Europe FPV Drone Market Size, Share, Trends & Growth Forecast Report, Segmented By Component Type (FPV Goggles, FPV Remote Controllers, Cameras, Battery, Flight Controller, Airframe, Motor, Processors, Others), Application, End User, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe) - Industry Analysis From (2026 To 2034)

Europe FPV Drone Market Report Summary

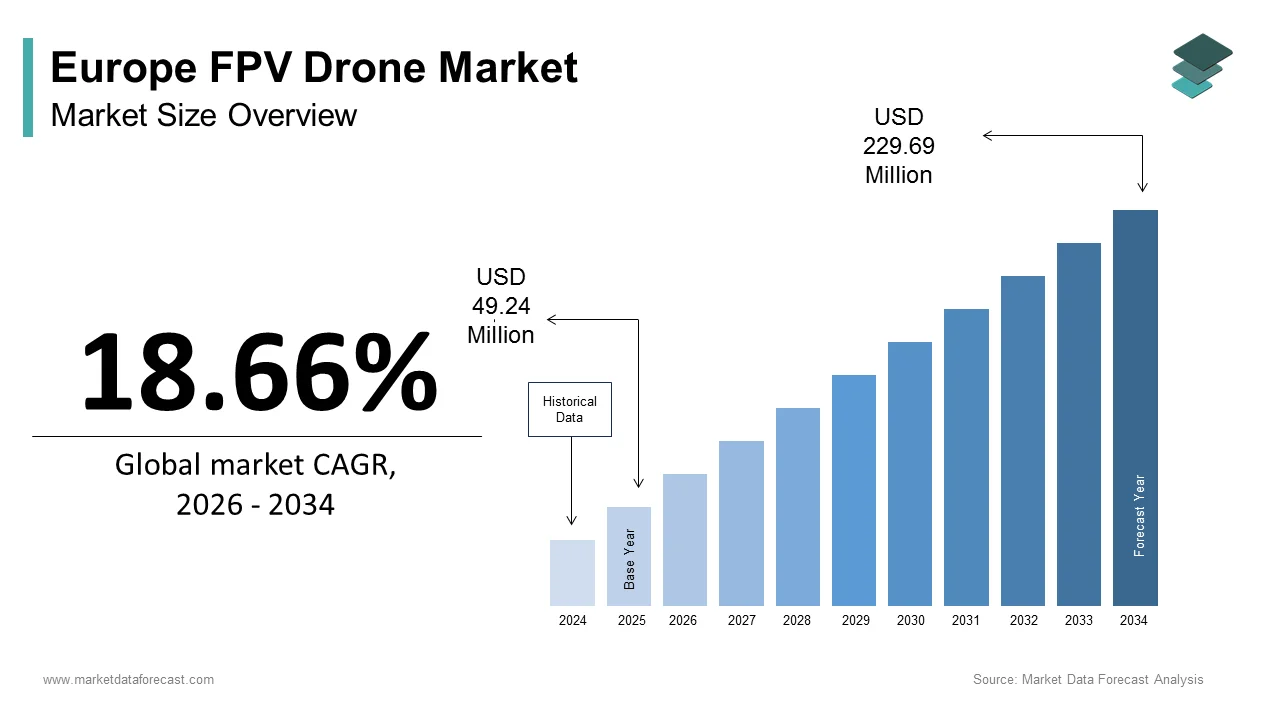

The Europe FPV drone market was valued at USD 49.24 billion in 2025 and is projected to reach USD 229.69 billion by 2034, growing from USD 58.43 billion in 2026 at a CAGR of 18.66% during the forecast period. The market is expanding rapidly due to the rising popularity of drone racing, immersive aerial videography, esports integration, and growing recreational drone adoption. Advancements in camera technology, low-latency transmission systems, and compact flight controllers are enhancing the FPV experience. Increasing regulatory clarity across Europe and expanding consumer electronics ecosystems are further supporting market growth.

