Europe Solar PV Inverters Market Size, Share, Trends, and Growth Analysis Report, Segmented by Type, Application, and Country – Industry Forecast From 2026 to 2034

Europe Solar PV Inverters Market Report Summary

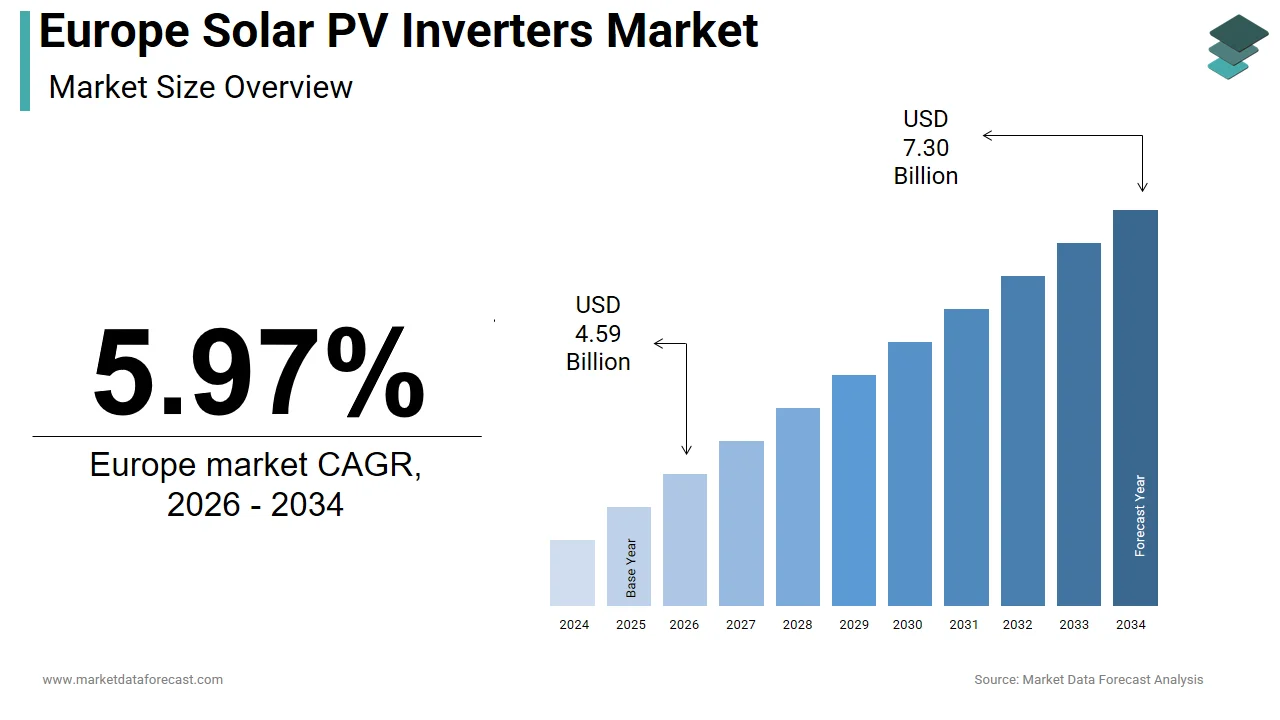

The Europe solar PV inverters market was valued at USD 4.33 billion in 2025, is estimated to reach USD 4.59 billion in 2026, and is projected to reach USD 7.30 billion by 2034, growing at a CAGR of 5.97% from 2026 to 2034. Market growth is driven by the increasing adoption of renewable energy, supportive government policies, and the transition toward decarbonization across Europe. Solar PV inverters play a critical role in converting solar energy into usable electricity, making them essential for both residential and commercial solar installations. Additionally, rising investments in distributed energy systems, energy storage integration, and smart grid infrastructure are further accelerating market expansion.

Key Market Trends

- Growing adoption of renewable energy and solar power systems.

- Increasing investments in distributed energy and smart grids.

- Rising demand for energy-efficient and high-performance inverters.

- Expansion of residential solar installations.

- Strong government incentives and decarbonization policies.

Segmental Insights

- Based on type, the string inverters segment dominated the Europe solar PV inverters market by capturing 64.6% share in 2025, driven by cost-effectiveness and ease of installation.

- Based on application, the residential segment led the market with 44.9% share in 2025, supported by increasing rooftop solar adoption.

Regional Insights

The Europe solar PV inverters market is witnessing steady growth across key renewable energy markets.

- Germany led the market in 2025 with 24.4% share, driven by strong renewable energy adoption and policy support.

- Italy followed as the second-largest market, supported by favorable climatic conditions and government incentives.

