Europe High Bandwidth Memory Market Size, Share, Trends, and Growth Analysis Report, Segmented by Type, Application, and Country – Industry Forecast From 2026 to 2034

Europe High Bandwidth Memory Market Report Summary

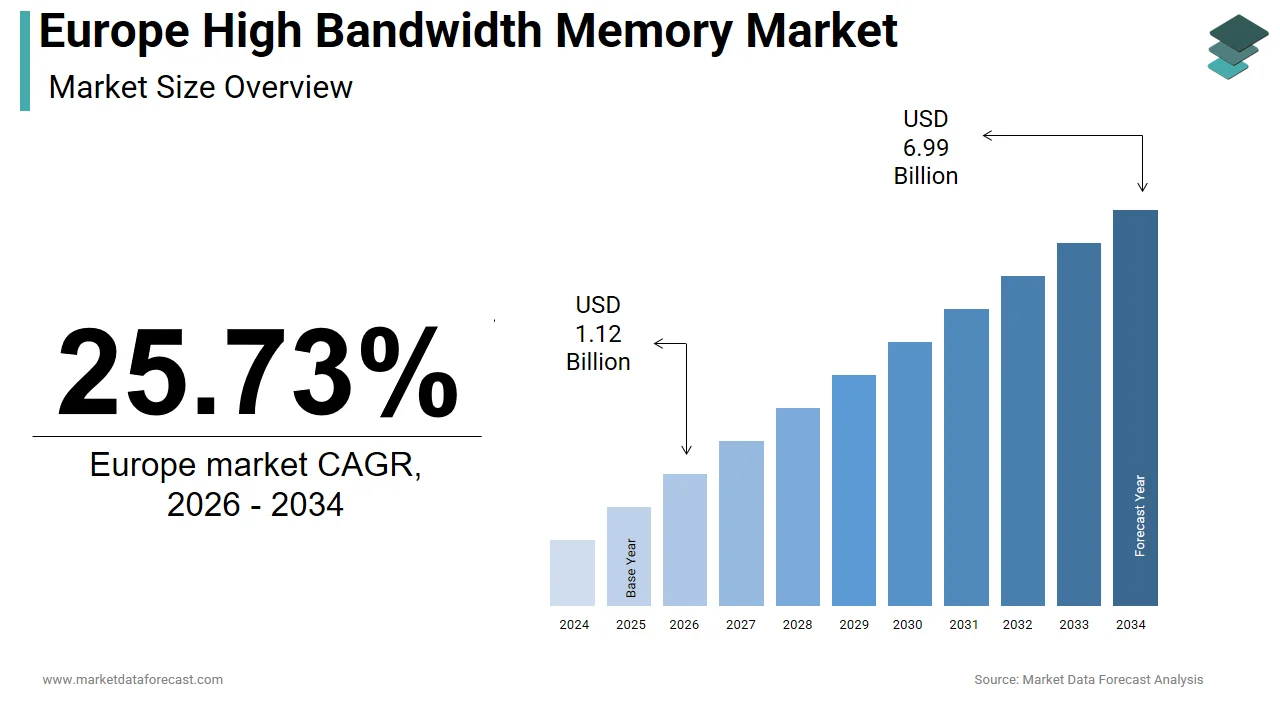

The Europe high bandwidth memory (HBM) market was valued at USD 0.89 billion in 2025, is estimated to reach USD 1.12 billion in 2026, and is projected to reach USD 6.99 billion by 2034, growing at a CAGR of 25.73% from 2026 to 2034. Market growth is driven by the increasing demand for high-performance computing, rapid expansion of data centers, and growing adoption of AI, machine learning, and advanced graphics applications. High bandwidth memory offers superior speed, energy efficiency, and data processing capabilities, making it essential for next-generation computing systems. The rising need for efficient memory solutions in cloud computing, gaming, and enterprise workloads is further accelerating market growth across Europe.

Key Market Trends

- Rising demand for high-performance computing and AI workloads.

- Rapid expansion of data centers and cloud infrastructure.

- Increasing adoption of advanced GPUs and accelerators.

- Growing use of HBM in gaming, AI, and scientific computing.

- Advancements in memory architecture and semiconductor technologies.

Segmental Insights

- Based on type, the graphics processing units (GPUs) segment dominated the Europe high bandwidth memory market in 2025, driven by increasing demand for high-speed processing in AI and graphics applications.

- Based on application, the data centers segment led the market by capturing 55.7% share in 2025, supported by the rapid growth of cloud computing and enterprise data workloads.

