Europe Underfloor Heating Market Size, Share, Trends, and Growth Analysis Report, Segmented by Product Type, Application, System, Installation Type, and Country – Industry Forecast From 2026 to 2034

Europe Underfloor Heating Market Report Summary

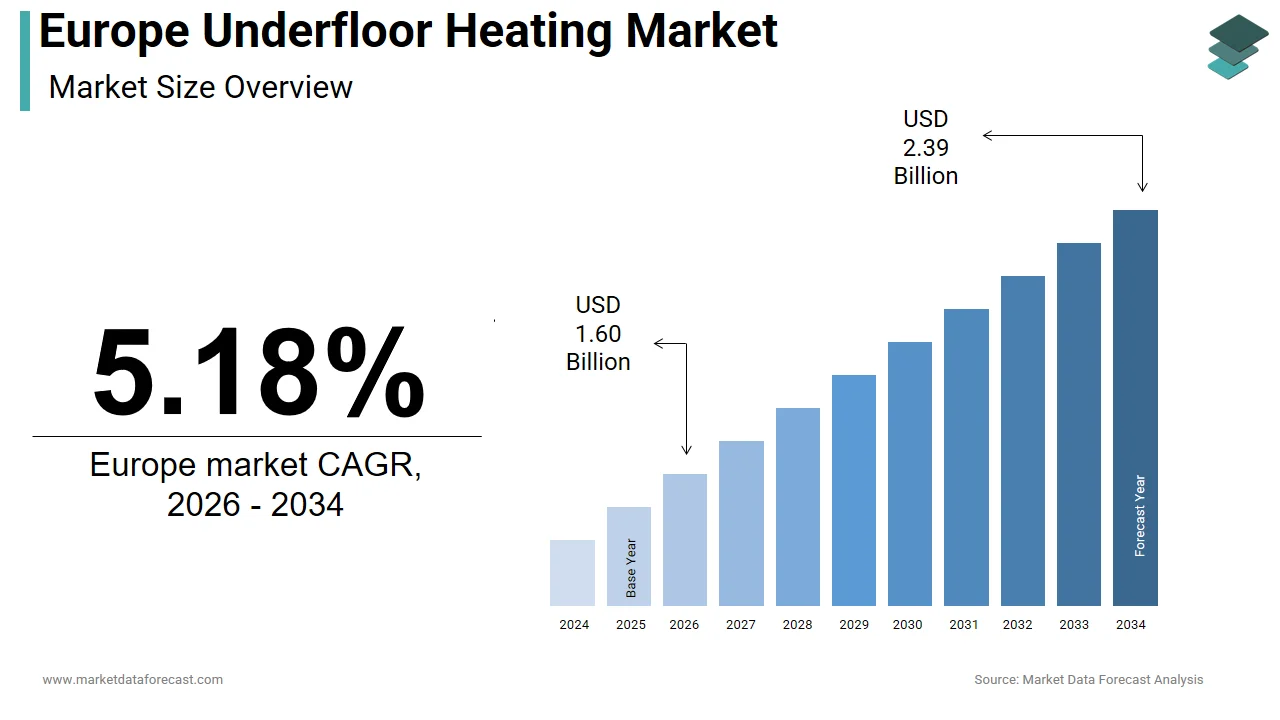

The Europe underfloor heating market was valued at USD 1.52 billion in 2025, is estimated to reach USD 1.60 billion in 2026, and is projected to reach USD 2.39 billion by 2034, growing at a CAGR of 5.18% from 2026 to 2034. Market growth is driven by increasing demand for energy-efficient heating systems, rising adoption of smart home technologies, and stringent regulations promoting sustainable building solutions. Underfloor heating systems offer improved energy efficiency, enhanced comfort, and space optimization, making them increasingly popular in residential and commercial applications. Additionally, the expansion of green building initiatives and renovation activities across Europe is further supporting market growth.

Key Market Trends

- Growing demand for energy-efficient and sustainable heating solutions.

- Increasing adoption of smart home and automation technologies.

- Rising focus on green buildings and eco-friendly construction.

- Expansion of renovation and retrofitting projects.

- Improved consumer preference for comfort and space-saving heating systems.