- Spain is expected to witness strong growth due to abundant solar resources and progressive renewable energy policies.

Competitive Landscape

The Europe solar PV inverters market is competitive, with companies focusing on technological innovation, efficiency improvements, and integration with smart energy systems. Strategic partnerships and expansion of product portfolios are key competitive strategies.

Prominent companies operating in the Europe solar PV inverters market include Fimer SpA, Fronius International GmbH, Siemens AG, Huawei Technologies Co., Ltd., SMA Solar Technology AG, Mitsubishi Electric Corporation, General Electric Company, and Schneider Electric SE.

Europe Solar PV Inverters Market Size

The size of the Europe solar PV inverters market was worth USD 4.33 billion in 2025. The regional market is anticipated to grow at a CAGR of 5.97% from 2026 to 2034, reaching USD 7.30 billion by 2034, up from USD 4.59 billion in 2026.

Solar PV inverters constitute a critical segment of the renewable energy infrastructure, serving as the technological bridge that converts direct current generated by photovoltaic panels into alternating current suitable for grid integration and household consumption. This market is pivotal in the continent's transition toward decarbonization and energy independence. As per Eurostat, the share of renewable energy in the European Union's gross final energy consumption reached 23 percent in 2022, reflecting a substantial shift away from fossil fuels. Furthermore, the International Energy Agency stated that solar photovoltaic capacity additions in Europe exceeded 41 gigawatts in 2022, marking a record high and underscoring the urgent need for efficient inversion technology. The regulatory landscape, driven by the European Green Deal, mandates significant reductions in greenhouse gas emissions, thereby accelerating the deployment of solar installations across residential, commercial, and utility-scale sectors. Inverters are not merely conversion devices but intelligent components that manage grid stability, optimize energy yield, and facilitate battery storage integration. The increasing complexity of modern power grids requires advanced inverter functionalities such as reactive power control and frequency regulation. According to the European Commission, the REPowerEU plan aims to install 600 gigawatts of solar photovoltaic capacity by 2030, which necessitates a robust supply chain for high-efficiency inverters. These market dynamics are influenced by technological advancements in silicon carbide semiconductors and digital monitoring capabilities, ensuring that solar energy systems operate at peak performance while maintaining grid compatibility and safety standards throughout the diverse climatic conditions of the European region.

MARKET DRIVERS

Aggressive government mandates and subsidy schemes accelerate residential adoption.

Government initiatives across Europe are one of the key factors propelling the growth of the European solar PV inverters market, particularly in the residential sector. Nations such as Germany, Italy, and Spain have implemented generous feed-in tariffs and tax incentives that lower the initial investment barrier for homeowners. As per the German Federal Network Agency, newly installed photovoltaic systems in Germany reached approximately 8.7 gigawatts in 2022, driven largely by favorable policy frameworks. These policies often mandate or strongly encourage the installation of smart inverters that can communicate with the grid to enhance stability. The European Union’s Recovery and Resilience Facility allocates billions of euros to green transitions, with a significant portion dedicated to renewable energy infrastructure. According to the Italian National Agency for New Technologies, Energy and Sustainable Economic Development, the superbonus scheme led to a 150 percent increase in residential solar installations in 2021 compared to the previous year. Such fiscal measures directly stimulate demand for inverters, as every solar panel array requires at least one unit. Additionally, net metering policies allow consumers to sell excess electricity back to the grid, increasing the economic viability of solar projects. The certainty provided by long-term policy commitments encourages manufacturers to expand production capacities and invest in research and development. This regulatory support creates a stable environment for market growth, ensuring that the adoption of solar technology continues to rise despite broader economic fluctuations, thereby sustaining high demand for both string and micro inverters across the continent.

Rising electricity prices and energy security concerns drive decentralized generation.

The surge in electricity prices and increased concerns over energy security have significantly boosted the demand for solar PV inverters as consumers and businesses seek to reduce reliance on centralized power grids, which is further aiding the regional market expansion. The geopolitical tensions in Eastern Europe disrupted natural gas supplies, leading to unprecedented spikes in energy costs across the continent. As per Eurostat, the average electricity price for households in the European Union increased by 29 percent in the second half of 2022 compared to the same period in the previous year. This economic pressure has accelerated the payback period for solar investments, which is making self-consumption an attractive financial strategy. Consequently, there is a growing preference for hybrid inverters that can integrate with battery storage systems, allowing users to store excess energy for use during peak pricing hours or outages. According to the Solar Power Europe association, the residential storage market in Europe grew by 85 percent in 2022, closely linked to the adoption of advanced inverter technologies. Businesses are also adopting solar solutions to mitigate operational costs and ensure business continuity. The desire for energy independence is no longer just an environmental choice but a financial imperative. This shift drives the market for sophisticated inverters capable of managing complex energy flows between solar panels, batteries, and the grid. The trend towards prosumerism, where consumers also produce energy, is reshaping the retail energy landscape, necessitating robust and intelligent inversion solutions that can handle bidirectional power flow and maintain grid stability amidst fluctuating supply and demand patterns.

