Europe Plastic Injection Molding Market Size, Share, Trends & Growth Forecast Report Segmented By Raw Material Type (Polypropylene, Acrylonitrile Butadiene Styrene, Polystyrene, Polyethylene, Polyvinyl Chloride, Others, Application, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe), Industry Analysis From 2026 To 2034

Europe Plastic Injection Molding Market Report Summary

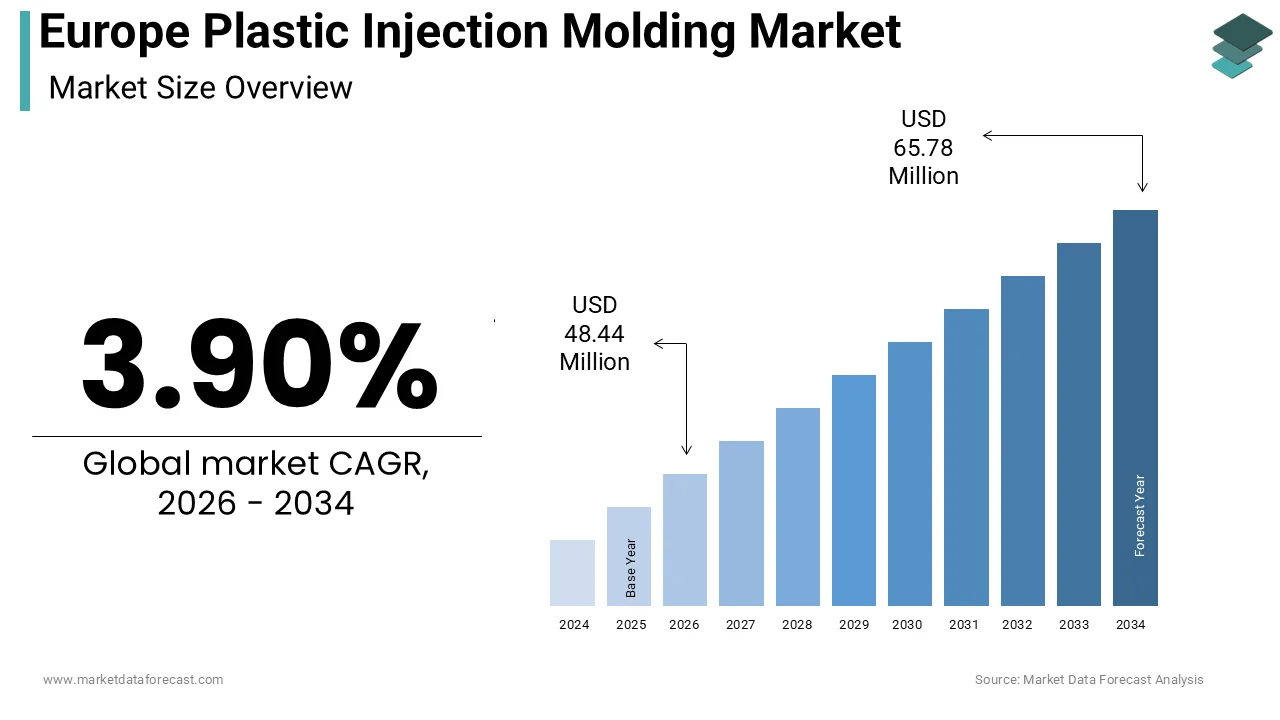

The Europe plastic injection molding market was valued at USD 46.62 million in 2025 and is projected to reach USD 65.78 million by 2034, growing from USD 48.44 million in 2026 at a CAGR of 3.90% during the forecast period. Market growth is driven by increasing demand for lightweight, durable, and cost-effective plastic components across automotive, packaging, healthcare, and consumer goods industries. The rising adoption of advanced manufacturing technologies and automation is further supporting the growth of the Europe plastic injection molding market.

Key Market Trends

- Increasing demand for lightweight plastic components in automotive applications

- Growth in packaging industry and sustainable plastic solutions

- Rising adoption of precision molding and automation technologies

- Expansion of healthcare and medical device applications

- Increasing focus on recyclable and bio-based plastics

Segmental Insights

- Based on raw material type, the polypropylene segment dominated the Europe plastic injection molding market in 2025 by accounting for 28.5% of the regional market share, driven by its versatility, durability, and cost-effectiveness

- Based on application, the packaging segment led the market in 2025 by capturing 35.6% of the total market share, supported by increasing demand for consumer goods and food packaging

Regional Insights

- Germany led the Europe plastic injection molding market in 2025 by holding 26.3% of the regional market share, supported by strong automotive and manufacturing industries

- Italy ranked second with 18.1% share in 2025, driven by industrial production and manufacturing activities

- France holds a significant share, supported by aerospace, automotive, and healthcare sectors

- United Kingdom is witnessing steady growth due to demand from the packaging and healthcare industries

- Spain is anticipated to expand significantly during the forecast period, driven by packaging and the automotive sector growth

Competitive Landscape

- The Europe plastic injection molding market is highly competitive, with companies focusing on material innovation, automation, and sustainable manufacturing practices. Market players are investing in advanced molding technologies and recyclable materials to meet regulatory and environmental requirements.

