North America Recreational Boating Market Size, Share, Trends & Growth Forecast Report By Boat Type (Inboard & Sterndrive Boats, Outboard Powerboats, Personal Watercraft (PWC), Sailboats, Yachts (30–120 ft), Inflatable & RIB Boats), Hull Material (Fiberglass / GRP, Aluminum, Wood, Steel, Composites), Length, Power Source, Activity / Application, Distribution Channel, and Country (United States, Canada, Mexico, Rest of North America) – Industry Analysis, 2026 to 2034

North America Recreational Boating Market Size

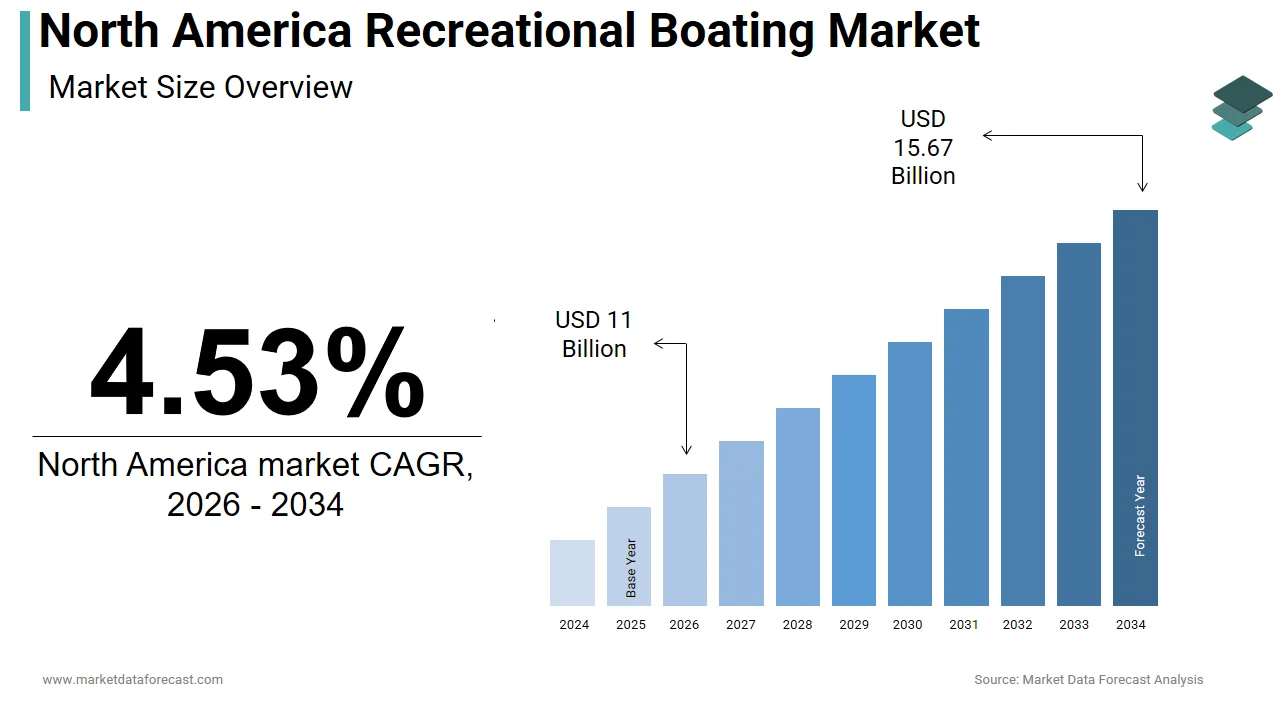

The size of the North America recreational boating market was worth USD 10.52 billion in 2025. The market is anticipated to grow at a CAGR of 4.53% from 2026 to 2034 and be worth USD 15.67 billion by 2034 from USD 11 billion in 2026.

