Europe Test and Measurement Equipment Market Size, Share, Trends, and Growth Analysis Report, Segmented by Offering, Vertical, and Country – Industry Forecast From 2026 to 2034

Europe Test and Measurement Equipment Market Report Summary

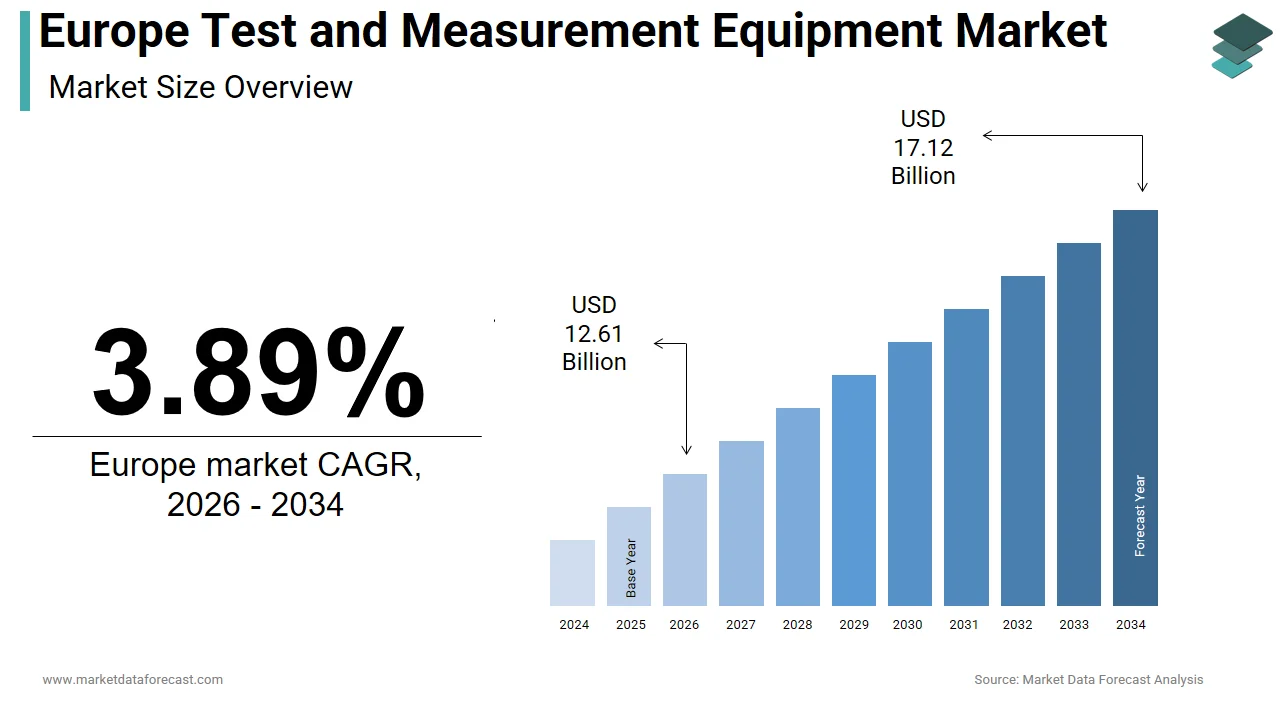

The Europe test and measurement equipment market was valued at USD 12.14 billion in 2025, is estimated to reach USD 12.61 billion in 2026, and is projected to reach USD 17.12 billion by 2034, growing at a CAGR of 3.89% from 2026 to 2034. Market growth is driven by increasing demand for precision testing across industries such as electronics, telecommunications, automotive, and aerospace. The expansion of 5G infrastructure, advancements in semiconductor technologies, and the growing complexity of electronic devices are key factors fueling demand. Additionally, the need for quality assurance, regulatory compliance, and performance optimization is supporting steady market growth across Europe.

Key Market Trends

- Growing demand for advanced testing in electronics and semiconductors.

- Expansion of 5G networks and telecommunications infrastructure.

- Increasing focus on quality assurance and regulatory compliance.

- Rising adoption of automated and digital testing solutions.

- Technological advancements in precision measurement tools.

Segmental Insights

- Based on offering, the product segment dominated the Europe test and measurement equipment market by capturing 65.1% share in 2025, driven by demand for advanced instruments and devices.

- Based on vertical, the electronics and semiconductor segment led the market with 28.2% share in 2025, supported by rapid innovation and production in the electronics industry.

Regional Insights

The Europe test and measurement equipment market is witnessing steady growth across major industrial economies.

- Germany led the market in 2025 with 22.3% share, driven by strong manufacturing and industrial automation sectors.

