Europe Supercar Market Size, Share, Trends & Growth Forecast Report – Segmented By Vehicle Type, Propulsion, Engine Capacity, Power, Speed, Transmission, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Supercar Market Report Summary

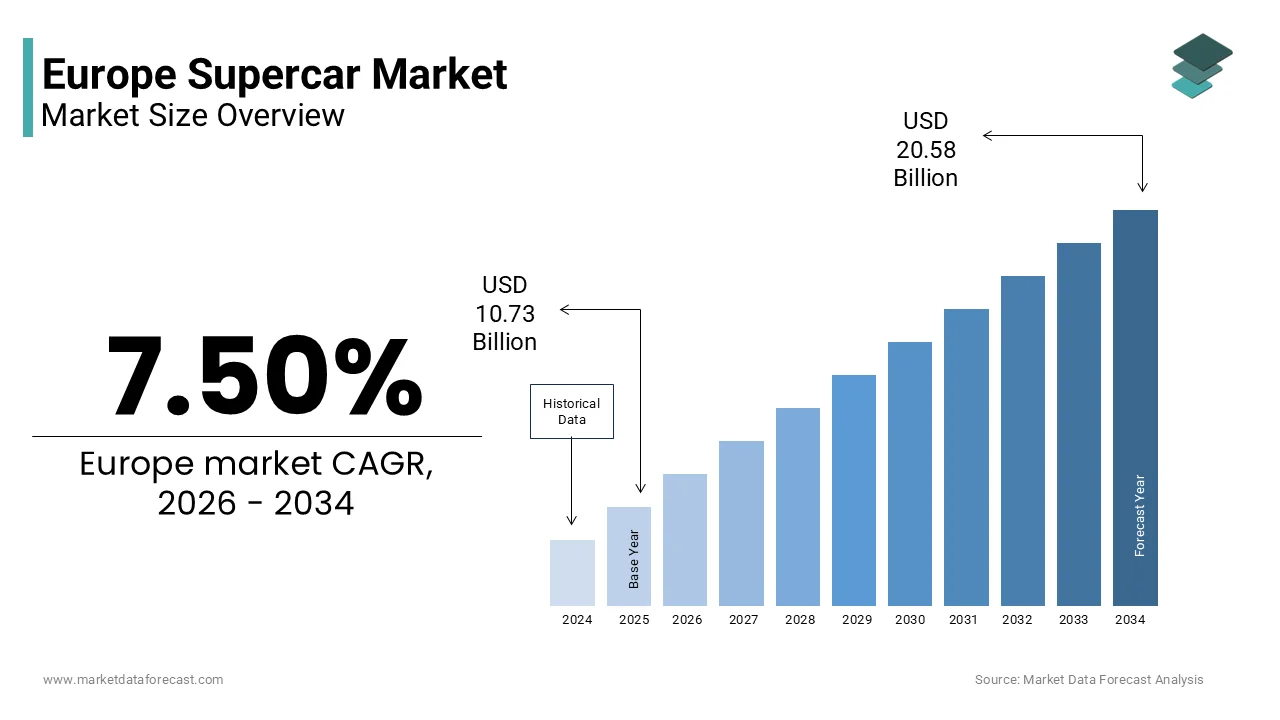

The Europe supercar market was valued at USD 10.73 billion in 2025, is estimated to reach USD 11.54 billion in 2026, and is projected to reach USD 20.58 billion by 2034, growing at a CAGR of 7.50% during the forecast period. The growth of the Europe supercar market is driven by rising demand for high performance luxury vehicles, increasing disposable incomes among affluent consumers, and strong brand appeal of premium automotive manufacturers. Technological advancements in engine performance, aerodynamics, and lightweight materials are further accelerating market expansion. Additionally, the growing influence of electric and hybrid supercars, along with expanding customization options, is enhancing consumer engagement and shaping the future of the market.

Key Market Trends

- Increasing demand for high performance coupe supercars driven by their aerodynamic design, speed capabilities, and strong consumer preference for two door luxury sports cars.

- Rising popularity of gasoline powered supercars due to their superior engine performance, sound experience, and established infrastructure support across Europe.

- Growing focus on hybrid and electric supercars as manufacturers shift towards sustainability and emission reduction regulations.

- Advancements in lightweight materials such as carbon fiber and aluminum to enhance speed, efficiency, and vehicle handling.

- Increasing demand for personalised and limited edition supercars among high net worth individuals seeking exclusivity and brand prestige.