Segmental Insights

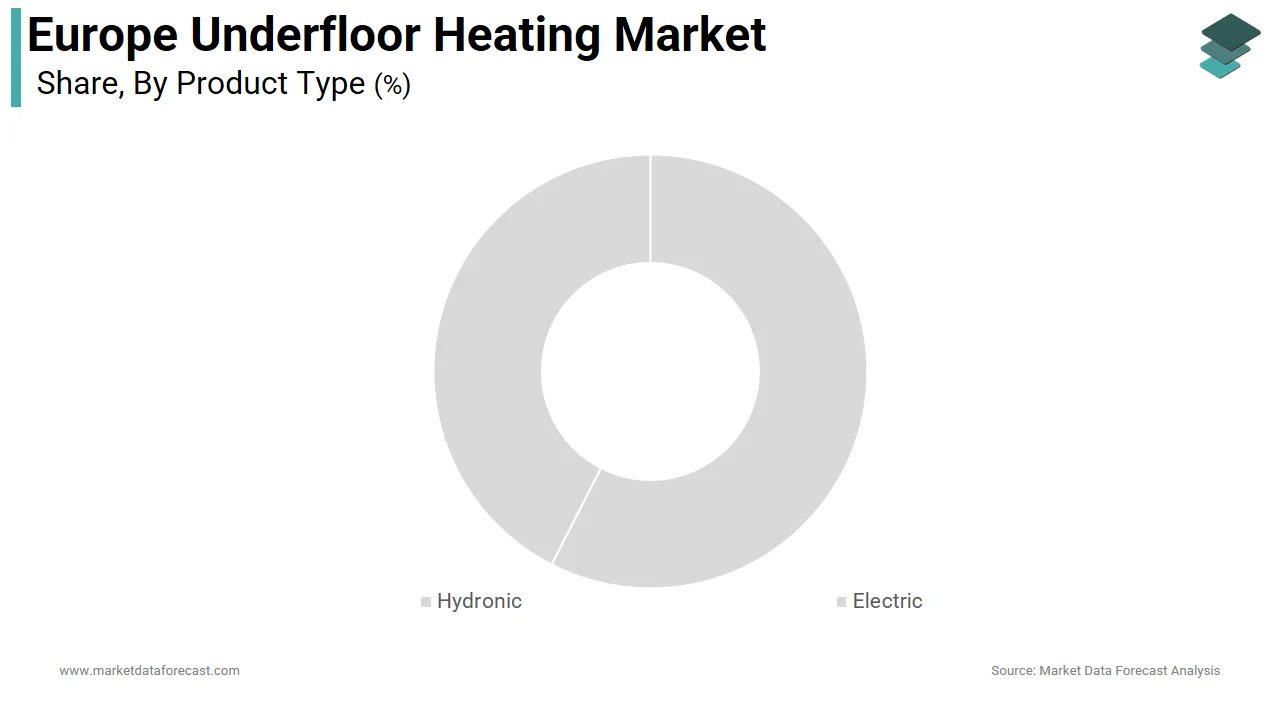

- Based on product type, the hydronic underfloor heating segment dominated the Europe underfloor heating market by capturing 65.5% share in 2025, driven by higher efficiency and suitability for large spaces.

- Based on application, the residential segment held a substantial share in 2025, supported by increasing home renovation and new housing developments.

- Based on installation type, the new installation segment led the market with 60.4% share in 2025, driven by integration in new construction projects.

Regional Insights

The Europe underfloor heating market is witnessing steady growth across major construction and renovation markets.

- Germany led the market in 2025 with 22.7% share, driven by strong construction activity and energy efficiency regulations.

- France followed with 16.8% share, supported by government incentives for sustainable housing.

- The United Kingdom holds a notable share due to increasing adoption of smart heating systems and home renovation trends.

Competitive Landscape

The Europe underfloor heating market is moderately competitive, with companies focusing on product innovation, energy efficiency, and integration with smart home systems. Strategic partnerships and expansion into renovation markets are key growth strategies.

Prominent companies operating in the Europe underfloor heating market include Uponor Corporation, Honeywell International, Inc., Robert Bosch GmbH, Rehau Group, Pentair PLC, Mitsubishi Electric Corporation, Emerson Electric Co., Schneider Electric SE, Siemens AG, The Danfoss Group, and Warmup PLC.

Europe Underfloor Heating Market Size

The size of the Europe underfloor heating market was worth USD 1.52 billion in 2025. The regional market is anticipated to grow at a CAGR of 5.18% from 2026 to 2034 and be worth USD 2.39 billion by 2034 from USD 1.60 billion in 2026.

Underfloor heating (UFH) is a form of central heating that uses the entire floor surface to distribute heat evenly throughout a room. This technology offers a uniform heat distribution that eliminates cold spots and enhances indoor air quality by reducing dust circulation compared to traditional radiators. The adoption of these systems is closely linked to the region’s stringent energy efficiency standards and the growing preference for sustainable building practices. As per Eurostat, buildings account for approximately 40 percent of final energy consumption in the European Union, making heating efficiency a critical policy target. The European Commission has emphasized that renovating existing building stock is essential to meet climate goals, with a focus on replacing inefficient heating solutions. Furthermore, the rise in new residential constructions incorporating smart home technologies supports the integration of underfloor heating, which can be precisely controlled via digital interfaces. According to Eurostat, space heating represents 62.5 percent of household energy use in the European Union, highlighting the potential impact of efficient systems. The shift towards low-temperature heating sources, such as heat pumps, also favors underfloor installations due to their compatibility with lower operating temperatures. These factors collectively drive the transition from conventional radiators to underfloor solutions across both residential and commercial sectors in Europe.

MARKET DRIVERS

Stringent Energy Efficiency Regulations and Green Building Standards Drive Adoption

The implementation of rigorous energy efficiency regulations across the region serves as a primary driver for the Europe underfloor heating market. The European Union’s Energy Performance of Buildings Directive mandates that all new buildings must be nearly zero energy buildings, which requires highly efficient heating systems. As stated by the European Commission, the vast majority of the European Union's building stock currently falls below modern energy performance standards, necessitating a widespread renovation movement under the newly revised Energy Performance of Buildings Directive. Underfloor heating systems operate at lower temperatures than traditional radiators making them ideal for integration with renewable energy sources such as heat pumps and solar thermal systems. This compatibility significantly reduces overall energy consumption and carbon emissions. The International Energy Agency highlights that transitioning from traditional fossil-fuel boilers to high-efficiency heat pumps is a critical step in decarbonising buildings and achieving global climate goals. Governments across Europe offer subsidies and tax incentives for installing energy-efficient heating solutions, further accelerating market growth. For instance, Germany’s Federal Office for Economic Affairs and Export Control provides substantial grants for replacing oil and gas heaters with sustainable alternatives. These financial incentives lower the initial investment barrier for homeowners and developers. Additionally, green building certifications such as BREEAM and LEED award points for installing efficient heating systems, encouraging commercial projects to adopt underfloor heating. The regulatory push towards decarbonization ensures that underfloor heating becomes a standard feature in modern European construction.