Key Market Trends

- Rapid growth of competitive drone racing and rotor cross events

- Rising adoption of immersive FPV goggles with HD digital transmission

- Expansion of FPV drones in cinematography and content creation

- Increasing integration of AI-assisted flight stabilization

- Growing interest in educational and STEM-based drone programs

Segmental Insights

- Based on component type, the FPV goggles segment dominated the Europe FPV drone market in 2024 by accounting for 28.3% of the total market share, driven by their role as the primary human-machine interface enabling immersive real-time flight experiences

- Based on application, the rotor cross segment led the market in 2025 by capturing 54.3% of the regional market share, supported by the strong growth of competitive drone racing leagues

- Based on end user, the consumer electronics segment held the largest share in 2025, reflecting strong demand from hobbyists, gamers, and professional content creators

Regional Insights

- Germany led the Europe FPV drone market in 2025 by holding 23.1% of the regional market share, supported by strong engineering culture and organized drone racing communities

- United Kingdom ranked second in 2025 with 19.4% share, driven by mature consumer drone adoption and competitive drone sports

- France is expected to witness significant growth opportunities, supported by structured sporting events and public safety applications

- Sweden is projected to grow steadily, driven by innovation in industrial FPV applications and sustainable drone design

- Netherlands is anticipated to expand during the forecast period, supported by regulatory leadership and educational integration initiatives

Competitive Landscape

The Europe FPV drone market is highly dynamic, with companies focusing on advanced camera modules, high-performance flight controllers, and immersive digital transmission systems. Manufacturers are emphasizing lightweight materials, modular drone kits, and upgraded FPV goggles to enhance user experience and competitive performance.

Prominent players in the Europe FPV drone market include DJI, Parrot, iFlight Technology, BetaFPV Technology, GEPRC, Lumenier, Horizon Hobby, Holy Stone, Skyzone, and Syma

Europe FPV Drone Market Size

The Europe FPV drone market size was calculated to be USD 49.24 billion in 2025 and is anticipated to be worth USD 229.69 billion by 2034, from USD 58.43 billion in 2026, growing at a CAGR of 18.66% during the forecast period.

The FPV (First Person View) drone is the design, manufacture, and use of unmanned aerial vehicles equipped with real-time video transmission systems that allow pilots to navigate through immersive goggles or monitors as if seated in the cockpit. Unlike standard camera drones optimized for stability and automated flight, FPV drones prioritize agility, speed, and low-latency video feeds by making them essential for racing, freestyle acrobatics, cinematic filming, and emerging industrial inspection applications. As per the European Union Aviation Safety Agency (EASA), over 120000 FPV-capable drones were registered by recreational and professional operators across the EU in 2025, which reflects growing adoption beyond niche hobbyist circles. Technological convergence with AI, lightweight materials, and digital HD video systems has further blurred boundaries between consumer entertainment and professional utility, positioning FPV drones as a dynamic segment at the intersection of sport, media, and advanced aerial robotics.

MARKET DRIVERS

Proliferation of Drone Racing and Freestyle Communities Drives Recreational Demand

The organized FPV drone sports have evolved from underground gatherings into mainstream competitive disciplines by creating sustained demand for high-performance equipment. The proliferation of drone racing and freestyle communities is majorly accelerating the growth of Europe FPV drone market. According to the Federation Aeronautique Internationale, over 850 officially recognized drone racing events took place in Europe in 2025, with national leagues in Germany, France, and the UK attracting thousands of participants and spectators. The Drone Champions League alone reported 1.2 million live viewers for its 2025 European finals held in Switzerland, broadcast on Eurosport and YouTube. National aviation authorities now recognize FPV racing as a legitimate sport, with countries like Sweden and the Netherlands allocating public land for permanent race tracks. Youth engagement is particularly strong, where a 2025 survey found that 63% of members aged 14 to 25 began flying FPV drones through school clubs or local racing teams.