Segmental Insights

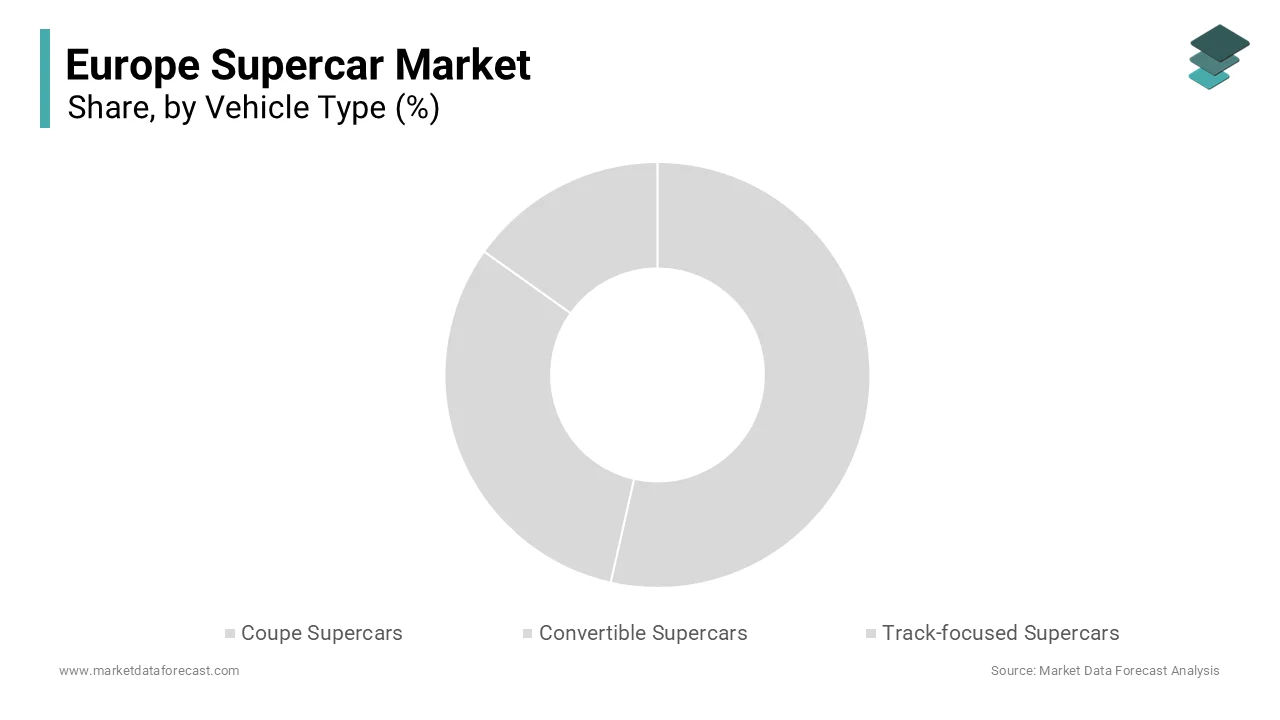

- Based on vehicle type, the coupe supercars segment dominated the Europe supercar market and held a share of 65.9% in 2025, driven by their superior performance, sleek design, and strong market preference among enthusiasts and collectors.

- Based on propulsion, the gasoline powered supercars segment was the largest and accounted for 55.8% of the Europe supercar market share in 2025, supported by high power output, established fueling infrastructure, and consumer inclination toward traditional performance engines.

- Based on engine capacity, the mid size 3000cc to 3999cc segment led the market with a 45.7% share in 2025, owing to its optimal balance between power, efficiency, and driving dynamics preferred in high performance vehicles.

Regional Insights

- The Europe supercar market is witnessing strong growth across key countries, supported by the presence of leading automotive manufacturers and a well established luxury vehicle ecosystem.

- Germany was the largest contributor, accounting for 22.6% of the Europe supercar market share in 2025, driven by its strong automotive industry, high consumer purchasing power, and technological innovation in performance vehicles.

Competitive Landscape

The Europe supercar market is highly competitive, characterized by the presence of globally recognized luxury and performance automotive brands focusing on innovation, performance enhancement, and exclusivity. Companies are investing in advanced engineering, electrification, and bespoke customization to strengthen their market position and attract elite consumers. Leading players in the Europe supercar market include Bugatti, Ferrari N.V., Automobili Lamborghini S.p.A., McLaren, Porsche, Aston Martin, Koenigsegg, Pagani, Rimac, Pininfarina, Lotus, Mercedes-AMG, Audi Sport, Lexus, Ford Performance, Maserati, Bentley, Rolls-Royce, and Dodge.

Europe Supercar Market Size

The Europe supercar market size was valued at USD 10.73 billion in 2025 and is projected to reach USD 20.58 billion by 2034 from USD 11.54 billion in 2026, growing at a CAGR of 7.50%.

A supercar is a high-performance, street-legal luxury sports car that sits at the top of the automotive hierarchy. They are defined by three main pillars: extraordinary speed, exotic design, and exclusive pricing. This market encompasses high performance machines typically producing over 600 horsepower and featuring advanced aerodynamics lightweight materials and cutting edge propulsion systems. The region serves as the historical and cultural heartland of supercar manufacturing hosting iconic brands such as Ferrari Lamborghini McLaren and Bugatti. Multiple studies indicate that the premium and luxury car segments have maintained resilience despite economic headwinds. This trend is driven by High Net Worth Individuals (HNWIs) who continue to invest in high-value, often personalized, automotive assets, distinct from the volume-based data tracked by associations like the ACEA. The definition of a supercar has evolved to include hybrid and fully electric powertrains reflecting the industry's shift towards sustainability without compromising performance. As per data from Altrata’s World Ultra Wealth Report 2024 (using Wealth-X data), the number of ultra-high-net-worth individuals in Europe increased by 9.4% in 2023, reaching approximately 115,000 individuals (surpassing Asia to become the second-largest ultra-wealth region), who form the primary customer base for these exclusive vehicles. The market is not merely about transportation but serves as a symbol of status technological prowess and artistic expression. Regulatory frameworks in Europe are increasingly stringent regarding emissions and noise levels prompting manufacturers to innovate with hybrid technologies. The presence of world class racing circuits and automotive events such as the Geneva Motor Show and Goodwood Festival of Speed further cements Europe's dominance in this niche sector. These factors create a unique ecosystem where heritage meets innovation driving continuous demand for limited edition models that appreciate in value over time.

MARKET DRIVERS

Accumulation of Wealth Among Ultra High Net Worth Individuals Fuels Demand

The consistent growth in wealth among ultra-high net worth individuals is the primary driver of the Europe supercar market. These individuals view the vehicles as both lifestyle assets and investment opportunities. This demographic possesses the disposable income necessary to purchase vehicles priced significantly above standard luxury cars often exceeding 300000 euros. According to the UBS Global Wealth Report 2024, the total wealth held by adults in Europe was estimated to be approximately 104 trillion US dollars in 2023, with the top 1 percent holding a substantial portion of this asset base. This concentration of wealth ensures a stable demand pool for exclusive automotive products that offer scarcity and prestige. Supercar manufacturers often produce limited editions with production runs capped at fewer than 500 units creating an artificial scarcity that drives desirability. For instance Ferrari’s strategy of limiting production to maintain brand exclusivity has resulted in long waiting lists and strong residual values. The psychological aspect of ownership also plays a crucial role as these vehicles serve as tangible symbols of success and social status. Furthermore the integration of bespoke customization programs allows buyers to personalize every aspect of their vehicle enhancing emotional attachment and willingness to pay premium prices. The resilience of this wealthy segment during economic downturns provides a buffer against market volatility ensuring steady sales volumes for flagship models. Wealth continues to concentrate in major European hubs like London, Zurich, and Monaco. Consequently, demand for high-performance automobiles remains robust and unaffected by broader consumer trends.

