Europe Uranium Market Size, Share, Trends & Growth Forecast Report By Type, By Application, and By Country (France, Russia, United Kingdom, Sweden, Czech Republic & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Uranium Market Size

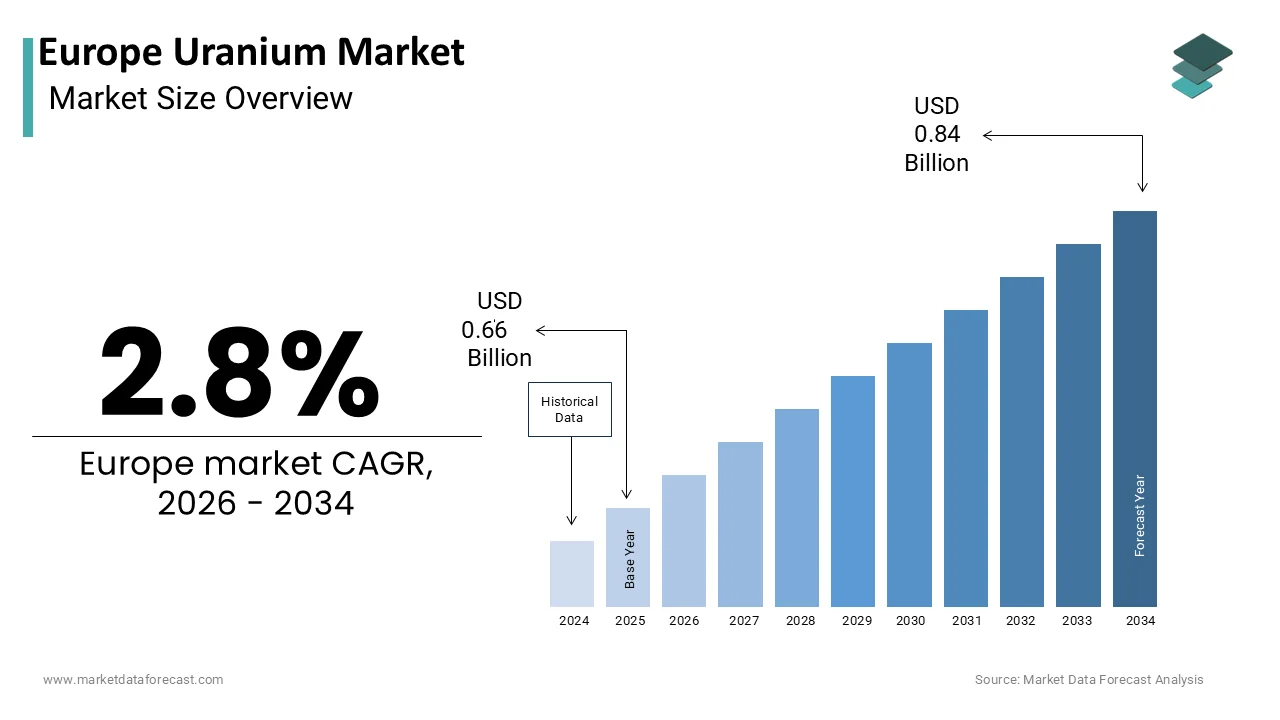

The Europe uranium market was valued at USD 0.66 billion in 2025, is estimated to reach USD 0.68 billion in 2026, and is projected to reach USD 0.84 billion by 2034, growing at a CAGR of 2.8% from 2026 to 2034.