MARKET RESTRAINTS

Supply chain disruptions and raw material scarcity constrain production capabilities.

One of the significant restraints to the growth of the European solar PV inverters market is the ongoing supply chain disruptions and scarcity of critical raw materials required for manufacturing. Inverters rely heavily on semiconductors, copper, and aluminum, all of which have experienced volatile pricing and availability issues in recent years. As per the European Semiconductor Industry Association, the global chip shortage impacted various sectors, including renewable energy, causing lead times for electronic components to extend by several months in 2022. This delay hampers the ability of inverter manufacturers to meet the surging demand, resulting in project postponements and increased costs. Additionally, the dependence on Asian suppliers for key components exposes European manufacturers to geopolitical risks and logistical bottlenecks. According to the International Renewable Energy Agency, the cost of critical minerals such as lithium and cobalt, essential for associated storage systems, fluctuated wildly, affecting the overall economics of solar plus storage projects. The lack of domestic semiconductor fabrication facilities in Europe further exacerbates this vulnerability. While the European Chips Act aims to boost local production, its full impact will take years to materialize. In the interim, manufacturers struggle to secure consistent supplies, forcing them to redesign products or source alternative components, which can compromise performance or require recertification. These supply-side constraints limit the market's growth potential, as installers face delays and higher procurement costs, which can dampen consumer enthusiasm and slow down the pace of new installations across the region.

Grid infrastructure limitations and regulatory complexities hinder seamless integration.

Aging grid infrastructure and complex regulatory frameworks are further impeding the expansion of the European solar PV inverters market. Many distribution networks were designed for unidirectional power flow and lack the capacity to handle the bidirectional energy streams generated by distributed solar installations. As per the European Network of Transmission System Operators for Electricity, significant investments are required to upgrade grid infrastructure to accommodate higher shares of variable renewable energy. Without these upgrades, grid operators may impose strict curtailment rules or connection restrictions on new solar projects, limiting the effective utilization of installed inverter capacity. Furthermore, the lack of harmonized technical standards across different European countries creates barriers for manufacturers and installers. Each nation may have specific grid code requirements for inverters, necessitating customized solutions and increasing compliance costs. According to a report by the European Commission, fragmented regulatory landscapes slow down the deployment of cross-border renewable energy projects and create inefficiencies in the single energy market. The approval process for grid connections can be lengthy and bureaucratic, delaying project commissioning. Additionally, concerns about voltage fluctuations and frequency instability caused by high penetration of solar power lead to conservative grid management practices. These technical and administrative hurdles increase the complexity and cost of deploying solar PV systems, acting as a brake on market expansion despite strong demand for renewable energy solutions.

MARKET OPPORTUNITIES

Integration of artificial intelligence for predictive maintenance and optimization

The integration of artificial intelligence and machine learning into solar PV inverters presents a significant opportunity for the European solar PV inverters market. Smart inverters equipped with AI algorithms can predict equipment failures, optimize energy conversion efficiency, and adjust operations based on real-time weather and grid conditions. As per a study by the Fraunhofer Institute for Solar Energy Systems, predictive maintenance can reduce operation and maintenance costs by up to 30 percent by identifying issues before they lead to downtime. This capability is particularly valuable for large-scale utility projects where manual inspection is costly and inefficient. AI-driven inverters can also participate in virtual power plants, aggregating distributed energy resources to provide grid services such as frequency regulation and voltage support. According to the European Technology and Innovation Platform for Photovoltaics, the digitalization of photovoltaic systems is key to unlocking their full potential in a flexible energy system. The ability to remotely monitor and control inverters allows operators to maximize energy yield and extend asset lifespan. Furthermore, data analytics can provide insights into consumer behavior and energy usage patterns, enabling tailored energy services. This technological advancement transforms inverters from passive components into active grid assets, creating new revenue streams for owners and operators. The growing emphasis on digital twins and Internet of Things connectivity further amplifies this opportunity, positioning AI-enabled inverters as central elements of the future smart grid infrastructure in Europe.