Growing Preference for Comfort and Aesthetic Interior Design Solutions

Consumer demand for enhanced thermal comfort and minimalist interior design greatly propels the expansion of the Europe underfloor heating market. Unlike radiators, which occupy wall space and create uneven heat distribution, underfloor systems provide consistent warmth throughout the room, eliminating cold corners. Trends within the European Thermal Management sector indicate that homeowners and architects increasingly favor heating solutions that prioritize minimalist interior design and enhanced living comfort. Underfloor heating frees up wall space, allowing for flexible furniture placement and uncluttered interiors, which is particularly valued in urban apartments with limited square footage. The technology also improves indoor air quality by reducing convection currents that circulate dust and allergens, benefiting individuals with respiratory issues. According to World Health Organization guidelines, improving indoor air quality is essential for respiratory health, with health benefits achieved by adopting clean heating technologies that reduce the presence of airborne contaminants and fine particles. The integration of smart thermostats allows users to control heating zones individually, enhancing personal comfort and energy savings. Modern electric underfloor heating systems are easy to install in retrofit projects, making them accessible for renovations. The luxury real estate market in countries like France and Italy frequently specifies underfloor heating as a premium feature, driving its adoption in high-end residential developments. This combination of health benefits, aesthetic appeal, and technological convenience sustains strong consumer interest.

MARKET RESTRAINTS

High Initial Installation Costs and Retrofitting Complexities Restrain Market Growth

The high initial installation cost and technical complexities associated with retrofitting existing buildings impede the growth of the Europe underfloor heating market. Installing hydronic underfloor heating requires extensive floor preparation, including insulation, screed laying, and pipe installation, which increases labor and material costs. As per the European Parliament, renovation projects often face barriers such as high upfront investment costs and limited access to financing, making expensive heating upgrades less attractive to homeowners. The need to raise floor levels can cause issues with door heights and transitions between rooms, requiring additional structural modifications. Electric systems, while easier to install, have higher operational costs in regions with expensive electricity, limiting their appeal for whole-house heating. According to Eurostat, energy prices in the EU have fluctuated significantly, with electricity prices remaining higher than natural gas in many member states. This economic disparity makes electric underfloor heating less competitive for primary heating sources. Furthermore, the disruption caused by installation in occupied homes discourages many residents from undertaking such projects. The lack of skilled installers familiar with modern underfloor systems can lead to improper installation and performance issues. These factors combined create a high barrier to entry, particularly for the large segment of existing housing stock that requires renovation. Installation processes need to become more streamlined and cost-effective. Until then, mass adoption in the retrofit sector will remain limited.

Compatibility Issues with Existing Flooring Materials and Thermal Resistance

Compatibility issues with various flooring materials and their thermal resistance properties pose a considerable restraint on the European underfloor heating market. Not all flooring types are suitable for underfloor heating, as some materials act as insulators, preventing efficient heat transfer. As per European Standard EN 1264, thick carpets and wooden floors with high thermal resistance can significantly reduce the heat output and efficiency of underfloor heating systems, whereas stone and ceramic tiles are highly conductive. Homeowners often hesitate to replace existing flooring due to the additional cost and effort involved. Wood flooring, for example, requires specific moisture content and stability to prevent warping under temperature changes, limiting the choice of materials. According to European Standard EN 1264, flooring materials must meet specific thermal resistance limits to ensure the optimal performance and maximum efficiency of underfloor heating systems. Many older buildings in Europe have solid wood floors or heritage tiles that are incompatible with modern heating systems without costly modifications. The risk of damaging expensive flooring materials due to improper temperature control also deters potential users. Additionally, the slow response time of hydronic systems makes it difficult to adjust quickly to changing weather conditions when paired with high resistance flooring. These technical limitations restrict the applicability of underfloor heating in certain residential contexts. Innovative flooring solutions with better thermal conductivity are not yet widely available and affordable. Until they are, this constraint will persist.

MARKET OPPORTUNITIES

Integration with Renewable Energy Sources and Heat Pump Systems Presents Opportunities

The increasing integration of UFH with renewable energy sources, particularly heat pumps, offers a significant opportunity for the European underfloor heating market growth. Heat pumps operate most efficiently at lower flow temperatures which aligns perfectly with the requirements of underfloor heating systems. According to the European Heat Pump Association (EHPA), the market has begun to recover following a period of contraction, with future growth closely tied to the stabilization of government support and the reduction of electricity taxes relative to fossil fuels. Underfloor heating maximizes the coefficient of performance of heat pumps by allowing them to run at optimal low temperatures reducing electricity consumption. This synergy supports the European Union’s goal of phasing out fossil fuel heating systems. As noted by the International Energy Agency (IEA), transitioning from traditional boilers to heat pumps significantly lowers carbon footprints across all major markets, particularly as national electricity grids become increasingly powered by renewable sources. New construction projects are increasingly designed with this combination in mind ensuring long term energy savings. Retrofitting older properties with insulated underfloor systems also enables the use of heat pumps where previously only high temperature radiators were feasible. Manufacturers are developing hybrid systems that combine underfloor heating with solar thermal panels further enhancing sustainability. The growing availability of green financing options for renewable heating installations encourages homeowners to invest in these integrated solutions. This trend towards sustainable heating infrastructure creates a robust demand pipeline for underfloor heating products.