The Europe uranium market constitutes a specialized segment of the global nuclear fuel cycle characterized by the procurement, conversion, and enrichment of uranium for use in nuclear power generation. Although Europe possesses limited domestic uranium mining activities, the region remains a pivotal consumer due to its extensive network of operational nuclear reactors. The market dynamics are heavily influenced by geopolitical shifts, energy security concerns, and the continent’s decarbonization objectives. As per the International Atomic Energy Agency, Europe accounts for approximately 25% of the world’s nuclear electricity generation, highlighting the critical role of uranium in the regional energy mix. The European Union has increasingly recognized nuclear energy as a transitional tool for achieving climate neutrality under the Taxonomy Regulation. According to Eurostat, nuclear energy provided about 24% of the total electricity production in the EU in recent years, underscoring its significance in the baseline load supply. The supply chain relies predominantly on imports from countries such as Kazakhstan, Canada, and Australia, which is making supply security a strategic priority. According to the data from the World Nuclear Association, several European nations are extending the operational lifetimes of existing reactors, thereby sustaining long-term demand for uranium fuel. The market is also shaped by regulatory frameworks governing nuclear safety, waste management, and non-proliferation. These factors collectively define the operational landscape where energy independence and environmental sustainability drive procurement strategies and investment in nuclear infrastructure across the continent.

MARKET DRIVERS

Strategic Shift towards Energy Security and Independence

The critical need for energy autonomy has become a primary catalyst for the European uranium market, particularly after recent disruptions in natural gas availability. European nations are re-evaluating their energy mixes to reduce reliance on imported fossil fuels and ensure stable electricity provision. According to the European Commission, the REPowerEU plan emphasizes the need for diverse and secure energy sources, including nuclear power, to mitigate supply risks. This policy shift has led to renewed interest in maintaining and even expanding nuclear capacity in several member states. As per data from the International Energy Agency, the share of nuclear power in the European electricity mix is expected to remain stable or increase slightly as countries prioritize energy autonomy. France, for instance, has announced plans to construct new reactors while other nations, like Poland, are developing their first nuclear programs. The recognition of nuclear energy as a reliable base load source complements intermittent renewable energies such as wind and solar. This strategic realignment ensures consistent demand for uranium as the fundamental fuel for nuclear fission. Governments are facilitating long-term contracts with uranium suppliers to secure future deliveries. The emphasis on sovereign energy capabilities reduces vulnerability to external market fluctuations. This geopolitical context creates a robust and sustained demand environment for uranium in Europe.

Regulatory Recognition of Nuclear Energy in Climate Goals

The official inclusion of nuclear power within the European Union’s sustainable finance framework is further boosting the expansion of the European uranium market, as it unlocks critical funding for the sector. This regulatory milestone allows nuclear projects to access green bonds and sustainable financing mechanisms that were previously restricted. According to the European Parliament, the delegated act on climate change mitigation acknowledges nuclear energy as a transitional activity contributing to climate objectives. This designation encourages private and public investments in nuclear infrastructure and fuel supply chains. As per the World Nuclear Industry Status Report, several European countries have revised their national energy plans to include nuclear power as a key component of their decarbonization strategies. The extension of reactor lifetimes in countries like Sweden and Belgium further sustains uranium consumption. The regulatory clarity reduces uncertainty for utilities and investors, fostering a favorable environment for long-term planning. The alignment with the European Green Deal objectives positions nuclear energy as a complementary technology to renewables. This policy supports the modernization of existing plants and the development of new projects. Consequently, the demand for uranium remains robust as nuclear power plays an integral role in meeting the EU’s 2050 climate neutrality targets.

MARKET RESTRAINTS

Public Opposition and Political Resistance in Key Markets

The growth of the uranium market is significantly hindered by deep-seated political friction and public skepticism regarding nuclear power in several major nations. Historical incidents and concerns regarding radioactive waste disposal have fostered skepticism among certain populations and political groups. According to Eurobarometer surveys, attitudes towards nuclear energy vary significantly across member states, with some countries maintaining strong anti-nuclear sentiments. Germany’s decision to phase out its remaining nuclear power plants exemplifies the impact of political will driven by public opinion. As per the German Federal Ministry for Economic Affairs and Climate Action, the exit from nuclear energy was finalized despite energy security concerns, reflecting deep-seated societal preferences. This political stance reduces the overall demand for uranium within the region and discourages new investments in nuclear infrastructure. Other countries face similar pressures where local protests and legal challenges delay licensing and construction processes. The lack of social license to operate can lead to premature shutdowns and hinder the expansion of nuclear capacity. Anti-nuclear lobbying influences legislative frameworks, imposing stringent regulations that increase operational costs. The divergence in national policies creates a fragmented market environment. This socio-political landscape limits the growth potential of the uranium market in Europe. Overcoming these barriers requires extensive public engagement and transparent communication about safety and benefits.