Adoption in Cinematic and Professional Aerial Filmmaking Expands Commercial Use

FPV drones are increasingly favored by European filmmakers and content creators for their unmatched ability to capture dynamic, immersive shots previously achievable only with expensive cranes or helicopters. The adoption in cinematic and professional aerial filmmaking is additionally accelerating the growth of Europe FPV drone market. According to the European Film Academy, 41% of independent film productions in 2025 incorporated FPV drone footage for chase sequences, forest tracking shots, and architectural fly-throughs due to their maneuverability and cost efficiency. Broadcasters like BBC and ARD now employ dedicated FPV units for nature documentaries and live sports coverage, such as mountain biking and skiing events, where traditional drones cannot match speed or proximity. The shift to digital HD analog systems like DJI’s Digital FPV System and Walksnail’s Avatar has reduced latency to under 30 milliseconds while delivering 1080p clarity, meeting broadcast quality standards. This professional validation elevates FPV from a hobbyist tool to a critical production asset, driving demand for reliable, cinema-grade systems with failsafe telemetry and modular payload options.

MARKET RESTRAINTS

Stringent EU Aviation Regulations Restrict Operational Freedom

The significant legal constraints under EASA’s regulatory framework, which mandates that all flights maintain a direct visual line of sight unless granted specific operational authorization, are one of the factors restricting the growth of Europe FPV drone market. Since FPV flying inherently involves looking at a screen rather than the aircraft, it is automatically classified under the “specific” category requiring risk assessment, pilot certification, and often an observer to maintain visual contact, where a logistical barrier for casual users. According to the European Commission’s Mobility and Transport Directorate, some of the FPV pilot applications for recreational use received approval in 2025 due to complex documentation and inconsistent interpretation across member states. Countries like Germany and Austria impose additional restrictions near urban areas and natural reserves, while France requires mandatory geo-fencing compliance.

Short Flight Times and High Maintenance Demands Limit Accessibility

FPV drones suffer from inherent technical limitations that constrain mainstream adoption due to brief battery life and mechanical fragility. This factor is also degrading the growth of Europe FPV drone market. Most high-speed FPV quads operate for only 3 to 6 minutes per lithium polymer battery cycle, as confirmed by independent testing from the German Aerospace Center (DLR) in 2025. Pilots must carry multiple batteries, chargers, and spare parts, often spending more time repairing crashes than flying. A single competitive build can cost over 800 euros and require weekly maintenance, including motor replacements, frame repairs, and ESC recalibration. According to a 2025 survey by the European FPV Pilots Network, 57% of new pilots abandoned the hobby within six months, citing cost and complexity. While ready-to-fly models have simplified entry, they still lack the durability of conventional camera drones. This high barrier to sustained engagement restricts the market to dedicated enthusiasts and professionals, inhibiting mass consumer penetration.

MARKET OPPORTUNITIES

Integration of AI and Autonomous Navigation for Industrial Inspection

The adoption of FPV technology for industrial applications, where speed and obstacle navigation are positively impacting the growth of Europe FPV drone market. Companies are developing AI-enhanced FPV drones capable of autonomously inspecting confined or complex structures, such as wind turbine blades, power plant boilers, and railway tunnels. In 2025, the Swedish energy firm Vattenfall piloted an FPV system with onboard neural networks that could detect microcracks in offshore wind towers at speeds up to 70 kilometers per hour, three times faster than traditional drones. Similarly, Deutsche Bahn deployed FPV drones in German rail tunnels to assess infrastructure integrity without service disruption. These systems leverage FPV’s low latency and agility while adding collision avoidance and data logging features compliant with industrial safety standards.

Development of Simulated Training and Digital Twin Platforms

The rise of realistic FPV drone simulators is lowering entry barriers and accelerating skill development, which is also expected to escalate new opportunities for the growth of Europe FPV drone market. Platforms like Liftoff and Velocidrone now offer physics-accurate environments where pilots can practice racing lines and acrobatics without risking hardware. According to the European Simulation Education Consortium, many schools and vocational institutes integrated FPV simulators into STEM curricula in 2025, using them to teach aerodynamics, coding, and spatial reasoning. Esports organizations, such as ESL, have launched official FPV racing leagues with virtual qualifiers by enabling global participation regardless of local regulations or weather. These digital twins also serve professional sectors, whereas Airbus uses custom simulators to train inspection drone pilots for aircraft hangar assessments. Simulation expands the talent pipeline and creates recurring software revenue streams, transforming FPV from a hardware-centric hobby into an ecosystem blending physical and virtual engagement.