Recreational boating is a broad spectrum of water-based leisure activities involving the use of boats for personal enjoyment, sport fishing, water sports, and cruising. The market includes various types of vessels such as motorboats, sailboats, personal watercraft (PWC), and yachts, catering to a diverse consumer base. The United States is the dominant player in this market, driven by a strong boating culture, extensive coastline, and an expansive network of lakes and rivers. The market has seen increased demand post-pandemic, as more individuals turned to outdoor activities, with 2022 witnessing a record number of new boat sales. This evolving consumer behavior, coupled with technological advancements and infrastructure development, continues to shape the dynamics of the North America recreational boating market.

MARKET DRIVERS

Rising Disposable Incomes and Lifestyle Preferences

The increasing disposable income among middle- and upper-income households, which has significantly enhanced purchasing power for luxury and lifestyle-oriented products such as recreational boats, is one of the primary drivers of the North America recreational boating market. This financial flexibility has allowed more consumers to invest in high-value recreational assets, including boats, yachts, and personal watercraft. Additionally, shifting lifestyle preferences toward experiential consumption have fueled interest in boating as a leisure activity. This growing participation is particularly evident among millennials and Gen X consumers, who prioritize outdoor experiences and adventure-based recreation. The rise in home-based work environments post-pandemic has also contributed to a redefined work-life balance, encouraging individuals to explore weekend getaways and water-based recreation.

Expansion of Waterway Infrastructure and Marina Facilities

The expansion and modernization of waterway infrastructure and marina facilities, which have improved accessibility and convenience for boat owners, is another significant driver of the North America recreational boating market. The U.S. Army Corps of Engineers manages over 12,000 miles of inland waterways, and recent federal investments have focused on enhancing navigability and safety across these routes. Additionally, marina infrastructure has seen notable growth, with a notable number of marinas operating across the U.S., many of which have undergone upgrades to accommodate larger vessels and offer enhanced amenities such as fuel stations, repair services, and docking facilities. This enhanced infrastructure not only supports existing boaters but also encourages new entrants by reducing logistical challenges associated with boat storage, maintenance, and access to waterways.

MARKET RESTRAINTS

High Ownership and Maintenance Costs

The high cost of boat ownership and maintenance, which limits market accessibility to a broader consumer base, is one of the key restraints affecting the North America recreational boating market. Beyond the initial purchase price, owning a recreational boat involves recurring expenses such as insurance, fuel, docking fees, winterization, and regular maintenance. Docking costs also vary significantly depending on location. These cumulative expenses make recreational boating a financially intensive hobby, particularly for first-time buyers or those in lower-income brackets. As a result, many potential consumers are deterred from entering the market despite growing interest in water-based leisure activities. Furthermore, the rising cost of raw materials used in boat manufacturing, such as fiberglass and aluminum, has led to increased retail prices. This upward pricing trend, combined with ongoing operational costs, continues to act as a barrier to entry for a significant portion of the population, thereby constraining the overall growth of the recreational boating market.

Environmental Regulations and Emission Standards

Environmental regulations and emission standards have emerged as a significant restraint on the North America recreational boating market, particularly as governments intensify efforts to combat climate change and reduce water and air pollution. Regulatory bodies such as the U.S. Environmental Protection Agency (EPA) and Environment and Climate Change Canada (ECCC) have implemented stringent emission norms for marine engines, requiring manufacturers to adopt cleaner technologies and alternative fuels. Compliance with these standards has increased production costs for boat manufacturers, leading to higher retail prices for consumers. Moreover, restrictions on the use of certain fuels and engines in protected water bodies have limited the usability of boats in ecologically sensitive areas. For example, the National Park Service has banned the use of personal watercraft in several national parks, including Yellowstone and Everglades, citing environmental concerns. Additionally, the push for electrification in the marine industry, while promising, remains in its early stages due to high battery costs and limited charging infrastructure. These regulatory pressures, while essential for environmental protection, have introduced financial and operational challenges for both manufacturers and consumers, thereby slowing the expansion of the recreational boating market in North America.