Complex Waste Management and Decommissioning Liabilities

Managing radioactive waste and handling the long-term costs of decommissioning old plants are substantial economic burdens that restrain market expansion. The safe storage and disposal of spent nuclear fuel and high-level waste require sophisticated infrastructure and substantial financial provisions. According to the European Commission, each member state is responsible for managing its own radioactive waste, leading to varied approaches and capabilities. The lack of a unified European solution for final disposal creates uncertainty and delays. As per data from the National Radioactive Waste Management Agency in France, the construction of deep geological repositories faces technical and societal hurdles requiring decades of planning and investment. These liabilities deter new entrants and impose financial burdens on existing operators. The high costs of decommissioning aging reactors further strain utility budgets, potentially affecting funds available for fuel procurement. Regulatory requirements for waste handling are stringent and evolving, adding to compliance complexities. Public concern over waste safety often translates into political pressure against nuclear expansion. The unresolved issue of long-term waste storage undermines the perceived sustainability of nuclear energy. These factors collectively restrain the market by increasing the total cost of ownership for nuclear power. Addressing these challenges requires coordinated European efforts and technological innovation.

MARKET OPPORTUNITIES

Development of Small Modular Reactors and Advanced Technologies

The advent of Small Modular Reactors (SMRs) and next-generation reactor designs offers a major growth path for the European uranium market by providing more adaptable and cost-efficient power options. SMRs require less initial capital and can be deployed in diverse locations, including remote areas and industrial sites. According to the International Atomic Energy Agency, over 70 SMR designs are under development globally, with several European companies actively participating in this innovation. These reactors offer enhanced safety features and reduced waste production, appealing to regulators and investors. As per the European Industrial Alliance on Small Modular Reactors, the deployment of SMRs could revitalize the nuclear sector by providing customizable energy options. The modular nature allows for factory fabrication and quicker assembly, reducing construction risks. This technology opens new markets for uranium beyond traditional large-scale power plants. Industrial applications such as hydrogen production and desalination can utilize SMRs, creating additional demand streams. The European Union supports research and demonstration projects through funding programs, fostering technological leadership. The potential for SMRs to complement renewable energy systems enhances grid stability. This technological evolution diversifies the application of uranium and stimulates market growth. Early adopters can gain competitive advantages in the emerging low-carbon energy landscape.

Expansion of Nuclear Fuel Services and Enrichment Capabilities

Broadening Europe's internal capacity for uranium conversion and enrichment represents a key opportunity for the European uranium market to bolster supply chain independence. Currently, Europe relies heavily on imported enriched uranium, primarily from Russia and other non-EU countries. According to the World Nuclear Association, establishing domestic enrichment capabilities can strengthen energy sovereignty and security. Several European companies are investing in advanced centrifuge technologies to increase local production capacity. As per industry reports, the development of alternative enrichment sources is a strategic priority for many utilities seeking to diversify their supply chains. The European Uranium Enrichment Initiative aims to boost regional capabilities, ensuring reliable fuel availability. This shift creates opportunities for technology providers and service companies specializing in fuel fabrication. The localization of fuel services reduces logistical risks and geopolitical vulnerabilities. It also supports high-skilled jobs and technological innovation within the region. The demand for high-assay low-enriched uranium for advanced reactors further drives this segment. Collaborative efforts among European nations can create a robust internal market for fuel services. This strategic autonomy enhances the competitiveness of the European nuclear industry. The investment in fuel infrastructure supports long-term market stability.