Intense Competition from Low-Cost Asian Manufacturers Undermines Brand Value

The flooded with inexpensive, often uncertified components from Chinese manufacturers sold via e-commerce platforms like Amazon and Banggood, eroding trust in quality and safety. This factor is substantially acting as a barrier for the growth of Europe FPV drone market. According to the European Commission’s RAPEX alert system, 23 FPV-related products were flagged in 2025 for non-compliant batteries, misleading CE markings, or excessive radio interference. These substandard units, priced 40 to 70% below reputable brands, frequently fail mid-flight or catch fire, damaging the category’s reputation. Established European brands like TBS and Lumenier struggle to justify premium pricing when consumers perceive similar specs at lower costs. Without harmonized EU-wide import screening or mandatory conformity verification for drone components, responsible manufacturers bear disproportionate costs for certification and support, while unsafe alternatives proliferate, increasing accident risks and regulatory scrutiny for the entire sector.

Lack of Standardized Training and Certification Pathways Hinders Professionalization

The lack of a unified FPV pilot certification framework creates uncertainty for employers and insurers, which is additionally degrading the growth of Europe FPV drone market. While EASA mandates theoretical knowledge exams for drone operators, these do not address FPV-specific skills such as depth perception in goggles, emergency recovery, or low-latency response. According to the European Aviation Training Association, only three countries, such as Switzerland, Finland, and the Netherlands, offer accredited FPV training modules as of 2025. Consequently, film studios and inspection firms rely on informal credentials or self-declared experience, increasing liability risks. Insurers like Allianz report that FPV-related claims are 2.3 times higher than standard drone incidents due to crash frequency and property damage. Until standardized curricula, competency assessments, and insurance protocols are established, professional adoption will remain fragmented and risk-averse, limiting the market’s transition from enthusiast passion to scalable industry.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 18.66% |

| Segments Covered | By Component Type, Application, End User, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | DJI, Parrot Drones, iFlight Technology, BetaFPV Technology, GEPRC, Lumenier, Horizon Hobby, Holy Stone, Skyzone, Syma |

SEGMENTAL ANALYSIS

By Component Type Insights

The FPV goggles segment was the largest by holding 28.3% of the Europe FPV drone market share in 2025, owing to their role as the primary human-machine interface that defines the immersive FPV experience. Unlike other components, which can be shared across builds, each pilot requires a dedicated goggle system, driving consistent per capita demand. The shift from analog to digital HD systems, such as DJI’s Digital FPV Goggles and Walksnail’s Avatar series, has further amplified value per unit. In 2025, over 72% of new FPV pilots in Germany, France, and the UK purchased digital goggles as their first major investment. Regulatory compliance also plays a role, where EASA guidelines increasingly require low-latency video feeds for authorized operations by making high-quality goggles a non-optional safety tool rather than a luxury accessory. Their centrality to both recreational and professional use ensures sustained replacement cycles due to technological obsolescence and physical wear.

The processors segment is expected to witness the fastest CAGR of 18.6% from 2025 to 2033, owing to the integration of AI edge computing into FPV systems for autonomous navigation, obstacle avoidance, and real-time telemetry analysis. Modern flight stacks now incorporate ARM Cortex M7 and RISC-V-based processors capable of running neural networks onboard without ground dependency. In 2025, the Swedish startup SkyPerception launched an FPV inspection drone using a custom processor that processes LiDAR and video data simultaneously to navigate turbine interiors at 60 kilometers per hour. Similarly, European film studios increasingly demand Google processors that support 1080p60 video with under 25 millisecond latency to meet broadcast standards. As EU regulations mandate enhanced situational awareness for beyond visual line of sight operations, processors become enablers of compliance, scalability, and safety, pushing innovation beyond traditional flight control functions.