Technological Innovation in Hybrid and Electric Powertrains Attracts Enthusiasts

Technological advancements in hybrid and electric powertrains have revitalized interest in the European supercar market. They achieve this by offering unprecedented performance capabilities alongside environmental compliance. Traditional internal combustion engines are being supplemented or replaced by electric motors that provide instant torque and enhanced acceleration metrics. According to the International Energy Agency, sales of electric cars in Europe reached nearly 3.2 million units in 2023, accounting for more than 20 percent of total car sales, indicating a broader acceptance of electrified technologies. Supercar manufacturers are leveraging this trend to create vehicles that exceed previous performance benchmarks. For example the Ferrari SF90 Stradale combines a V8 engine with three electric motors to produce 1000 horsepower enabling acceleration from 0 to 100 kilometers per hour in just 2.5 seconds. This fusion of sustainability and performance appeals to a new generation of buyers who prioritize technological sophistication without sacrificing driving dynamics. The development of solid state batteries and advanced energy recovery systems further enhances the appeal of these vehicles by reducing weight and improving range. Regulatory pressures such as the Euro 7 emission standards also compel manufacturers to adopt cleaner technologies ensuring long term viability in the European market. The novelty of electric supercars attracts media attention and consumer curiosity driving showroom traffic and order books. This technological renaissance positions European manufacturers as leaders in high performance electrification distinguishing them from competitors in other regions.

MARKET RESTRAINTS

Stringent Emission Regulations Limit Engine Configuration Options

Increasingly stringent emission regulations are heavily restricting the European supercar market. As a result, the use of high-displacement internal combustion engines is under threat. The European Union’s Fit for 55 package aims to reduce greenhouse gas emissions by 55 percent by 2030 compared to 1990 levels posing significant challenges for manufacturers reliant on traditional powertrains. According to the European Environment Agency transport remains the only major sector where emissions have continued to rise necessitating aggressive policy interventions. These regulations force manufacturers to invest heavily in hybridization and electrification which can alter the characteristic sound and driving experience associated with supercars. The cost of compliance also increases vehicle prices potentially pricing out some enthusiasts. For instance the introduction of real driving emissions tests requires complex after treatment systems that add weight and reduce efficiency. Some manufacturers have already discontinued certain V12 and V8 models in favor of smaller turbocharged or hybrid units. The uncertainty surrounding future regulatory frameworks creates hesitation among buyers who fear rapid obsolescence or restricted usage in urban areas. Low emission zones in major cities such as Paris and London further limit the practicality of owning high performance vehicles. While hybrids offer a transitional solution the ultimate shift towards zero emission mandates may erode the traditional appeal of supercars. This regulatory pressure constrains product diversity and forces rapid technological transitions that may not align with consumer preferences for raw mechanical engagement.

Economic Volatility and Inflation Impact Discretionary Spending Patterns

Economic volatility and persistent inflation act as significant restraints on the Europe supercar market. These factors restrain growth by negatively affecting consumer confidence and discretionary spending patterns. Although ultra high net worth individuals are less sensitive to economic cycles prolonged periods of uncertainty can lead to cautious investment behavior. According to Eurostat, the average inflation rate in the Euro Area remained elevated throughout the previous year, impacting the general cost of goods and services and affecting the overall financial flexibility of households. This economic environment can delay large discretionary purchases such as supercars as buyers reassess their financial portfolios. Rising interest rates also increase the cost of financing for those who leverage loans to acquire vehicles making ownership more expensive. The volatility in global financial markets can impact the value of assets held by potential buyers leading to a temporary freeze in luxury spending. Additionally supply chain disruptions and increased raw material costs contribute to higher vehicle prices and longer delivery times which can deter impulsive purchases. The geopolitical tensions in Europe further exacerbate economic uncertainty affecting business investments and consumer sentiment. While the core demographic remains wealthy the broader economic context influences market liquidity and transaction volumes. Dealerships report longer sales cycles and increased negotiation periods as buyers become more price sensitive. This economic headwind restricts market growth and forces manufacturers to offer more flexible purchasing options to maintain sales momentum amidst uncertain financial conditions.

MARKET OPPORTUNITIES

Expansion into Digital Ownership and Non Fungible Tokens Creates New Revenue Streams

Digital ownership and non-fungible tokens are emerging as a massive opportunity for the European supercar market. This shift allows brands to engage younger demographics and significantly expand their reach. Manufacturers are exploring virtual showrooms and digital collectibles that allow enthusiasts to own unique digital assets associated with physical vehicles. According to Deloitte, luxury brands are increasingly utilizing digital innovations to build deeper emotional connections with tech-savvy consumers, viewing the digital realm as a vital landscape for relationship-based value creation. Supercar companies can launch limited edition digital models that grant owners exclusive access to events merchandise or even priority allocation for physical cars. This strategy enhances brand loyalty and creates a new revenue stream independent of physical production constraints. For instance Lamborghini has launched NFT collections that provide holders with unique experiences and community benefits. The integration of blockchain technology also enables transparent tracking of vehicle history and provenance enhancing resale value and trust. Virtual reality platforms allow potential buyers to configure and experience vehicles in immersive environments reducing the need for physical dealership visits. This digital transformation aligns with the growing metaverse trend where luxury goods are increasingly valued for their virtual presence. By embracing digital innovation European supercar brands can maintain relevance in a rapidly evolving cultural landscape. This approach also facilitates global marketing campaigns that transcend geographical boundaries attracting a diverse international audience to the European heritage of supercar manufacturing.