MARKET CHALLENGES

Geopolitical Dependencies and Supply Chain Vulnerabilities

The European uranium market is currently wrestling with its significant reliance on external suppliers, which makes the region susceptible to global trade shocks. The region imports the majority of its uranium and relies on a few key countries for conversion and enrichment services. According to the United States Geological Survey, Kazakhstan, Canada, and Australia are the primary sources of uranium imports for Europe. Disruptions in these supply routes due to political tensions or trade restrictions can severely impact availability. As per the European External Action Service, the reliance on Russian nuclear fuel services poses a strategic risk, prompting efforts to diversify suppliers. The concentration of processing capabilities in a handful of nations creates bottlenecks. Any instability in producing regions can lead to price volatility and supply shortages. The lack of domestic mining limits Europe’s ability to control upstream supplies. Logistics and transportation of nuclear materials involve strict security and regulatory requirements, adding complexity. Currency fluctuations and trade barriers further complicate procurement. Ensuring a resilient supply chain requires strategic partnerships and stockpiling initiatives. The geopolitical landscape remains unpredictable, affecting long-term planning. Mitigating these risks involves significant investment in alternative sources and technologies. This dependency remains a critical challenge for market stability.

High Capital Costs and Long Lead Times for New Projects

The massive upfront financial requirements and decades-long development cycles of nuclear infrastructure pose a steep hurdle for expanding uranium demand, which is further challenging the European market growth. Constructing new nuclear power plants requires billions of euros and can take over a decade to complete. According to the International Energy Agency, the average cost of nuclear power plant construction has increased significantly in recent years due to regulatory requirements and safety standards. These financial barriers discourage private investment and limit the pace of new capacity addition. As per data from the World Nuclear Industry Status Report, many planned projects in Europe have faced delays and cost overruns, affecting their viability. The long timeline between investment decision and commercial operation creates uncertainty for uranium suppliers. Financing such projects is challenging given the perceived risks and competition from cheaper renewable alternatives. The complexity of licensing and permitting processes further extends timelines. These factors hinder the rapid expansion of nuclear capacity needed to boost uranium demand. Utilities must navigate intricate financial and regulatory landscapes to proceed. The slow pace of new developments constrains market growth potential. Addressing these challenges requires streamlined regulations and innovative financing models.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2025 to 2034 |

| Segments Covered | By Type, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Cameco Corporation, Kazatomprom, Orano S.A., Rio Tinto Group, BHP Group Limited, Uranium One Inc., Paladin Energy Ltd., CGN Mining Company Limited, Energy Fuels Inc., Denison Mines Corp., Yellow Cake plc, Urenco Group Limited |