- Prominent players in the Europe plastic injection molding market include BASF SE, Covestro AG, LyondellBasell Industries N.V, INEOS Group, SABIC, Arkema S.A, Evonik Industries AG, Solvay S.A, Röchling Group, Faurecia SE, Magna International Inc, Plastic Omnium, Engel Austria GmbH, Arburg GmbH + Co. KG, and Husky Injection Molding Systems Ltd.

Europe Plastic Injection Molding Market Size

The Europe plastic injection molding market size was calculated to be USD 46.62 million in 2025 and is anticipated to be worth USD 65.78 million by 2034, from USD 48.44 million in 2026, growing at a CAGR of 3.90% during the forecast period.

Plastic Injection Molding is a mass-manufacturing process used to produce large volumes of identical plastic parts. This process involves injecting molten thermoplastic or thermosetting polymers into a mold cavity where they cool and solidify into the desired shape. The technology is indispensable for producing complex geometries with tight tolerances required in automotive, medical device,s consumer goods, and packaging sectors. As per Plastics Europe and Eurostat data from 2024/2025, the European Union's plastic production reached approximately 52 million tonnes, with injection molding remaining a primary processing technique despite a 13% decrease in sector turnover since 2022. The region’s robust industrial base, particularly in Germany, Italy, and France, supports advanced manufacturing capabilities driven by automation and digitalization. Under the European Commission's Packaging and Packaging Waste Regulation (PPWR), all plastic packaging placed on the EU market must be recyclable in an economically viable way by 2030, with specific reuse targets applied to high-volume categories to drive material circularity. Furthermore, the International Energy Agency (IEA) indicates that the industrial sector accounts for nearly 40% of global energy consumption, a pressure point that is accelerating the adoption of high-efficiency electric motors and energy-optimized injection molding machinery across Europe. The integration of Industry 4.0 technologies, such as real-time monitoring and predictive maintenance, enhances operational efficiency and reduces waste. These technological advancements, coupled with stringent environmental regulations, define the current operational framework. The market is increasingly shifting towards sustainable practice,s including the use of bio-based polymers and recycled materials to align with the European Green Deal objectives. This transition necessitates significant investment in new machinery and process optimization to maintain competitiveness while adhering to evolving regulatory standards.

MARKET DRIVERS

Robust Automotive Sector Demand for Lightweight Components Accelerates Market Growth

The automotive industry remains a key growth enabler for the Europe plastic injection molding market. This is due to the increasing demand for lightweight components that enhance fuel efficiency and reduce emissions. Based on data from Plastics Europe, the average modern car contains between 150 and 200 kilograms of plastic materials, which represents approximately 12 to 15 percent of the total vehicle weight. This usage is supported by the need to meet stringent CO2 emission targets set by the European Union, which mandate a 55 percent reduction in emissions for new cars by 2030 compared to 2021 levels. Injection molding enables the production of complex interior parts, exterior trim, and under-the-hood components with high precision and consistency. For instance, dashboard assemblies, door panels, and bumpers are predominantly manufactured using this technique due to its ability to integrate multiple functions into single parts. The shift towards electric vehicles further amplifies this demand as manufacturers seek to offset the weight of heavy battery packs. The International Energy Agency (IEA) indicates that global electric car sales increased by 35 percent in 2023 (OR: Data from the European Automobile Manufacturers’ Association indicates that new battery-electric car registrations in the EU increased by 37 percent in 2023), driving demand for specialized plastic components for battery housings and charging infrastructure. Additionally, the trend towards autonomous driving systems necessitates the integration of sensors and cameras, which are housed in intricately molded plastic casings. The ability of injection molding to produce high-volume parts with minimal post-processing makes it cost-effective for automotive suppliers. Thus, the continuous evolution of automotive design and regulatory pressure for sustainability sustains a strong demand for advanced injection molding services across the region.

Expansion of the Medical Device Industry Drives Precision Manufacturing Requirements

The rapid proliferation of the medical device industry in the region greatly boosts the expansion of the Europe plastic injection molding market. This is because of the critical need for high precision and sterile components. MedTech Europe demonstrates that the medical technology sector is a cornerstone of the regional economy, representing a multi-billion euro market. The industry supports a vast workforce across thousands of companies, the majority of which are small and medium-sized enterprises. This sector remains a primary driver of innovation and high-value employment within the healthcare ecosystem. Plastic injection molding is essential for producing disposable medical devices such as syringes, IV connectors, surgical instruments, and diagnostic equipment housings. Official demographic data from Eurostat emphasizes a consistent upward trend in the proportion of the population reaching retirement age and beyond. This structural shift in the European population continues to increase the clinical demand for chronic disease management, long-term care solutions, and advanced diagnostic tools provided by the medical technology industry. This demographic shift increases the prevalence of chronic diseases requiring regular medical interventions and thus boosts the consumption of single-use plastic medical products. Furthermore, theCOVID-199 pandemic highlighted the importance of resilient supply chains for medical supplies, leading to increased domestic production capabilities. The European Medicines Agency has streamlined approval processes for critical medical devices, encouraging innovation and faster market entry. Injection molding offers the advantage of producing components with tight tolerances and smooth surfaces that minimize bacterial growth, ensuring patient safety. Materials such as polypropylene and polycarbonate are widely used due to their biocompatibility and ability to withstand sterilization processes. The European Commission and regional trade bodies report that Europe remains a global leader in the trade of medical instruments and apparatus. Driven by a reputation for rigorous safety standards and advanced manufacturing, European-produced medical devices are a significant export commodity, experiencing steady growth in international markets outside the trade bloc. Therefore, the growing healthcare needs and regulatory support for medical innovation drive sustained demand for precision injection molding services.

