Europe Submersible Pump Market Size, Share, Trends & Growth Forecast Report By Type, By Drive Type, By End-User, and By Country (Germany, France, United Kingdom, Italy, Spain & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Submersible Pump Market Size

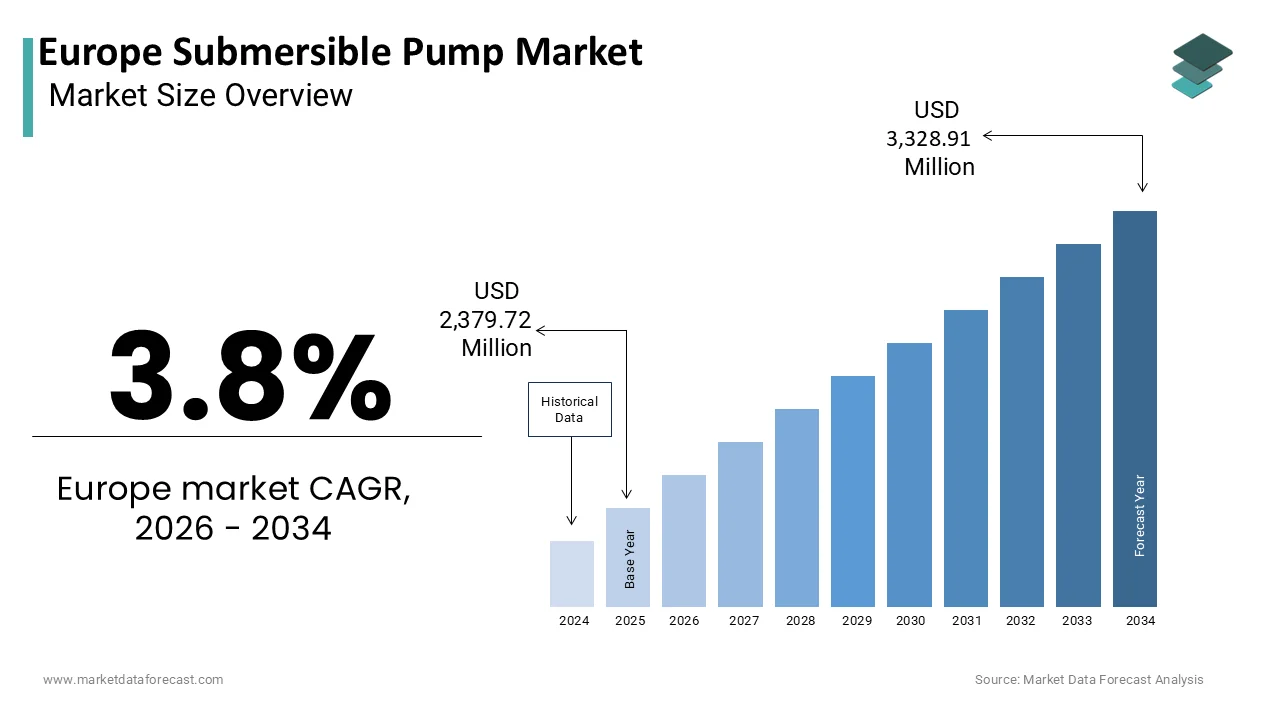

The Europe submersible pump market was valued at USD 2,379.72 million in 2025, is estimated to reach USD 2,470.15 million in 2026, and is projected to reach USD 3,328.91 million by 2034, growing at a CAGR of 3.8% from 2026 to 2034.

A submersible pump is a mechanical device designed to operate while completely submerged in the fluid it is meant to move. These pumps are integral to various applications, including wastewater management,t agricultural irrigation, mining operations, and residential water supply systems. The unique design prevents cavitation and eliminates the need for priming, making them highly efficient for deep well and sewage applications. The operational context of this market is deeply influenced by the region’s extensive urbanization and stringent environmental regulations. As per Eurostat, approximately 75% of the European population resides in urban areas, creating a substantial demand for efficient wastewater removal and drainage solutions. Furthermore, the aging infrastructure in many European cities necessitates regular upgrades and replacements of pumping systems. According to the EEA and the Council of the EU, while 92% of urban wastewater is now satisfactorily treated, infrastructure upgrades are still required to address new pollutants and achieve the EU's 2050 zero-pollution goal. Climate change also plays a critical role in the increased frequency of heavy rainfall events, leading to flooding risks. The Joint Research Centre indicates that flood damage in Europe could increase significantly by the end of the century if adaptation measures are not implemented. This reality drives the installation of robust submersible pumps in flood defense systems. Besides, according to the European Parliament, the agricultural sector accounts for over 80% of total water use in some Southern European regions, relying heavily on submersible pumps to access stable groundwater reserves. These factors collectively define the operational landscape and strategic importance of submersible pumps in maintaining water security and sanitation standards across the continent.