SEGMENTAL ANALYSIS

By Type Insights

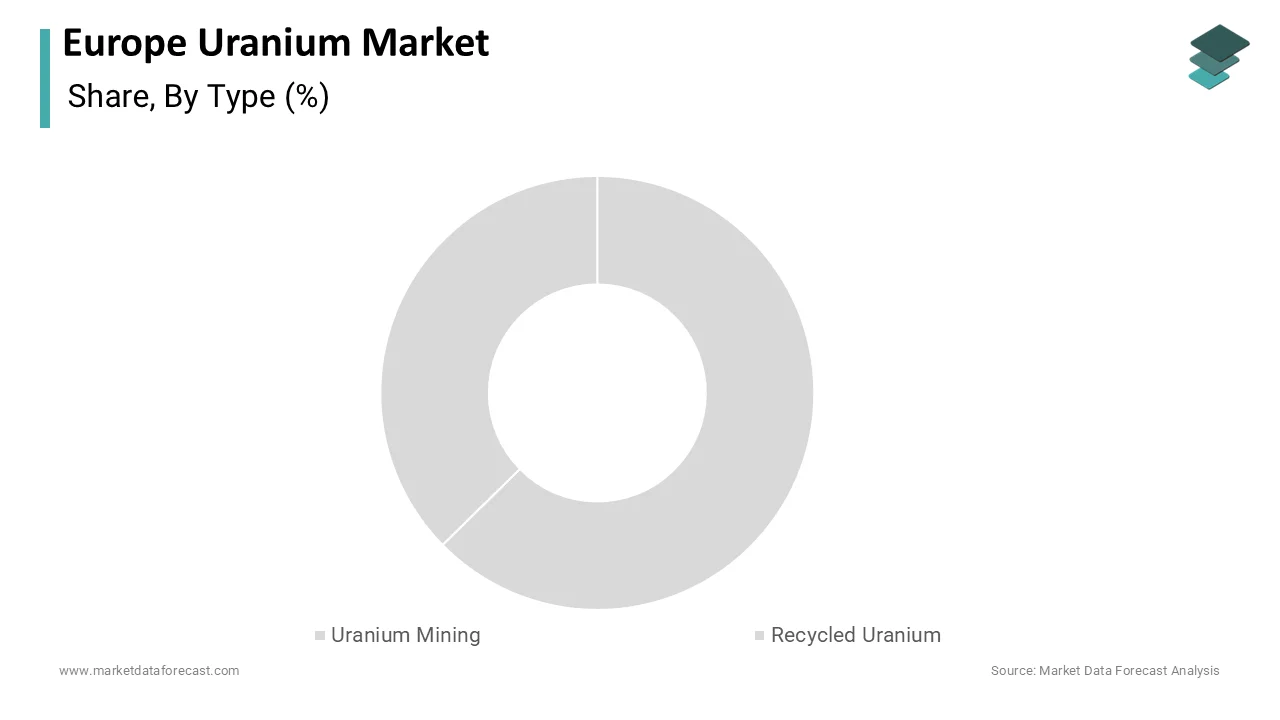

The uranium mining segment led the market by holding the highest share of 86.5% of the European uranium market in 2025. This dominance is driven by the fundamental requirement of fresh uranium fuel for the majority of operational nuclear reactors across the continent. Although Europe has negligible domestic mining activity, it remains a massive importer of mined uranium concentrate from global producers. According to the World Nuclear Association, the global nuclear power industry requires approximately 67000 tonnes of uranium annually, with European utilities securing long-term contracts for a significant portion of this supply. The reliability and established logistics of primary uranium supply chains make it the preferred source for base load power generation. As per data from the International Atomic Energy Agency, the existing fleet of light-water reactors in Europe is designed to operate on low-enriched uranium derived directly from mined ore. The economic viability of mining in countries like Kazakhstan and Canada ensures a steady flow of material to European conversion facilities. The sheer scale of electricity generation from nuclear sources in France, Sweden, and other nations necessitates continuous replenishment of fuel stocks. Primary mining offers a predictable quality and isotopic composition that is essential for safe and efficient reactor operation. The infrastructure for handling and processing mined uranium is well established within the European nuclear fuel cycle. This structural reliance on primary sources sustains the segment's market leadership despite emerging alternatives.

However, the recycled uranium segment is gaining momentum through efforts to improve fuel efficiency and sustainability, and is estimated to register a promising CAGR in the European uranium market during the forecast period due to the increasing efforts to enhance resource efficiency and reduce the environmental footprint of the nuclear fuel cycle through reprocessing spent nuclear fuel. Recycled uranium, also known as RepU, is recovered from used fuel rods and can be re-enriched for reuse in certain reactor types. According to the French Alternative Energies and Atomic Energy Commission, Orano operates one of the world’s largest reprocessing plants at La Hague, which recovers significant quantities of uranium and plutonium. As per the World Nuclear Institute, the use of recycled uranium helps conserve natural uranium resources and reduces the volume of high-level waste requiring disposal. European countries like France and Russia have advanced capabilities in reprocessing technology, allowing them to reintegrate RepU into the fuel cycle. The rising cost of primary uranium and strategic desires for energy independence drive interest in closed fuel cycles. Regulatory support for circular economy principles in the European Union further encourages the adoption of recycling technologies. Advances in enrichment techniques have made it easier to handle the specific isotopic characteristics of recycled uranium. This segment benefits from technological innovations that improve the economic feasibility of reprocessing. The push towards sustainable nuclear practices ensures that recycled uranium gains a larger share of the fuel mix.