MARKET RESTRAINTS

Stringent Environmental Regulations Increase Compliance Costs and Operational Complexity

Strict environmental regulations imposed by the European Union pose a significant hindrance to the Europe plastic injection molding market. These rules increase compliance costs and operational complexity. The European Green Deal and the Circular Economy Action Plan mandate significant reductions in plastic waste and promote the use of recycled materials. The European Environment Agency (EEA) and Eurostat indicate that while plastic recycling rates have improved over the last decade, a significant portion of collected plastic waste still bypasses the circular economy through incineration or landfilling. This reality creates pressure on manufacturers to align with the European Commission's circularity goals, which mandate increased levels of recycled content in new products. Manufacturers are required to adhere to the Single Use Plastics Directive, which bans certain plastic products and imposes extended producer responsibility schemes. These regulations necessitate substantial investments in new technologies and processes to handle recycled materials, which often have different flow characteristics and thermal properties compared to virgin plastics. For instance, the integration of post-consumer recycled PCR content requires advanced filtration and compounding systems to ensure product quality. The European Commission notes that the implementation of the Packaging and Packaging Waste Regulation (PPWR) presents a complex administrative challenge for smaller firms. These businesses must invest in new material tracking systems and redesign products to meet strict recyclability standards, which can place a strain on their financial resources compared to larger competitors. Additionally, the Carbon Border Adjustment Mechanism introduces costs for carbon-intensive materials, affecting the overall cost structure of plastic production. Companies must also invest in energy-efficient machinery to reduce their carbon footprint, which involves high capital expenditure. The German Federal Ministry for Economic Affairs and Climate Action notes that energy prices in Europe remain volatile, impacting the profitability of energy-intensive manufacturing processes. These regulatory and financial burdens constrain the flexibility of manufacturers and slow down market growth, particularly for smaller players who lack the resources to adapt quickly.

Volatility in Raw Material Prices and Supply Chain Disruptions Impact Profitability

The volatility in raw material prices and ongoing supply chain disruptions are major constraints to the Europe plastic injection molding market. Plastic resins such as polyethylene, polypropylene, and polystyrene are derived from crude oil and natural gas making their prices highly susceptible to geopolitical tensions and market fluctuations. This price instability makes it difficult for manufacturers to predict costs and maintain stable pricing for their customers. Many injection molding companies operate on thin margins, and sudden spikes in resin prices can erode profitability significantly. For example, small manufacturers often lack the bargaining power to negotiate long-term contracts with suppliers, leaving them exposed to spot market volatility. Additionally, the reliance on imported raw materials exposes the European market to global supply chain risks. The Joint Research Centre of the European Commission highlights that Europe depends on imports for a significant portion of its polymer precursors. Disruptions in shipping lanes or political instability in supplier regions can lead to material shortages and production delays. The COVID-19 pandemic exposed these vulnerabilities, causing widespread delays in component delivery. Although supply chains have stabilized, recent geopolitical conflicts continue to pose risks. The International Monetary Fund reports that global trade fragmentation could further exacerbate supply chain inefficiencies. Hence, the uncertainty in raw material availability and pricing creates a challenging operating environment for injection molding companies, hindering their ability to plan and invest in future growth.

MARKET OPPORTUNITIES

Adoption of Biodegradable and Bio-Based Polymers Opens New Market Avenues

The increasing adoption of biodegradable and bio-based polymers provides major chances for the growth of the Europe plastic injection molding market as consumers and regulators demand sustainable alternatives. Projections from European Bioplastics indicate a significant surge in global and regional production capacity for biopolymers. This expansion is heavily influenced by the European Union's legislative frameworks, such as the Packaging and Packaging Waste Regulation (PPWR), which incentivizes the use of renewable feedstocks. Growing consumer awareness regarding environmental sustainability is further accelerating the transition from traditional fossil-based resins to bio-based and biodegradable alternatives. Injection molding companies that invest in processing these innovative materials can differentiate themselves and capture new market segments. Bio-based polymers such as polylactic acid PLA and polyhydroxyalkanoates PHA offer similar mechanical properties to conventional plastics but with a lower environmental footprint. These materials are increasingly used in packaging consumer goods and agricultural applications. The European Commission’s Bioeconomy Strategy supports the development of sustainable biological resources, encouraging innovation in material science. Companies that develop expertise in processing bio-based materials can partner with brands seeking to enhance their sustainability credentials. Furthermore, advancements in polymer chemistry are improving the heat resistance and durability of bio-based plastics, expanding their application range. The ability to mold these materials using existing infrastructure with minor modifications lowers the barrier to entry. So, the shift towards circular economy principles creates lucrative opportunities for manufacturers who can provide eco-friendly molding solutions.