Expansion of hybrid inverter solutions for energy storage compatibility

The rising demand for energy storage systems creates a lucrative opportunity for the expansion of the European solar PV inverters market. Hybrid inverters can manage both solar input and battery storage, allowing for greater energy self-sufficiency and resilience against grid outages. As per BloombergNEF, the European home battery market is expected to grow at a compound annual growth rate of 25 percent through 2030, driven by falling battery costs and increasing electricity prices. This trend necessitates inverters that are compatible with various battery chemistries and communication protocols. Manufacturers are developing versatile hybrid models that offer seamless switching between grid-tied and off-grid modes, enhancing reliability for consumers. According to the Solar Power Europe association, the attachment rate of batteries to new residential solar installations in key markets like Germany and Italy exceeded 50 percent in 2022. This high adoption rate underscores the critical role of hybrid inverters in enabling stored energy utilization. Additionally, regulatory frameworks in several countries are beginning to recognize the value of storage in grid stabilization, offering incentives for combined solar and storage systems. The ability of hybrid inverters to provide backup power during emergencies is increasingly valued by homeowners and businesses alike. This convergence of solar generation and storage capabilities opens new market segments and drives innovation in inverter design, focusing on efficiency, modularity, and user-friendly interfaces for managing complex energy flows.

MARKET CHALLENGES

Volatility in semiconductor supply chains impacts manufacturing consistency.

The volatility in semiconductor supply chains that directly impacts manufacturing consistency and product availability is primarily challenging the European solar PV inverters market growth. Inverters rely on sophisticated power electronics, including insulated gate bipolar transistors and metal oxide semiconductor field effect transistors, which are subject to global supply fluctuations. As per the European Semiconductor Industry Association, the lead times for certain power semiconductors extended to over 50 weeks in 2022, causing significant production delays for inverter manufacturers. This scarcity forces companies to compete for limited allocations, driving up component costs and squeezing profit margins. The concentration of semiconductor manufacturing in Asia further exacerbates the risk, as geopolitical tensions or logistical disruptions can severely impact supply. According to the International Energy Agency, supply chain bottlenecks were cited as a primary reason for the delay in several large-scale solar projects in Europe during the past year. Manufacturers must constantly adapt their designs to use available components, which requires rigorous testing and recertification, adding time and expense to the product development cycle. This instability makes it difficult for planners to forecast inventory levels and meet customer delivery expectations. The lack of transparent visibility into upstream supply chains complicates risk management strategies. Until domestic semiconductor production capabilities are strengthened or diversified sourcing strategies are fully implemented, the market will remain vulnerable to these external shocks, hindering its ability to scale rapidly in response to growing demand for renewable energy infrastructure.

Cybersecurity threats to connected inverter systems pose operational risks.

The increasing connectivity of solar PV inverters introduces significant cybersecurity challenges, as these devices become potential entry points for cyberattacks on the power grid, which further challenges the regional market growth. Modern inverters are equipped with communication modules that allow for remote monitoring and control, making them susceptible to hacking and malware infiltration. As per the European Union Agency for Cybersecurity, the energy sector is one of the most targeted industries for cyber threats, with incidents increasing by 20 percent in 2022. A successful attack on inverter networks could lead to widespread power disruptions, data theft, or even physical damage to equipment. The lack of standardized security protocols across different manufacturers complicates the implementation of robust defense mechanisms. According to a report by the Joint Research Centre of the European Commission, many existing inverters lack basic security features such as encryption and secure boot processes, leaving them vulnerable to exploitation. As the number of connected devices grows, the attack surface expands, requiring continuous updates and patches to address emerging threats. However, the lifecycle of solar installations often exceeds the support period for software updates, creating long-term vulnerabilities. Ensuring the integrity and confidentiality of data transmitted by inverters is crucial for maintaining grid stability and consumer trust. Manufacturers must prioritize security by design, incorporating advanced authentication and encryption methods. Failure to address these cybersecurity risks could result in regulatory penalties, reputational damage, and reluctance among utilities to integrate distributed solar resources, posing a persistent challenge to market growth.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Application, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled |

|

SEGMENTAL ANALYSIS

By Type Insights

The string inverters segment dominated the market by holding 64.6% of the regional market share in 2025. The dominance of the string inverter segment in the European market is driven by its optimal balance between cost efficiency and performance for residential and commercial applications. This technology connects multiple solar panels in series, allowing for centralized conversion, which reduces the number of components required compared to micro inverters. The primary driver for this dominance is the widespread adoption of rooftop solar installations across European households and small businesses. As per Solar Power Europe, residential solar installations accounted for over 50 percent of the total newly installed capacity in the European Union in 2022, creating sustained demand for reliable and affordable string inverters. These devices offer easier maintenance and lower initial capital expenditure, making them attractive to price-sensitive consumers. Furthermore, technological advancements such as the integration of multiple maximum power point trackers allow string inverters to handle shading issues more effectively than earlier models. According to the Fraunhofer Institute for Solar Energy Systems, the efficiency of modern string inverters has surpassed 98 percent, ensuring minimal energy loss during conversion. The established supply chain and extensive installer familiarity with string inverter technology further reinforce its market position. Manufacturers continue to innovate by adding smart monitoring capabilities and hybrid functionalities that support battery storage, aligning with the growing trend of energy independence. This versatility ensures that string inverters remain the preferred choice for the majority of distributed generation projects in Europe, sustaining their dominant share in the market landscape.

However, the micro inverters segment is growing rapidly and is estimated to showcase a CAGR of projected to register the highest compound annual growth rate of 18.5 percent during the forecast period, fueled by the increasing demand for module-level power electronics and enhanced safety features. Unlike string inverters, micro inverters are attached to individual solar panels, optimizing energy production for each unit independently. This architecture eliminates the risk of single-point failure and maximizes yield in complex roof environments with partial shading or varying orientations. As per a report by Wood Mackenzie, the global micro inverter market is expanding rapidly, with Europe emerging as a key growth region due to stringent safety regulations and consumer preference for high reliability. The ability to monitor performance at the panel level provides homeowners with detailed insights into system health, facilitating proactive maintenance. According to the National Fire Protection Association standards adopted by many European countries, direct current voltage limitations in residential settings favor micro inverter technology, which operates at lower voltages. This safety advantage is particularly compelling in densely populated urban areas. Additionally, the rising popularity of premium residential solar systems, where aesthetics and performance are prioritized, drives adoption. Micro inverters simplify system design and installation, reducing labor costs and time. The integration of advanced grid support functions and seamless compatibility with battery storage systems further enhances their appeal. As consumers become more educated about the long-term benefits of module-level optimization, the demand for micro inverters continues to surge, outpacing other technology segments in terms of growth rate.

By Application Insights

The residential segment commanded the highest share of 44.9% of the regional market in 2025 due to the rising electricity prices and strong government incentives for homeowners. The economic case for self-consumption has become increasingly compelling as household energy bills have surged across the continent. As per Eurostat, the average electricity price for households in the European Union rose by 29 percent in the second half of 2022, accelerating the payback period for solar investments. This financial pressure has motivated millions of homeowners to install rooftop solar systems, directly driving demand for residential-grade inverters. Government schemes such as net metering and feed-in tariffs further enhance the attractiveness of residential solar by allowing users to sell excess energy back to the grid. According to the German Federal Network Agency, Germany alone added over 800000 new rooftop solar systems in 2022, reflecting a broader European trend. The simplicity of installing string or micro inverters on single-family homes makes them accessible to a wide consumer base. Additionally, the growing awareness of climate change and environmental responsibility encourages households to adopt clean energy solutions. The integration of smart home technologies with solar inverters allows users to manage energy consumption efficiently, adding value to the investment. The decentralized nature of residential installations also reduces strain on the central grid, aligning with national energy security goals. These factors collectively sustain the residential segment as the largest contributor to the market, with consistent growth expected as more households seek energy independence.

However, the utility scale segment is predicted to grow at the fastest rate and register a CAGR of 17.7% over the forecast period in the European solar PV inverters market, owing to the large-scale renewable energy projects aimed at meeting national carbon neutrality targets. Governments and private developers are investing heavily in solar farms to replace fossil fuel-based power generation. As per the International Energy Agency, utility-scale solar projects accounted for nearly 40 percent of the total solar capacity additions in Europe in 2022, highlighting the shift towards centralized renewable energy production. These projects require high-capacity central inverters that can handle massive power outputs efficiently and reliably. The competitive bidding processes for renewable energy contracts often favor large-scale installations due to their economies of scale and lower levelized cost of energy. According to the European Commission, the REPowerEU plan mandates significant increases in renewable energy capacity, prompting accelerated development of utility-scale solar parks in countries like Spain and Italy. Technological advancements in central inverters, such as higher voltage ratings and improved grid stability features, make them suitable for integration into high-voltage transmission networks. The ability of utility-scale projects to provide bulk clean energy supports grid decarbonization efforts effectively. Furthermore, corporate power purchase agreements are increasingly funding large solar developments, providing financial certainty for developers. This robust pipeline of utility-scale projects ensures rapid growth in the demand for high-power inverters, making this segment the fastest expanding within the market.