By Application Insights

The nuclear power plants segment dominated the market by holding the leading share of the European uranium market in 2025. This overwhelming dominance is underpinned by the critical role of uranium as the primary fuel for generating electricity in nuclear reactors. According to Eurostat, nuclear energy accounted for roughly 24% of the total electricity production in the European Union in recent years, highlighting its significance in the regional energy mix. The operation of over 100 nuclear reactors across Europe requires a consistent and substantial supply of uranium fuel assemblies. As per data from the International Energy Agency, the baseload power provided by nuclear plants is essential for grid stability and decarbonization efforts. Countries such as France, Slovakia, and Hungary rely heavily on nuclear power for their national electricity needs, ensuring steady demand for uranium. The long operational lifetimes of these reactors, often extending to 40 or 60 years, create a predictable and long-term consumption pattern. The inability of other energy sources to fully replace the capacity of nuclear plants in the short term sustains this demand. Regulatory frameworks supporting nuclear energy as a low-carbon source further reinforce its position. The scale of fuel required for each refueling outage drives the majority of market transactions. This structural dependence on nuclear fission for large-scale power generation cements the segment's leadership.

On the other hand, the medicine segment is promising and is estimated to grow at a healthy CAGR in the European uranium market during the forecast period, owing to the increasing use of radioisotopes derived from uranium and nuclear processes for diagnostic imaging and cancer treatment. Technetium-99m, a widely used medical radioisotope, is often produced in research reactors fueled by uranium. According to the European Association of Nuclear Medicine, the demand for nuclear medicine procedures is rising due to an aging population and the increasing prevalence of chronic diseases such as cancer and cardiovascular conditions. As per data from the Organisation for Economic Co-operation and Development Health at a Glance report, healthcare spending in Europe continues to grow, supporting the expansion of diagnostic services. The development of targeted alpha therapies using actinium-225 and other isotopes derived from uranium decay chains opens new therapeutic avenues. Research reactors in countries like Belgium and the Netherlands are key suppliers of these medical isotopes. The shift towards personalized medicine increases the need for precise diagnostic tools provided by nuclear techniques. Investment in new radiopharmaceuticals and production facilities supports this growth. The high value-added nature of medical applications drives innovation and market expansion. This segment benefits from advancements in nuclear technology and healthcare infrastructure.

COUNTRY LEVEL ANALYSIS

France Uranium Market Analysis

France remained the primary leader of the European uranium market in 2025, with its vast reactor network necessitating the highest volume of fuel. The country’s extensive nuclear power program is the primary driver of uranium consumption. According to the French Ministry of Ecological Transition, nuclear energy provides about 70% of France’s electricity, making it the most nuclear-dependent country in the world. France operates 56 nuclear reactors managed by Électricité de France, which require regular refueling with uranium. As per the World Nuclear Association, France has a fully integrated nuclear fuel cycle, including conversion and enrichment capabilities through Orano. The country’s strategy involves maintaining its existing fleet and developing new generation reactors such as the EPR2. The government’s commitment to nuclear energy as a pillar of carbon neutrality ensures long-term demand. France also engages in reprocessing spent fuel, which contributes to the recycled uranium segment. The presence of major nuclear industry players fosters a robust domestic market. Regulatory support and public acceptance remain relatively high compared to other European nations. The strategic importance of energy independence drives continued investment in nuclear infrastructure. France’s leadership in nuclear technology influences regional market dynamics. The country’s procurement policies significantly impact global uranium trade flows.

Russia Uranium Market Analysis

Russia holds a substantial portion of the market. Russia provides critical fuel supply and enrichment services that many European nations still depend upon. Although geographically transcontinental, Russia’s nuclear industry is deeply integrated with European markets. According to the World Nuclear Association, Rosatom is a global leader in nuclear technology and fuel supply, providing enriched uranium to several European countries. Despite geopolitical tensions, many European utilities still rely on Russian fuel services due to long-term contracts and limited alternative capacity. As per data from the International Atomic Energy Agency, Russia possesses substantial uranium reserves and advanced enrichment capabilities. The country exports nuclear fuel to nations such as Hungary, Bulgaria, and Slovakia. The construction of new nuclear plants in Turkey and potential projects in other regions further strengthen its market position. Russia’s state-owned enterprises dominate the global fuel cycle, offering competitive pricing and technical expertise. The geopolitical landscape introduces complexity, but the technical dependency remains a key factor. The country’s ability to provide full-service nuclear solutions, including build-own-operate models, enhances its influence. Russia’s role in the European market is characterized by strategic supply relationships. The diversification efforts by European countries aim to reduce this dependency over time.