Development of Sustainable Materials Enhances Brand Image and Compliance

The adoption of sustainable materials in supercar construction offers a compelling opportunity for manufacturers to enhance their brand image and meet environmental expectations, which is likely to promote the expansion of the Europe supercar market. Consumers are increasingly conscious of the ecological footprint of luxury goods prompting demand for ethically sourced and recyclable components. According to the Ellen MacArthur Foundation the transition to a circular economy in the automotive sector could generate significant economic benefits while reducing waste. Supercar makers are incorporating bio based composites recycled carbon fiber and vegan leather interiors to reduce reliance on virgin materials. For example McLaren has introduced flax based composite materials that offer comparable strength to carbon fiber with a lower environmental impact. These innovations appeal to environmentally conscious buyers who seek luxury without compromising their values. The use of sustainable materials also helps manufacturers comply with upcoming regulations regarding end of life vehicle recycling and material sourcing. Marketing these eco friendly features differentiates brands in a crowded market and attracts positive media coverage. Collaborations with material science startups enable continuous innovation in lightweight and sustainable structures. This shift towards sustainability does not detract from performance but rather enhances it through advanced engineering solutions. By leading the way in green luxury European supercar brands can set new industry standards and attract a broader customer base. This strategic pivot ensures long term viability and relevance in a world increasingly focused on environmental responsibility and ethical consumption.

MARKET CHALLENGES

Supply Chain Disruptions for Specialized Components Delay Production Timelines

The vulnerability of supply chains for specialized components such as semiconductors and carbon fiber materials is a major challenge to the Europe supercar market. The complexity of supercar production requires precise coordination among numerous suppliers many of whom operate globally. According to the European Automobile Manufacturers Association, while supply chains stabilized for a period, the industry continues to face episodic logistics and component disruptions that threaten production consistency across the region. These disruptions result in extended waiting periods for customers which can lead to order cancellations and dissatisfaction. The reliance on single source suppliers for critical technologies increases the risk of production halts if any link in the chain fails. Geopolitical tensions and trade restrictions further complicate the procurement of raw materials and components. For instance restrictions on rare earth elements used in electric motors and batteries can impact the production of hybrid and electric supercars. Manufacturers must invest in inventory buffering and supplier diversification to mitigate these risks which increases operational costs. The Just in Time manufacturing model prevalent in the industry is particularly susceptible to such shocks requiring a strategic shift towards more resilient supply chain practices. Delayed deliveries also affect cash flow and financial planning for manufacturers. Ensuring consistent availability of high quality components is essential for maintaining brand reputation and customer trust. Addressing these supply chain vulnerabilities remains a critical operational challenge for European supercar makers striving to meet demand in an unpredictable global environment.

Retention of Skilled Craftsmanship Amidst Technological Transition

Retaining skilled craftsmanship and engineering talent amidst a rapid transition towards electrification and digitalization remains an impediment to the European supercar market. Traditional supercar manufacturing relies heavily on artisanal skills for hand assembling engines shaping body panels and customizing interiors. According to the European Commission there is a growing skills gap in the automotive sector as the industry shifts towards software defined vehicles. Younger engineers and technicians are often more attracted to tech industries than traditional manufacturing leading to a shortage of specialized labor. The loss of experienced craftsmen who possess tacit knowledge of internal combustion engines threatens the heritage and quality associated with European supercars. Retraining existing workforce members to handle high voltage systems and software integration requires significant time and investment. Additionally the competitive labor market drives up wages increasing production costs. Manufacturers must balance the preservation of traditional craftsmanship with the adoption of new technologies to maintain their unique value proposition. Failure to address this human capital challenge could result in a decline in build quality and brand authenticity. Collaborations with technical universities and apprenticeship programs are essential to cultivate the next generation of automotive experts. Preserving the cultural heritage of supercar manufacturing while embracing modern engineering practices is a delicate balancing act. Ensuring a steady pipeline of talented individuals is crucial for sustaining the excellence and innovation that define the Europe supercar market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.50% |

| Segments Covered | By Vehicle Type, Propulsion, Engine Capacity, Power, Speed, Transmission, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Bugatti, Ferrari N.V., Automobili Lamborghini S.p.A., McLaren, Porsche, Aston Martin, Koenigsegg, Pagani, Rimac, Pininfarina, Lotus, Mercedes AMG, Audi Sport, Lexus, Ford Performance, Maserati, Bentley, Rolls Royce, and Dodge. |