- The United Kingdom followed with 18.4% share, supported by technological innovation and R&D investments.

- France holds a significant position due to its strong presence in aerospace, energy, and defense sectors.

Competitive Landscape

The Europe test and measurement equipment market is competitive, with companies focusing on innovation, product development, and expanding application areas. Investments in next-generation testing technologies and strategic collaborations are key competitive strategies.

Prominent companies operating in the Europe test and measurement equipment market include Viavi Solutions, Inc., Yokogawa Electric Corporation, Keysight Technologies, Inc., Fortive Corporation (Tektronix, Inc.), Ametek, Inc., Rohde & Schwarz GmbH & Co. KG, Anritsu Corporation, National Instruments, Advantest Corporation, Teledyne FLIR LLC (Teledyne Technologies Incorporated), and EXFO, Inc.

Europe Test and Measurement Equipment Market Size

The Europe test and measurement equipment market was valued at USD 12.14 billion in 2025, is estimated to reach USD 12.61 billion in 2026, and is projected to reach USD 17.12 billion by 2034, growing at a CAGR of 3.89% from 2026 to 2034.

Test and measurement (T&M) equipment refers to specialized instruments used to evaluate, analyze, and quantify the performance of physical, electrical, or mechanical systems. These tools ensure that products meet stringent regulatory standards and operational specifications before reaching the end user. The region’s strong emphasis on precision engineering and manufacturing excellence drives the continuous adoption of advanced testing solutions. As per Eurostat, the manufacturing sector in the European Union accounted for approximately 14 percent (specifically ~13.8% of GDP) of the total economy in 2024, following a 2.0% decrease in the production of manufactured goods compared to the previous year. This substantial industrial base necessitates rigorous quality control measures thereby fueling demand for sophisticated test and measurement devices. According to the European Commission the digital transformation of European industry is a key priority with significant investments allocated to smart manufacturing technologies. The integration of Internet of Things devices and automated production lines requires precise calibration and monitoring capabilities to maintain efficiency. Furthermore the European Union’s Green Deal initiative mandates stricter environmental compliance for industrial processes which increases the need for emissions testing and energy efficiency measurements. As enshrined in the European Climate Law, the European Union has set a binding target to reduce net greenhouse gas emissions by at least 55 percent by 2030 compared to 1990 levels, a goal monitored and analyzed by organizations including the International Energy Agency. Achieving these goals requires extensive testing of new materials and energy systems. The presence of leading automotive manufacturers and aerospace giants further amplifies the requirement for high precision testing equipment to ensure safety and performance. Consequently, the convergence of regulatory pressures technological advancement and industrial modernization creates a robust foundation for the growth of the test and measurement equipment sector in Europe.

MARKET DRIVERS

Rapid Expansion of the Electric Vehicle Ecosystem Necessitates Advanced Testing Infrastructure

The transition towards electric mobility in the region drives the growth of the Europe test and measurement equipment market. This has created an unprecedented demand for specialized test and measurement equipment tailored to electric vehicle components. Manufacturers are increasingly investing in facilities to test battery packs power electronics and charging infrastructure to ensure safety and performance standards. According to the European Automobile Manufacturers’ Association (ACEA), sales of new battery-electric cars in the European Union totaled approximately 1.44 million units in 2024, accounting for 13.6% of the total car market. This surge in production volume requires extensive validation processes including thermal management testing electrical safety checks and durability assessments. The European Battery Alliance has facilitated the establishment of multiple gigafactories across the continent each requiring sophisticated testing laboratories to monitor cell quality and pack integrity. As per the Joint Research Centre of the European Commission rigorous testing protocols are essential to comply with the new EU Battery Regulation which mandates strict sustainability and performance criteria. Companies are deploying high voltage test systems and automated inspection tools to handle the complexity of electric powertrains. The need for rapid prototyping and iterative design cycles further accelerates the adoption of flexible and modular testing solutions. Additionally the development of solid state batteries introduces new testing requirements for material characterization and interface analysis. Thus, the electrification of transport serves as a primary driver propelling the market for advanced test and measurement equipment as manufacturers strive to meet evolving technical and regulatory benchmarks in a competitive landscape.