MARKET DRIVERS

Expansion of Municipal Wastewater Treatment Infrastructure Drives Demand

The continuous expansion and modernization of municipal wastewater treatment facilities accelerate the growth of the Europe submersible pump market. Strict regulatory frameworks such as the Urban Wastewater Treatment Directive mandate higher efficiency in sewage collection and treatment processes. Regional regulations mandate that populated areas maintain systems for gathering and processing runoff to protect public health and the environment. This regulatory pressure necessitates the installation of high-performance submersible pumps capable of handling solid-laden fluids and operating continuously under harsh conditions. Financial institutions indicate that significant annual capital is required to modernize these systems across the continent. A significant portion of this investment is allocated to upgrading pumping stations and replacing outdated equipment with energy-efficient models. Submersible pumps are preferred in these applications due to their compact design and ability to operate silently underwater, reducing noise pollution in urban environments. Studies observe that the regular need to upgrade mechanical components ensures consistent activity for equipment providers. Moreover, the push towards circular economy principles encourages the recovery of resources from wastewater, which requires sophisticated pumping systems to manage sludge and biosolids. Thus, the ongoing commitment to improving sanitation standards and environmental protection directly fuels the procurement of advanced submersible pumping technologies across European municipalities.

Increasing Frequency of Extreme Weather Events and Flood Management Needs

The rising incidence of heavy rainfall and flooding is a key contributor to the expansion of the Europe submersible pump market. These units are crucial in modern flood management and drainage applications. Climate change has altered precipitation patterns in Europe, leading to more intense and frequent storm events that overwhelm traditional drainage systems. Environmental monitors report that extreme weather events result in substantial annual financial burdens for the regional economy. To mitigate these risks, cities and regions are investing heavily in resilient water management infrastructure, including enhanced pumping capabilities. Submersible pumps are essential in stormwater pumping stations where they rapidly remove excess water from low-lying areas and prevent urban flooding. Official climate strategies advocate for integrating natural landscapes with traditional engineering to protect communities from rising water levels. Scientific projections indicate that the threat of overflowing river systems will intensify significantly in the coming decades if protective measures are not enhanced. This projection prompts local authorities to upgrade existing drainage networks with high-capacity submersible pumps that can handle sudden surges in water volume. Additionally, the construction of new residential and commercial complexes in flood-prone areas requires compliant drainage systems equipped with reliable pumping units. The urgency to protect property and public safety from water damage ensures a consistent demand for robust and efficient submersible pumping solutions in the European market.

MARKET RESTRAINTS

High Energy Consumption and Operational Costs Restrain Market Growth

These pumps are significant consumers of electricity, despite their inherent efficiency, which inhibits the growth of the Europe submersible pump market. As a result, rising energy costs and stringent sustainability targets in Europe pose a substantial constraint on their usage. Pumping systems account for nearly double the stated percentage of global electricity consumption (approx. 20%), a figure widely cited by major industrial technology companies like ABB rather than the International Energy Agency. In Europe, where energy prices have experienced volatility and upward trends, operators face increasing operational expenditures. High energy costs discourage the replacement of existing systems with new units unless the energy savings are substantial and immediate. Many small and medium-sized enterprises in the agricultural and industrial sectors operate on tight margins and may delay upgrades to avoid capital expenditure and higher running costs. As per Eurostat, the price of electricity for non-household consumers in the EU increased significantly more than 30 percent (peaking at record highs) in 2022 compared to the previous year, driven by the energy crisis. This financial pressure makes the total cost of ownership a critical decision factor, slowing down market penetration for premium high-efficiency models. Although energy-efficient pumps offer long-term savings, the initial investment is often higher, creating a barrier for budget-constrained buyers. Furthermore, the complexity of integrating variable speed drives and smart controls to optimize energy usage adds to the upfront cost. Without sufficient financial incentives or subsidies, many potential customers hesitate to adopt advanced submersible pump technologies. This economic constraint limits the rate of market growth as users prioritize short-term cost containment over long-term efficiency gains.

Stringent Environmental Regulations on Material Composition and Disposal

Strict environmental regulations regarding the materials used in pump manufacturing and the disposal of end-of-life equipment act as a significant restraint on the European submersible pump market. The European Union’s Restriction of Hazardous Substances Directive and Waste Electrical and Electronic Equipment Directive impose rigorous standards on the use of certain chemicals and the recycling of electronic components. Compliance with these regulations requires manufacturers to invest in research and development for eco-friendly materials and sustainable production processes. Various sources indicate that the registration and evaluation of new substances under the European Chemicals Agency (REACH regulation) frameworks can be time-consuming and costly, potentially delaying product launches. Manufacturers must ensure that seals, impellers, and motors do not contain prohibited substances, which can limit material choices and increase production costs. Additionally, the disposal of old pumps requires specialized handling to prevent environmental contamination, adding to the lifecycle cost for users. According to the European Commission, the transition to a circular economy requires products to be designed for durability, reparability, and recyclability. Achieving these design goals often involves complex engineering solutions that raise the price of the final product. Small manufacturers may struggle to meet these compliance requirements, leading to market consolidation and reduced competition. The administrative burden and financial implications of adhering to evolving environmental standards can slow down innovation and market entry for new players, thereby restraining overall market dynamism.