MARKET OPPORTUNITIES

Growth of Boat Sharing and Subscription-Based Models

The rise of boat-sharing platforms and subscription-based boating services, which are making recreational boating more accessible and affordable for a broader audience, is a significant opportunity emerging in the North America recreational boating market. Traditional boat ownership comes with high upfront costs and logistical challenges, but these alternative models allow consumers to enjoy boating without the burden of full ownership. Companies such as Boatsetter, GetMyBoat, and Freedom Boat Club have gained traction by offering flexible rental, sharing, and membership options. Additionally, these platforms not only reduce financial barriers but also offer convenience through flexible booking, professional maintenance, and easy access to marinas. This shift in consumer behaviour presents a substantial growth avenue for the recreational boating industry, encouraging traditional manufacturers and marina operators to integrate digital platforms and expand their service offerings to meet evolving market demands.

Technological Advancements in Electric and Hybrid Boats

Technological advancements in electric and hybrid propulsion systems are opening new growth avenues in the North America recreational boating market, particularly as consumers and regulators push for sustainable and low-emission alternatives. Leading manufacturers such as Brunswick Corporation, Yamaha Marine, and Torqeedo are investing heavily in the development of electric outboard motors and hybrid propulsion systems that offer quieter operation, lower maintenance costs, and reduced environmental impact. Companies like Vision Marine Technologies and Pure Watercraft have launched high-performance electric boats capable of matching or exceeding the performance of traditional combustion engines. This shift toward electrification not only aligns with environmental goals but also enhances the boating experience through reduced noise and vibration, positioning electric and hybrid boats as a major growth opportunity in the North American market.

MARKET CHALLENGES

Seasonal Nature of Boating Demand

The highly seasonal nature of boating demand, which creates fluctuations in sales, rentals, and related services, is a significant challenge facing the North America recreational boating market. Unlike year-round industries, recreational boating experiences a sharp peak during the warmer months, typically from April to September, with a notable decline in activity during the fall and winter seasons. This seasonal pattern affects not only consumer purchasing behavior but also the operational efficiency of manufacturers, dealers, and marina operators, who must manage inventory and staffing accordingly. The seasonal constraint also impacts financing and insurance services, as lenders and insurers face uneven demand cycles. Additionally, cold-weather regions such as Canada and the northern U.S. experience extended off-seasons, limiting boating activity to a few months each year. To mitigate this challenge, industry players are increasingly promoting indoor boating simulators, winter maintenance packages, and off-season memberships to sustain customer engagement. However, the fundamental seasonality of the market remains a persistent challenge, affecting revenue predictability and long-term investment planning across the recreational boating value chain.

Regulatory and Permitting Hurdles for New Marina Development

The complex regulatory and permitting environment for new marina development, which hampers infrastructure expansion and limits boating accessibility, is another major challenge in the North America recreational boating market. The process of obtaining permits for marina construction or expansion often involves multiple federal, state, and local agencies, each with its own environmental, zoning, and navigational requirements. In the U.S., the Army Corps of Engineers, Environmental Protection Agency (EPA), and state coastal zone management authorities play a key role in approving marina projects, often leading to lengthy approval timelines. In Canada, similar challenges exist, with provincial environmental assessments and Indigenous consultation requirements adding complexity to marina development. These delays contribute to a shortage of available docking spaces, particularly in high-demand coastal and lakefront regions. Limited marina capacity not only restricts boat ownership growth but also increases slip rental costs, further deterring potential buyers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Boat Type, Hull Material, Length, Power Source, Activity/Application, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | United States, Canada, Mexico, Rest of North America |

| Market Leaders Profiled | Brunswick Corporation, Groupe Beneteau, Azimut Benetti Group, Ferretti Group, Malibu Boats Inc., and others. |