Integration of Industry 4.0 Technologies Enhances Efficiency and Customization

The integration of Industry 4.0 technologies such as Internet of Things IoT artificial intelligence, and big data analytics offers substantial opportunities for enhancing efficiency and customization in the Europe plastic injection molding market. The European Commission emphasizes that the integration of Industry 4.0 technologies, such as the Internet of Things (IoT) and advanced data analytics, is essential for the long-term competitiveness of the European manufacturing base. These digital tools enable "smart" factories to achieve significant gains in operational efficiency, optimize energy consumption, and implement predictive maintenance schedules that prevent costly downtime. Smart injection molding machines equipped with sensors can monitor parameters such as temperature, pressure, and cycle time in real time, enabling predictive maintenance and minimizing downtime. This data-driven approach allows manufacturers to optimize process parameters for better quality and reduced waste. For example, Siemens and Bosch Rexroth have developed digital solutions that enable remote monitoring and control of injection molding operations. These technologies facilitate mass customization, allowing manufacturers to produce small batches of customized parts economically. Additionally, digital twins can simulate the molding process before production, reducing trial and error and accelerating time to market. The ability to offer rapid prototyping and flexible production runs appeals to industries such as medical devices and consumer electronics, where product life cycles are short. Furthermore, cloud-based platforms enable collaboration between designers, manufacturers, and customers enhancing supply chain transparency. Consequently, the adoption of Industry 4.0 technologies empowers injection molding companies to improve operational efficiency, reduce costs, and meet the growing demand for personalized products.

MARKET CHALLENGES

High Energy Consumption and Rising Utility Costs Strain Operational Budgets

High energy consumption and rising utility costs are a major challenge for the Europe plastic injection molding market. Because the process is inherently energy-intensive, these costs threaten profitability. Injection molding machines require significant amounts of electricity to melt plastic resins and operate hydraulic or electric drives. According to the International Energy Agency, the industrial sector in Europe faces some of the highest energy prices globally due to geopolitical tensions and the transition away from fossil fuels. The International Energy Agency (IEA) confirms that European manufacturers operate in a high-cost environment compared to international competitors. Geopolitical shifts have forced a transition to more expensive energy sources, creating a structural price disadvantage for energy-intensive processes like plastic molding. This surge in energy costs directly impacts the profitability of injection molding companies, which operate on narrow margins. Small and medium-sized enterprises are particularly vulnerable as they lack the financial resources to invest in energy-efficient technologies. European Plastic Converters (EuPC) indicates that energy expenditures now represent a substantial and volatile portion of a manufacturer's total operating budget. This increased financial burden limits the capital available for reinvestment in new machinery or sustainable material transitions. To mitigate this challenge, companies must invest in modern all-electric injection molding machines which are more energy efficient than traditional hydraulic models. However, the high upfront cost of these machines poses a financial barrier. Additionally, the variability in energy supply due to renewable energy integration can disrupt production schedules. While the German Federal Network Agency (Bundesnetzagentur) maintains high current reliability standards, industry groups express concern over long-term price stability and infrastructure readiness as the continent shifts toward intermittent renewable energy. Therefore, managing energy costs and ensuring reliable power supply remain critical challenges that threaten the competitiveness of the European injection molding industry.

Shortage of Skilled Labor Impedes Technological Adoption and Productivity

The shortage of skilled labor is a persistent challenge for the European plastic injection molding market. This hinders the adoption of advanced technologies and the maintenance of productivity. Operating modern injection molding machines requires specialized knowledge in programming, maintenance, and quality control, which is increasingly scarce. Research underscores a significant and growing mismatch between the skills available in the workforce and the technical requirements of modern manufacturing. This "skills gap" is particularly acute in areas requiring expertise in automation and digital systems. This skills gap is exacerbated by the aging workforce and the lack of interest among younger generations in pursuing careers in manufacturing. Surveys by the Association of German Chambers of Commerce and Industry (DIHK) reveal that a vast majority of industrial firms face persistent difficulties in recruiting qualified technical personnel. This shortage of human capital acts as a primary bottleneck, delaying the adoption of advanced production technologies and slowing overall productivity growth. Without skilled operators, companies cannot fully leverage the capabilities of automated and digitalized injection molding systems, leading to suboptimal performance and increased error rates. Training existing employees requires time and resources, which smaller companies may not afford. Additionally, the rapid pace of technological change means that skills become obsolete quickly, necessitating continuous professional development. The French Ministry of Labor emphasizes the need for updated vocational training programs to address the mismatch between educational outcomes and industry needs. Furthermore, the competition for talent from other high-tech sectors, such as information technology and renewable energy, intensifies the recruitment challenge. Thus, the inability to attract and retain skilled personnel limits the growth potential of injection molding companies and affects their ability to innovate and compete effectively in the global market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.90% |

| Segments Covered | By Raw Material Type, Application, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | BASF SE, Covestro AG, LyondellBasell Industries N.V., INEOS Group, SABIC, Arkema S.A., Evonik Industries AG, Solvay S.A., Röchling Group, Faurecia SE, Magna International Inc., Plastic Omnium, Engel Austria GmbH, Arburg GmbH + Co KG, Husky Injection Molding Systems Ltd. |

