks and unauthorized drone incursions. According to the European Union Agency for Law Enforcement Cooperation, the threat of asymmetric attacks using commercial drones has heightened the demand for effective countermeasures. Directed energy weapons offer a precise and non-lethal option for neutralizing such threats without causing widespread disruption. The ability to disable drones electronically or physically without debris fallout is particularly valuable in urban environments. Additionally, the rise in civil unrest and protests has prompted law enforcement agencies to consider non-lethal directed energy tools for crowd management. Government investments in smart city security and border protection further support this trend. The versatility of directed energy applications in civilian security contexts expands the market beyond traditional defense.

REGIONAL ANALYSIS

Germany Directed Energy Weapons Market Analysis

Germany was the top performer of the Europe directed energy weapons market by holding 25.7% of the share in 2025, with its strong engineering base and active participation in European defense collaborations. According to the German Federal Ministry of Defence, the Special Fund for the Bundeswehr includes allocations for next-generation weapon systems, including directed energy technologies. The strategic location of Germany within NATO makes it a key hub for air and missile defense planning. The government’s emphasis on technological sovereignty encourages indigenous development of critical defense capabilities. Recent tests of laser prototypes on ground vehicles have demonstrated progress towards operational deployment. The presence of a skilled workforce and advanced manufacturing infrastructure facilitates rapid prototyping and production.

United Kingdom Directed Energy Weapons Market Analysis

The United Kingdom's directed energy weapons market growth was positioned second by holding 18.2% of share in 2026 in aerospace and defense technology. The UK Ministry of Defence has been a pioneer in directed energy research, with projects such as Dragonfire achieving notable milestones in laser weapon development. The Strategic Defence and Security Review emphasizes the importance of emerging technologies in maintaining national security. The presence of renowned universities and research centers fosters innovation in photonics and artificial intelligence, which are critical for beam control. The UK’s exit from the European Union has not diminished its commitment to collaborative defense projects with European partners. The Royal Navy’s interest in equipping ships with laser defenses drives demand for naval-specific systems. Government funding for science and technology remains robust, supporting the transition from prototype to production.

France Directed Energy Weapons Market Analysis

France's directed energy weapons market growth is likely to grow with its strong industrial base and strategic focus on technological independence. The French Ministry of Armed Forces has launched several initiatives to develop directed energy capabilities, including laser weapons for air defense. The Future Combat Air System program includes considerations for directed energy effects to enhance aircraft survivability. The high-energy physics and optics support the development of advanced weapon systems. France’s participation in European collaborative projects, such as the Permanent Structured Cooperation, reinforces its role in shaping regional defense standards. The need to protect overseas territories and critical infrastructure drives demand for versatile directed energy solutions. The government’s commitment to maintaining a credible deterrent and expeditionary capability ensures sustained funding for innovative weapons.

Italy Directed Energy Weapons Market Analysis

Italy's directed energy weapons market growth is driven by its strong naval tradition and involvement in European defense collaborations. According to research, a leading Italian aerospace and defense company significant resources to the development of directed energy technologies, including high-energy lasers. The Horizon-class frigates and future destroyers are potential platforms for these systems. Italy’s participation in NATO and European Union defense programs facilitates knowledge exchange and joint development efforts. The strategic importance of the Mediterranean region necessitates robust air and missile defense capabilities. Government incentives for defense innovation encourage private sector investment in directed energy research.

Sweden Directed Energy Weapons Market Analysis

Sweden's directed energy weapons market growth is driven by its high level of technological sophistication and strong defense industry. According to the Swedish Armed Forces, the integration of directed energy systems is part of a broader strategy to enhance air defense capabilities. Saab, a major Swedish defense contractor, is involved in the development of integrated air defense systems that may incorporate directed energy effects in the future. Sweden’s neutrality tradition has evolved into active participation in European defense cooperation, enhancing opportunities for collaboration. The country’s expertise in electronics and software contributes to the development of sophisticated beam control systems. The need to protect critical infrastructure in remote areas drives interest in mobile directed energy solutions.

COMPETITION OVERVIEW

The competition in the Europe directed energy weapons market is characterized by intense rivalry among established defense primes and specialized technology firms vying for leadership in this emerging sector. Leading companies leverage their extensive expertise in aerospace electronics and optics to develop advanced laser and microwave systems. The market sees significant competition in the development of high-energy lasers for counter-drone and missile defense applications. Strategic partnerships and collaborative projects are common as companies seek to share the high costs and risks associated with research and development. Governments play a crucial role in shaping the competitive landscape through funding initiatives and procurement policies that favor indigenous technologies. Differentiation is achieved through technological superiority, system integration capabilities, and proven operational performance. The threat of new entrants is moderate due to high barriers related to technical complexity and security clearances.