MARKET OPPORTUNITIES

Integration of Internet of Things and Smart Pumping Technologies Presents Opportunities

Integrating IoT technology into pumps enables predictive maintenance and remote monitoring. This advancement offers a significant opportunity for the Europe submersible pumps market growth. Smart pumps equipped with sensors can transmit real-time data on performance metrics such as vibration, temperature, and flow rate to central management systems. Studies indicate that the adoption of digital water technologies can significantly reduce operational expenditures and improve efficiency, with reports from Global Water Intelligence highlighting that these technologies can improve energy efficiency by more than 15%. This capability allows operators to detect issues before they lead to catastrophic failures, minimizing repair costs and service interruptions. The European Union’s Digital Decade policy aims to ensure that by 2030, 75% of EU companies take up cloud computing services, big data, or artificial intelligence. This digital transformation trend creates a favorable environment for the adoption of smart submersible pumps in industrial and municipal applications. According to a study, the adoption of digital water technologies is shown to improve energy efficiency by more than 15%, while specific smart pumping solutions from vendors like Siemens can also deliver similar energy savings. The ability to optimize pump operation based on real-time demand data further enhances energy savings. Moreover, smart pumps facilitate better resource management by providing accurate data for billing and regulatory reporting. As connectivity becomes more ubiquitous and affordable, the demand for intelligent pumping solutions is expected to rise. Manufacturers who innovate in this space can differentiate their offerings and capture value-added service revenue streams, driving market expansion.

Growth in Renewable Energy Applications and Geothermal Systems Creates New Avenues

The expanding renewable energy sector, particularly geothermal heating and cooling systems, provides a potential prospect for the European submersible pump market. Geothermal systems rely on submersible pumps to circulate fluids through underground loops for heat exchange, offering a sustainable alternative to fossil fuel-based heating. As per the European Geothermal Energy Council, the sector is targeting rapid expansion, while the European Union's RePowerEU plan has set a specific target to install 30 million heat pumps by 2030. This growth trajectory drives the demand for specialized submersible pumps capable of operating in high-temperature and corrosive environments. The European Green Deal aims to make Europe climate neutral by 2050, which incentivizes the adoption of renewable heating solutions in residential and commercial buildings. According to Eurostat, the share of renewable energy in gross final consumption of energy in the EU reached 23 percent in 2022. This shift towards sustainable energy sources increases the installation of ground source heat pumps, which require reliable submersible circulation pumps. Furthermore, government subsidies and tax incentives for green building projects encourage property developers to integrate geothermal systems. The durability and efficiency of submersible pumps make them ideal for these long-term installations. As the construction sector aligns with sustainability goals, the demand for pumps compatible with renewable energy infrastructure will continue to grow. This segment offers manufacturers a chance to diversify their product portfolios and tap into a rapidly expanding market driven by environmental consciousness and policy support.

MARKET CHALLENGES

Supply Chain Disruptions and Raw Material Volatility Pose Significant Challenges

Supply chain disruptions and volatility in raw material prices are slowing down the growth of the Europe submersible pump market. The manufacturing of submersible pumps relies heavily on metals such as stainless steel, cast iron, and copper, as well as rare earth elements for motors. As per the European Central Bank, producer prices for intermediate goods have experienced significant fluctuations in recent years due to geopolitical tensions and logistical bottlenecks. These price instabilities make it difficult for manufacturers to maintain consistent profit margins and plan long-term production schedules. The dependence on imports for certain critical components exposes the supply chain to global risks, including trade restrictions and transportation delays. According to the European Investment Bank (EIB), supply chain resilience has become a top priority, but achieving it requires substantial investment in diversification and inventory management. Shortages of semiconductor chips also affect the production of smart pumps and variable frequency drives, which are increasingly common in modern designs. These disruptions can lead to longer lead times and delayed project completions, affecting customer satisfaction. Additionally, the carbon footprint associated with transporting raw materials and finished goods is under scrutiny, requiring companies to optimize logistics for sustainability. Balancing cost efficiency with supply chain reliability remains a complex challenge. Manufacturers must navigate these uncertainties while meeting customer demands for timely delivery and competitive pricing. Failure to manage these risks effectively can result in lost market share and reduced profitability.

Shortage of Skilled Labor for Installation and Maintenance Hinders Market Efficiency

A persistent shortage of skilled labour for the installation, maintenance, and repair of these pumps is a serious obstruction to the European submersible pump market. The complexity of modern submersible systems, especially those integrated with digital control,s requires technicians with specialized training in both mechanical and electrical disciplines. As per the European Centre for the Development of Vocational Training,g there is a growing mismatch between the skills available in the workforce and the demands of advanced manufacturing and service sectors. This skills gap leads to delays in project execution and increased labor costs as companies compete for qualified personnel. Incorrect installation or poor maintenance can significantly reduce the lifespan and efficiency of pumps, leading to higher operational costs for end users. According to GCP Europe, the aging workforce in the trades sector is exacerbating the shortage as fewer young people enter these professions. The lack of standardized training programs across different European countries further complicates the availability of competent technicians. This challenge is particularly acute in rural areas where access to specialized service providers is limited. Without an adequate pool of skilled workers, the full benefits of advanced submersible pump technologies cannot be realized. Manufacturers and industry bodies must collaborate to develop training initiatives and apprenticeship programs to address this deficit. The labor shortage represents a significant constraint on market growth and customer satisfaction. This barrier will persist until the shortage is mitigated.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Drive Type, End-User, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Borets International Ltd., Gorman-Rupp Co., Flowserve Corporation, Sulzer AG, Schlumberger Limited, Baker Hughes Company, Halliburton Company, Weir Group PLC, Grundfos Holding A/S, Atlas Copco AB, EBARA Corporation, KSB SE & Co. KGaA |