SEGMENTAL ANALYSIS

By Raw Material Type Insights

The polypropylene segment dominated the Europe plastic injection molding market and accounted for a 28.5% share in 2025. This dominance of the segment is mainly driven by its exceptional versatility, chemical resistance, and low density which make it suitable for a wide range of applications from packaging to automotive components. The material’s ability to withstand high temperatures without deforming makes it ideal for dishwasher-safe containers and automotive under-the-hood parts. Additionally, polypropylene is highly recyclable, aligning with the European Union’s circular economy goals. Its cost-effectiveness compared to engineering plastics further enhances its appeal for mass-produced consumer goods. Manufacturers favor polypropylene for its ease of processing and short cycle times, which boost production efficiency. Thus, the combination of performance attributes, sustainability potential, and economic advantages ensures polypropylene remains the dominant raw material in the European injection molding landscape. The robust demand from the packaging and automotive sectors significantly reinforces the leadership of polypropylene in the injection molding market. In the packaging industry, polypropylene is preferred for rigid containers, caps, and closures due to its excellent barrier properties and durability. The rise of e-commerce has further accelerated the demand for durable and lightweight packaging solutions, where polypropylene excels. For example, major retailers across Europe have shifted towards polypropylene-based reusable crates for logistics, reducing waste and operational costs. In the automotive sector, the transition towards electric vehicles necessitates weight reduction to extend battery range. Polypropylene composites offer a viable solution by replacing heavier metal components with lighter plastic alternatives. Furthermore, advancements in polymer technology have enhanced the mechanical strength of polypropylene, allowing it to be used in structural applications. The French Automotive Industry Committee highlights that new grades of reinforced polypropylene are being adopted for bumper beams and interior panels. These developments expand the application scope of polypropylene, ensuring its continued dominance. Consequently, the sustained growth in key end-use industries drives the extensive utilization of polypropylene in Europe.

The polylactic acid and other bio-based polymers segment is expected to exhibit a noteworthy CAGR of 12.5% between 2026 and 2034. Robust regulatory mandates aimed at mitigating fossil fuel dependency and reducing plastic pollution are fuelling significant growth in this segment. Government initiatives such as the Single Use Plastics Directive mandate the replacement of conventional plastics with sustainable alternatives in specific applications. For instance, France has implemented laws requiring certain single-use items to be made from compostable materials, driving demand for polylactic acid. The European Commission’s Bioeconomy Strategy provides financial incentives for research and development in bio-based materials, fostering innovation. Companies are increasingly investing in facilities capable of processing these materials to meet customer demands for eco-friendly products. Additionally, consumer awareness regarding environmental issues is influencing purchasing decisions, prompting brands to adopt sustainable packaging solutions. So, the regulatory and consumer-driven shift towards sustainability propels the rapid expansion of biobased polymers in the injection molding sector. Technological advancements in the formulation and processing of bio-based polymers further accelerate their market growth. Historically, bio-based plastics faced challenges related to thermal stability and mechanical strength, limiting their application scope. However, recent innovations have significantly improved these properties, making them viable alternatives to conventional plastics. These improvements enable manufacturers to produce durable consumer goods and automotive components using bio-based materials. For example, Volvo Cars has introduced interior parts made from bio-based composites, demonstrating the feasibility of these materials in high-performance applications. Additionally, the development of specialized injection molding machines optimized for biopolymers reduces processing defects and improves surface finish. Furthermore, collaborations between material suppliers and molders facilitate the customization of bio-based formulations for specific needs. These technological strides lower the barriers to entry and expand the application potential of bio-based polymers. Consequently, the continuous improvement in material performance and processing efficiency drives the rapid adoption of this segment.

By Application Insights

In 2025, the packaging segment maintained the majority share of 35.6% of the Europe plastic injection molding market. This supremacy of the segment is attributed to the booming e-commerce sector and the increasing consumer preference for convenient and durable packaging solutions. Injection-molded plastic containers, crates, and pallets are essential for logistics and distribution networks, ensuring product integrity. For instance, studies show that the use of reusable plastic crates has increased annually due to their cost-effectiveness and sustainability benefits. Additionally, the food and beverage industry relies heavily on injection-molded packaging such as cups, lids, and tubs for ready-to-eat meals. The European Food Safety Authority emphasizes the importance of safe and hygienic packaging materials, driving the use of food-grade plastics like polypropylene and polyethylene. The convenience of single-serve portions and resealable containers appeals to busy consumers, boosting demand. Furthermore, innovations in thin-wall injection molding allow manufacturers to produce lightweight packaging that reduces material usage and transportation costs. Therefore, the synergy between e-commerce growth, consumer convenience, and technological innovation sustains the leadership of the packaging segment. The regulatory focus on recyclability and circular economy principles significantly influences the packaging segment’s dominance. The European Union’s Packaging and Packaging Waste Regulation mandates that all plastic packaging must be designed for recycling by 2030. This directive drives manufacturers to adopt mono-material structures, which are easier to recycle than multi-layer complexes. Injection molding plays a crucial role in producing mono-material packaging solutions that meet these regulatory requirements. For example, many companies are shifting from multi-layer films to injection-molded containers made entirely of polypropylene or polyethylene. The French Ministry of Ecological Transition supports these transitions through grants for eco-design projects. Additionally, the introduction of extended producer responsibility schemes incentivizes companies to design packaging with higher recycled content. Brands are increasingly marketing their sustainability efforts, appealing to environmentally conscious consumers. Thus, the regulatory push for recyclability, combined with brand sustainability initiatives, drives the continued dominance of the packaging segment in the injection molding market.