SEGMENTAL ANALYSIS

By Vehicle Type Insights

The coupe supercars segment held the majority share of 65.9% of the Europe supercar market in 2025. This supremacy of the segment is mainly driven by the superior structural rigidity offered by fixed roof designs which is critical for high performance handling and aerodynamic efficiency. The absence of complex retractable roof mechanisms allows engineers to optimize weight distribution and lower the center of gravity resulting in sharper cornering capabilities and faster lap times. According to automotive engineering studies, a fixed roof structure provides vastly superior torsional stiffness compared to convertible counterparts, significantly reducing chassis flex and ensuring more precise suspension geometry during high-performance maneuvers. Manufacturers such as Ferrari and Porsche prioritize coupe configurations for their flagship models like the 296 GTB and 911 Turbo S because they deliver the purest driving experience. The aesthetic appeal of sleek uninterrupted lines also resonates strongly with buyers who view supercars as art pieces. Furthermore coupes are generally lighter than their convertible counterparts which improves acceleration and braking performance. The production process for coupes is also less complex and costly allowing manufacturers to maintain higher profit margins while offering competitive pricing. This combination of performance benefits aesthetic superiority and manufacturing efficiency ensures that coupe supercars remain the preferred choice for enthusiasts and collectors across Europe who prioritize driving dynamics over open air experiences. The domination of the coupe segment is further reinforced by its stronger resale value stability compared to convertible and track focused variants. Ultra high net worth individuals often view supercars as alternative investments and coupes historically retain their value better due to higher demand in the secondary market. According to Hagerty Insurance valuation tools classic and modern coupe supercars such as the Porsche 911 GT3 and Ferrari F8 Tributo have shown appreciation or minimal depreciation over five year periods whereas convertibles often suffer from higher depreciation rates due to perceived mechanical complexity and wear. The reliability of fixed roof structures reduces long term maintenance concerns related to hydraulic systems and weather sealing which are common issues in convertibles. This financial predictability makes coupes more attractive to buyers who consider total cost of ownership. Additionally the exclusivity of limited edition coupe models drives up demand among collectors. For instance the Ferrari Monza SP series although unique follows the coupe ethos of focused performance and has seen significant value increases. The European market particularly values heritage and authenticity which are often associated with traditional coupe designs. Dealerships report faster turnover rates for coupe models indicating robust liquidity. This economic advantage coupled with performance benefits solidifies the coupe segment's leading position in the Europe supercar market ensuring sustained demand from both drivers and investors.

The track focused supercars segment is predicted to witness the highest CAGR of 9.2% from 2026 to 2034 due to the increasing popularity of circuit driving experiences and exclusive track day clubs among wealthy enthusiasts. Owners of these high performance vehicles seek venues to exploit their cars' capabilities safely and legally leading to a surge in demand for vehicles optimized for track use. According to regional automotive organizations, participation in private track events and motorsport-affiliated clubs in major European markets has seen steady growth, driven by an increasing consumer preference for performance-based experiences. Manufacturers are responding by producing homologation specials and track only models such as the McLaren Senna and Aston Martin Vulcan which offer extreme aerodynamics and lightweight construction. These vehicles provide an immersive driving experience that road cars cannot match appealing to purists who value engagement over comfort. The proliferation of private racing circuits and luxury driving holidays in Europe further supports this trend. Events like the Ferrari Challenge and Porsche Track Experience allow owners to compete and socialize fostering a community around track focused machines. This cultural shift towards active participation in motorsport rather than passive ownership drives the growth of this niche segment. As enthusiasts seek greater thrills and exclusivity track focused supercars become increasingly desirable ensuring robust growth rates in the coming years. The accelerated growth of the track focused segment is also fueled by technological advancements in aerodynamics and lightweight materials that enhance on circuit performance. Innovations such as active aero systems carbon ceramic brakes and titanium exhausts allow these vehicles to achieve unprecedented levels of grip and stopping power. According to engineering reports from Formula 1 technology transfer initiatives materials developed for racing are increasingly being adapted for road legal track cars reducing weight by up to 20 percent compared to standard models. This weight reduction significantly improves power to weight ratios enabling faster acceleration and agility. European manufacturers leverage their motorsport heritage to integrate these technologies into consumer vehicles creating a direct link between race track success and road car desirability. For example the Mercedes AMG One utilizes a hybrid powertrain derived directly from Formula 1 attracting immense interest from tech savvy buyers. The ability to customize these vehicles with track specific options such as roll cages and racing seats further appeals to serious drivers. The perception of owning a piece of racing history enhances the emotional value of these cars. As technology continues to evolve the performance gap between race cars and road legal track cars narrows making them more appealing to enthusiasts. This technological allure combined with exclusivity drives the fast paced growth of the track focused supercar segment in Europe.

By Propulsion Insights

The gasoline powered supercars segment was the largest segment in the Europe supercar market and captured a 55.8% share in 2025. This prominence of the segment attributed to the emotional appeal of internal combustion engine sound and the rich heritage associated with traditional engines. Enthusiasts value the auditory experience of high revving V8 V10 and V12 engines which are integral to the supercar identity. Brands like Ferrari and Lamborghini have built their reputations on the distinctive sounds of their naturally aspirated engines creating a loyal customer base that resists electrification. The tactile feedback and linear power delivery of gasoline engines also provide a driving experience that many purists prefer over electric alternatives. Despite regulatory pressures manufacturers continue to refine internal combustion technologies to meet emission standards while preserving character. The introduction of turbocharging has allowed for smaller displacements without sacrificing performance ensuring compliance with Euro 7 norms. This balance of tradition and adaptation keeps gasoline supercars relevant. The extensive network of service centers and specialized mechanics for internal combustion engines also provides confidence to buyers regarding long term maintenance. As long as the emotional connection to engine sound remains strong gasoline powered supercars will continue to dominate the market despite the rise of alternative powertrains. The dominance of the gasoline segment is further supported by the established refueling infrastructure and convenience it offers across Europe. Unlike electric vehicles which require planning for charging stops gasoline supercars can be refueled quickly at any service station enabling spontaneous long distance travel. In contrast gasoline stations are ubiquitous and offer consistent availability reducing range anxiety for owners who frequently drive their supercars. This convenience is particularly important for grand touring scenarios where owners cover significant distances. The reliability of gasoline technology also means fewer concerns about battery degradation or charging times which can detract from the ownership experience. Manufacturers continue to optimize fuel efficiency in gasoline engines to mitigate running costs making them more practical for regular use. The familiarity of gasoline powertrains also simplifies the buying process for customers who are hesitant to adopt new technologies. This infrastructural advantage ensures that gasoline supercars remain the default choice for buyers prioritizing ease of use and flexibility. Until charging infrastructure becomes as seamless as refueling gasoline propulsion will retain its leading position in the Europe supercar market.