SEGMENTAL ANALYSIS

By Type Insights

The non-clog clog submersible pump segment led the Europe submersible pump market and captured a 42.1% share in 2025. This leading position of the segment is mainly driven by the extensive municipal wastewater infrastructure and stringent environmental regulations requiring efficient sewage handling. The dominance of on-clogog submersible pumps is heavily influenced by the continuous modernization of urban wastewater treatment plants across Europe. These pumps are specifically designed to handle solids and debris without clogging, ng making them indispensable for sewage applications. As per the European Commission, ion the Urban Wastewater Treatment Directive requires all member states to ensure proper collection and treatment of urban wastewater, which drives the installation of robust pumping systems. The European Investment Bank states that approximately 100 billion euros are needed annually to upgrade water infrastructure in the EU, with a significant portion allocated to wastewater management. Non-clogging pumps are preferred in these facilities due to their ability to maintain consistent flow rates despite the presence of solid waste. Market best practices highlight a shift toward replacing legacy pumping infrastructure with high-performance units to lower operational costs and decrease energy usage. The average lifespan of these pumps in harsh sewage environments is around 10 to 15 years, rs creating a steady replacement market. Furthermore, Eurostat shows that a large portion of the population resides in urban and intermediate areas, which increases the demand for municipal wastewater processing. This necessitates reliable pumping solutions that can operate continuously without failure. The regulatory push for zero untreated discharge further compels municipalities to invest in advanced non-clogging pump technology, es ensuring this segment remains the largest contributor to market revenue. A further key factor driving the dominance of non-clog submersible pumps is the increasing need for effective stormwater management in the face of climate change. Heavy rainfall events often carry large amounts of debris into drainage systems, ms requiring pumps that can handle mixed fluids without blockage. The European Environment Agency reveals that flooding accounts for a significant portion of economic damage from climate events, necessitating more resilient public infrastructure. Non-clogging submersible pumps are integral to stormwater pumping stations, ns where they prevent urban flooding by rapidly removing excess water. The Joint Research Centre predicts that flood risks in Europe could double by 2050 if adaptation measures are not implemented. This projection has led to increased public investment in drainage infrastructure equipped with high-capacity non-clogging pumps. According to the European Union Adaptation Strategy, all member states are encouraged to integrate gray infrastructure, re such as a pump-sum with nature-based solutions to enhance resilience. Cities like Rotterdam and Copenhagen have implemented advanced stormwater systems relying on robust non-clogging pumps to manage extreme weather events. The ability of these pumps to handle variable flow rates and solid content makes them the preferred choice for flood defense mechanisms. Hence, the growing frequency of extreme weather events sustains high demand for on-clog submersible pumps, ps securing their leading market position.

The borewell submersible pump segment is estimated to register the fastest CAGR of 6.8% between 2026 and 20,,34 owing to the increasing reliance on groundwater for agricultural irrigation and domestic supply in water-stressed regions. In addition, the main driver for the rapid growth of borewell submersible pumps is the escalating water scarcity in Southern and Central Europe, pe which forces farmers to rely more heavily on groundwater extraction. Agriculture accounts for more than 60 percent of total water abstraction in Southern European countries like Spain and Italy, according to the European Environment Agency. As surface water sources become unreliable due to drought,hts farmers are drilling deeper wells, ls requiring efficient borewell submersible pumps. The European Commission’s Common Agricultural Policy encourages sustainable water use but also supports investments in efficient irrigation infrastructure. According to Eurostat, the area equipped for irrigation in the EU has remained stable, le but the intensity of groundwater usage has increased significantly. Borewell pumps are ideal for these applications due to their ability to lift water from great depths with high efficiency. The shift towards precision agriculture also demands reliable water supply systems that can be integrated with automated irrigation controls. As per the Food and Agriculture Organization of the United Nations, ns groundwater provides drinking water for at least 50 percent of the global population and irrigates about 40 percent of all irrigated agriculture. In Europe, pe this trend is mirrored as farmers seek to secure their water supply against climate variability. The durability and energy efficiency of modern borewell pumps make them a cost-effective solution for long-term agricultural productivity, ty driving their accelerated adoption. The growing trend of decentralized water supply systems in rural and semi-urban areas is another key factor boosting the borewell submersible pump segment. Many households in Europe are installing private wells to reduce dependence on municipal water supplies and lower utility bills. As per the World Health Organization, approximately 15 percent of the European population relies on small water supplies or private wells for their drinking water. This number is higher in rural regions where centralized infrastructure is less developed or expensive to extend. Borewell submersible pumps are the standard choice for these domestic applications due to their compact size and quiet operation. The European Union Drinking Water Directive emphasizes the quality of water from small supplies,s encouraging homeowners to invest in reliable extraction equipment. According to Eurosta, the rising water tariffs in several European countries have made private well installation more economically attractive for residents. Additionally,lly the increasing awareness of water conservation self-sufficiency drives the adoption of household rainwater harvesting and groundwater extraction systems. Manufacturers are responding by offering user-friendly, energy-efficient borewell pumps tailored for residential use. The ease of installation and low maintenance requirements further appeal to individual consumers. More households are seeking independence from public utilities. Consequently, the demand for borewell submersible pumps is rising faster than other segments.