By Application Insights

The rotor cross segment was the largest by holding 54.3% of the Europe FPV drone market share in 2025, with the freestyle discipline emphasizing acrobatic maneuvers through natural or urban environments. The growth of the segment is also driven by the broad accessibility, low barrier to entry, and strong social media appeal. Unlike structured racing, Rotor Cross requires no formal track, only open space and creativity, making it ideal for solo or small group flying in forests, parks, or abandoned structures. Platforms like YouTube and Instagram feature millions of Rotor Cross clips with hashtags like #FPVFreestyle, generating over 3 billion views in 2025 alone, fueling viral adoption among youth. National communities in the UK, Germany, and Spain organize weekly “meetups” where pilots share routes and techniques, fostering grassroots growth. Equipment manufacturers prioritize durability and camera quality over speed, aligning product development with this dominant use case and ensuring consistent demand for wide-angle cameras and impact-resistant airframes.

The time trial FPV racing segment is likely to witness the fastest CAGR of 15.2% throughout the forecast period, which involves solo pilots navigating standardized courses against the clock, combining precision speed and consistency for televised and online competition. The 2025 European Time Trial Championship held in Switzerland attracted over 200 competitors and 500000 live viewers on Twitch, demonstrating its spectator potential. Broadcasters favor Time Trial for its clean production logistics and measurable performance metrics, unlike chaotic multi-pilot races. Standardized course kits from brands like MultiGP enable backyard setup, driving home use. Its blend of sport science and entertainment positions Time Trial as the gateway for institutional and mainstream engagement beyond niche hobbyist circles.

By End User Insights

The consumer electronics segment was the largest by holding a prominent share of the Europe FPV drone market in 2025, with the category’s roots in hobbyist culture, where individuals purchase ready-to-fly kits or build custom drones for recreation, content creation, and community participation. Over 850000 Europeans identified as active FPV pilots in 2025, with an average annual spending of 1200 euros on component upgrades and accessories. Retail channels like Amazon, MediaMarkt, and specialized online stores such as GetFPV dominate distribution, catering to tech-savvy consumers who value modularity and performance. Social media further fuels consumption with unboxing videos and build tutorials, driving component turnover. Unlike commercial users who prioritize reliability, consumer pilots embrace rapid iteration, seeking marginal gains in speed or camera quality, ensuring consistent demand for the latest processors, motors, and batteries even amid regulatory uncertainty.

The commercial segment is expanding at a CAGR of 21.4% from 2025 to 2033, owing to the industrial adoption in energy infrastructure and media, where FPV’s agility enables inspections and filming previously deemed too risky or costly. In 2025, Vattenfall deployed FPV drones to inspect offshore wind farms in the Baltic Sea, reducing turbine downtime by 40% compared to conventional methods. Similarly, BBC Studios used FPV units to film mountain biking sequences for the Planet Earth III series, achieving shots impossible with cable cams. EU Horizon Europe grants have funded over 30 projects integrating FPV with digital twins for predictive maintenance in railways and power grids.

REGIONAL ANALYSIS

Germany FPV Drone Market Analysis

Germany was the largest contributor to the Europe FPV drone market by capturing 23.1% of the share in 2025, with the technical rigor, strong maker culture, and early regulatory clarity. Over 180000 registered FPV pilots operate under the country’s well-structured LUC (Light UAS Operator Certificate) system, enabling authorized beyond visual line of sight flights. Berlin, Hamburg, and Munich host thriving communities that organize weekly freestyle events and engineering workshops. German manufacturers like TBS and Lumenier lead in high-end component design, particularly in flight controllers and video transmitters. The government’s Digital Infrastructure Act allocates funding for drone corridors in industrial zones, accelerating commercial adoption in logistics and energy sectors. Strict CE and EMC compliance also makes Germany a testing ground for EU-wide product certification.