United Kingdom Uranium Market Analysis

The United Kingdom accounts for a prominent share of the European uranium market over the forecast period. The UK is balancing the phase-out of older stations with ambitious plans for new nuclear infrastructure. The country’s nuclear power stations contribute significantly to the national electricity grid. According to the UK Department for Energy Security and Net Zero, nuclear energy provides around 15% of the UK’s electricity. The UK operates several advanced gas-cooled reactors and pressurized water reactors that require uranium fuel. As per the World Nuclear Association, the UK government has announced plans to expand nuclear capacity, including the development of small modular reactors and large-scale projects like Sizewell C. The decommissioning of older plants is balanced by investments in new infrastructure. The UK seeks to enhance energy security and meet climate targets through nuclear power. The country imports uranium from various global sources, ensuring supply diversity. The nuclear industry supports thousands of jobs and contributes to the economy. Regulatory frameworks ensure safety and environmental protection. The UK’s exit from the European Union has led to new bilateral agreements for nuclear cooperation. The focus on innovation and next-generation technologies drives market activity. The UK remains a key consumer and developer of nuclear energy in Europe.

Sweden Uranium Market Analysis

With its recent policy pivot toward expanding nuclear capacity, Sweden maintains a significant share of the European market. The country relies on nuclear power for a significant portion of its electricity production. According to the Swedish Energy Agency, nuclear energy provides about 30% of Sweden’s electricity, contributing to its low-carbon energy mix. Sweden operates three nuclear power plants with multiple reactors that are undergoing life extension programs. As per the World Nuclear Association, the Swedish government has reversed previous phase-out policies and now supports the construction of new nuclear capacity. This policy shift drives renewed interest in uranium procurement and fuel services. The country aims to achieve fossil-free electricity production by 2040, with nuclear playing a crucial role. Swedish utilities collaborate with international suppliers to secure fuel deliveries. The strong regulatory framework ensures high safety standards. Public opinion has shifted towards greater acceptance of nuclear energy due to climate concerns. The investment in new technologies and maintenance of existing plants sustains demand. Sweden’s commitment to clean energy reinforces its position in the market. The country serves as a model for nuclear integration with renewable sources.

Czech Uranium Market Analysis

The Czech Republic is a notable player in Central Europe by prioritizing nuclear energy expansion to secure its domestic power supply and meet climate goals. The country has a long history of uranium mining and currently relies on nuclear power for a large share of its electricity. According to the Czech Ministry of Industry and Trade, nuclear energy accounts for about 35% of the nation’s electricity production. The Dukovany and Temelín nuclear power plants are the primary consumers of uranium fuel. As per the World Nuclear Association, the Czech government has approved plans to build new nuclear units to replace aging capacity and meet growing demand. The state-owned utility ČEZ is leading these expansion efforts. The country aims to increase the share of nuclear power in its energy mix to enhance security and reduce emissions. The Czech Republic has domestic expertise in nuclear engineering and fuel management. It maintains strategic partnerships with international fuel suppliers. The government’s energy policy prioritizes nuclear as a stable and clean source. The expansion projects will drive significant uranium demand in the coming decades. The country’s proactive approach to nuclear development strengthens its market position. The focus on energy independence motivates continued investment in the sector.

COMPETITIVE LANDSCAPE

The Europe uranium market exhibits a concentrated competitive landscape characterized by a few dominant global suppliers and state-owned enterprises. Competition is primarily driven by supply security, reliability, and long-term contractual relationships rather than price alone. Major players leverage their integrated nuclear fuel cycle capabilities to maintain market leadership. The market sees intense rivalry in securing long-term supply agreements with European utilities seeking to diversify away from single sources. Geopolitical factors significantly influence competitive dynamics, with countries striving for energy independence. New entrants face high barriers due to stringent regulatory requirements and capital-intensive infrastructure needs. Strategic collaborations between governments and private companies are common tactics to develop domestic fuel cycle capabilities. The shift towards sustainable and secure supply chains has intensified competition in enrichment and recycling segments. Companies differentiate themselves through technological innovation and adherence to environmental standards. This dynamic environment fosters continuous improvement and investment in resilient supply chains among participants striving to maintain competitive edges in a market influenced by political and economic factors.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global europe uranium market include

- Cameco Corporation

- Kazatomprom

- Orano S.A.