Expansion of Smart Home Technology and Zone Control Systems

The expansion of smart home technology and advanced zone control systems provides a lucrative prospect for the Europe underfloor heating market. Modern underfloor heating systems can be integrated with smart thermostats and home automation platforms, allowing users to control temperature settings remotely via smartphones. As per the Smart Homes Market Report, the adoption of smart home devices in Europe is growing rapidly, with heating control being a key application. Zone control enables different rooms to be heated independently based on occupancy and usage patterns, optimizing energy efficiency. According to the European Commission, the deployment of intelligent heating controls and digital thermostats serves as a vital tool for reducing domestic energy waste by ensuring that heating is only active when and where it is truly required. This level of precision appeals to energy-conscious consumers and aligns with sustainability goals. The ability to schedule heating cycles and monitor energy usage in real time provides valuable insights for users. Manufacturers are developing user-friendly interfaces that simplify the management of complex heating systems. Integration with voice assistants and artificial intelligence algorithms further enhances convenience and automation. The rental market also benefits from smart controls, as landlords can monitor and manage heating usage in multiple properties. As smart home ecosystems become more standardized, the interoperability of underfloor heating systems with other devices will improve. This technological evolution drives upgrades and new installations in both residential and commercial sectors.

MARKET CHALLENGES

Shortage of Skilled Installers and Technical Expertise Poses Challenges

The shortage of skilled installers and technical expertise required for proper system design and installation is a significant challenge to the Europe underfloor heating market. Underfloor heating systems require precise calculation of heat loss pipe spacing and manifold configuration to ensure efficient operation. As per the European Construction Industry Federation there is a persistent skills gap in the construction sector with fewer young people entering specialized trades. Incorrect installation can lead to uneven heating leaks or system failures, which damage customer trust and increase maintenance costs. According to the European Plumbing and Heating Contractors Association training programs for underfloor heating installation are not uniformly standardized across member states. This lack of consistency results in varying quality of workmanship. The complexity of integrating underfloor heating with existing building structures requires experienced professionals who understand both hydraulic and electrical principles. Many general contractors lack the specific knowledge to handle these systems leading to reliance on specialized subcontractors who may be in short supply. Delays in finding qualified installers can prolong project timelines and increase costs. Additionally the rapid evolution of technology means that existing workers need continuous training to keep up with new products and smart controls. Addressing this skills deficit requires coordinated efforts between industry bodies educational institutions and governments. The workforce is not yet adequately trained. Consequently, installation quality and reliability may remain inconsistent.

Regulatory Fragmentation and Varying Building Codes Across Countries

Regulatory fragmentation and varying building codes across European countries are also a considerable hindrance for manufacturers and installers in the Europe underfloor heating market. Each country has its own standards for energy performance safety and installation practices, which complicates the development of uniform products. As per the European Committee for Standardization while efforts are made to harmonize standards national annexes and local regulations often differ significantly. This diversity requires manufacturers to adapt their products and documentation for each market increasing compliance costs and time to market. According to the European Commission the single market for construction products still faces barriers due to differing national interpretations of regulations. Installers operating across borders must navigate complex legal requirements which can hinder cross border trade and service provision. For example insulation requirements and maximum floor temperatures may vary between Germany and France, necessitating different system designs. This fragmentation limits economies of scale and increases the complexity of supply chain management. Small and medium sized enterprises often struggle to meet diverse regulatory demands, limiting their market reach. The lack of a unified European framework for underfloor heating certification creates uncertainty for investors and developers. Harmonizing these regulations would facilitate smoother market operations and innovation. Companies must invest heavily in local compliance strategies. This is necessary until greater regulatory alignment is achieved.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Application, System, Installation Type, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Uponor Corporation, Honeywell International, Inc., Robert Bosch GmbH, Rehau Group, Pentair PLC, Mitsubishi Electric Corporation, Emerson Electric Co., Schneider Electric SE, Siemens AG, The Danfoss Group, Warmup PLC, and Others. |