Regional Insights

The Europe high bandwidth memory market is witnessing strong growth across major countries due to increasing digitalization and demand for advanced computing technologies.

- Germany led the regional market in 2025 with 26.8% share, supported by strong industrial and technological capabilities.

- France followed with 18.4% share in 2025, driven by growing investments in AI, research, and data infrastructure.

- The United Kingdom holds a significant position due to its strong academic research ecosystem, fintech sector, and life sciences innovation.

Competitive Landscape

The Europe high bandwidth memory market is highly competitive, with the presence of leading semiconductor manufacturers and technology companies. Market players are focusing on innovation, improving memory performance, and expanding production capabilities. Strategic partnerships, R&D investments, and advancements in chip design are shaping competitive dynamics across the region.

Prominent companies operating in the Europe high bandwidth memory market include SK Hynix Inc., Micron Technology, Inc., Samsung Electronics Co., Ltd., Advanced Micro Devices, Inc. (AMD), NVIDIA Corporation, Intel Corporation, Broadcom Inc., Texas Instruments Inc., Xilinx, Inc., and Qualcomm Incorporated.

Europe High Bandwidth Memory Market Size

The Europe high bandwidth memory market was valued at USD 0.89 billion in 2025, is estimated to reach USD 1.12 billion in 2026, and is projected to reach USD 6.99 billion by 2034, growing at a CAGR of 25.73% from 2026 to 2034.

High Bandwidth Memory (HBM) is a high-performance and 3D-stacked DRAM technology designed for massive data transfer speeds at lower power, essential for AI accelerators and high-performance GPUs. This technology serves as the critical backbone for high performance computing, artificial intelligence accelerators, and graphics processing units that power the continent's digital transformation. Unlike traditional memory architectures, high bandwidth memory utilizes through silicon vias to create a wide interface, enabling terabytes per second of throughput essential for complex computational tasks. The European landscape is uniquely defined by its strong presence in industrial automation, automotive research, and scientific supercomputing rather than mass consumer electronics manufacturing. According to Eurostat, the information and communication technology (ICT) sector within the European Union employed approximately 7.2 million people in 2022, while the total number of ICT specialists across the economy reached 9.8 million in 2023, driven by growth in data-intensive industries. Furthermore, the European Commission's Digital Decade policy programme sets a target for 75% of EU enterprises to adopt at least one of three key technologies, cloud computing, big data analytics, or artificial intelligence (AI), by 2030, a goal that necessitates massive upgrades in server infrastructure to handle exponential data growth. Data from the EuroHPC Joint Undertaking (EuroHPC JU) confirms that the region hosts some of the world's most powerful supercomputers, including the LUMI system in Finland, Leonardo in Italy, and the exascale JUPITER system in Germany, which are primary consumers of high-bandwidth memory modules. This convergence of strategic digital sovereignty goals and existing high performance computing infrastructure positions Europe as a pivotal demand center for next generation memory technologies.

MARKET DRIVERS

Surge in Artificial Intelligence and Machine Learning Deployment

The rapid integration of generative artificial intelligence and machine learning models across European industries drives exponential demand for high throughput memory architectures.

The aggressive adoption of AI and machine learning accelerates the growth of the Europe high bandwidth memory market. These technologies are being deployed across diverse sectors ranging from automotive design to pharmaceutical research. Training large language models and running complex inference engines require memory subsystems capable of feeding massive datasets to processors without bottlenecks, a capability that only high bandwidth memory can provide at scale. According to the European Commission, venture capital investment in European artificial intelligence reached new heights recently, with funding totals reflecting a significant push for sovereign technological capabilities to compete globally. These initiatives rely heavily on graphics processing unit clusters equipped with high bandwidth memory to process unstructured data efficiently. Multiple studies project that spending on artificial intelligence solutions across the region will expand at a rapid compound annual rate through the end of the decade, driving a corresponding surge in the acquisition of high-performance server infrastructure. Furthermore, the automotive sector, a cornerstone of the European economy, is increasingly utilizing AI for autonomous driving development, which demands real time processing of sensor data streams. The European Automobile Manufacturers Association highlights that a major portion of new vehicle development is now centered on integrating advanced driver assistance systems that utilize sophisticated AI-driven processing. This widespread deployment ensures a sustained and growing requirement for high bandwidth memory as the foundational enabler of intelligent computation.

Expansion of Exascale Supercomputing Initiatives

Strategic government investments in exascale supercomputing infrastructure create a robust baseline demand for stacked memory technologies in scientific and industrial applications.