The hybrid segment is estimated to register the fastest CAGR of 12.5% during the forecast period owing to the ability of electric motors to enhance performance through instant torque fill and additional power output. Hybrid systems allow manufacturers to exceed traditional performance limits while complying with emission regulations. This synergy results in acceleration times that surpass purely gasoline powered predecessors appealing to performance oriented buyers. The electric motor provides immediate response at low speeds eliminating turbo lag and improving drivability in urban environments. This dual benefit of enhanced performance and daily usability makes hybrid supercars attractive to a broader audience. Buyers appreciate the versatility of switching between electric mode for quiet city driving and combined power for spirited runs. The technological sophistication of hybrid systems also adds to the exclusivity and prestige of these vehicles. As manufacturers refine hybrid architectures the weight penalty is reduced further improving handling dynamics. This performance led adoption ensures that hybrid supercars grow rapidly as they offer the best of both worlds in terms of power and efficiency. The accelerated growth of the hybrid segment is also fueled by regulatory compliance benefits and improved access to urban centers. Many European cities are implementing low emission zones that restrict or charge high polluting vehicles making hybrid supercars more practical for owners living in metropolitan areas. This regulatory advantage allows owners to drive their supercars more frequently without facing penalties or restrictions. The ability to operate in zero emission mode for short distances aligns with environmental goals while retaining the option for high performance driving. Manufacturers are marketing these benefits to attract environmentally conscious buyers who do not want to compromise on performance. Tax incentives for low emission vehicles in countries such as Germany and France further reduce the total cost of ownership for hybrid supercars. These financial and operational benefits make hybrids a pragmatic choice in an increasingly regulated environment. As emission standards tighten the appeal of hybrid technology will continue to grow ensuring its status as the fastest growing segment. The transition towards electrification is thus facilitated by hybrid systems which serve as a bridge between traditional and future mobility solutions.

By Engine Capacity Insights

The Mid-size (3000cc-3999cc) segment led the Europe supercar market and occupied a share of 45.7% in 2025. This leading position of the segment is supported by the optimal balance of power output and fuel efficiency achieved through advanced turbocharging technologies. Engines in this range typically feature V6 or V8 configurations that deliver substantial horsepower while remaining compliant with stringent emission norms. According to sources, turbocharged 3.0 liter and 3.9 liter engines can produce over 600 horsepower with better thermal efficiency than larger displacement units. This allows manufacturers to meet Euro 7 standards without sacrificing performance. Models such as the Ferrari F8 Tributo and McLaren 720S utilize engines in this range to achieve exceptional power to weight ratios. The compact size of these engines also aids in vehicle packaging allowing for better aerodynamics and interior space utilization. Buyers appreciate the responsiveness and torque curve of turbocharged mid-size engines which provide strong acceleration across the rev range. The cost of production for these engines is also lower than larger V12 units enabling more competitive pricing. This combination of regulatory compliance performance and cost effectiveness ensures that mid-size engines remain the most popular choice for European supercar manufacturers and buyers alike. The leadership of the mid-size segment is further reinforced by its versatility across different supercar categories including grand tourers and track focused machines. Engines in the 3000cc to 3999cc range are adaptable to various vehicle architectures making them suitable for a wide range of applications. For instance the same basic engine block can be tuned differently to suit a comfortable grand tourer or a aggressive track car. This flexibility allows brands to streamline production and reduce development costs while offering diverse product lines. The widespread adoption of this engine capacity also ensures a robust supply chain and availability of spare parts. Mechanics and service centers are well equipped to handle these engines reducing maintenance complexity for owners. The proven reliability of mid-size turbocharged engines builds consumer confidence encouraging purchases. As manufacturers continue to refine these engines with hybrid assistance their appeal is likely to persist. The ability to deliver high performance in a package that is manageable for daily driving ensures that the mid-size segment remains dominant in the Europe supercar market.

The compact engine capacity segment is anticipated to witness the fastest CAGR of 8.8% between 2026 and 2034. This rapid growth of the segment is driven by the adoption of high performance four cylinder and small displacement V6 engines equipped with advanced turbocharging and hybridization. Manufacturers are downsizing engines to reduce weight and emissions while maintaining power outputs through technological innovation. Models like the Alpine A110 and Lotus Emira demonstrate that smaller engines can deliver engaging driving dynamics and agility. This shift appeals to buyers who prioritize handling and responsiveness over raw displacement. The lower weight of compact engines improves front rear weight distribution enhancing cornering ability. Additionally the reduced fuel consumption and emissions make these vehicles more acceptable in regulated markets. The cost savings associated with smaller engines also allow manufacturers to offer more accessible entry level supercars expanding the customer base. As technology continues to advance the performance gap between compact and larger engines narrows driving growth in this segment. The rapid expansion of the compact segment is also fueled by its role in providing entry level accessibility to the supercar market. Vehicles with smaller engines are generally priced lower than their larger displacement counterparts making them attainable for a wider range of affluent buyers. The demographic growth is crucial for sustaining long term market vitality. Brands are leveraging this segment to build brand loyalty among newer customers who may upgrade to larger models in the future. The lower running costs and insurance premiums associated with compact engines also reduce the barrier to ownership. Government taxes based on engine displacement in countries like Italy and France further incentivize the purchase of smaller engines. This fiscal advantage combined with lower upfront costs drives demand. As manufacturers introduce more models in this category the variety and appeal increase. The compact segment thus serves as a gateway to the supercar world ensuring steady growth and broadening the market reach in Europe.