Stringent Regulatory Frameworks for Wireless Standards Drive Continuous Upgrades

The proliferation of wireless technologies and connected devices in the region has intensified the need for comprehensive electromagnetic compatibility and radio frequency testing, which further propels the expansion of the Europe test and measurement equipment market. Regulatory bodies enforce strict compliance standards to prevent interference and ensure the reliable operation of electronic devices in shared spectra. According to the European Commission (via the Digital Decade/5G Observatory reports), the deployment of fifth-generation networks has expanded significantly, with basic 5G coverage reaching approximately 81% of the EU population by the reporting period in 2024. This widespread adoption necessitates rigorous testing of antennas transceivers and network infrastructure to guarantee signal integrity and data throughput. The introduction of new frequency bands for sixth generation research further complicates the testing landscape requiring equipment capable of handling higher frequencies and wider bandwidths. As per research, the number of connected Internet of Things (IoT) devices in Europe is estimated to reach approximately 4 billion by 2025, representing a significant portion of the global total. Each device must undergo certification processes to meet electromagnetic emission and immunity limits. Manufacturers are investing in anechoic chambers and spectrum analyzers to simulate real world conditions and identify potential interference issues early in the design phase. The complexity of modern communication protocols such as Wi Fi 6E and Bluetooth Low Energy demands precise measurement tools to validate performance. Hence, the relentless evolution of wireless standards and the increasing density of connected devices act as a powerful driver for the test and measurement equipment market ensuring sustained demand for high precision diagnostic solutions.

MARKET RESTRAINTS

High Initial Capital Expenditure Restricts Accessibility for Small Enterprises

The acquisition of state of the art test and measurement equipment involves substantial financial investment which poses a significant barrier for small and medium sized enterprises in the Europe test and measurement equipment market. Advanced instruments such as vector network analyzers oscilloscopes and environmental test chambers often cost hundreds of thousands of Euros limiting their accessibility to smaller players. According to Eurostat small and medium sized enterprises constitute approximately 99 percent of all businesses in the European Union yet they face greater challenges in accessing capital for technological upgrades. The high cost of ownership extends beyond the initial purchase price to include regular calibration software updates and specialized training for operators. As per the European Investment Bank, small businesses often face financing gaps for intangible assets (such as R&D and software) and scale-up projects, which are critical for long-term competitiveness. This financial constraint forces smaller companies to rely on external testing services which can lead to longer development cycles and reduced control over proprietary data. Furthermore the rapid pace of technological obsolescence means that equipment may become outdated within a few years necessitating frequent replacements. The economic uncertainty following recent global disruptions has also made companies more cautious about large capital expenditures. Therefore, the high cost burden acts as a major restraint preventing widespread adoption of advanced testing solutions among smaller entities and potentially stifling innovation in this segment of the market.

Shortage of Skilled Professionals Impedes Efficient Utilization of Complex Systems

The effective use of modern test and measurement equipment requires a workforce with specialized skills in electronics data analysis and instrumentation, which in turn hampers the expansion of the Europe test and measurement equipment market. However Europe faces a growing shortage of qualified engineers and technicians capable of managing these sophisticated systems. According to Cedefop, there are persistent skill shortages in STEM and ICT professions, contributing to a broader labour market tightness where the job vacancy rate in the EU reached 2.9% (representing millions of total vacancies). This talent shortage affects the ability of companies to fully leverage the capabilities of their testing infrastructure leading to underutilization and inefficiencies. Operating advanced instruments such as mixed signal oscilloscopes or automated test equipment requires deep understanding of both hardware and software interfaces. A study indicates that the lack of trained personnel directly impacts operational efficiency, resulting in longer setup times, increased error rates, and delayed product launches. Companies often need to invest heavily in internal training programs or hire expensive consultants to bridge this knowledge gap. The complexity of modern testing scenarios involving multiple parameters and real time data processing further exacerbates the challenge. Educational institutions have struggled to keep pace with the rapid advancements in testing technology resulting in graduates who lack practical experience. As a result, the scarcity of skilled professionals acts as a critical restraint hindering the optimal deployment of test and measurement equipment and limiting the overall productivity gains that these technologies promise to deliver.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence Offers Efficiency and Predictive Maintenance Capabilities

Artificial intelligence and machine learning are being integrated into test and measurement equipment. This shift offers a transformative opportunity for the European test and measurement equipment market. These technologies enable automated data analysis pattern recognition and predictive maintenance which significantly enhance testing speed and accuracy. According to the European Commission's Eurostat data, the adoption of AI in the EU reached 20% of enterprises in 2025, with manufacturing adoption reaching approximately 19%, trailing behind the Information and Communication sector which leads at 42.2%. AI driven testing systems can identify anomalies and defects in real time reducing the need for manual inspection and minimizing false positives. This capability is particularly valuable in high volume production environments such as semiconductor manufacturing where precision is paramount. Research from the Fraunhofer Institute for Integrated Circuits (IIS) demonstrates that machine learning models and quantization techniques can optimize test sequences and reduce time complexity by over 80% for specific industrial and software applications. This efficiency gain translates into lower operational costs and faster time to market for new products. Furthermore predictive maintenance features allow equipment to self diagnose potential failures before they occur ensuring uninterrupted operation and extending instrument lifespan. The ability to process vast amounts of test data quickly enables manufacturers to gain deeper insights into product performance and quality trends. So, the synergy between artificial intelligence and test and measurement equipment opens new avenues for innovation allowing companies to achieve higher levels of automation and operational excellence in their quality control processes.