COUNTRY LEVEL ANALYSIS

Germany Solar PV Inverters Market Analysis

Germany led the solar PV inverters market in Europe in 2025 with 24.4% of the regional market share. The dominance of Germany in the European market is mainly driven by its longstanding commitment to renewable energy and robust policy framework. The country’s Energiewende policy has created a mature market for solar technologies, with widespread adoption across residential, commercial, and utility sectors. As per the German Federal Ministry for Economic Affairs and Climate Action, Germany installed approximately 7.9 gigawatts of new solar capacity in 2022, driving substantial demand for inverters. The presence of leading inverter manufacturers such as SMA Solar Technology fosters local innovation and supply chain resilience. German consumers are highly aware of energy efficiency and sustainability, leading to high penetration rates of solar systems in single-family homes. According to the German Solar Association, there are over 2 million photovoltaic systems installed in the country, creating a steady replacement and upgrade market for inverters. The government’s recent amendments to the Renewable Energy Sources Act aim to accelerate solar deployment further, targeting 215 gigawatts of installed capacity by 2030. This ambitious goal ensures continued demand for advanced inverter technologies, including hybrid models that support battery storage. The well-established installer network and favorable financing options facilitate easy access to solar solutions for homeowners. Additionally, the industrial sector’s focus on reducing carbon footprints drives commercial solar adoption. Germany’s combination of policy support, technological leadership, and consumer engagement solidifies its position as the dominant market for solar PV inverters in Europe.

Italy Solar PV Inverters Market Analysis

Italy secured the second-largest share of the European solar PV inverters market in 2025 due to the favorable climatic conditions and aggressive government incentives. The country’s Superbonus scheme, although modified, initially spurred a massive wave of residential retrofitting and solar installations. As per the Italian National Agency for New Technologies, Energy and Sustainable Economic Development, solar capacity additions in Italy reached record levels in 2022, with significant contributions from the residential sector. The high solar irradiance in southern Italy makes photovoltaic systems highly efficient, encouraging widespread adoption. Italian retailers and distributors have expanded their offerings to include smart inverters with remote monitoring capabilities, catering to tech-savvy consumers. According to Terna, the Italian transmission system operator, the country aims to reach 72 gigawatts of solar capacity by 2030, that require substantial investment in inverter infrastructure. The commercial and industrial sectors are also increasingly adopting solar solutions to mitigate high energy costs, driving demand for three-phase string inverters. Local manufacturing capabilities and strong partnerships with international inverter brands ensure adequate supply to meet growing demand. The regulatory environment supports self-consumption and energy-sharing communities, fostering innovative business models for solar energy. Furthermore, the integration of agrivoltaics, which combines agriculture with solar power generation, opens new avenues for inverter deployment in rural areas. Italy’s strategic focus on leveraging its natural solar resources through supportive policies and market mechanisms sustains its strong position in the regional market.

Spain Solar PV Inverters Market Analysis

Spain is estimated to showcase a promising CAGR in the European solar PV inverters market during the forecast period, owing to its exceptional solar resources and progressive renewable energy policies. The country has emerged as a hub for large-scale solar projects, attracting significant foreign investment. As per the Spanish Ministry for Ecological Transition, Spain added over 5 gigawatts of new solar capacity in 2022, primarily from utility-scale installations. This boom drives demand for high-power central inverters capable of managing large arrays efficiently. The government’s National Integrated Energy and Climate Plan targets 76 gigawatts of installed solar capacity by 2030, ensuring a robust pipeline of projects. Spanish utilities are actively developing solar parks to meet renewable energy mandates, creating steady demand for reliable inversion technology. According to Red Eléctrica de España, the grid operator, the integration of renewable energy sources is prioritized, requiring inverters with advanced grid support functions. The residential sector is also growing, supported by simplified administrative procedures for self-consumption installations. Tax incentives and subsidies for rooftop solar encourage homeowners to adopt photovoltaic systems. The presence of major engineering procurement and construction firms facilitates the rapid deployment of solar projects. Additionally, the declining cost of solar modules and inverters makes projects economically viable without heavy subsidies. Spain’s combination of natural advantages, policy clarity, and investment momentum positions it as a key growth engine for the solar PV inverters market in Europe, particularly in the utility-scale segment.