SEGMENTAL ANALYSIS

By Product Type Insights

The hydronic underfloor heating segment was the largest segment in the Europe underfloor heating market and accounted for a 65.5% share in 2025. This prominence of the segment is attributed to its superior energy efficiency and compatibility with renewable energy sources which align with European sustainability goals. Hydronic underfloor heating systems are highly favored for their ability to operate at low water temperatures, typically between 35 and 45 degrees Celsius, which makes them ideal partners for heat pumps. This synergy allows homeowners to reduce their energy consumption compared to traditional high temperature radiators. The European Commission’s Renewable Energy Directive encourages the adoption of such efficient combinations to meet climate targets. Hydronic systems distribute heat evenly across the floor surface eliminating cold spots and reducing the need for excessive thermostat settings. The long term operational savings of hydronic systems outweigh the higher initial installation costs, appealing to environmentally conscious consumers. Furthermore these systems can be integrated with solar thermal panels providing a fully renewable heating solution. The durability of hydronic pipes which can last over 50 years ensures a reliable investment for property owners. This combination of efficiency, sustainability, and longevity secures the dominant market position of hydronic underfloor heating. Hydronic underfloor heating is the preferred choice for large scale residential and commercial projects due to its scalability and cost-effectiveness for extensive areas. In new construction developments, developers prioritize hydronic systems because they can be installed during the building phase, minimizing disruption and cost. Hydronic systems allow for zonal control enabling different areas of a building to be heated independently, which enhances comfort and reduces waste. In commercial settings such as offices and retail spaces the uniform heat distribution improves employee productivity and customer comfort. The ability to connect multiple zones to a single manifold simplifies maintenance and management for facility operators. Additionally hydronic systems do not produce electromagnetic fields, making them safer for sensitive environments like hospitals and schools. These factors make hydronic underfloor heating the standard for large scale applications across Europe.

The electric underfloor heating segment is predicted to witness the highest CAGR of 8.5% during the forecast period. This swift growth of the segment is propelled by its ease of installation and suitability for retrofit projects and small spaces. Electric underfloor heating systems are gaining popularity due to their straightforward installation process which requires minimal structural changes to existing buildings. Unlike hydronic systems electric mats or cables can be laid directly beneath floor coverings such as tiles, laminate, or engineered wood without raising floor levels significantly. The thin profile of electric heating elements allows them to be installed in bathrooms, kitchens, and conservatories where space is limited. Homeowners prefer electric systems for quick upgrades because they do not require connection to a central boiler or complex plumbing work. The installation can often be completed in a single day reducing labor costs and inconvenience. This convenience drives demand among DIY enthusiasts and professional contractors alike. Furthermore, electric systems offer precise temperature control with fast response times allowing users to heat specific areas only when needed. This flexibility appeals to modern lifestyles where energy usage is monitored closely. The simplicity of electric underfloor heating ensures its rapid adoption in the retrofit market. The integration of electric underfloor heating with smart home technologies and renewable electricity sources is accelerating its growth. Electric systems are inherently compatible with digital thermostats and home automation platforms enabling remote control and scheduling via smartphones. Users can program heating schedules based on occupancy patterns ensuring that energy is not wasted on empty rooms. Additionally the rising availability of green electricity from solar photovoltaic panels allows homeowners to power their electric underfloor heating with clean energy. The trend supports the decarbonization of heating without the need for gas boilers. Electric underfloor heating also eliminates the risk of leaks associated with hydronic systems making it a safer option for apartments and multi-story buildings. The modular nature of electric systems allows for easy expansion or repair. Electric underfloor heating is growing in popularity as grids become greener and smarter. Consequently, the market is expanding rapidly.

By Application Insights

The residential application segment dominated the Europe underfloor heating market and accounted for a substantial share in 2025. This dominance of the segment is driven by the high volume of housing construction and renovation activities across the region. The residential sector is the primary consumer of underfloor heating due to the continuous construction of new homes and the renovation of existing properties. Developers recognize that underfloor heating adds value to properties by offering modern comfort and energy efficiency. The European Commission’s Renovation Wave strategy aims to double annual energy renovation rates which further boosts demand for efficient heating solutions in existing homes. Underfloor heating is particularly popular in bathrooms and kitchens where warm floors enhance comfort. The aesthetic benefit of removing radiators also appeals to homeowners seeking minimalist interiors. In new builds underfloor heating is often mandated by local building codes that require high energy performance standards. This regulatory support ensures a steady demand from the residential sector. Additionally the rise of self-build projects allows homeowners to customize their heating systems, choosing underfloor options for better control. The sheer scale of residential activity compared to commercial or industrial sectors ensures its leading position. Consumer demand for enhanced thermal comfort and health benefits significantly drives the adoption of underfloor heating in residential settings. Underfloor heating provides radiant heat which warms objects and people directly rather than just the air, resulting in a more natural and comfortable environment. Underfloor heating eliminates cold drafts and reduces humidity levels preventing mold growth, which is a common issue in older European homes. Parents appreciate the safety of underfloor heating as there are no hot surfaces or sharp edges unlike traditional radiators. This safety feature is particularly valued in households with young children. The ability to maintain consistent temperatures throughout the day enhances overall well being and sleep quality. Surveys indicate that homeowners who install underfloor heating report higher satisfaction levels with their living conditions. This positive user experience drives word of mouth recommendations and repeat purchases. The focus on health and comfort makes underfloor heating a preferred choice for residential applications across Europe.