The effort by European nations to maintain global leadership in high-performance computing also contributes to the expansion of the Europe high bandwidth memory market. They are doing this by deploying exascale supercomputers under the EuroHPC Joint Undertaking. These monumental machines, designed to perform quintillions of calculations per second, are essential for climate modeling, materials science, and genomic research, all of which generate petabytes of data requiring ultra fast memory access. The EuroHPC Joint Undertaking has established a multi-billion euro investment program to develop a world-class supercomputing ecosystem, successfully deploying its first exascale system alongside a network of pre-exascale machines. Each of these supercomputers integrates thousands of accelerators that depend exclusively on high bandwidth memory to achieve their peak performance metrics. Research partnership data indicates that the utilization of these supercomputing facilities by both public and private sectors has grown substantially, reflecting a marked increase in complex computational workloads for science and industry. Additionally, the push for digital twins in manufacturing, supported by the European Green Deal, relies on these supercomputers to simulate complex industrial processes for energy optimization. Regional nations are rapidly upgrading their computing centers to exascale capabilities. This is driving exceptionally strong, resilient demand for high bandwidth memory modules that defies consumer market trends.

MARKET RESTRAINTS

Limited Domestic Manufacturing Capacity for Advanced Packaging

The scarcity of local fabrication facilities capable of producing advanced 2.5D and 3D integrated circuits constrains supply security and increases dependency on imports.

Limited domestic manufacturing capacity for advanced packaging technologies slows down the growth of the Europe high bandwidth memory market. Specifically, this involves 2.5D and 3D integration, which are essential for assembling high-bandwidth memory stacks. Europe possesses strong capabilities in chip design and equipment manufacturing. However, the assembly of high-bandwidth memory requires specialized foundries, which are currently concentrated almost entirely in Asia. The geographic disconnect creates vulnerabilities in the supply chain, as evidenced by recent global logistics disruptions that delayed the delivery of critical components to European data center builders. Although the European Chips Act aims to boost local production, the construction of advanced packaging facilities requires years of lead time and billions in capital expenditure. Market constraints from external supply will persist until domestic capabilities are operational. Consequently, European system integrators face challenges in securing volumes and favorable pricing.

Prohibitive Costs and Thermal Management Complexities

The exorbitant price premium of high bandwidth memory and the intense thermal density associated with its operation hinder widespread adoption beyond niche high-end applications.

The prohibitively high cost of high-bandwidth memory compared to conventional double data rate memory further restricts the expansion of the Europe high bandwidth memory market. Furthermore, this technology presents severe thermal management challenges. The complex manufacturing process involving precise die stacking and through silicon via formation results in a price point that can be higher than standard memory solutions, making it economically unviable for many mid range enterprise servers and edge devices. According to sources, the cost per gigabyte of high bandwidth memory remains a significant barrier for small and medium sized enterprises in Europe looking to upgrade their IT infrastructure. Furthermore, the high density of power consumption in stacked memory arrays generates substantial heat that requires sophisticated and expensive cooling solutions, such as liquid immersion or direct to chip cooling, which many existing European data centers are not equipped to handle. The combined burden of higher upfront hardware costs and the necessity for extensive facility retrofits slows down the adoption rate, restricting the market largely to hyperscalers and government funded supercomputing projects while excluding a vast segment of potential commercial users.

MARKET OPPORTUNITIES

Emergence of Sovereign AI Cloud Infrastructure

The development of independent European artificial intelligence cloud platforms offers a transformative opportunity to localize demand and reduce reliance on non-European tech giants.

Building sovereign AI cloud infrastructure is a paramount opportunity for the European High Bandwidth Memory market. This initiative would operate independently of U.S. and Asian hyperscalers. The European Union is actively fostering the creation of homegrown cloud ecosystems, such as Gaia X, to ensure data sovereignty and provide secure environments for training sensitive AI models, which will necessitate the deployment of vast amounts of high performance computing resources. According to the European Commission, several member states have announced plans to invest billions in constructing AI factories dedicated to training large scale models for public sector and industrial use cases. These dedicated facilities will require thousands of graphics processing units and tensor processing units, all of which mandate high bandwidth memory for optimal performance, creating a guaranteed and localized demand stream. As these sovereign clouds come online, they will act as anchor tenants for high bandwidth memory suppliers, encouraging them to establish stronger logistical and technical support networks within the region. This shift towards digital autonomy not only secures supply but also stimulates innovation in memory optimized architectures tailored specifically for European regulatory and industrial needs.

Integration in Next Generation Automotive Electronics

The evolution of software defined vehicles and autonomous driving systems presents a lucrative avenue for deploying high bandwidth memory in embedded automotive domains.