Expansion of Renewable Energy Infrastructure Creates Demand for Specialized Grid Testing

The aggressive expansion of renewable energy sources in the region generates substantial prospects for the Europe test and measurement equipment market. The demand is particularly high for solutions in grid integration and component validation. As countries transition away from fossil fuels the complexity of the electrical grid increases due to the intermittent nature of solar and wind power. As per the International Energy Agency (IEA) 2024 Mid-Year Update, renewable energy sources accounted for approximately 50% of the European Union's electricity generation in 2024, a significant milestone driven by solar PV and wind expansion. Ensuring the stability and reliability of this decentralized grid requires advanced testing of inverters transformers and energy storage systems. Test equipment manufacturers are developing specialized solutions to measure power quality harmonic distortion and frequency response in real time. The European Network of Transmission System Operators for Electricity (ENTSO-E) mandates strict technical requirements for Power Generating Modules and large-scale industrial units to ensure grid stability, specifically focusing on instability detection technologies in power electronics-dominated systems. The development of offshore wind farms also necessitates robust testing of subsea cables and connection hardware under harsh environmental conditions. Additionally, the growth of green hydrogen production introduces new testing requirements for electrolyzers and fuel cells. Companies are investing in high power testing facilities to validate the performance of these emerging technologies. Thus, the shift towards a sustainable energy landscape drives demand for innovative test and measurement solutions that ensure the safe and efficient operation of renewable energy infrastructure across Europe.

MARKET CHALLENGES

Rapid Technological Obsolescence Challenges Equipment Longevity and Return on Investment

The rapid pace of technological advancement in sectors such as telecommunications and semiconductors leads to frequent obsolescence of this equipment, which slows down the growth of the Europe test and measurement equipment market. New standards for wireless communication and chip architectures emerge regularly rendering existing instruments incapable of meeting current testing requirements. In line with Moore’s Law, the number of transistors on a chip has historically doubled every two years. However, the Semiconductor Industry Association (SIA) now highlights that future complexity gains will rely on 3D structures and chiplet architectures to bypass physical scaling limits. This rapid evolution forces companies to frequently upgrade or replace their equipment to stay competitive. According to the European Semiconductor Industry Association (ESIA), the mass adoption of 3nm and GAAFET (Gate-All-Around) technologies requires advanced metrology to manage critical dimension (CD) variations and quantum mechanical effects that impact yield. Older instruments often lack the bandwidth or accuracy needed to characterize these advanced devices effectively. The short lifecycle of testing technology reduces the return on investment for manufacturers who must constantly reinvest in new hardware. Furthermore the lack of backward compatibility between different generations of equipment complicates inventory management and increases operational complexity. Companies must balance the need for cutting edge capabilities with the financial burden of frequent upgrades. This challenge is particularly acute for smaller firms with limited budgets. Hence, the relentless speed of technological change poses a significant challenge to the test and measurement equipment market requiring stakeholders to adopt flexible strategies such as equipment leasing or modular designs to mitigate the risks associated with obsolescence.

Supply Chain Disruptions Impact Production Timelines and Instrument Availability

Heavy reliance on a complex global supply chain for critical components such as semiconductors sensors and display panels is negatively impacting the expansion of the Europe test and measurement equipment market. Disruptions in this supply chain can significantly delay production and limit the availability of instruments to end users. The European Central Bank (ECB) reports that supply chain strains since 2020 reduced euro area industrial production by a cumulative 2.6%, driven by a combination of logistics disruptions and a massive rotation of consumer demand toward electronics. The shortage of specific microcontrollers and analog chips has forced equipment manufacturers to extend lead times and prioritize certain orders. While the severe "50-week" delays of the pandemic era have subsided, the European Electronic Component Manufacturers Association (EECA) and market analysts like Sourceability note that HBM (High Bandwidth Memory) and specialized automotive power devices still face volatility, with lead times often exceeding 16 weeks. This uncertainty makes it difficult for manufacturers to plan production schedules and meet customer demand promptly. The geopolitical tensions and trade restrictions further exacerbate these challenges by limiting access to raw materials and finished goods from certain regions. Companies are forced to hold larger inventories of critical components which increases working capital requirements and storage costs. Additionally the reliance on single source suppliers for specialized parts creates vulnerabilities that can halt entire production lines. Therefore, supply chain instability represents a major challenge for the test and measurement equipment market compelling companies to diversify their supplier base and invest in local manufacturing capabilities to enhance resilience against future disruptions.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Offering, Vertical, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled |

|

SEGMENTAL ANALYSIS

By Offering Insights

The product segment dominated the Europe test and measurement equipment market and accounted for a 65.1% share in 2025. This dominance of the segment is driven by the continuous need for hardware upgrades across industries to keep pace with evolving technological standards. The main factor fueling this segment is the widespread adoption of general purpose test equipment such as oscilloscopes and multimeters in research and development facilities. According to Eurostat, the European Union's investment in research and development reached a record €403.1 billion in 2024, representing 2.24% of GDP. This financial commitment directly translates into procurement of advanced testing instruments required for prototype validation and quality assurance. Furthermore the expansion of semiconductor manufacturing capabilities in Europe necessitates high precision measurement tools. As per the Semiconductor Industry Association (SIA), global semiconductor sales hit $791.7 billion in 2025, a 25.6% increase from the previous year, driven primarily by high demand for logic and memory chips used in AI applications. The establishment of new fabrication plants requires substantial capital expenditure on testing infrastructure to ensure yield and reliability. Additionally the automotive sector’s shift towards electric vehicles demands specialized battery testing equipment which falls under the product category. Manufacturers are increasingly investing in automated test systems to handle complex power electronics. Thus, the relentless demand for physical instruments to support industrial modernization and technological advancement ensures the product segment remains the largest contributor to market revenue.

The calibration services segment is predicted to witness the highest CAGR of 7.8% from 2026 to 2034. This accelerated growth of the segment is largely attributed to stringent regulatory requirements mandating regular instrument calibration to maintain accuracy and compliance. Industries such as pharmaceuticals aerospace and healthcare operate under strict quality management systems that require documented proof of measurement traceability. Reports from European Accreditation (EA) indicate that while the number of overall accreditations remained stable at approximately 35,400, demand has surged specifically in the energy and health sectors, which saw R&D growth of 13% and 19.8% respectively. This expansion reflects the critical importance of maintaining measurement integrity in safety sensitive applications. Furthermore the increasing complexity of modern electronic devices necessitates more frequent and precise calibration intervals. While ISO/IEC 17025:2017 continues to be the standard for measurement competence, the upcoming ISO 9001:2025 revision introduces new focuses on data reliability, digital infrastructure, and ethical accountability, prompting laboratories to modernize their quality management systems. The rise of Industry 4.0 also contributes to this growth as connected manufacturing environments rely on synchronized and accurate data from multiple sensors. Any deviation in measurement can lead to significant production errors or safety hazards. Hence, manufacturers are opting for comprehensive service contracts that include regular calibration maintenance and certification. This shift from reactive to proactive maintenance strategies fuels the rapid expansion of the calibration services segment ensuring instruments remain within specified tolerances throughout their operational lifecycle.

By Vertical Insights

The electronics and semiconductor segment led the Europe test and measurement equipment market and captured a 28.2% share in 2025. This leading position of the segment is supported by the region’s robust semiconductor industry and the increasing complexity of electronic components. A key driver is the massive investment in semiconductor fabrication facilities aimed at achieving strategic autonomy in chip production. According to the European Chips Act the European Union aims to double its global market share in semiconductors to 20 percent by 2030 requiring billions of Euros in investment. This initiative has spurred the construction of new fabs in countries like Germany and France each requiring extensive test and measurement infrastructure for wafer probing and final package testing. Furthermore the miniaturization of transistors to nanometer scales demands ultra precise measurement tools capable of detecting minute defects. The European Commission estimates that the Chips Act will mobilise at least €86 billion in total investment through 2030, with a major focus on R&D for advanced technologies like 2-nanometer nodes and quantum chips. These advancements require sophisticated equipment such as electron microscopes and parametric testers to ensure functionality and reliability. The proliferation of Internet of Things devices also drives demand for testing radio frequency and power efficiency characteristics. Therefore, the strategic imperative to strengthen the semiconductor supply chain combined with technological complexity ensures the electronics and semiconductor segment remains the dominant vertical in the market.