United Kingdom FPV Drone Market Analysis

The United Kingdom FPC drone market ranked second by holding 19.4% of the market share in 2025, with grassroots racing and cinematic innovation. London serves as a hub for FPV cinematography, with studios like SkyMagic producing content for major broadcasters. According to the UK Civil Aviation Authority, over 65000 FPV operators held valid PfCO or GVC certifications in 2025, enabling commercial work. The UK introduced streamlined authorization pathways for FPV operations under the Drone and Model Aircraft Registration Scheme, reducing approval times by 50% compared to EU averages.

France FPV Drone Market Analysis

The French FPV drone market is expected to grow with significant opportunities during the forecast period, with a distinctive emphasis on organized sport and public safety integration. The shaped by national initiatives like the French Drone Federation, which hosts the annual Coupe de France de Drone Racing, attracting over 500 competitors. Paris and Lyon have designated urban FPV zones allowing controlled freestyle flights near landmarks, a model being replicated across Europe. The French Ministry of Interior has piloted FPV drones for firefighting reconnaissance in high-rise buildings, leveraging their ability to navigate smoke-filled corridors. Strong aerospace heritage and engineering education pipelines ensure a steady supply of skilled builders and developers, reinforcing France’s position as a continental leader in both competitive and applied FPV domains.

Sweden FPV Drone Market Analysis

Sweden's FPV drone market growth is likely to grow with the innovation in industrial FPV applications and sustainable design. In 2025, Vattenfall and Fortum deployed FPV inspection fleets across Nordic hydroelectric and wind facilities using AI-enabled drones to assess infrastructure integrity in extreme cold. Swedish startups like SkyPerception embed recyclable materials and modular architectures into FPV systems, aligning with the country’s circular economy mandates. The Swedish Transport Agency offers one of Europe’s most efficient authorization processes for commercial FPV operations, with 90% of applications approved within 10 days. Universities in Stockholm and Gothenburg integrate FPV into robotics curricula, producing a talent pool that attracts EU research funding and corporate R&D partnerships, positioning Sweden as a testbed for next-generation autonomous FPV solutions.

Netherlands FPV Drone Market Analysis

The Netherlands FPV drone market growth is likely to grow with anticipated regulatory leadership and educational integration. Its market status is defined by proactive airspace management through the Dutch U-space program, which enables automated FPV flight approvals in designated zones around Amsterdam, Rotterdam, and Eindhoven. The Dutch Ministry of Education funds FPV STEM kits in 300 secondary schools, teaching aerodynamics, coding, and spatial reasoning through drone racing simulations. Companies like Avy use FPV platforms for medical delivery trials in rural areas, leveraging low-latency control for precision landings.

COMPETITION OVERVIEW

The Europe FPV drone market features intense rivalry between global tech giants, niche component specialists, and agile startups. DJI dominates with integrated systems but faces pressure from open source alternatives like Walksnail that offer greater customization at lower costs. European firms such as TBS leverage regional expertise in radio telemetry and regulatory navigation to serve professional and racing segments. Competition centers on video latency reliability and compliance rather than price alone. The market is highly fragmented, with pilots often mixing components from multiple brands, creating opportunities for interoperable solutions. Regulatory complexity under EASA favors companies with legal resources and local presence, while community credibility remains critical for grassroots adoption.

KEY MARKET PLAYERS

- A few major players of the Europe FPV drone market include

- DJI

- Parrot Drones

- iFlight Technology

- BetaFPV Technology

- GEPRC

- Lumenier

- Horizon Hobby

- Holy Stone

- Skyzone

- Syma

Top Strategies Used by the Key Market Participants

Key players in the Europe FPV drone market are investing in digital HD video systems with ultra-low latency to meet broadcast and safety standards. They are enhancing regulatory compliance through automatic geo-fencing firmware updates and EASA-aligned operational features. Companies are establishing local service centers and training programs to build trust and reduce repair turnaround times. Strategic partnerships with retailers, racing leagues, and educational institutions help expand community engagement and skill development. Additionally, they are adopting open architecture designs to ensure compatibility with third-party components, fostering ecosystem loyalty and reducing consumer lock-in barriers.