The rapid evolution of the automotive sector towards software defined vehicles and higher levels of autonomy presents a substantial opportunity for the integration of HBM directly into vehicle electronic architectures. This evolution is anticipated to boost the expansion of the Europe high bandwidth memory market. As cars become rolling data centers processing inputs from lidar, radar, and high resolution cameras in real time, the bandwidth requirements for onboard computers are skyrocketing beyond the capabilities of traditional automotive memory. Several European original equipment manufacturers and tier one suppliers are already prototyping central compute platforms that incorporate high bandwidth memory to handle neural network inference for object detection and path planning. The transition opens a completely new vertical for high bandwidth memory beyond data centers, offering manufacturers a chance to diversify their customer base into the high volume automotive market. High bandwidth memory is poised to become a standard requirement in vehicles, driven by evolving safety mandates for faster processing. This transition is fueling significant volume growth.

MARKET CHALLENGES

Geopolitical Fragmentation and Export Control Volatility

Escalating geopolitical tensions and shifting export control regimes create an environment of uncertainty that disrupts long-term supply planning and technology access.

The increasing volatility caused by geopolitical fragmentation and the imposition of stringent export controls on advanced semiconductor technologies by global powers is a major challenge confronting the Europe high bandwidth memory market. The trade restrictions enacted by the United States and countermeasures by China regarding high end chips and memory technologies create a complex web of compliance requirements that can abruptly alter supply chains and limit access to cutting edge nodes. According to research, the European Union finds itself caught between competing technological spheres, forcing companies to navigate conflicting regulations that may restrict the sale or purchase of high bandwidth memory components containing specific intellectual property or manufacturing equipment. The uncertainty makes it difficult for European system integrators to commit to long term roadmaps or secure multi year supply contracts, as the availability of specific high bandwidth memory generations could be jeopardized by sudden policy shifts. Furthermore, the risk of being excluded from certain global technology ecosystems threatens to isolate European innovators, potentially slowing down the pace of adoption and forcing costly redesigns of products to comply with varying national security mandates.

Acute Shortage of Specialized Engineering Talent

The critical deficit of engineers skilled in advanced memory architecture and heterogeneous integration hampers the effective deployment and optimization of high bandwidth memory systems.

An acute shortage of specialized engineering talent hinders the expansion of the Europe high bandwidth memory market. This shortage hampers the ability to design, integrate, and optimize systems utilizing advanced memory architectures. The complexity of high bandwidth memory, which involves intricate knowledge of signal integrity, thermal dynamics, and 3D stacking protocols, requires a highly skilled workforce that is currently in short supply across the continent. Universities and technical institutes often lag behind the rapid pace of technological advancement, failing to produce graduates with hands on experience in the latest memory interfaces and interconnect technologies. The talent barrier delays the time to market for new products and limits the ability of European firms to fully leverage the performance benefits of high bandwidth memory. The region must make a concerted effort to upskill its workforce and attract global talent. Without these actions, it risks falling behind in technology deployment, which will stifle growth and innovation.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Application, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | SK Hynix Inc., Micron Technology, Inc., Samsung Electronics Co., Ltd., Advanced Micro Devices, Inc. (AMD), NVIDIA Corporation, Intel Corporation, Broadcom Inc., Texas Instruments Inc., Xilinx, Inc., Qualcomm Incorporated, and Others. |

SEGMENTAL ANALYSIS

By Type Insights

The Graphics Processing Units (GPUs) segment dominated the Europe high bandwidth memory market and accounted for a substantial share in 2025. This dominance of the segment is driven by the insatiable demand for parallel processing power required to train large language models and render complex simulations, tasks where GPUs paired with high bandwidth memory are unmatched. The primary driver for GPU dominance is their indispensable role as the engine for generative artificial intelligence training, a sector experiencing explosive growth across European research institutions and technology firms. Training foundational models requires moving massive datasets between memory and processors at terabytes per second, a bottleneck that only the wide interface of high bandwidth memory integrated with GPUs can resolve. Furthermore, the emergence of sovereign AI initiatives in countries like France and Germany has led to the construction of dedicated supercomputers populated almost exclusively by GPU accelerators. The inability of other processor types to match the memory throughput required for deep learning ensures that GPUs remain the primary vehicle for high bandwidth memory consumption, solidifying their market supremacy. Next, this segment is strengthened by its widespread adoption in scientific simulation and the creation of digital twins for industrial applications, a key pillar of the European Green Deal. Industries ranging from automotive to pharmaceuticals rely on GPU accelerated computing to model fluid dynamics, molecular interactions, and manufacturing processes with extreme fidelity, all of which demand rapid access to vast memory pools. According to sources, a notable portion of the workloads running on the region's top supercomputers utilize GPU acceleration to achieve necessary performance levels. The EuroHPC Joint Undertaking has deployed multiple petascale and exascale systems specifically designed around GPU architectures to support these scientific endeavors. The unique ability of GPUs to handle thousands of concurrent threads while leveraging high bandwidth memory makes them the preferred choice for these complex calculations. European industries are doubling down on simulation to reduce physical prototyping and energy consumption. Consequently, reliance on GPU-based, high-bandwidth memory systems will continue to deepen.