By Drive Type Insights

The electric drive segment dominated the Europe submersible pump market and occupied a substantial share in 2025. This overwhelming prevalence is driven by the widespread availability of electrical infrastructure and the superior efficiency of electric motors in continuous operation applications. The supremacy of electric drive submersible pumps is fundamentally supported by the extensive and reliable electrical grid infrastructure present across Europe. Unlike hydraulic or mechanical drives, es electric pumps offer higher energy efficiency and lower operational complexity, ty which aligns with the region’s strict energy conservation goals. As per the International Energy Agency, electricity accounts for a prominent and growing share of final energy consumption in the European Union, with industrial and residential sectors being major users. Electric submersible pumps are preferred because they can be easily integrated with variable frequency drives to optimize energy usage based on demand. According to Eurostat, the average electricity price for industrial consumers has stabilized after recent volatility ty making electric operations predictable and manageable. The efficiency of electric motors has improved significantly, ly with premium efficiency classes becoming mandatory under EU ecodesign regulations. This regulatory framework ensures that new pumps consume less energy, thereby reducing the total cost of ownership for users. Furthermore, the simplicity of electric drive systems reduces maintenance requirements compared to hydraulic alternatives,ives which involve complex fluid circuits. The European Committee of Manufacturers of Electrical Machines and Power Electronics reports that optimizing motor systems, particularly through the use of variable speed drives, can yield significant energy savings in pumping applications. This significant savings potential,ntial combined with the ease of control and monitoring,toring makes electric drives the default choice for most submersible pump installations in Europe. The increasing integration of renewable energy sources into the European power grid further solidifies the position of electric drive submersible pumps. Solar and wind energy production often requires flexible load management,t which electric pumps can provide through smart control systems. As per the European Commission, ion the share of renewables in the EU energy mix reached 23 percent in 2022 and is expected to grow significantly under the Green Deal. Electric submersible pumps can be powered directly by solar panels in remote agricultural or residential settings, reducing reliance on the main grid. This capability is particularly valuable in off-grid locations where diesel or hydraulic pumps would be less efficient and more polluting. According to SolarPower Europe, the installed solar capacity in Europe is expanding rapidly, creating opportunities for solar-powered pumping solutions. Electric drives are also compatible with smart grid technology, enabling demand response programs where pumps operate during periods of low electricity prices or high renewable generation. This flexibility enhances the economic viability of electric pumps and supports grid stability. The ability to monitor and control electric pumps remotely via Internet of Things platforms adds another layer of value. Europe is transitioning towards a decarbonized energy system. This shift ensures the continued dominance of electric drives in the submersible pump market, thanks to their compatibility with clean energy sources.

The hydraulic drive segment is anticipated to witness the fastest CAGR of 5.2% during the forecast period. This quick surge of the segment is propelled by specific industrial applications where high torque and explosion-proof capabilities are required. The rapid growth of hydraulic drive submersible pumps is largely driven by their inherent safety features in hazardous environments such as oil and gas facilities and chemical plants. Hydraulic motors do not produce sparks, ks making them ideal for explosive atmospheres where electric motors pose a risk. The European Union establishes strict regulations governing equipment used in potentially explosive atmospheres under the ATEX Directives, for which the European Agency for Safety and Health at Work provides implementation guidance. Industries dealing with flammable liquids or gases prefer hydraulic drives to mitigate the risk of ignition. The oil and gas sector in Europe, pe although transitioning, ng still maintains significant infrastructure requiring safe pumping solutions. The International Association of Oil and Gas Producers develops technical standards to enhance reliability and process safety in offshore operations, which industry experts cite as a key factor in the deployment of essential equipment systems. The ability of hydraulic pumps to handle high viscosity fluids and operate under extreme pressures also contributes to their adoption in specialized industrial processes. Furthermore, hydraulic drives offer high power density, ty allowing for compact designs in space-constrained environments. The European Chemical Industry Council identifies safety and sustainability as strategic priorities for the sector, which market analysts highlight as a primary driver for the adoption of efficient processing and pumping technologies. As industrial safety standards become more stringent,nt the demand for explosion-proof hydraulic submersible pumps continues to rise. This niche but critical application area ensures steady growth for the hydraulic drive segment despite the overall dominance of electric drives. Also, a key factor contributing to the fast growth of hydraulic drive submersible pumps is their ability to deliver high torque at low speeds, ds which is essential for heavy-duty mining and construction applications. These industries often require pumps to handle abrasive slurries and thick muds that demand robust mechanical performance. The European Raw Materials Alliance works to secure resilient value chains for critical raw materials and the circular economy, while the mining industry separately focuses on sustainable extraction methods that utilize advanced fluid handling systems. Hydraulic drives provide the necessary power to operate large impellers in challenging conditions without the risk of motor burnout. The construction industry also utilizes hydraulic submersible pumps for dewatering excavation sites, es where reliability is crucial to prevent project delays. The European Construction Industry Federation reports that infrastructure projects frequently face challenges such as tight deadlines and labor shortages, which increase the operational pressure to maintain continuous site productivity. Hydraulic systems are known for their durability and ability to withstand shock loads and harsh operating environments. Additionally, ly hydraulic power packs can serve multiple tools simultaneously,, ly offering versatility on construction sites. The ability to vary speed and torque precisely allows operators to optimize pumping performance for different materials. As infrastructure investment increases across Europe to support green transition projects,s the demand for heavy-duty hydraulic pumping solutions is expected to grow. This specific industrial need drives the faster expansion of the hydraulic drive segment compared to other types.