The automotive and transportation segment is estimated to register the fastest CAGR of 8.5% during the forecast period due to the radical transformation towards electric and autonomous vehicles. The transition from internal combustion engines to electric powertrains introduces new testing requirements for batteries motors and charging systems. According to the European Automobile Manufacturers' Association (ACEA), battery-electric vehicles reached a 13.6% market share in 2024 with approximately 1.44 million registrations, while hybrid-electric vehicles surged to a 30.9% share (over 3.2 million units).This surge necessitates extensive testing of high voltage systems to ensure safety and performance compliance. Additionally the development of autonomous driving technologies requires rigorous validation of sensors such as lidar radar and cameras under various environmental conditions. As per the United Nations Economic Commission for Europe new regulations on automated lane keeping systems mandate strict testing protocols before market approval. Manufacturers are investing in hardware in the loop simulation systems to replicate real world driving scenarios and verify software algorithms. The integration of vehicle to everything communication technologies further expands the scope of testing to include connectivity and cybersecurity aspects. So, the convergence of electrification automation and connectivity in the automotive sector creates a sustained demand for advanced test and measurement solutions driving rapid growth in this vertical.

COUNTRY LEVEL ANALYSIS

Germany Test and Measurement Equipment Market Analysis

Germany was the top performer in the Europe test and measurement equipment market and occupied a 22.3% share in 2025. The country’s position is driven by its powerful manufacturing base particularly in the automotive and machinery sectors. The German automotive industry is undergoing a profound transformation towards electromobility which drives significant demand for battery and powertrain testing solutions. According to the German Association of the Automotive Industry (VDA), German automakers are investing approximately €280 billion globally through 2028 in electric mobility and digitalization to maintain their competitive edge. This capital expenditure includes the establishment of comprehensive testing laboratories to validate new technologies. Furthermore Germany is home to leading semiconductor manufacturers who require precise measurement tools for chip production. The BMWK has allocated approximately €20 billion in federal funding for the semiconductor sector, supporting first-of-a-kind facilities in line with the European Chips Act. This funding facilitates the construction of new fabrication plants and research centers equipped with state of the art testing infrastructure. The presence of major instrument manufacturers in Germany also fosters a strong ecosystem for innovation and local supply. Additionally the country’s emphasis on Industry 4.0 promotes the adoption of automated testing systems in smart factories. Consequently Germany’s robust industrial landscape and strategic investments in future technologies sustain its dominance in the European test and measurement equipment market.

United Kingdom Test and Measurement Equipment Market Analysis

The United Kingdom was the second largest country in the Europe test and measurement equipment market and accounted for a 18.4% share in 2025. This growth of the UK market is propelled by a strong aerospace and defense industry which requires high precision testing for safety critical components. As per the ADS Group, the UK aerospace industry generated £30.5 billion in turnover in 2024, supporting over 100,000 direct high-skilled jobs across the country. This industry relies heavily on advanced non destructive testing and structural analysis equipment to ensure aircraft integrity. Furthermore the UK is a leader in telecommunications technology with significant investments in fifth generation network infrastructure. As per Ofcom the rollout of standalone fifth generation networks is accelerating requiring extensive radio frequency testing to optimize performance. The country also boasts a vibrant semiconductor design industry although manufacturing capacity is limited. The government’s National Semiconductor Strategy aims to strengthen the domestic ecosystem through research and development support. Additionally the healthcare sector in the UK is expanding its use of medical devices which necessitates rigorous regulatory testing. The National Health Service procurement policies emphasize quality and safety driving demand for compliant testing services. Consequently the diverse industrial base and strategic focus on high technology sectors maintain the United Kingdom’s prominent position in the regional market.

France Test and Measurement Equipment Market Analysis

France occupies a significant position in the Europe test and measurement equipment market due to its strong presence in aerospace energy and defense sectors. France is a key player in the European aerospace industry hosting major manufacturers who require sophisticated testing for aircraft systems and materials. The French government, through the France 2030 program, has committed €1.2 billion to decarbonizing aviation, with a goal of producing a low-carbon aircraft by 2030. This investment drives demand for environmental testing and material characterization equipment. Additionally France’s reliance on nuclear energy necessitates rigorous testing of components to ensure safety and longevity. As per the French Alternative Energies and Atomic Energy Commission significant funds are allocated to maintain and upgrade nuclear facilities requiring specialized radiation and structural testing instruments. The country is also advancing its semiconductor capabilities through the France 2030 investment plan which aims to produce innovative chips. This initiative supports the development of local testing infrastructure to support design and prototyping activities. Furthermore the telecommunications sector is expanding fifth generation coverage requiring ongoing network optimization and testing. Hence, France’s strategic industries and government support for technological sovereignty drive steady demand for test and measurement equipment.