SEGMENTAL ANALYSIS

By Boat Type Insights

The Inboard & Sterndrive boats segment accounted for the largest boat type in the North America recreational boating market by holding 38.4% of total boat sales in 2024. The strong demand for towed water activities such as wakeboarding and skiing, which require the powerful engines and stable hulls typically found in inboard and sterndrive models, is a key driver of their market growth. These boats are particularly popular for their versatility, offering a balance between performance, comfort, and utility, making them ideal for watersports, cruising, and family outings. Additionally, the integration of advanced onboard technologies, such as digital dashboards and wake control systems, has enhanced user experience and attracted tech-savvy buyers. Manufacturers like MasterCraft and Malibu Boats have capitalized on this trend, introducing smart boats that allow for customizable wake settings and remote diagnostics. This technological evolution, combined with the enduring popularity of lake-based recreation in the U.S., continues to solidify the dominance of inboard and sterndrive boats in the regional market.

The Personal Watercraft (PWC) segment is emerging as the fastest-growing in the North America recreational boating market and is projected to expand at CAGR of 6.8% from 2026 to 2034. The relatively lower entry cost compared to full-sized boats, making PWCs more accessible to a broader demographic, including younger consumers and first-time buyers, is one of the primary growth drivers. The affordability, combined with ease of storage and transport, appeals to urban and suburban buyers who may not have access to permanent dock space. The growing appeal of solo and small-group recreation, particularly among millennials who prioritize convenience and agility in their leisure activities, is another key factor. Yamaha, Sea-Doo, and Kawasaki dominate this segment, with continuous innovation in fuel efficiency, emissions control, and rider ergonomics. These factors are propelling PWCs into a position of accelerated growth within the North American recreational boating landscape.

By Length Insights

The Boats measuring less than 20 feet in length segment led the North America recreational boating market by capturing 62.3% of total sales in 2024. The low cost of ownership compared to larger vessels is one of the major factors contributing to their dominance. These smaller boats are particularly favored by first-time buyers, families, and individuals who use them for fishing, watersports, and short recreational trips on lakes and rivers. Additionally, these boats require minimal storage space, with many owners opting for trailerable models that can be stored at home or in low-cost outdoor facilities. Moreover, the increasing availability of compact, high-performance models equipped with advanced electronics and fuel-efficient engines has broadened their appeal. Companies such as Lund, Sylvan, and Yamaha have introduced lightweight, durable models that cater to both novice and experienced boaters.

The segment of boats 26 feet and above is the fastest-growing in the North America recreational boating market, with a projected compound annual growth rate (CAGR) of 7.3% from 2023 to 2030. Increasing disposable incomes of high-net-worth individuals and the growing trend of experiential luxury spending is largely propelling the growth of this segment. Also, the financial strength has enabled affluent consumers to invest in premium recreational assets such as yachts and large cruisers. The expansion of luxury marina infrastructure and the growing availability of concierge-style boating services are other key factors. Additionally, the rise of remote work and flexible lifestyles has led to increased demand for liveaboard yachts and long-distance cruising options. Companies such as Beneteau, Azimut, and Viking Yacht have reported record order backlogs in 2023, reflecting strong market momentum. These factors are collectively driving the rapid expansion of the larger boat segment in North America.

By Power Source Insights

The Internal combustion (IC) engine-powered boats segment continued to dominate the North America recreational boating market in 2025. This overwhelming market share is primarily attributed to the established infrastructure for fueling and maintenance, which makes IC engines more practical for a wide range of boaters. Additionally, IC engines offer higher power output and longer range compared to alternative power sources, making them the preferred choice for activities such as watersports, long-distance cruising, and offshore fishing. The reliability and familiarity of these engines also contribute to their continued dominance, as many boaters are accustomed to their performance characteristics and ease of repair. Furthermore, major manufacturers such as Mercury Marine and Yamaha Marine continue to invest in advanced combustion technologies, including direct fuel injection and hybrid-compatible engine platforms, to enhance efficiency and reduce emissions. These factors strengthen the dominance of internal combustion engines in the North American recreational boating sector.