By End User Insights

The water and wastewater segment held the majority share of 55.2% of the Europe submersible pump market in 2025. This prominence of the segment is supported by the critical need for efficient water distribution and sewage treatment in densely populated urban areas. The leading position of the water and wastewater segment is primarily sustained by stringent regulatory mandates requiring improved sewage treatment standards across Europe. The European Union Urban Wastewater Treatment Directive sets clear targets for the collection and treatment of urban wastewater,ter compelling municipalities to upgrade their infrastructure. As per sources, billions of euros are invested annually in wastewater treatment plants to comply with these regulations. Submersible pumps are essential components in these facilities for moving raw sewage sludge and treated effluent. Non-clogging submersible pumps are particularly vital in this sector due to their ability to handle solid waste without frequent maintenance. According to research, the replacement of old pumping stations with energy-efficient models is a priority for many utilities. This ongoing modernization effort ensures a consistent demand for submersible pumps in the wastewater sector. Furthermore, re the push for resource recovery from wastewaters, er such biogas production requires reliable pumping systems to manage process flows. The regulatory landscape thus creates a stable and substantial market for submersible pumps in water and wastewater applications. Rapid urbanization and the subsequent expansion of water infrastructure in major European cities also drive the dominance of the water and wastewater segment. Cities are expanding their networks to accommodate growing populations requiring new pumping stations and pipeline upgrades. Submersible pumps are preferred for these applications due to their space-saving design and ability to operate underground. A study emphasizes that urban water infrastructure requires significant funding to maintain service quality and prevent leaks. European cities are investing in smart water grids that utilize advanced submersible pumps for real-time monitoring and control. This technological integration enhances the efficiency of water distribution and reduces non-revenue water. The construction of new residential and commercial complexes also contributes to the demand for submersible pumps for basement drainage and water supply. Urban centers across Europe continue to grow and modernize. Consequently, the water and wastewater sector remains the largest consumer of submersible pump technology.

The mining and construction industry segment is likely to experience the fastest CAGR of 6.5% over the forecast period. Elevated infrastructure spending combined with a revival in European strategic mining is fueling this segment's expansion. The fastest growth in this segment is driven by substantial infrastructure investments aimed at supporting Europe’s green transition. The European Green Deal requires massive construction of renewable energy facilities, electric vehicle charging networks, and energy-efficient buildings. Construction sites frequently require dewatering solutions to manage groundwater and rainwater,, er ensuring safe working conditions. Submersible pumps are essential for this purpose due to their portability and reliability. Various sources point out that the sector is experiencing a surge in activity driven by public and private investment. Additionally, the construction of underground transport systems and tunnels requires robust dewatering pumps to handle high water inflows. Submersible pumps are also used in concrete mixing and site cleaning operations. The scale and pace of these green infrastructure projects create a heightened demand for durable and efficient submersible pumps. As Europe accelerates the build-out of sustainable infrastructure, re the mining and construction sector will continue to drive rapid market growth. The resurgence of mining activities for critical raw materials in Europe is another key driver for the fast growth of this segment. The European Union has identified a list of critical raw materials essential for digital and green technologies, such as lithium, cobalt u,,m cobalt, and rare earth elements. Mining operations require extensive dewatering and slurry handling systems to extract minerals efficiently. Submersible pumps are widely used in open-pit and underground mines to remove water and transport ore slurries. The Critical Raw Materials Act aims to strengthen the EU’s supply chain for these materials,, ls leading to new mining projects. This policy supports investment in modern mining equipment, including high-performance submersible pumps. The harsh conditions in mining environments demand pumps that can handle abrasive materials and operate continuously. As new mines come online and existing ones expand their operations, the demand for specialized submersible pumps in the mining sector is accelerating. This strategic shift towards domestic resource extraction ensures sustained growth for the mining and construction end-user segment.

COUNTRY LEVEL ANALYSIS

Germany Submersible Pump Market Analysis

Germany outperformed other countries in the Europe submersible pump market and occupied a 20.5% share in 2025. High-quality pumping solutions are in demand due to the country’s strong industrial base and sophisticated manufacturing sector. Germany is home to several leading pump manufacturers, which fosters innovation and technical excellence. The German government’s focus on energy efficiency and environmental protection mandates the use of high-performance pumps in industrial and municipal applications. As per the Federal Ministry for Economic Affairs and Climate Action, industrial energy efficiency programs encourage the replacement of old pumps with premium efficiency models. The country’s extensive wastewater treatment infrastructure also contributes significantly to market demand. According to the German Water Partnership, the digitalization of water management is a key trend driving the adoption of smart submersible pumps. Major cities like Berlin and Hamburg are upgrading their drainage systems to cope with climate change impacts. The construction sector in Germany is also robust, st supported by government housing initiatives. According to the Federal Statistical Office, construction output has declined due to economic fluctuations. This steady activity ensures consistent demand for dewatering pumps. Germany’s commitment to sustainability and technological leadership positions it as the largest market for submersible pumps in Europe.