The healthcare segment is predicted to witness the highest CAGR of 9.2% over the forecast period, owing to the aging population and the rising prevalence of chronic diseases, which increases the demand for medical devices and disposable products. This demographic shift necessitates increased healthcare services, including surgeries, diagnostics, and home care. Injection molding is critical for producing high-precision components such as syringes, IV connectors, inhalers, and surgical instruments. The precision and sterility offered by injection molding ensure patient safety and compliance with strict regulatory standards. For instance, the production of insulin pens and glucose monitors relies heavily on intricate plastic components manufactured through this process. Additionally, the expansion of home healthcare services increases the need for user-friendly and portable medical devices. Consequently, the growing healthcare needs of an aging population drive the rapid expansion of the healthcare application segment. Technological advancements in minimally invasive surgical procedures further accelerate the growth of the healthcare segment in the injection molding market. These procedures require specialized instruments and devices that are often made from high-performance plastics due to their biocompatibility and sterilization resistance. Injection molding enables the production of complex geometries required for catheters, endoscopes, and robotic surgical tools. For example, the da Vinci Surgical System utilizes numerous plastic components manufactured through precision injection molding. Additionally, the development of drug delivery systems, such as transdermal patches and implantable devices, relies on advanced molding techniques. The European Medicines Agency has approved several new drug delivery platforms that incorporate molded plastic parts. Furthermore, the trend towards personalized medicine drives the demand for customized diagnostic devices. 3D printing combined with injection molding allows for the rapid prototyping and production of patient-specific tools. These innovations expand the application scope of injection molding in healthcare. So, the integration of advanced technologies and the shift towards minimally invasive treatments fuel the rapid growth of this segment.

REGIONAL ANALYSIS

Germany Plastic Injection Molding Market Analysis

Germany led the Europe plastic injection molding market and held a 26.3% share in 2025 because of its robust automotive and manufacturing sectors, which are major consumers of molded plastic components. The German Federal Ministry for Economic Affairs and Climate Action (BMWK) identifies the automotive industry as the nation's most vital industrial branch. Its total contribution to the economy, including the extensive supply chain, represents a significant share of the national GDP and remains a primary driver for high-performance, lightweight materials. Germany is home to leading machinery manufacturers such as Arburg and Engel which provide advanced injection molding technologies globally. The presence of these industry leaders fosters a strong ecosystem for innovation and efficiency. Additionally, the country’s emphasis on Industry 4.0 has led to the widespread adoption of smart manufacturing practices in injection molding facilities. According to the German Engineering Federation (VDMA), the vast majority of German manufacturers have now integrated advanced digital solutions. This shift toward smart manufacturing is essential for maintaining productivity and global competitiveness in the capital goods market. The healthcare sector also contributes significantly, with Germany being a major exporter of medical devices. The German Medical Technology Association (BVMed) reports that the sector continues to achieve record international sales. High demand for quality "Made in Germany" medical devices has led to a robust export performance, particularly in diagnostic and surgical equipment. Furthermore, the government’s support for circular economy initiatives encourages the use of recycled materials in molding processes. Consequently, the combination of industrial strength technological leadership and sustainability focus solidifies Germany’s position as the dominant player in the European market.

Italy Plastic Injection Molding Market Analysis

Italy followed closely behind in the Europe plastic injection molding market and occupied a 18.1% share in 2025. This position of the segment is driven by its strong presence in the packaging, automotive, and consumer goods sectors. Specific high-tech niches within the manufacturing sector have remained resilient. Italian producers continue to rely on strong international demand to balance domestic economic shifts. Italy is renowned for its design excellence, which extends to plastic products, particularly in the furniture and appliance industries. The Italian Association of Plastics Machinery Manufacturers reports that the country is a leading exporter of injection molding machines, catering to global demand. Additionally, the packaging industry is a significant consumer of molded plastic,s driven by the food and beverage sector. The Italian Food and Drink Industry Federation (Federalimentare) notes that the sector is managing increased costs related to sustainable packaging. Manufacturers are investing in new materials to comply with environmental regulations while maintaining food safety standards. The automotive sector also contributes, with manufacturers like Fiat Stellantis utilizing local suppliers for plastic components. Furthermore, the government’s National Recovery and Resilience Plan includes investments in green technologies, promoting the adoption of sustainable molding practices. Consequently, the synergy between design innovation, industrial capability, and policy support maintains Italy’s strong position in the European market.

France Plastic Injection Molding Market Analysis

France plays a key role in the Europe plastic injection molding market owing to its diverse industrial base, including aerospace, automotive, and healthcare sectors. According to the French Aerospace Industries Association (GIFAS), the sector has surpassed pre-pandemic performance, with global turnover reaching record highs. This growth is fueled by a surge in orders for civil aircraft and a strong defense export market, necessitating massive investments in high-performance polymer components for lightweighting. Injection molding is essential for producing lightweight and durable parts that meet stringent safety standards. Additionally, the automotive sector is transitioning towards electric vehicles, boosting demand for specialized plastic components. France's Automotive Platform (PFA) highlights that while overall domestic production is recovering, the registration of full-battery electric vehicles has seen the most dramatic growth. Manufacturers are retooling French plants to produce new electric models, driving demand for specialized battery housing materials. The healthcare sector also plays a vital role, with France being a major producer of medical devices. Furthermore, the government’s Anti-Waste Law promotes the use of recycled plastics in manufacturing. These regulatory measures encourage manufacturers to adopt sustainable practices. Additionally, the presence of major chemical companies like Arkema supports the supply of innovative polymer materials. Thus, the combination of advanced industries, regulatory support and material innovation drives the growth of the injection molding market in France.