The Application-Specific Integrated Circuits (ASICs) segment is expected to exhibit a noteworthy CAGR of 24.5% during the forecast period due to the shift towards customized silicon designed for specific AI inference tasks, offering superior energy efficiency and lower total cost of ownership compared to general purpose GPUs. The main reason for the explosive growth of ASICs is the urgent need for energy efficient hardware to perform artificial intelligence inference at the edge, where power constraints and latency requirements rule out bulky GPU solutions. As AI models move from training centers to deployment in factories, vehicles, and retail environments, specialized chips optimized for specific neural network architectures offer significantly better performance per watt. According to research, the market for edge AI processors in Europe is expected to expand significantly, driven by industries seeking to reduce operational costs and carbon footprints. Tech giants and European startups alike are designing custom ASICs that integrate high bandwidth memory to deliver the necessary throughput for real time decision making without the overhead of general purpose logic. The ability of ASICs to be tailored for specific algorithms allows for tighter integration with high bandwidth memory, maximizing bandwidth utilization. This trend towards specialization ensures that the ASIC segment will outpace general purpose processors as AI becomes ubiquitous in everyday European infrastructure. Following this, the segment is backed by the strategic push by European nations and corporations to develop sovereign and custom silicon designs to reduce dependency on foreign suppliers. The European Chips Act has incentivized the design and manufacture of application specific integrated circuits tailored for European needs in automotive, telecommunications, and secure communications. According to sources, several major projects funded under the Chips Act focus specifically on developing custom accelerators for 5G base stations and autonomous driving systems, all of which require high bandwidth memory for data intensive operations. Companies are increasingly opting for custom solutions that offer better security and control over their supply chain, rather than relying on off the shelf components. The maturity and volume production of custom designs are causing demand for ASIC-packaged high-bandwidth memory to surge. Consequently, this segment is expected to experience a growth rate significantly higher than the market average.

By Application Insights

In 2025, the data centers segment held the majority share of the 55.7% of the Europe high bandwidth memory market. This supremacy of the segment is credited to the massive consolidation of computing resources in hyperscale facilities that serve as the backbone for cloud services, artificial intelligence platforms, and enterprise data processing across the continent. The preeminence of the data center segment is fundamentally driven by the aggressive expansion of hyperscale cloud infrastructure in Europe to meet the soaring demand for compute capacity from digital enterprises and government bodies. These facilities house thousands of servers equipped with high performance accelerators that rely on high bandwidth memory to manage concurrent user requests and massive data flows. According to research, Europe added several new hyperscale data centers in 2023, with significant clusters located in Germany, the Netherlands, and France. Each of these facilities represents a massive deployment of high bandwidth memory modules to support the underlying graphics processing units and tensor processing units. The centralization of workloads in these giant facilities ensures that they remain the primary consumers of advanced memory technologies. As more European businesses migrate critical operations to the cloud to enhance agility and scalability, the density of high bandwidth memory within these data centers will continue to increase, securing their leading market position. This segment is also built up by the critical role they play in hosting and servicing generative artificial intelligence models, which require unprecedented memory bandwidth for low latency inference. Unlike traditional web hosting, serving large language models involves constant access to billions of parameters, a task that necessitates the high throughput provided by high bandwidth memory integrated into server accelerators. Major cloud providers operating in Europe are upgrading their fleets with the latest generation of AI servers specifically designed to leverage high bandwidth memory for optimal performance. The inability of standard memory architectures to meet the speed requirements of modern AI models forces data center operators to prioritize high bandwidth memory upgrades. This structural shift in workload characteristics ensures that data centers remain the largest and most dynamic application segment for high bandwidth memory in the region.