France Submersible Pump Market Analysis

France was the next prominent player in the Europe submersible pump market and held a 15.3% share in 2025. The nation’s extensive agricultural sector and nuclear power industry are key drivers of pump demand. France is one of the largest agricultural producers in Europe, ope requiring efficient irrigation systems. As per the French Ministry of Agriculture, true groundwater extraction for irrigation is common in regions prone to drought. Submersible pumps are essential for accessing deep water sources for crop production. The nuclear power sector also relies heavily on submersible pumps for cooling and water circulation processes. According to the French Nuclear Safety Authority,, ty strict safety standards require reliable pumping equipment for power plants. Additionally, France has a well-developed wastewater treatment network that undergoes regular upgrades. The French Environment and Energy Management Agency promotes energy-efficient technologies in water management. Urban development projects in Paris and other major cities also contribute to the demand for dewatering pumps. The country’s focus on renewable energy,gy including hydropower, er further supports the market. France’s diverse industrial and agricultural landscape ensures a steady and varied demand for submersible pumps.

United Kingdom Submersible Pump Market Analysis

The United Kingdom continues to be a noteworthy player in the Europe submersible pump market. Its aging water infrastructure and frequent rainfall propel the need for efficient pumping solutions. Water companies in the UK are under pressure to reduce leakage and improve sewage management. According to Ofwat, the water regulator is enforcing mandatory, wide-scale capital investment programs for water companies to improve network resilience and supply security over the coming years. Submersible pumps are critical for wastewater transport and stormwater management in urban areas. The UK experiences heavy rainfall, which often leads to flooding requiring robust drainage systems. As per the Environment Agency, government funding for flood and coastal risk management is reaching record-breaking levels to repair existing assets and construct new defenses for vulnerable properties. The construction sector in the UK is also active with numerous residential and commercial projects. The government’s housing targets drive construction activity, ty increasing the demand for dewatering pumps. Additionally, the oil and gas industry in the North Sea utilizes submersible pumps for offshore operations. The UK’s commitment to net zero emissions encourages the adoption of energy-efficient pumping technologies. These factors collectively sustain the UK’s significant position in the regional market.

Italy Submersible Pump Market Analysis

Italy witnessed a consistent growth in the Europe submersible pump market. Factors such as its significant agricultural sector and tourism industry are major contributors to pump demand. Italy faces water scarcity issues, especially in the south, which necessitates efficient irrigation systems. As per the Italian National Institute of Statistics (ISTAT), the agricultural sector is the primary consumer of the nation's water resources, far exceeding domestic and industrial usage. Submersible pumps are widely used for groundwater extraction to support crop production. The tourism industry also drives demand for water supply and wastewater management in coastal areas. Hotels and resorts require reliable pumping systems to ensure an adequate water supply for guests. According to Utilitalia, the water utility association, the strategic modernization of aging distribution networks is vital to address systemic leakages that currently waste a significant portion of the treated water supply. Italy also has a strong manufacturing base that utilizes submersible pumps for industrial processes. The construction sector benefits from government incentives for building renovation and energy efficiency. These initiatives increase the use of pumps for dewatering and heating systems. Italy’s unique combination of agricultural needs and tourism infrastructure supports a robust market for submersible pumps.

Spain Submersible Pump Market Analysis

Spain is anticipated to expand significantly in the Europe submersible pump market between 2026 and 2034. The country’s arid climate and extensive agricultural activities make it a key market for irrigation pumps. Spain is one of the most water-stressed countries in Europe,e relying heavily on groundwater for farming. According to the Spanish Ministry for Ecological Transition and Demographic Challenge (MITECO), agricultural irrigation represents the overwhelming bulk of total water demand across the country. Submersible pumps are essential for accessing deep aquifers to support fruit and vegetable production. The government promotes modern irrigation techniques to improve water efficiency. As per the National Federation of Irrigation Communities (FENACORE), there is a significant shift toward modernizing fields with pressurized irrigation methods and energy-efficient pumping systems powered by renewable energy. Tourism also plays a role in driving demand for water management solutions in coastal regions. Urban development in cities like Madrid and Barcelona requires advanced drainage and wastewater systems. The construction sector is recovering with new infrastructure projects underway. Spain’s focus on renewable energy includes solar-powered pumping solutions for remote agricultural areas. These factors ensure Spain remains a significant player in the European submersible pump market.