United Kingdom Plastic Injection Molding Market Analysis

The United Kingdom expanded steadily in the Europe plastic injection molding market due to a strong focus on packaging and healthcare applications. The country’s market is also driven by the booming e-commerce sector, which demands efficient and durable packaging solutions. The Office for National Statistics (ONS) indicates that the UK remains one of the world's most mature e-commerce markets. While the rapid growth seen during the pandemic has leveled off, online sales continue to account for more than a quarter of all retail activity, maintaining a high demand for protective plastic packaging. Injection-molded crates, containers, and protective packaging are essential for logistics operations. Additionally, the healthcare sector is a significant contributor, with the UK being a hub for pharmaceutical and medical device manufacturing. The Association of the British Pharmaceutical Industry (ABPI) notes that while the UK remains a global R&D hub, the industry faces increasing pressure from global competition. Despite this, pharmaceutical companies continue to invest billions annually in UK-based research, particularly in advanced therapies and genomics. This investment drives the demand for precision-molded components for drug delivery systems and diagnostic devices. The National Health Service’s emphasis on improving patient care further boosts the consumption of single-use medical plastics. Furthermore, the government’s Plastic Packaging Tax incentivizes the use of recycled materials in packaging. So, the synergy between e-commerce growth, healthcare innovation, and sustainability regulations supports the steady expansion of the injection molding market in the UK.

Spain Plastic Injection Molding Market Analysis

Spain is likely to grow significantly in the Europe plastic injection molding market from 2026 to 2034, owing to its robust packaging and automotive industries. The country’s market benefits from its strategic location as a gateway to European and African markets. According to the Spanish National Statistics Institute (INE), the manufacturing industry experienced moderate growth as it navigated high energy costs and rising interest rates. While the sector held up better than some European counterparts, its overall momentum was tempered by stagnant sales volumes in most branches. The packaging industry is a major consumer of injection-molded products, particularly for the food and beverage sector. The Spanish Federation of Food and Drink Industries (FIAB) indicates that while the sector remains a primary industrial pillar, it faced a slowdown in production value during the last year. Inflation and adverse weather conditions impacted consumption patterns, though the industry continues to see a gradual shift toward more sustainable and returnable packaging solutions. The automotive sector also contributes significantly, with manufacturers like Seat utilizing local suppliers for plastic components. Additionally, the tourism industry drives demand for consumer goods and hospitality-related plastic products. The Spanish Confederation of Hotels and Tourist Accommodations indicates that tourist arrivals reached pre-pandemic levels, boosting consumption. Furthermore, the government’s Recovery Transformation and Resilience Plan includes funds for digitalization and sustainability in manufacturing. These initiatives encourage manufacturers to adopt efficient and eco-friendly molding practices. Consequently, the combination of industrial diversity, strategic location, and policy support sustains Spain’s significant presence in the European market.

COMPETITION OVERVIEW

The competition in the Europe plastic injection molding market is intense, characterized by the presence of established global manufacturers and specialized regional players. Leading companies differentiate themselves through technological innovation, particularly in electrification and digital connectivity. The shift towards sustainable manufacturing practices drives manufacturers to develop energy-efficient machines and processes that comply with stringent regulatory standards. Price competition remains significant but is often secondary to factors such as reliability, after-sales support, and total cost of ownership. Brands with strong service networks and comprehensive automation offerings gain a competitive edge by ensuring minimal downtime for customers. The rise of Industry 4.0 influences market dynamics as companies integrate smart technologies to enhance productivity and quality. Smaller manufacturers focus on niche applications and customized solutions to capture specific market segments. Intellectual property protection and patenting of new technologies are critical for maintaining competitive advantages. Collaboration with material suppliers enhances the value proposition through optimized processing of bio-based and recycled polymers. The market witnesses the continuous entry of new players offering innovative designs, which pressures incumbents to accelerate product development cycles. Overall, the competitive landscape is shaped by the ability to balance performance, sustainability, and cost-effectiveness while adapting to evolving customer needs and regulatory requirements in the European region.

KEY MARKET PLAYERS

A few major players of the Europe plastic injection molding market include

- BASF SE

- Covestro AG

- LyondellBasell Industries N.V

- INEOS Group

- SABIC

- Arkema S.A

- Evonik Industries AG

- Solvay S.A

- Röchling Group

- Faurecia SE

- Magna International Inc

- Plastic Omnium

- Engel Austria GmbH

- Arburg GmbH + Co. KG

- Husky Injection Molding Systems Ltd

Top Strategies Used by the Key Market Participants

Key players in the Europe plastic injection molding market primarily focus on technological innovation and digital integration to maintain a competitive advantage. Companies invest heavily in research and development to create energy-efficient machines that comply with strict environmental regulations. Strategic partnerships with software firms enable the implementation of Industry 4.0 solutions such as predictive maintenance and real-time monitoring. Manufacturers also expand their service networks to provide comprehensive after-sales support and minimize customer downtime. Product diversification through the development of specialized machines for electric vehicles and medical devices addresses emerging market needs. Sustainability initiatives including the use of recycled materials and carbon-neutral manufacturing processes, are increasingly adopted to meet regulatory demands. Additionally, companies pursue strategic acquisitions to broaden their product portfolios and enter new geographic segments. Training programs for skilled labor help address workforce shortages and ensure optimal machine utilization. These strategies collectively drive growth and ensure long-term viability in the dynamic European manufacturing landscape.