REGIONAL ANALYSIS

Germany Supercar Market Analysis

Germany dominated the Europe supercar market and accounted for a 22.6% share in 2025. This dominance of the German market is driven by its strong economy and high concentration of wealth. The country is home to a significant number of ultra high net worth individuals who have a strong affinity for high performance automobiles. Germany's extensive network of autobahns with unlimited speed sections provides a unique environment for experiencing supercar performance legally. This infrastructure encourages ownership and regular usage of high speed vehicles. The presence of major automotive hubs and events such as the Essen Motor Show further stimulates interest. German buyers are known for their technical appreciation and preference for engineering excellence which aligns with the attributes of modern supercars. The country also hosts numerous exclusive dealerships and service centers ensuring convenient ownership. Government policies supporting automotive innovation also foster a favorable environment. The cultural emphasis on precision and performance makes Germany a key market for brands like Porsche and Mercedes AMG as well as Italian and British marques. The sustained economic strength and automotive culture ensure Germany's leading role in the regional supercar landscape.

United Kingdom Supercar Market Analysis

The United Kingdom was the second largest country in the Europe supercar market and captured a share of 18.5% share in 2025 because of a deep rooted motorsport heritage and wealthy consumer base. The UK is home to iconic supercar manufacturers such as McLaren and Aston Martin which drive domestic interest and pride. The presence of exclusive automotive events like the Goodwood Festival of Speed creates a vibrant community of enthusiasts. British buyers are particularly attracted to limited edition and bespoke models valuing exclusivity and customization. The country's financial sector centered in London generates significant wealth that fuels luxury spending. Additionally the UK has a well developed network of private racing circuits and driving clubs that support supercar usage. Despite Brexit related challenges the demand for high performance vehicles remains resilient. The cultural appreciation for automotive design and engineering ensures a steady market. Government incentives for low emission vehicles also influence purchasing decisions favoring hybrid supercars. The combination of heritage wealth and infrastructure maintains the UK's strong position in the Europe supercar market.

Italy Supercar Market Analysis

Italy holds a significant position in the Europe supercar market due to its status as the birthplace of legendary supercar brands. Home to Ferrari Lamborghini and Pagani Italy has a unique cultural connection to high performance automobiles. The country's scenic roads and historic racing circuits such as Monza and Imola provide ideal settings for supercar driving. Italian buyers are known for their passion for design and emotion often prioritizing aesthetic appeal and brand heritage. The government supports the automotive sector through initiatives promoting Made in Italy excellence. Tourism also plays a role as visitors rent or purchase supercars to experience the Italian lifestyle. The presence of specialized workshops and restoration services enhances the ownership experience. Despite economic fluctuations the emotional value of supercars in Italy sustains demand. The integration of hybrid technology in Italian supercars also aligns with European regulations ensuring continued relevance. Italy's enduring legacy and passionate consumer base secure its significant share in the regional market.

France Supercar Market Analysis

France grew steadily in the Europe supercar market owing to its luxury lifestyle and urban wealth centers. Paris and the French Riviera are hubs for ultra high net worth individuals who view supercars as status symbols. The country's sophisticated infrastructure and scenic routes along the Mediterranean coast attract supercar owners. French buyers appreciate elegance and innovation often favoring brands that offer unique design elements. The government's push for electric mobility is influencing the market with increased interest in hybrid and electric supercars. Low emission zones in major cities encourage the adoption of cleaner high performance vehicles. The presence of exclusive automotive events and clubs fosters a community of enthusiasts. France's strong luxury goods sector complements the supercar market creating synergies in branding and marketing. The cultural emphasis on style and refinement aligns with the supercar ethos. Despite regulatory pressures the demand for exclusive automotive experiences persists. France's strategic location and affluent population ensure its continued relevance in the Europe supercar market.

Switzerland Supercar Market Analysis

Switzerland is predicted to expand notably in the Europe supercar market during the forecast period due to its high concentration of wealth and favourable tax environment. The country has one of the highest densities of supercars per capita globally particularly in cities like Zurich and Geneva. Swiss buyers value privacy exclusivity and quality often opting for bespoke and limited edition models. The country's pristine roads and alpine scenery provide a picturesque backdrop for supercar driving. The absence of value added tax on certain transactions and favorable import duties attract buyers from neighboring countries. Switzerland is also a hub for automotive storage and maintenance facilities offering high security and climate controlled environments. The cultural appreciation for precision engineering aligns with the technical sophistication of modern supercars. The strong financial sector supports discretionary spending on luxury assets. Despite small geographic size Switzerland's economic power ensures a disproportionate impact on the market. The demand for high performance vehicles remains robust among the elite. Switzerland's unique combination of wealth infrastructure and culture sustains its significant role in the Europe supercar market.

COMPETITIVE LANDSCAPE

The competition in the Europe supercar market is intense and characterized by a few dominant legacy brands and emerging challengers vying for the attention of ultra high net worth individuals. Established manufacturers like Ferrari and Lamborghini leverage their rich heritage and brand equity to maintain loyal customer bases while newcomers attempt to disrupt the status quo with innovative electric powertrains. Competitive dynamics are driven by technological superiority exclusivity and bespoke customization capabilities rather than price alone. Companies strive to differentiate themselves through unique design languages and performance metrics that appeal to discerning buyers. The shift towards electrification has intensified rivalry as brands race to develop hybrid systems that meet regulatory standards without compromising driving excitement. Limited production runs create artificial scarcity enhancing desirability and resale values. Strategic collaborations with luxury lifestyle brands further extend market reach and brand visibility. Despite high barriers to entry due to capital requirements and engineering complexity the allure of the supercar segment attracts continuous investment. Manufacturers must balance tradition with innovation to stay relevant. The focus on creating immersive ownership experiences through exclusive events and personalized services becomes crucial for retaining customers in this highly specialized and competitive automotive landscape.

KEY MARKET PLAYERS

Some of the notable key players in the Europe supercar market are

- Bugatti

- Ferrari N.V.

- Automobili Lamborghini S.p.A.