COMPETITIVE LANDSCAPE

The competition in the Europe submersible pump market is intense and characterized by the presence of several established global and regional players. Leading companies compete based on product quality, ty technological innovation, energy efficiency,e and after-sales service. The market exhibits a moderate level of consolidation as major manufacturers acquire smaller firms to expand their technological capabilities and geographic reach. Differentiation is achieved through the development of smart pumping solutions equipped with Internet of Things connectivity and predictive maintenance features. Price competition exists but is often secondary to the value proposition of reliability and operational efficiency. New entrants face high barriers to entry due to the need for significant capital investment and compliance with strict European standards. However, er niche players continue to emerge with specialized products for specific applications such as mining or agriculture. Collaborative ecosystems are becoming increasingly important as stakeholders seek interoperable solutions for complex water management challenges. The focus on sustainability and digital transformation drives continuous innovation and shapes the competitive landscape. Companies that successfully integrate these elements while maintaining strong customer relationships are best positioned to succeed in this dynamic market environment.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Submersible Pump Market include

- Borets International Ltd.

- Gorman-Rupp Co.

- Flowserve Corporation

- Sulzer AG

- Schlumberger Limited

- Baker Hughes Company

- Halliburton Company

- Weir Group PLC

- Grundfos Holding A/S

- Atlas Copco AB

- EBARA Corporation

- KSB SE & Co. KGaA

TOP LEADING PLAYERS IN THE MARKET

- Xylem Inc is a global leader in water technology with a strong presence in the Europe submersible pump market. The company offers a comprehensive portfolio of efficient and reliable pumping solutions for wastewater and water supply applications. Xylem contributes to the global market by driving innovation in smart water technologies and sustainable infrastructure. Recent actions include the launch of advanced non-clogging pumps with integrated sensors for real-time monitoring. These innovations help utilities reduce energy consumption and improve operational efficiency. Xylem also engages in strategic partnerships with local distributors to expand its reach in European markets. The company focuses on digital transformation by integrating its pumps with cloud-based analytics platforms. This approach enables predictive maintenance and enhances customer value. Xylem’s commitment to sustainability aligns with European regulatory standards, ds making it a preferred partner for municipalities and industries. Their continuous investment in research and development ensures they remain at the forefront of technological advancements in the sector.

- KSB SE & Co KGaA is a prominent manufacturer of pumps and valves with a significant footprint in the Europe submersible pump market. The company provides high-quality submersible motors and pumps for diverse applications, including mini, ng construction and wastewater treatment. KSB contributes globally by delivering customized solutions that meet specific customer requirements. Recent initiatives involve the expansion of production facilities in Germany to increase capacity and reduce lead times. The company has also introduced energy-efficient pump models compliant with strict European ecodesign regulations. KSB strengthens its market position through extensive service networks offering maintenance and repair support. Their focus on digitalization includes the development of smart pump systems with remote diagnostic capabilities. KSB collaborates with engineering firms to integrate its products into large-scale infrastructure projects. This strategy enhances their visibility and credibility in the industrial sector. KSB maintains a strong reputation by prioritizing quality and reliability. They are a top choice for European customers seeking durable pumping solutions.

- Grundfos Holding A/S is a leading pump manufacturer headquartered in Denmark with a dominant role in the Europe submersible pump market. The company is renowned for its innovative and energy-efficient pumping solutions for water and wastewater management. Grundfos contributes to the global market by setting benchmarks in sustainability and digital integration. Recent actions include the introduction of intelligent submersible pumps with built-in connectivity features. These products enable seamless integration into smart water grids and facilitate data-driven decision-making. Grundfos invests heavily in research and development to create environmentally friendly materials and designs. The company also expands its service offerings by providing comprehensive training and support to partners. Grundfos collaborates with utilities to implement pilot projects demonstrating the benefits of smart pumping technologies. Their commitment to circular economy principles drives the design of recyclable and long-lasting products. Grundfos is strengthening its European leadership by focusing on innovation and customer-centric solutions. This strategic approach drives their continued market success.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe submersible pump market primarily focus on product innovation and digital integration to maintain a n competitive advantage. Companies invest heavily in research and development to create energy-efficient and smart pumping solutions that comply with stringent environmental regulations. Strategic partnerships and collaborations with technology firms are common to enhance digital capabilities and offer comprehensive water management systems. Mergers and acquisitions are also utilized to expand product portfolios and enter new geographic markets within Europe. Manufacturers emphasize sustainability by developing eco-friendly materials and promoting circular economy practices in production processes. Additionally, companies strengthen their after-sales service networks to provide timely maintenance and support,, rt which enhances customer loyalty. Participation in industry exhibitions and trade shows helps firms showcase their latest technologies and build brand awareness. Pricing strategies often reflect the total cost of ownership rather than just the initial purchase price, highlighting long-term savings. These strategies collectively enable key participants to address evolving customer needs and regulatory requirements effectively.

MARKET SEGMENTATION

This research report on the europe submersible pump market is segmented and sub-segmented into the following categories:

By Type

- Non-Clog Submersible Pumps

- Borewell Submersible Pumps

- Openwell Submersible Pumps

- Slurry Submersible Pumps

- Utility / Dewatering Submersible Pumps

By Drive Type

- Electric Drive

- Hydraulic Drive

By End-User

- Water & Wastewater

- Agriculture

- Oil & Gas

- Mining & Construction

- Industrial

- Residential

By Country

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com