Leading Players in the Europe Plastic Injection Molding Market

- Arburg GmbH and Co KG stands as a premier manufacturer of injection molding machines globally with a profound impact on the European market. The company is renowned for its Allrounder series, which offers exceptional versatility and precision for diverse applications. Arburg strengthens its market position through continuous innovation in electric drive technology and digitalization via its Arburg Production Control system. Recent initiatives include the expansion of its facility in Lossburg, Germany, to enhance production capacity for energy-efficient machines. The company actively promotes sustainable manufacturing by developing solutions for processing bio-based and recycled materials. Arburg’s commitment to customer-centric service and modular machine concepts allows clients to customize equipment for specific needs. This approach ensures high operational efficiency and reduced downtime for manufacturers across the automotive, healthcare, and packaging sectors. By integrating Industry 4.0 standards into their offerings, Arburg facilitates smart factory implementations. Their global network supports local customers with expert technical assistance, reinforcing their reputation for reliability and technological leadership in the competitive European landscape.

- Haitian International Holdings Limited has established a formidable presence in the Europe plastic injection molding market through its subsidiary Haitian Plastics Machinery. The company is recognized for providing cost-effective and reliable injection molding solutions that cater to a broad spectrum of industrial needs. Haitian strengthens its market position by expanding its European service network and establishing assembly plants in regions such as Germany and Slovakia. Recent actions include the launch of advanced servo-driven machines that offer superior energy savings and faster cycle times. The company focuses on delivering high-value propositions to small and medium-sized enterprises by balancing performance with affordability. Haitian’s strategic partnerships with local distributors ensure timely support and availability of spare parts. The introduction of the Zhafir brand targets the premium segment with innovative all-electric machines designed for high-precision applications. By leveraging economies of scale and continuous research and development, Haitian enhances its competitiveness. Their emphasis on sustainability aligns with European regulatory requirements promoting the adoption of eco-friendly manufacturing processes. This strategic focus enables Haitian to capture significant demand across various end-use industries in Europe.

- Engel Austria GmbH is a leading innovator in the Europe plastic injection molding market, known for its comprehensive range of machinery and automation solutions. The company plays a pivotal role in advancing injection molding technology through its focus on digitalization and integration. Engel strengthens its market position by offering complete cell solutions that combine injection molding machines with robots and peripheral equipment. Recent developments include the enhancement of its inject 4.0 platform, which enables seamless connectivity and data analysis for optimized production. The company has invested heavily in research facilities to develop technologies for processing lightweight composites and recycled materials. Engel’s collaboration with automotive manufacturers drives the adoption of large-scale injection molding for electric vehicle components. Their commitment to sustainability is evident in the series of all-electric machines, which reduce energy consumption significantly. Engel also provides extensive training programs to address the skills gap in the industry. By focusing on system integration and process stability, Engel delivers high productivity and quality to its customers. This holistic approach solidifies its reputation as a trusted partner for complex manufacturing challenges in Europe.

MARKET SEGMENTATION

This research report on the Europe plastic injection molding market has been segmented and sub-segmented based on raw material type, application & region.

By Raw Material Type

- Polypropylene

- Acrylonitrile Butadiene Styrene

- Polystyrene

- Polyethylene

- Polyvinyl Chloride

- Others

By Application

- Packaging

- Building and Construction

- Consumer Goods

- Electronics

- Automotive and Transportation

- Healthcare

- Other Applications

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What are the key drivers of the market?

Major drivers include rising demand in automotive lightweighting, increasing packaging needs, and technological advancements in molding processes.

2. Which industries use plastic injection molding the most?

Key industries include automotive, packaging, healthcare, electronics, and consumer goods.

3. What materials are commonly used in injection molding?

Common materials include polyethylene (PE), polypropylene (PP), polystyrene (PS), and ABS.

4. What are the major applications of plastic injection molding?

Applications include automotive components, packaging products, medical devices, and electronic housings.

5. What trends are shaping the market?

Key trends include sustainable plastics, recycled materials, and automation in manufacturing.

6. What challenges does the market face?

Challenges include environmental concerns, strict regulations, and fluctuating raw material prices.

7. How is sustainability impacting the market?

There is increasing demand for biodegradable and recyclable plastics, driving innovation in eco-friendly materials.

8. Who are the key market players in Europe?

Major players include BASF SE, Covestro AG, INEOS Group, SABIC, and Röchling Group.

9. What role does technology play in the market?

Advanced technologies such as automation, AI, and precision molding improve efficiency and product quality.

10. What opportunities exist in the Europe plastic injection molding market?

Opportunities include growth in electric vehicles, medical applications, and sustainable packaging solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com