Netherlands Solar PV Inverters Market Analysis

The Netherlands is expected to exhibit a healthy CAGR in the European solar PV inverters market during the forecast period due to the high population density and strong environmental consciousness among consumers. The country has one of the highest densities of solar panels per capita in Europe, driven by effective subsidy schemes and net metering arrangements. As per Statistics Netherlands, the total installed solar capacity exceeded 18 gigawatts in 2022, with the majority located on residential rooftops. This widespread adoption creates consistent demand for string and micro inverters suitable for small-scale installations. The Dutch government’s commitment to reducing greenhouse gas emissions supports the continued expansion of solar energy. According to the Netherlands Enterprise Agency, subsidies for sustainable energy investments remain available, encouraging both households and businesses to install solar systems. The flat terrain and urban planning practices facilitate the easy installation of solar panels on various building types. Innovations in building-integrated photovoltaics are gaining traction, requiring specialized inverters that blend seamlessly with architectural elements. The commercial sector is also adopting solar solutions to meet corporate sustainability goals, driving demand for commercial-grade inverters. Grid congestion issues have prompted the development of smart inverters that can manage peak loads and provide grid services. The collaborative approach between government, industry, and consumers ensures a stable and growing market for solar PV inverters. The Netherlands’ focus on innovation and sustainability maintains its significant share in the European market, with a particular emphasis on residential and distributed generation applications.

United Kingdom Solar PV Inverters Market Analysis

The United Kingdom is predicted to hold a notable share of the European solar PV inverters market over the forecast period, owing to its ambitious net-zero targets and evolving energy policies. Although historical subsidy reductions slowed growth, recent initiatives such as the Smart Export Guarantee have revitalized interest in solar installations. As per the Department for Business, Energy and Industrial Strategy, the UK added approximately 1.5 gigawatts of new solar capacity in 2022, with significant contributions from commercial and industrial projects. The high cost of electricity has made self-consumption an attractive option for businesses, driving demand for commercial inverters. The residential sector is also recovering, with homeowners seeking to reduce energy bills through solar adoption. According to the Solar Trade Association, the UK market is seeing increased interest in battery storage systems, boosting sales of hybrid inverters. The government’s commitment to decarbonizing the grid by 2035 necessitates substantial increases in renewable energy capacity. Offshore wind and solar are key components of this strategy, with large-scale solar farms being developed across the country. The regulatory framework is becoming more supportive, with streamlined planning permissions for solar projects. The presence of experienced installers and financiers facilitates project execution. Additionally, the focus on energy security following global supply disruptions has elevated the priority of domestic renewable generation. The UK’s strategic shift towards renewable energy and supportive policy environment ensures steady growth in the demand for solar PV inverters, maintaining its relevant position in the European market.

COMPETITIVE LANDSCAPE

The competition in the Europe solar PV inverters market is intense and characterized by the presence of established global giants and agile regional specialists vying for dominance. Leading manufacturers compete on the basis of technological innovation, product reliability, and comprehensive after-sales support. The market sees continuous advancements in inverter efficiency, grid compatibility, and smart connectivity features as companies strive to offer superior value propositions. Price competition remains significant, particularly in the residential segment, prompting firms to optimize production costs and supply chain efficiencies. Differentiation is achieved through specialized solutions such as hybrid inverters for battery storage and micro inverters for complex roof layouts. Regulatory compliance with varying national grid codes serves as a critical barrier to entry, favoring incumbents with extensive certification portfolios. Collaborations with local installers and distributors are essential for market penetration and brand loyalty. The rapid pace of technological change requires constant investment in research and development to stay ahead. New entrants from Asia challenge European manufacturers with competitive pricing, forcing local players to emphasize quality, security, and sustainability. This dynamic environment drives continuous improvement and innovation, benefiting consumers through better performance and lower costs while shaping the future of renewable energy infrastructure in Europe.

KEY MARKET PLAYERS

The leading companies operating in the Europe solar PV inverters market include:

- Fimer SpA

- Fronius International GmbH

- Siemens AG

- Huawei Technologies Co Ltd

- SMA Solar Technology AG

- Mitsubishi Electric Corporation

- General Electric Company

- Schneider Electric SE

TOP PLAYERS IN THE MARKET

- SMA Solar Technology AG is a pioneering German manufacturer that has significantly shaped the global solar inverter landscape through its robust engineering and innovation. The company provides a comprehensive portfolio of string and central inverters tailored for residential, commercial, and utility-scale applications across Europe. SMA contributes to the global market by setting high standards for efficiency, reliability, and grid compatibility in photovoltaic systems. Recent actions to strengthen its position include the expansion of its production facilities in Germany to meet surging European demand and the launch of next-generation hybrid inverters with enhanced battery integration capabilities. The company focuses heavily on research and development to introduce smart energy management solutions that optimize self-consumption. By emphasizing local manufacturing and service networks, SMA ensures rapid response times and strong customer support, reinforcing its reputation for quality and durability in the competitive European market while maintaining its status as a trusted global brand.