KEY MARKET PLAYERS

A few major players of the Europe directed energy weapons market include

- Lockheed Martin Corporation

- Raytheon Technologies Corporation

- Northrop Grumman Corporation

- BAE Systems plc

- Leonardo S.p.A

- Thales Group

- Rheinmetall AG

- MBDA

- Elbit Systems Ltd

- L3Harris Technologies, Inc

Top Strategies Used by Key Market Participants

Key players in the Europe directed energy weapons market primarily employ strategies focused on strategic collaborations and joint research initiatives to share development costs and risks. Companies are increasingly partnering with government agencies and academic institutions to accelerate technological breakthroughs in laser and microwave technologies. Investment in research and development is prioritized to enhance beam quality, power scaling, and thermal management capabilities. Manufacturers are also focusing on modular designs that allow for easy integration onto existing military platforms such as ships, vehicles, and aircraft. Demonstrating operational effectiveness through live fire trials and prototypes is a critical strategy to gain customer confidence and secure procurement contracts. Additionally, firms are expanding their supply chains to ensure access to specialized components like high-quality optics and advanced power sources.

Leading Players in the Market

- Rheinmetall AG is a leading defense technology company in Europe with a strong focus on directed energy weapons. The company has developed the high-energy laser effecter, which successfully demonstrated its capability to intercept drones and mortar shells. Rheinmetall actively collaborates with international partners to integrate laser systems onto various platforms, including naval vessels and ground vehicles. Their recent actions include expanding production facilities for laser components and securing contracts with the German Bundeswehr for prototype testing. The company continues to invest in research and development to enhance the power and efficiency of its laser weapons, ensuring they meet the evolving needs of modern warfare and maintain technological superiority in the global market.

- MBDA is a major European missile systems manufacturer that is increasingly integrating directed energy technologies into its portfolio. The company focuses on developing hybrid systems that combine kinetic interceptors with high-energy lasers for layered defense. MBDA has participated in several European collaborative projects aimed at advancing laser weapon capabilities for air and missile defense. Recent actions include partnering with industry leaders to develop compact and scalable laser modules suitable for naval and land-based applications. They are also exploring high-power microwave technologies to counter drone swarms. Their commitment to interoperability and standardization ensures their solutions align with NATO requirements, strengthening their market presence and influence in the defense sector.

- Leonardo S.p.A. is a prominent Italian aerospace and defense company actively engaged in the development of directed energy weapons. The company leverages its expertise in electronics and photonics to create advanced laser systems for military applications. Leonardo has been involved in multiple research initiatives funded by the Italian Ministry of Defence and the European Union to explore the potential of high-energy lasers. Recent actions include demonstrating prototype laser weapons for naval defense and collaborating with academic institutions to improve beam control algorithms. They are also investigating the integration of directed energy effects into future combat air systems.

MARKET SEGMENTATION

This research report on the Europe market has been segmented and sub-segmented based on product type, technology, platform, application & region.

By Product Type

- Lethal

- Non-lethal

By Technology

- High Energy Laser

- High-power radio frequency

- Electromagnetic weapons

- Sonic weapons

By Platform

- Land

- Airborne

- Naval

- Space

By Application

- Military & Defense

- Homeland security

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is driving the growth of this market in Europe?

Growth is driven by increasing defense budgets, rising geopolitical tensions, and the need for advanced, cost-effective defense systems.

2. What types of directed energy weapons are used in Europe?

The main types include high-energy laser systems, high-power microwave systems, and particle beam weapons.

3. What are the key applications of DEWs?

Applications include missile defense, drone neutralization, electronic warfare, and protection of critical infrastructure.

4. What are the advantages of directed energy weapons?

They offer precision targeting, low cost per shot, reduced collateral damage, and rapid response capabilities.

5. What challenges does the Europe DEW market face?

Challenges include high development costs, technological complexity, power requirements, and regulatory constraints.

6. Who are the key players in the Europe directed energy weapons market?

Major players include Lockheed Martin Corporation, Raytheon Technologies Corporation, BAE Systems plc, Leonardo S.p.A., Thales Group, and Rheinmetall AG.

7. How are directed energy weapons different from conventional weapons?

Unlike traditional weapons that use kinetic energy or explosives, DEWs use electromagnetic energy to engage targets at the speed of light.

8 . What role does research and development play in this market?

R&D is critical, as continuous innovation is required to improve power efficiency, targeting accuracy, and operational effectiveness.

9. What is the impact of DEWs on modern warfare?

DEWs are transforming warfare by enabling precise, rapid, and cost-efficient defense solutions against emerging threats like drones and missiles.

10. What is the future outlook of the Europe DEW market?

The market is expected to grow significantly due to rising defense modernization programs and increasing investments in advanced weapon technologies.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com