Italy Test and Measurement Equipment Market Analysis

Italy is moving ahead steadfastly in the Europe test and measurement equipment market owing to its diverse manufacturing base including automotive machinery and industrial automation. Also, Italy is a major producer of automotive components and machinery requiring extensive quality control and performance testing. According to the Italian National Institute of Statistics (ISTAT) and World Bank data, the manufacturing sector accounts for approximately 15% of Italy's GDP, making it the second-largest manufacturing powerhouse in Europe. The transition towards electric vehicles is prompting Italian suppliers to invest in new testing capabilities for electronic components and battery systems. As per the Italian Association of Machinery Manufacturers exports of industrial machinery reached record levels in 2024 driving demand for integrated testing solutions within production lines. The country also has a growing electronics sector focused on specialized applications such as automotive electronics and industrial controls. These sectors require precise measurement tools to ensure product reliability and compliance with international standards. Additionally the Italian government supports innovation through national recovery and resilience plan funds which include provisions for digital transformation and technological upgrades. This financial support enables small and medium enterprises to adopt advanced testing technologies. Therefore, Italy’s strong manufacturing tradition and ongoing modernization efforts sustain its significant role in the European market.

Netherlands Test and Measurement Equipment Market Analysis

The Netherlands is likely to grow significantly in the Europe test and measurement equipment market from 2026 to 2034 due to its pivotal role in the global semiconductor equipment industry. Home to a leading lithography machine manufacturer the Netherlands serves as a critical hub for semiconductor technology development. According to the Netherlands Enterprise Agency (RVO) and CBS, the high-tech sector is a dominant exporter, with specialized semiconductor manufacturing machinery alone generating $25 billion in exports in 2024, contributing to a total machinery export value exceeding €100 billion. This sector relies on ultra precise measurement and inspection equipment to develop and maintain complex manufacturing tools. The presence of major research institutions such as IMEC’s partner facilities fosters innovation in metrology and testing techniques. As per the Dutch Semiconductor Industry Association collaboration between industry and academia drives advancements in nanoscale measurement capabilities. Furthermore the Netherlands is a logistics gateway for Europe facilitating the distribution of test and measurement instruments to other regions. The country also has a strong agricultural technology sector which increasingly uses sensors and testing devices for precision farming. Government initiatives supporting digitalization and sustainability further encourage the adoption of advanced monitoring and testing solutions. So, the Netherlands’ specialized expertise in semiconductor equipment and strong research ecosystem secure its place as a key market participant.

COMPETITIVE LANDSCAPE

The competition in the Europe test and measurement equipment market is intense characterized by the presence of established global leaders and specialized regional players. Major companies compete on the basis of technological innovation product reliability and comprehensive customer support services. The market sees frequent product launches featuring advanced capabilities such as higher bandwidth faster processing speeds and integrated software analytics. Differentiation is achieved through specialized solutions tailored to specific industries like automotive aerospace and semiconductors. Price competition exists but is secondary to performance and accuracy which are critical for industrial applications. Companies also compete on the strength of their distribution networks and after sales service capabilities including calibration and repair. Strategic alliances and collaborations are common as firms seek to combine expertise in hardware and software to offer integrated solutions. The entry of new players with disruptive technologies such as virtual instrumentation and cloud based testing adds to the competitive dynamics. Intellectual property protection is crucial as companies strive to safeguard their innovations. Overall the market demands continuous innovation and adaptability to meet the evolving needs of diverse industrial sectors across Europe.

KEY MARKET PLAYERS

The leading companies operating in the Europe test and measurement equipment market include:

- Viavi Solutions, Inc.

- Yokogawa Electric Corporation

- Keysight Technologies, Inc.

- Fortive Corporation (Tektronix, Inc.)

- Ametek, Inc.

- Rohde & Schwarz GmbH & Co. KG

- Anritsu Corporation

- National Instruments

- Advantest Corporation

- Teledyne FLIR LLC (Teledyne Technologies Incorporated)

- EXFO, Inc.

TOP PLAYERS IN THE MARKET

- Rohde and Schwarz is a leading German manufacturer specializing in test and measurement solutions for communications electronics and cybersecurity. The company plays a pivotal role in the global market by providing advanced instruments for fifth generation network testing and semiconductor validation. In Europe it maintains a strong presence through extensive research and development facilities that drive innovation in radio frequency and microwave technologies. Recent actions include the launch of new software defined radio platforms that enhance flexibility for automotive and aerospace applications. The company actively collaborates with standardization bodies to ensure its equipment meets emerging regulatory requirements. By focusing on sustainable manufacturing practices and digital transformation Rohde and Schwarz strengthens its competitive position. Its commitment to customer support and localized service networks ensures high client retention across European industries. This strategic focus on technological leadership and customer centric solutions solidifies its reputation as a trusted partner in the test and measurement sector.