The commercial application segment is estimated to register the fastest CAGR of 7.8% from 2026 to 2034 owing to the expansion of office spaces, retail outlets, ts and hospitality venues prioritizing energy efficiency. Strict energy efficiency regulations for commercial buildings are a major driver for the rapid growth of underfloor heating in this segment. The European Union’s Energy Performance of Buildings Directive requires commercial properties to meet high standards of energy consumption and carbon emissions. Underfloor heating allows for lower operating temperatures which reduces energy costs for businesses. Office buildings, hotels, and retail stores are increasingly adopting underfloor systems to comply with green building certifications such as LEED and BREEAM. Underfloor heating also frees up wall space, allowing for flexible interior layouts, which is valuable in retail and office environments. The uniform heat distribution enhances customer and employee comfort leading to increased productivity and sales. Facility managers appreciate the low maintenance requirements of underfloor systems compared to traditional radiators. The long-term cost savings and compliance benefits drive the rapid adoption of underfloor heating in the commercial sector. As businesses strive to meet sustainability goals the demand for efficient heating solutions continues to rise. The expansion of the hospitality and retail sectors in Europe is another key factor contributing to the fast growth of underfloor heating in commercial applications. Hotels, resorts, and restaurants prioritize guest comfort and ambiance, making underfloor heating an attractive option. Underfloor heating provides a luxurious feel in lobbies, bathrooms, and guest rooms, enhancing the guest experience. In retail stores, warm floors encourage customers to spend more time browsing, especially in colder months. The aesthetic appeal of invisible heating allows for unrestricted display arrangements and interior design creativity. Shopping malls and airports also utilize underfloor heating in large open spaces where traditional heating is inefficient. The ability to zone heating in different areas of a commercial property allows for optimized energy use based on foot traffic. This flexibility and comfort drive the adoption of underfloor heating in the growing hospitality and retail sectors.

By Installation Type Insights

The new installation segment held the majority share of 60.4% of the Europe underfloor heating market in 2025. This supremacy of the segment is credited to the ease of integration during the construction phase and regulatory mandates for energy efficiency. Regulatory mandates requiring new buildings to meet strict energy efficiency standards are the primary driver for the dominance of the new installation segment. The European Union’s Energy Performance of Buildings Directive mandates that all new constructions must be nearly zero-energy buildings. Builders and developers integrate underfloor heating during the initial construction phase to comply with these regulations without the complexities of retrofitting. Underfloor heating is often specified in architectural plans to maximize floor space and aesthetic appeal. The cost of installing underfloor heating during construction is significantly lower than retrofitting as it avoids the need to remove existing floors. This economic advantage makes it the default choice for new projects. Additionally green building certifications often require underfloor heating to achieve higher ratings. The alignment with regulatory and certification requirements ensures that new installations remain the largest segment in the market. Installing underfloor heating during new construction is more cost effective and offers greater design flexibility compared to retrofitting. This planning ensures efficient heat distribution and minimizes material waste. Developers can choose between hydronic and electric systems based on the building’s energy source and layout. The absence of radiators allows for flexible furniture arrangement and maximizes usable floor space which is a selling point for buyers. The installation process in new builds is streamlined as it coincides with other flooring preparations reducing labor time. Architects appreciate the freedom to design open-plan spaces without worrying about radiator placement. This design freedom is particularly valued in modern minimalist architecture. The combination of lower installation costs design benefits and market appeal solidifies the dominance of the new installation segment.

The retrofit installation segment is anticipated to witness the fastest CAGR of 9.2% between 2026 and 2034. This quick surge of the segment is fuelled by the vast number of older buildings requiring energy upgrades and the availability of low-profile systems. The vast number of older buildings in Europe that require energy efficiency upgrades presents a significant opportunity for retrofit underfloor heating. Homeowners are increasingly replacing old radiators with underfloor heating to improve comfort and reduce energy bills. Modern low-profile underfloor heating systems are designed specifically for retrofits requiring minimal floor height increase. The support lowers the financial barrier for retrofit projects. The desire to modernize interiors and remove unsightly radiators also drives demand. Retrofitting allows homeowners to enjoy the benefits of underfloor heating without moving house. The growing awareness of energy conservation and comfort fuels the rapid growth of the retrofit segment. Technological advancements in low profile underfloor heating systems have made retrofitting easier and more accessible. Traditional underfloor heating required thick screed layers which raised floor levels significantly, causing issues with doors and stairs. Newer systems use thin insulation boards and compact pipes or cables that add only a few millimeters to floor height. The innovation addresses one of the main barriers to retrofit adoption. Electric underfloor heating mats are particularly suitable for retrofits as they are thin and easy to install. The availability of specialized retrofit kits simplifies the process for DIY enthusiasts. These technological improvements expand the applicability of underfloor heating to a wider range of existing homes. As more homeowners become aware of these options, the retrofit segment continues to grow rapidly.

COUNTRY LEVEL ANALYSIS

Germany Underfloor Heating Market Analysis

Germany led the Europe underfloor heating market and captured a share of 22.7% in 2025. The national push for sustainable energy and improved efficiency is heavily influencing the rising demand for underfloor heating systems. Germany has stringent building regulations that require new constructions to meet high energy standards. According to the Federal Ministry for Economic Affairs and Climate Action (BMWK), financial incentives are provided for the installation of high-efficiency heating systems, specifically when underfloor components are integrated with heat pump technology. The German housing market sees significant new construction activity particularly in urban areas. Reports from the Federal Statistical Office (Destatis) indicate a significant downturn in residential construction permits, which currently acts as a primary headwind for the installation market. The prevalence of heat pumps in Germany further boosts underfloor heating adoption due to their compatibility. German consumers are environmentally conscious and willing to invest in sustainable technologies. The renovation of older buildings is also supported by government grants encouraging the switch from oil and gas heaters. Major manufacturers of heating systems are based in Germany, fostering innovation and availability. The country’s robust infrastructure and skilled workforce ensure high-quality installations. These factors combine to make Germany the largest market for underfloor heating in Europe.