The High-performance Computing segment is predicted to witness the highest CAGR of 21.8% between 2026 and 2034 owing to the deployment of exascale supercomputers under the EuroHPC initiative and the increasing use of HPC for climate modeling, drug discovery, and materials science. The primary engine for the rapid expansion of the high-performance computing segment is the strategic deployment of exascale supercomputing systems across Europe, which represent the pinnacle of computational power and are heavily reliant on high bandwidth memory. These machines, capable of performing quintillions of calculations per second, utilize thousands of accelerators interconnected with high bandwidth memory to solve grand challenge problems in science and engineering. These systems are essential for maintaining Europe's competitiveness in scientific research and are funded by substantial public investments that guarantee steady demand. As more member states upgrade their national centers to exascale capabilities to participate in this shared infrastructure, the consumption of high bandwidth memory in the HPC sector will accelerate at a pace surpassing commercial data centers. A further point supporting this segment is the expanding use of industrial digital twin simulations to optimize manufacturing processes and accelerate product development cycles. European industries are increasingly leveraging HPC clusters to create virtual replicas of physical systems, allowing for real time monitoring and predictive analysis that requires immense data throughput and memory speed. The complexity of these simulations, which often involve multi physics modeling and large scale data sets, mandates the use of high bandwidth memory to prevent processing bottlenecks. The industrial metaverse is driving a surge in demand for high-bandwidth memory (HBM) in HPC, fueled by more detailed and frequent simulations. This makes it the fastest-growing application segment in the industry.

COUNTRY LEVEL ANALYSIS

Germany High Bandwidth Memory Market Analysis

Germany outperformed other countries in the Europe high bandwidth memory market and captured a 26.8% share in 2025. The nation's top-tier standing is supported by its position as Europe’s premier economy, supported by a dense concentration of automotive manufacturers, industrial giants, and world-class research institutions that fuel demand for advanced AI and high-performance computing capabilities. Germany's supremacy is fuelled by its robust industrial base which is rapidly adopting Industry 4.0 technologies and artificial intelligence to maintain global competitiveness. The country is home to major automotive original equipment manufacturers who are investing heavily in autonomous driving research, a field that relies extensively on high bandwidth memory for processing sensor data and training neural networks. Furthermore, Germany hosts some of Europe's most powerful supercomputers, such as those at the Jülich Supercomputing Centre, which serve as critical resources for scientific research and industrial simulation. The strong presence of semiconductor equipment manufacturers and a supportive government strategy under the National Semiconductor Strategy further reinforce Germany's position. This combination of industrial demand, scientific excellence, and strategic investment ensures Germany remains the primary engine for high bandwidth memory adoption in Europe.

France High Bandwidth Memory Market Analysis

France was the second largest country in the European market and occupied a share of 18.4% in 2025. This growth of the segment is driven by its ambitious sovereign artificial intelligence strategy, strong aerospace and defense sectors, and significant state-led investments in supercomputing infrastructure. France's strong market standing is largely attributable to its proactive government policies aimed at achieving technological sovereignty in artificial intelligence and high performance computing. The French government has launched the "AI for Humanity" plan and committed billions of euros to build AI factories and upgrade national supercomputing capabilities, creating a guaranteed demand stream for high bandwidth memory. According to studies, the country aims to become a global leader in trusted AI, with specific funding allocated for the development of large language models and secure cloud infrastructure. The aerospace and defense industry, led by giants like Airbus and Thales, also contributes significantly to demand, utilizing high performance computing for complex simulations in aerodynamics and cryptography. Additionally, France is a key partner in the EuroHPC initiative, hosting several major supercomputing sites that require state of the art memory technologies. This concerted effort to build a sovereign digital ecosystem, combined with a strong industrial base, positions France as a critical hub for high bandwidth memory consumption in Europe.

United Kingdom High Bandwidth Memory Market Analysis

The United Kingdom is also a key player in the Europe high bandwidth memory market due to its world leading academic research institutions, vibrant fintech sector, and strong presence in life sciences and pharmaceutical research. The UK's market strength is underpinned by its exceptional capability in artificial intelligence research and development, fostered by prestigious universities and a dynamic startup ecosystem that pushes the boundaries of computational science. The country is home to DeepMind and numerous AI labs that are at the forefront of developing advanced machine learning models, driving substantial demand for high performance computing resources equipped with high bandwidth memory. The life sciences sector, a cornerstone of the UK economy, also relies heavily on high performance computing for genomic sequencing and drug discovery, applications that are memory intensive. Furthermore, the presence of major cloud provider regions in the UK ensures local access to the latest hardware technologies. This blend of academic excellence, industrial application, and financial support ensures the UK remains a pivotal market for high bandwidth memory technologies.