- McLaren

- Porsche

- Aston Martin

- Koenigsegg

- Pagani

- Rimac

- Pininfarina

- Lotus

- Mercedes-AMG

- Audi Sport

- Lexus

- Ford Performance

- Maserati

- Bentley

- Rolls-Royce

- Dodge

Top Players in the Market

- Ferrari N.V. stands as an iconic symbol of Italian engineering and luxury performance within the Europe supercar market. The company consistently delivers high performance vehicles that blend cutting edge technology with timeless design aesthetics. Ferrari contributes significantly to the global market by setting benchmarks for exclusivity and brand prestige. Recent actions include the launch of hybrid models like the SF90 Stradale which align with sustainability goals while maintaining exceptional power outputs. The company also expands its personalized customization programs allowing clients to create unique vehicles. Ferrari strengthens its position by limiting production volumes to ensure scarcity and high residual values. Strategic investments in research and development focus on advanced aerodynamics and lightweight materials. These initiatives reinforce Ferrari's reputation for innovation and desirability ensuring continued demand among ultra high net worth individuals who value heritage and performance in equal measure across European and international markets.

- Automobili Lamborghini S.p.A. is a leading force in the Europe supercar market known for its bold designs and aggressive performance characteristics. The brand captivates enthusiasts with vehicles that offer visceral driving experiences and distinctive styling. Lamborghini contributes globally by pushing boundaries in automotive design and engineering excellence. Recent actions include the introduction of the Revuelto a hybrid supercar that combines a V12 engine with electric motors for enhanced performance. The company also invests in sustainable manufacturing practices such as carbon fiber recycling initiatives. Lamborghini strengthens its market position by expanding its dealership network and offering exclusive driving experiences to customers. Collaborations with technology partners enable the integration of advanced connectivity features. These efforts ensure Lamborghini remains at the forefront of innovation appealing to a new generation of buyers who seek both tradition and modernity in their high performance automotive choices.

- McLaren Automotive Limited is a key player in the Europe supercar market leveraging its Formula 1 heritage to create technologically advanced vehicles. The company focuses on lightweight construction and aerodynamic efficiency to deliver superior handling and speed. McLaren contributes to the global market by pioneering carbon fiber manufacturing techniques and hybrid powertrains. Recent actions include the launch of the Artura a high performance hybrid supercar that showcases the brand's commitment to electrification. The company also enhances its customer engagement through personalized configuration tools and track day events. McLaren strengthens its position by optimizing production processes to improve quality and delivery times. Strategic partnerships with suppliers ensure access to cutting edge materials and components. These initiatives allow McLaren to compete effectively in the luxury segment by offering distinct driving dynamics and technological sophistication that appeal to discerning enthusiasts seeking precision and innovation in their supercar ownership experience.

Top Strategies Used by the Key Market Participants

Key players in the Europe supercar market primarily employ strategies focused on product exclusivity and technological innovation to maintain their competitive edge. Manufacturers limit production volumes to create scarcity and enhance brand prestige among ultra high net worth individuals. Companies invest heavily in hybrid and electric powertrain technologies to comply with stringent environmental regulations while preserving performance standards. Personalization programs are expanded to allow customers bespoke customization options increasing emotional attachment and value. Strategic partnerships with technology firms facilitate the integration of advanced digital features and connectivity solutions. Brands also organize exclusive driving events and track experiences to foster community and loyalty among owners. Sustainability initiatives such as using recycled materials and carbon neutral manufacturing processes are adopted to align with consumer values. These strategies collectively enable participants to differentiate their offerings and sustain demand in a niche but highly lucrative market segment across Europe.

MARKET SEGMENTATION

This research report on the European supercar market has been segmented and sub-segmented based on categories.

By Vehicle Type

- Coupe Supercars

- Convertible Supercars

- Track-focused Supercars

By Propulsion

- Gasoline

- Diesel

- Electric

- Hybrid

By Engine Capacity

- Compact (Below 2999cc)

- Mid-size (3000cc-3999cc)

- Full-size (Above 4000cc)

By Power

- Less than 300 (KW)

- 301 (KW) - 400 (KW)

- 401 (KW) - 500 (KW)

- More than 500 (KW)

By Speed

- Less than 200 mph

- 201 mph - 250 mph

- 251 mph - 300 mph

- 301 mph - 350 mph

- More than 350 mph

By Transmission

- Manual

- Automatic

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1.What factors are driving the growth of the Europe supercar market?

Key drivers include increasing high net worth individuals, rising demand for high performance luxury vehicles, and advancements in hybrid and electric supercar technologies.

2.Which countries dominate the Europe supercar market?

Italy, Germany, and the United Kingdom dominate due to their strong automotive legacy and presence of premium supercar manufacturers.

3.What types of supercars are most popular in Europe?

Internal combustion engine supercars remain dominant, but hybrid and electric supercars are gaining traction due to sustainability trends.

4.Who are the primary consumers in the Europe supercar market?

High net worth individuals, collectors, automotive enthusiasts, and luxury lifestyle buyers form the core consumer base.

5.How is electrification influencing the Europe supercar market?

Electrification is pushing manufacturers to develop hybrid and fully electric supercars that meet strict emission regulations while maintaining performance.

6.What role does technology play in the Europe supercar market?

Advanced technologies such as lightweight materials, aerodynamics, and driver assistance systems enhance performance, safety, and efficiency.

7.Are limited edition supercars in demand in Europe?

Yes, limited edition models are highly desirable due to exclusivity, brand prestige, and strong resale or investment potential.

8.How do environmental regulations impact the Europe supercar market?

Strict emission standards are encouraging automakers to innovate and shift toward cleaner propulsion systems.

9.What are the key distribution channels for supercars in Europe?

Supercars are mainly sold through authorized dealerships, exclusive brand showrooms, and direct manufacturer sales channels.

10.What challenges are faced by the Europe supercar market?

High production costs, regulatory pressures, and economic fluctuations pose challenges to market growth.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com