Leading Players in the Market

- DJI is a global leader in drone technology with significant influence in the Europe FPV drone market through its Digital FPV System and Avata platforms. The company contributes to the global ecosystem by setting benchmarks in low-latency HD video transmission, flight stability, and integrated safety features. In Europe, DJI has cultivated strong adoption among both recreational pilots and professional cinematographers by aligning its products with EASA regulatory frameworks. Recently, it strengthened its position by launching firmware updates that enable automatic geo-fencing compliance across all EU member states and introduced a modular goggle system with swappable batteries and diopter lenses, enhancing accessibility for diverse users while maintaining broadcast quality performance.

- Walksnail is an emerging Chinese innovator rapidly gaining traction in Europe through its Avatar HD FPV system, known for ultra-low latency and high-resolution video. The company contributes globally by challenging traditional analog dominance with affordable digital alternatives that democratize professional-grade immersion. In Europe, Walksnail has built a loyal following among freestyle and racing communities by prioritizing open architecture compatibility with third-party transmitters and goggles.

- TBS Crossfire is a German-based pioneer in FPV radio control systems and flight controllers with deep roots in Europe’s drone racing scene. The company contributes to the global market by developing long-range, robust telemetry solutions that enable reliable beyond visual line of sight operations. Its Crossfire and Tracer systems are industry standards in competitive racing and industrial inspection. Recently, TBS enhanced its European presence by releasing a new generation of ELRS-compatible receivers with enhanced encryption for commercial applications and launching a developer program for universities to integrate its flight stacks into autonomous research drones, fostering next-generation talent and innovation within the EU.

MARKET SEGMENTATION

This research report on the Europe market has been segmented and sub-segmented based on component type, application, end user, & region.

- By Component Type

- FPV Goggles

- FPV Remote Controllers

- Cameras

- Battery

- Flight Controller

- Airframe

- Motor

- Processors

- Others

By Application

- Rotor Cross

- Drag Racing

- Time Trail

- Others

By End User

- Commercial

- Aerospace & Defense

- Consumer Electronics

- Healthcare

- Other

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What factors are driving the growth of the Europe FPV drone market?

Key growth drivers include the rising popularity of drone racing leagues, demand for immersive aerial videography, advancements in battery life and transmission systems, and growing use in industrial inspections.

2. What are the major challenges faced by FPV drone manufacturers in Europe?

Strict aviation regulations, privacy concerns, high product costs, limited flight zones, and technical complexity for beginners are major challenges in the market.

3. What are the key applications of FPV drones in Europe?

FPV drones are widely used for drone racing, freestyle flying, aerial cinematography, surveillance, agriculture monitoring, infrastructure inspection, and military training simulations.

4. How is drone racing influencing the FPV drone market in Europe?

Drone racing is significantly boosting demand for high-performance FPV drones with advanced controllers, low-latency video transmission, and lightweight carbon fiber frames.

5. What impact do European drone regulations have on FPV drone adoption?

European Union Aviation Safety Agency (EASA) regulations require drone registration, pilot competency certification, and operational limitations, which impact adoption but also improve safety and structured growth.

6. What is the difference between FPV drones and standard consumer drones?

FPV drones provide real-time video transmission to goggles for immersive control and are usually manually piloted, whereas standard drones often have GPS stabilization, autonomous features, and easier controls.

7. Which distribution channels are most common for FPV drones in Europe?

Online retail platforms, specialty hobby stores, drone racing communities, and direct-to-consumer brand websites are the primary distribution channels.

8. How is technological advancement shaping the FPV drone industry in Europe?

Improvements in HD digital transmission systems, lightweight materials, brushless motors, AI-assisted stabilization, and longer battery life are enhancing performance and user experience.

9. How is the demand for high-performance cameras impacting FPV drone sales?

The rising demand for 4K and HD low-latency cameras for professional videography is driving upgrades and premium FPV drone sales.

10. What are the future trends expected in the Europe FPV drone market?

Future trends include integration of AI-based navigation, 5G-enabled transmission, improved battery efficiency, expanded drone racing leagues, and increased adoption in defense and industrial monitoring applications.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com