- Keysight Technologies is a prominent American company with significant operations in Europe offering comprehensive test and measurement solutions for various industries. It contributes globally by delivering cutting edge tools for electronic design automation and network emulation. In the European market Keysight focuses on supporting the automotive and telecommunications sectors with specialized testing infrastructure for electric vehicles and fifth generation networks. The company recently expanded its portfolio with AI driven analytics software that improves test efficiency and accuracy. Strategic partnerships with European universities and research institutes foster innovation in quantum computing and photonics. Keysight also invests in cloud based testing services allowing remote access to sophisticated instruments. These initiatives enhance its market position by addressing the growing demand for flexible and scalable testing solutions. Keysight leverages its broad product range and technical expertise to deliver value. This enables customers to achieve precise, reliable measurements in complex engineering environments.

- National Instruments now part of Emerson Electric Co is a key player in the Europe test and measurement equipment market known for its modular and software centric approach. The company provides graphical system design platforms that enable engineers to develop customized testing solutions rapidly. Its global contribution lies in empowering industries with flexible hardware and powerful software tools for automation and data analysis. In Europe National Instruments strengthens its position by supporting the industrial Internet of Things and smart manufacturing initiatives. Recent actions include the integration of advanced machine learning capabilities into its software suite to facilitate predictive maintenance and quality control. The company collaborates with local system integrators to deliver tailored solutions for automotive and aerospace clients. By emphasizing open standards and interoperability National Instruments ensures its platforms can seamlessly connect with existing infrastructure. This strategy enhances its appeal to manufacturers seeking agile and cost effective testing architectures. The combination of innovative technology and strong ecosystem partnerships drives its continued success in the European market.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe test and measurement equipment market primarily focus on strategic acquisitions and partnerships to expand their product portfolios and technological capabilities. Companies frequently acquire specialized firms to integrate advanced software algorithms and artificial intelligence features into their hardware offerings. This approach enables them to provide comprehensive solutions that address complex testing requirements in industries such as automotive and telecommunications. Another major strategy involves heavy investment in research and development to innovate new products that comply with evolving industry standards. Manufacturers also emphasize digital transformation by offering cloud based testing services and remote monitoring capabilities. These services enhance customer convenience and operational efficiency. Additionally companies prioritize sustainability by developing energy efficient instruments and adopting eco friendly manufacturing processes. Collaborations with academic institutions and industry consortia help drive innovation and maintain technological leadership. By aligning their strategies with market trends and customer needs key participants strengthen their competitive positions and ensure long term growth in the dynamic European landscape.

MARKET SEGMENTATION

This research report on the Europe test and measurement equipment market has been segmented and sub-segmented into the following categories.

By Offering

- Product

- General Purpose Test Equipment

- Mechanical Test Equipment

- Services

- Calibration Services

- Repair or After Sale Services

- Others

By Vertical

- Industrial

- Automotive & Transportation

- Electronics & Semiconductor

- Education & Government

- Healthcare & Dental

- Aerospace & Defense

- Manufacturing

- Telecom & IT

- Others

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe test and measurement equipment market?

The Europe test and measurement equipment market covers tools used for quality assurance, R&D, and regulatory compliance across electronics, automotive, and telecom industries.

How does the Europe test and measurement equipment market function?

The Europe test and measurement equipment market functions by providing precision instruments that validate product performance, ensure safety standards, and support manufacturing quality control.

What drives growth in the Europe test and measurement equipment market?

The Europe test and measurement equipment market grows due to 5G rollout, EV development, Industry 4.0 automation, and strict EU regulatory requirements for product testing.

Which countries lead the Europe test and measurement equipment market?

Germany leads the Europe test and measurement equipment market, followed by the UK, France, and Italy, supported by strong manufacturing and R&D infrastructure.

What products define the Europe test and measurement equipment market?

The Europe test and measurement equipment market includes general purpose equipment like oscilloscopes, multimeters, and spectrum analyzers, plus specialized mechanical test tools.

What industries shape the Europe test and measurement equipment market?

The Europe test and measurement equipment market serves electronics, automotive, aerospace, telecommunications, healthcare, and semiconductor manufacturing sectors.

How does regulation influence the Europe test and measurement equipment market?

EU directives on EMC, safety, and environmental compliance drive the Europe test and measurement equipment market by mandating rigorous product validation testing.

What trends affect the Europe test and measurement equipment market?

The Europe test and measurement equipment market sees growth in wireless testing, automated solutions, high-frequency equipment, and software-integrated platforms.

What challenges face the Europe test and measurement equipment market?

The Europe test and measurement equipment market faces rapid technology evolution, high R&D costs, skilled operator shortages, and competition from low-cost imports.

How does 5G impact the Europe test and measurement equipment market?

5G network deployment drives demand in the Europe test and measurement equipment market for high-frequency analyzers, protocol testers, and field measurement tools.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com