- Rio Tinto Group

- BHP Group Limited

- Uranium One Inc.

- Paladin Energy Ltd.

- CGN Mining Company Limited

- Energy Fuels Inc.

- Denison Mines Corp.

- Yellow Cake plc

- Urenco Group Limited

TOP LEADING PLAYERS IN THE MARKET

- Orano SA is a French multinational company and a global leader in the nuclear fuel cycle with significant operations in the Europe uranium market. The company specializes in mining, conversion enrichment,t and recycling of uranium. Orano recently focused on expanding its enrichment capacity in France to reduce European dependency on external suppliers. The company invested in advanced centrifuge technology to improve efficiency and sustainability. These initiatives strengthen its position as a key supplier for European utilities. Orano collaborates with governments to ensure energy security and supply chain resilience. Its commitment to innovation drives the development of next-generation nuclear fuels. The company continues to optimize its industrial footprint to meet environmental standards. Orano remains a pivotal player in shaping the future of nuclear energy in Europe through strategic investments and technological leadership.

- Rosatom is a Russian state corporation with a dominant presence in the global nuclear industry and significant influence in the Europe uranium market. The company provides comprehensive nuclear solutions, including fuel supply enrichment and plant construction. Rosatom recently focused on maintaining long-term fuel supply contracts with European utilities despite geopolitical tensions. The company leverages its vast uranium reserves and advanced enrichment capabilities to ensure reliable delivery. These actions strengthen its position as a critical supplier for several European nations. Rosatom continues to engage in international collaborations to support nuclear energy development. Its expertise in reactor design and fuel manufacturing ensures high-quality products. The company adapts to changing market dynamics by offering flexible commercial terms. Rosatom remains a major contributor to the European nuclear fuel supply chain through its extensive infrastructure and technical expertise.

- Kazatomprom is the national atomic company of Kazakhstan and the world’s largest producer of natural uranium with substantial exports to the Europe uranium market. The company supplies uranium concentrate to European utilities through long-term agreements. Kazatomprom recently focused on increasing production capacity to meet growing global demand. The company invested in sustainable mining practices and digitalization to enhance operational efficiency. These initiatives strengthen its position as a reliable primary supplier for European markets. Kazatomprom collaborates with international partners to secure logistics and distribution channels. Its commitment to responsible sourcing aligns with European environmental standards. The company continues to explore new markets and expand its customer base. Kazatomprom plays a crucial role in ensuring energy security for Europe by providing stable and cost-effective uranium supplies. Its strategic importance in the global supply chain remains unmatched.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe uranium market predominantly focus on securing long-term supply contracts to ensure stability and mitigate price volatility. Companies invest heavily in diversifying supply chains to reduce dependency on single sources and enhance energy security. Strategic partnerships with governments and utilities facilitate the development of domestic enrichment and fuel fabrication capabilities. Participants also prioritize sustainability initiatives by adopting cleaner mining and processing technologies. Expansion into recycled uranium markets supports circular economy goals and resource efficiency. Manufacturers leverage digital technologies for supply chain transparency and risk management. These strategies collectively strengthen market positions by improving reliability, ensuring regulatory compliance,e and meeting evolving customer needs in a complex geopolitical landscape.

MARKETSEGMENTATION

This research report on the europe uranium market is segmented and sub-segmented into the following categories.

By Type

- Uranium Mining

- Recycled Uranium

By Application

- Nuclear Power Plants

- Medicine

By Country

- France

- Russia

- United Kingdom

- Sweden

- Czech Republic

- Rest of Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com