- Huawei Technologies Co Ltd has emerged as a dominant force in the Europe solar PV inverters market by leveraging its expertise in digital power and artificial intelligence. The company offers smart string inverters that integrate advanced monitoring and optimization features, enhancing energy yield and system safety. Globally, Huawei drives innovation by combining photovoltaic technology with digital connectivity, enabling intelligent operation and maintenance for large-scale solar plants. To strengthen its market position in Europe, Huawei has established local partnerships with distributors and installers to expand its reach and provide tailored solutions for regional regulatory requirements. The company recently introduced upgraded fusion solar solutions that improve efficiency and reduce the levelized cost of energy. Its focus on cybersecurity and grid stability addresses key concerns of European utilities and regulators. By continuously innovating in power electronics and digital technologies, Huawei maintains a competitive edge and supports the continent's transition to sustainable energy systems through reliable and smart inverter products.

- Fronius International GmbH is an Austrian company renowned for its high-quality solar charging and inverter solutions, contributing significantly to the global adoption of renewable energy. The company specializes in string inverters for residential and commercial sectors, known for their snap-inverter design that simplifies installation and maintenance. Fronius plays a vital role in the global market by promoting energy independence through efficient and user-friendly photovoltaic systems. In Europe, Fronius strengthens its position by focusing on hybrid inverter technologies that seamlessly integrate with battery storage systems, catering to the growing demand for self-sufficiency. Recent initiatives include the expansion of its production capacity in Austria and the introduction of new software tools for enhanced system monitoring and control. The company emphasizes sustainability in its manufacturing processes and product lifecycle, aligning with European environmental values. By prioritizing innovation, quality, and customer-centric design, Fronius continues to be a preferred choice for installers and homeowners seeking reliable and efficient solar energy solutions in the European market.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe solar PV inverters market primarily focus on product innovation and technological advancement to maintain a competitive advantage. Companies invest heavily in research and development to create high-efficiency inverters with smart features such as artificial intelligence-driven monitoring and predictive maintenance. Strategic partnerships with battery manufacturers and energy management software providers enable the offering of integrated, holistic energy solutions. Expansion of local manufacturing and assembly facilities helps mitigate supply chain risks and reduces lead times for European customers. Firms also prioritize compliance with stringent grid codes and cybersecurity standards to build trust with utilities and regulators. Marketing efforts emphasize reliability, longevity, and after-sales service to differentiate brands in a crowded marketplace. Additionally, companies engage in strategic acquisitions to broaden their product portfolios and access new customer segments. These strategies collectively enhance market presence and ensure long-term growth by addressing the evolving needs of residential, commercial, and utility-scale solar projects across the diverse European landscape.

MARKET SEGMENTATION

This research report on the Europe solar PV inverters market has been segmented and sub-segmented into the following categories.

By Type

- Central Inverters

- String Inverters

- Micro Inverters

By Application

- Residential

- Commercial & Industrial

- Utility-scale

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe solar PV inverters market?

The Europe solar PV inverters market provides equipment converting solar panel DC output to AC power for homes, businesses, and utility grids across the region.

How does the Europe solar PV inverters market function?

The Europe solar PV inverters market functions by optimizing solar energy conversion, grid synchronization, and monitoring performance through string, central, and hybrid systems.

What drives growth in the Europe solar PV inverters market?

The Europe solar PV inverters market grows due to renewable targets, rooftop solar expansion, energy storage integration, and government incentives across member states.

Which countries lead the Europe solar PV inverters market?

Germany dominates the Europe solar PV inverters market, followed by Italy, Spain, France, and the UK with strong residential and commercial solar adoption.

What types define the Europe solar PV inverters market?

The Europe solar PV inverters market includes string inverters, central inverters, microinverters, and hybrid models supporting battery storage integration.

What applications shape the Europe solar PV inverters market?

The Europe solar PV inverters market serves residential rooftops, commercial installations, utility-scale solar farms, and hybrid systems with energy storage.

How does regulation influence the Europe solar PV inverters market?

EU renewable directives, grid codes, and feed-in tariffs shape the Europe solar PV inverters market by setting technical standards and deployment incentives.

What trends affect the Europe solar PV inverters market?

The Europe solar PV inverters market sees growth in hybrid inverters, smart monitoring, higher efficiency modules, and local manufacturing initiatives.

What challenges face the Europe solar PV inverters market?

The Europe solar PV inverters market faces supply chain issues, grid integration complexity, competition from Asian manufacturers, and policy uncertainty.

How do string inverters fit the Europe solar PV inverters market?

String inverters dominate the Europe solar PV inverters market for residential and small commercial use due to cost-effectiveness and reliable performance.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com