Netherlands High Bandwidth Memory Market Analysis

The Netherlands experienced a consistent growth in the European market owing to its status as a major data center hub for Europe, strong semiconductor equipment industry, and advanced digital infrastructure. The Netherlands' significant market presence is driven by its strategic position as the digital gateway to Europe, hosting a disproportionately large number of hyperscale data centers that serve the entire continent. Cities like Amsterdam and Groningen have become major clusters for cloud providers due to excellent connectivity and favorable business conditions, leading to high concentrations of servers utilizing high bandwidth memory. The country is also home to ASML, the world's leading supplier of lithography equipment, which fosters a strong ecosystem of semiconductor innovation and awareness of cutting edge memory technologies. Besides, the Dutch government's focus on digitizing public services and supporting smart port logistics in Rotterdam creates further demand for high performance computing. This unique combination of being a physical hub for data storage and a center for semiconductor technology ensures the Netherlands maintains a strong and growing share of the market.

Italy High Bandwidth Memory Market Analysis

Italy is likely to expand notably in the European market from 2026 to 2034 its growing investment in supercomputing, strong manufacturing sector undergoing digital transformation, and active participation in European joint undertakings for high performance computing. Its market trajectory is influenced by its strategic investments in high performance computing infrastructure, positioning itself as a key player in the European scientific landscape. The country hosts the Leonardo supercomputer, one of the most powerful in the world, which serves as a magnet for research projects requiring massive memory bandwidth for climate modeling and energy research. The manufacturing sector, particularly in the north of Italy, is increasingly adopting digital twin technologies and AI driven quality control systems, driving demand for edge and cloud computing resources. Furthermore, Italy's active role in the EuroHPC Joint Undertaking ensures continued access to and investment in next generation computing resources. This commitment to leveraging high performance computing for scientific and industrial advancement ensures Italy remains a vital and growing market for high bandwidth memory in Southern Europe.

COMPETITIVE LANDSCAPE

The competition in the Europe high bandwidth memory market is characterized by intense rivalry among a select group of global multinational corporations that dominate the landscape due to extremely high barriers to entry and proprietary manufacturing technologies. Established players leverage their extensive fabrication networks and decades of expertise in advanced packaging to secure long term supply agreements with major European hyperscalers and automotive manufacturers. The market is highly consolidated with few competitors possessing the necessary resources to conduct costly research and development cycles required for next generation stacked memory nodes. Innovation focuses heavily on increasing bandwidth density reducing power consumption and improving thermal performance to meet the rigorous demands of artificial intelligence workloads. Companies differentiate themselves through comprehensive technical support offerings including co design services and localized engineering teams that ensure optimal integration for European clients. Strategic alliances between memory makers and processor designers are critical for validating new standards and accelerating time to market. The competitive dynamic is further shaped by the urgent need for supply chain resilience which drives customers to multi source strategies while demanding guaranteed volumes. This environment fosters continuous technological advancement while limiting the ability of new entrants to gain significant footholds without massive capital investment or breakthrough intellectual property.

KEY MARKET PLAYERS

The leading companies operating in the Europe high bandwidth memory market include:

- SK Hynix Inc.

- Micron Technology, Inc.

- Samsung Electronics Co., Ltd.

- Advanced Micro Devices, Inc. (AMD)

- NVIDIA Corporation

- Intel Corporation

- Broadcom Inc.

- Texas Instruments Inc.

- Xilinx, Inc.

- Qualcomm Incorporated

TOP PLAYERS IN THE MARKET

- Samsung Electronics Co Ltd stands as a global pioneer in memory semiconductor technology with a profound impact on the Europe high bandwidth memory landscape through its advanced stacking solutions. The company contributes significantly to the global market by mass producing next generation high bandwidth memory modules that power artificial intelligence accelerators and supercomputers worldwide. Recently Samsung has strengthened its position by collaborating with major European cloud providers and research institutions to validate its latest high bandwidth memory generations for exascale computing applications. The firm actively invests in expanding its packaging capabilities to meet the surging demand from European data centers and automotive sectors. These strategic initiatives ensure their technology remains at the forefront of performance and energy efficiency while addressing the critical supply needs of the continent's digital infrastructure.

- SK Hynix Inc operates as a leading innovator in high bandwidth memory with a dominant presence in the European market particularly within the artificial intelligence and high performance computing segments. The company contributes globally by being the first to commercialize advanced high bandwidth memory specifications that enable breakthrough performance for graphics processing units. Their recent actions to solidify market presence include securing long term supply agreements with key European original equipment manufacturers and establishing technical support centers in Germany to assist local clients. SK Hynix has also invested heavily in increasing production capacity for its most advanced stacked memory products to alleviate global shortages. The firm frequently engages in joint development projects with European semiconductor designers to optimize memory interfaces for custom silicon. By focusing on yield improvement and technological leadership SK Hynix enhances reliability for mission critical applications. These efforts demonstrate their commitment to driving innovation and maintaining supremacy in the competitive European high bandwidth memory arena.