France Underfloor Heating Market Analysis

France was the next prominent country in the Europe underfloor heating market and held a 16.8% in 2025. Aesthetic considerations and the desire for improved comfort are propelling the widespread adoption of radiant floor heating. France has a large number of historic buildings undergoing renovation, where underfloor heating is preferred for its invisibility. As per the Ministry of Ecological Transition, national renovation grants are designed to incentivize homeowners to replace outdated equipment with modern, energy-efficient heating solutions. The French real estate market values properties with modern amenities, including underfloor heating. INSEE suggests that while underfloor heating is a growing preference in the high-end residential sector, it competes with various other low-carbon electric and hydraulic systems in new builds. The popularity of tile and stone flooring in French homes complements underfloor heating systems. The climate in certain regions of France also necessitates efficient heating solutions. Government policies promoting low-carbon heating sources support the integration of underfloor heating with heat pumps. The presence of established heating companies in France ensures wide availability and service support. Consumer preference for luxury and comfort sustains demand in both residential and commercial sectors. These dynamics ensure France maintains a strong position in the regional market.

United Kingdom Underfloor Heating Market Analysis

The United Kingdom occupies a promising share of the Europe underfloor heating market. Stringent UK environmental targets and a push for improved domestic energy efficiency are accelerating market demand. The UK government has set ambitious targets for net zero emissions, influencing building regulations. Under the Future Homes Standard and updated Building Regulations, new residential developments are increasingly mandated to adopt low-carbon heating technologies to phase out fossil fuel use. Underfloor heating is popular in new developments, particularly in bathrooms and extensions. The UK has a high rate of home renovations where homeowners seek to improve comfort and energy efficiency. The UK Green Building Council identifies radiant floor systems as a key technology for achieving thermal comfort while maintaining the low flow temperatures required for renewable energy efficiency. The rise of heat pump installations in the UK supports the adoption of underfloor heating. Consumer awareness of the benefits of underfloor heating, such as reduced dust and even heat distribution, is growing. The rental market also sees increased installation of underfloor heating to attract tenants. Government incentives like the Boiler Upgrade Scheme encourage the switch to renewable heating systems. These factors contribute to the UK’s significant share in the European market.

Italy Underfloor Heating Market Analysis

Italy holds a significant position in the Europe underfloor heating market. The country’s preference for tile and marble flooring makes underfloor heating a natural choice. Italy has a strong construction sector with ongoing residential and commercial projects. Following the expiration of major fiscal "bonus" programs, the Italian National Institute of Statistics (ISTAT) has noted a cooling period in residential building activity and renovation volumes. Underfloor heating is widely used in luxury villas and apartments for its aesthetic and comfort benefits. The Italian climate varies, with colder northern regions requiring efficient heating solutions. Government incentives for energy efficiency renovations support the adoption of underfloor heating. According to industry associations, the market is shifting toward hybrid configurations where radiant floors are paired with modern condensing systems or heat pumps to optimize seasonal performance. The tourism industry drives demand for underfloor heating in hotels and resorts. Italian consumers value design and quality, making underfloor heating a preferred option. The availability of skilled installers and local manufacturers supports market growth. These factors ensure Italy remains a key player in the European underfloor heating market.

Spain Underfloor Heating Market Analysis

Spain is likely to expand notably in the Europe underfloor heating market from 2026 to 2034. Its growing construction sector and focus on energy efficiency drive demand. Spain has seen an increase in new residential developments, particularly in coastal areas. According to the Ministry of Transport, Mobility, and Urban Agenda, the construction sector is navigating a period of stabilization as it adjusts to changing financing costs and urban development policies. Underfloor heating is popular in modern apartments and villas for its comfort and space-saving benefits. The mild climate in many parts of Spain means heating is used seasonally, but efficiency is still valued. Government regulations on the energy performance of buildings encourage the use of efficient heating systems. The Spanish Association of Heating and Air Conditioning (AFEC) shows that aerothermal heat pumps have become the preferred energy source for underfloor heating systems due to their ability to provide both heating and cooling. The renovation of older properties also contributes to market growth. Spanish consumers are increasingly aware of the health benefits of underfloor heating. The tourism sector drives demand in hospitality venues. These factors support Spain’s position in the European market.

COMPETITIVE LANDSCAPE

The competition in the Europe underfloor heating market is characterized by a mix of established multinational corporations and specialized regional manufacturers. Leading players compete based on technological innovation, product reliability, and after-sales support. The market exhibits a moderate level of consolidation as major companies acquire smaller firms to expand their technological capabilities. Differentiation is achieved through the development of smart control systems that integrate with home automation platforms. Price competition exists but is often secondary to the value proposition of energy efficiency and comfort. New entrants face barriers due to the need for technical expertise and compliance with strict building regulations. However, niche players continue to emerge with specialized solutions for retrofit applications. Collaborative ecosystems are becoming increasingly important as stakeholders seek interoperable systems. The focus on sustainability and digital transformation drives continuous innovation. Companies that successfully integrate these elements while maintaining strong distributor relationships are best positioned to succeed. Regulatory pressures regarding energy efficiency further shape the competitive landscape by favoring advanced technologies.