- Micron Technology Inc is a specialized memory and storage solutions provider that has established itself as a key player in the European market through its focus on high performance computing and data center applications. The company makes a substantial global contribution by delivering scalable high bandwidth memory portfolios that support diverse workloads from machine learning to scientific simulation. Their recent strategy to strengthen their European position involves launching new high bandwidth memory products tailored for sustainability and energy efficiency which align with strict European environmental regulations. Micron has also expanded its collaboration network with European universities and supercomputing centers to foster research into next generation memory architectures. The firm continues to invest in advanced packaging facilities to ensure a resilient supply chain for its European customers. By maintaining a dedicated focus on performance per watt and thermal management Micron addresses the evolving needs of modern data centers. Their persistent innovation in memory density and speed ensures they remain a vital partner for industries seeking cutting edge computational power.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe high bandwidth memory market predominantly employ strategic capacity expansion and technological collaboration to secure supply chains and meet escalating regional demand for artificial intelligence hardware. Companies frequently invest billions in constructing new advanced packaging facilities specifically for three dimensional stacked memory to support the electric vehicle and cloud computing sectors. Another major strategy involves forming deep collaborative partnerships with European original equipment manufacturers and research consortia to co develop customized memory solutions that address specific application requirements like exascale computing. Market participants also focus heavily on acquiring innovative startups specializing in thermal management or interconnect technologies to rapidly enhance their product portfolios. Investment in research and development remains a cornerstone strategy as firms strive to achieve breakthroughs in bandwidth density and energy efficiency. Additionally, companies pursue diversification of their manufacturing locations to mitigate geopolitical risks and ensure production continuity for European clients. These combined approaches allow industry leaders to navigate complex regulatory environments while maintaining a competitive edge in this rapidly evolving technological sector.

MARKET SEGMENTATION

This research report on the Europe high bandwidth memory market has been segmented and sub-segmented into the following categories.

By Type

- Graphics Processing Units (GPUs)

- Central Processing Units (CPUs)

- Field-Programmable Gate Arrays (FPGAs)

- Application-Specific Integrated Circuits (ASICs)

By Application

- Graphics

- High-performance Computing

- Networking

- Data Centers

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe high bandwidth memory market?

The Europe high bandwidth memory market supplies 3D-stacked DRAM for AI, HPC, and automotive applications. Germany leads R&D; UK excels in AI supercomputing and hyperscaler deployments.

How does the Europe high bandwidth memory market function?

The Europe high bandwidth memory market functions through silicon-interposer integration, TSV manufacturing, and JEDEC standardization. Module assembly serves GPU/AI chip makers and data centers.

What drives growth in the Europe high bandwidth memory market?

AI training demands, automotive ADAS expansion, and HPC supercomputing propel the Europe high bandwidth memory market. EU semiconductor sovereignty initiatives accelerate domestic adoption.

Which countries lead the Europe high bandwidth memory market?

Germany dominates the Europe high bandwidth memory market via automotive/semiconductor ecosystems. UK, France follow with AI research and data center investments.

What generations define the Europe high bandwidth memory market?

HBM3 and HBM3E define the Europe high bandwidth memory market, offering superior bandwidth for next-gen GPUs. HBM2E remains prevalent in transitional AI deployments.

What applications shape the Europe high bandwidth memory market?

AI accelerators and GPUs shape the Europe high bandwidth memory market, alongside HPC clusters and automotive processors. Data center inference drives volume demand.

How does regulation influence the Europe high bandwidth memory market?

EU Chips Act funding and export controls govern the Europe high bandwidth memory market, promoting domestic fabs while restricting advanced node technology transfers.

What trends affect the Europe high bandwidth memory market?

HBM4 development, co-packaged optics integration, and CXL memory pooling transform the Europe high bandwidth memory market. Automotive-qualified HBM gains traction.

What challenges face the Europe high bandwidth memory market?

Supply chain concentration, thermal management limits, and yield challenges confront the Europe high bandwidth memory market. EU fabs lag Asia in volume production.

How has AI impacted the Europe high bandwidth memory market?

AI training/inference workloads exploded demand for the Europe high bandwidth memory market, particularly HBM3 modules. UK supercomputers exemplify large-scale deployments.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com