KEY MARKET PLAYERS

The leading companies operating in the Europe underfloor heating market include:

- Uponor Corporation

- Honeywell International, Inc.

- Robert Bosch GmbH

- Rehau Group

- Pentair PLC

- Mitsubishi Electric Corporation

- Emerson Electric Co.

- Schneider Electric SE

- Siemens AG

- The Danfoss Group

- Warmup PLC

TOP PLAYERS IN THE MARKET

- Uponor Corporation is a leading provider of sustainable living and working solutions with a strong presence in the Europe underfloor heating market. The company specializes in hydronic systems that integrate seamlessly with renewable energy sources. Uponor contributes to the global market by promoting energy-efficient building practices and smart water management. Recent actions include the expansion of its digital platform Uponor Smatrix, which allows for precise control and monitoring of heating systems. This innovation enhances user comfort and reduces energy consumption. Uponor also focuses on strategic partnerships with installers and contractors to improve service quality. The company invests heavily in research and development to create durable and eco-friendly piping solutions. These efforts strengthen its reputation as a pioneer in sustainable heating technologies. Uponor’s commitment to circular economy principles ensures long-term value for customers and stakeholders alike.

- Rehau Group is a global polymer processing expert with a significant footprint in the Europe underfloor heating market. The company offers comprehensive heating and cooling solutions for residential and commercial applications. Rehau contributes to the global market through its innovative RAUTHERMEX pipe technology, which ensures high performance and reliability. Recent initiatives involve the launch of smart home integration tools that connect underfloor heating with broader building automation systems. Rehau emphasizes sustainability by using recycled materials in its production processes. The company strengthens its market position by providing extensive training programs for technicians and engineers. This focus on education ensures proper installation and optimal system performance. Rehau also collaborates with architects and developers to design energy-efficient buildings. Their holistic approach to construction solutions drives the adoption of underfloor heating across Europe.

- Danfoss A/S is a world leader in engineering solutions with a dominant role in the Europe underfloor heating market. The company provides advanced control systems and components that optimize heating efficiency. Danfoss contributes to the global market by enabling the transition to green energy through smart heating controls. Recent actions include the introduction of AI-driven algorithms that predict heating needs based on weather and usage patterns. This technology maximizes energy savings and comfort for users. Danfoss actively participates in industry standards development to promote interoperability and safety. The company expands its distribution network to reach more customers across Europe. By focusing on digitalization and electrification, Danfoss supports the decarbonization of the heating sector. Their robust portfolio of valves, thermostats, and controllers makes them a preferred partner for system integrators.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe underfloor heating market primarily focus on product innovation and digital integration to maintain a competitive advantage. Companies invest heavily in research and development to create energy-efficient systems compatible with heat pumps and renewable energy sources. Strategic partnerships with construction firms and installers are common to ensure proper implementation and service quality. Manufacturers emphasize sustainability by developing eco-friendly materials and promoting circular economy practices. Expansion into smart home ecosystems allows firms to offer integrated control solutions that enhance user convenience. Additionally, companies provide extensive training and certification programs for technicians to address the skills gap. Mergers and acquisitions are utilized to broaden product portfolios and enter new geographic markets. Pricing strategies often highlight long-term energy savings rather than initial costs. These strategies collectively enable key participants to meet evolving regulatory requirements and customer preferences effectively.

MARKET SEGMENTATION

This research report on the Europe underfloor heating market has been segmented and sub-segmented into the following categories.

By Product Type

- Hydronic

- Electric

By Application

- Residential

- Commercial

- Industrial

By System

- Heating System

- Control System

By Installation Type

- New Installation

- Retrofit Installation

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe underfloor heating market?

The Europe underfloor heating market covers systems that heat buildings from the floor upward. It includes hydronic and electric solutions for homes, offices, and commercial spaces.

How does the Europe underfloor heating market function?

The Europe underfloor heating market functions by circulating warm water or electric heat through floor systems to deliver even indoor warmth and higher comfort.

What drives growth in the Europe underfloor heating market?

The Europe underfloor heating market grows because of energy efficiency goals, low-carbon construction, smart heating demand, and renovation of older buildings.

Which countries lead the Europe underfloor heating market?

The Europe underfloor heating market is led by Germany, with the UK, France, Italy, and the Nordics also contributing strongly through building upgrades and new construction.

What types define the Europe underfloor heating market?

The Europe underfloor heating market includes hydronic systems and electric systems. These are used across residential, commercial, and renovation projects.

What applications shape the Europe underfloor heating market?

The Europe underfloor heating market serves homes, apartments, offices, retail spaces, hotels, and other buildings where comfort and even heat distribution are important.

How does regulation influence the Europe underfloor heating market?

The Europe underfloor heating market is shaped by carbon reduction rules, energy performance standards, and incentives for sustainable heating systems.

What trends affect the Europe underfloor heating market?

The Europe underfloor heating market is influenced by smart controls, renewable integration, modular installation, and demand for healthier indoor comfort.

What challenges face the Europe underfloor heating market?

The Europe underfloor heating market faces high installation costs, retrofit complexity, and dependence on construction activity in some countries.

How does hydronic heating impact the Europe underfloor heating market?

The Europe underfloor heating market benefits from hydronic systems because they offer strong efficiency, consistent heat, and compatibility with renewable energy.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com