The Electric and hybrid power boats segment is emerging as the fastest-growing in the North America recreational boating market, with a projected compound annual growth rate (CAGR) of 14.6% from 2026 to 2034. This rapid growth is primarily driven by increasing environmental awareness and regulatory pressure to reduce emissions from marine vessels. The U.S. Environmental Protection Agency (EPA) has mandated stricter emission standards for marine engines, prompting manufacturers to accelerate the development of cleaner propulsion systems. Another key growth driver is the advancement in battery technology, which has improved energy density and reduced charging times. Companies such as Torqeedo, Pure Watercraft, and Vision Marine Technologies have introduced high-performance electric motors that rival traditional combustion engines in terms of speed and endurance. Additionally, marina operators and rental companies are increasingly adopting electric fleets to meet sustainability goals and attract eco-conscious consumers.

By Activity / Application Insights

The Watersports segment remained the prominent application in the North America recreational boating market by contributing a 34.3% of overall boat usage in 2024. The popularity of towed water sports, which require specialized boats equipped with inboard engines and wake-enhancing features, is among the main reasons behind the rise of watersports segment. These boats offer powerful engines, ballast systems, and customizable wake settings, making them ideal for competitive and recreational use. Additionally, the presence of major watersports events such as the World Wakeboard Championships and the USA Water Ski & Wake Sports Foundation competitions has helped sustain interest in the activity. The economic impact of watersports is also significant. Furthermore, the rise of social media and influencer-driven content has amplified the appeal of watersports, particularly among younger demographics. Brands such as MasterCraft, Nautique, and Malibu have capitalized on this trend by introducing smart boats with integrated wake control systems and mobile connectivity. As a result, watersports continue to be a dominant and growing segment within the North American recreational boating market.

The Fishing and eco-tourism activities segment is emerging as the fastest-growing application segment in the North America recreational boating market, with a projected CAGR of 8.1%. A renewed interest in sustainable outdoor activities and the increasing popularity of freshwater and saltwater fishing destinations is fuelling the growth of this segment. Rise of eco-tourism, with more consumers seeking nature-based experiences that minimize environmental impact is another key factor. To support the demand, manufacturers such as Ranger Tugs, Lund, and Boston Whaler have introduced fuel-efficient, low-emission boats designed for quiet operation and minimal disturbance to marine ecosystems. Additionally, the introduction of electric outboard motors by companies like Torqeedo and Minn Kota has further enhanced the appeal of eco-friendly boating.

By Distribution Channel Insights

The dealer and showroom (OEM) channel segment commanded in the North America recreational boating market by capturing a substantial portion of total boat sales in 2025. Consumers continue to prefer purchasing through OEM dealers due to the assurance of factory warranties, certified pre-owned programs, and access to manufacturer-backed financing and service packages. Additionally, dealerships provide a comprehensive buying experience, allowing customers to test drive boats, customize orders, and receive expert advice on maintenance and insurance. A further contributing factor is the extensive dealership network maintained by major manufacturers such as Brunswick Corporation, Yamaha Marine, and Mercury Marine. These dealerships also serve as service hubs, offering parts, repairs, and winterization services that enhance customer retention. Furthermore, the rise of digital retailing tools, including virtual tours and online financing approvals, has made dealership-based sales more convenient.

The online and direct sales platforms segment is the fastest-growing distribution channel in the North America recreational boating market, with a projected CAGR of 12.4% from 2026 to 2034. Increasing digitalization of consumer purchasing behavior, particularly among millennials and Gen Z buyers who prefer streamlined, research-driven transactions, is driving the swift rise of this segment. Additionally, the emergence of online financing tools, virtual walkthroughs, and contactless delivery options has enhanced the convenience of purchasing boats remotely. Companies such as Freedom Boat Club and Boatsetter have further accelerated this trend by integrating subscription-based and peer-to-peer models into their digital platforms. The rise of digital marketplaces has also enabled manufacturers to reach broader audiences without the overhead of traditional dealership networks.

COUNTRY-LEVEL ANALYSIS

United States Recreational Boating Market Insights

The United States secured the dominant position in the North America recreational boating market by accounting for 87.2% of the regional share in 2025. This strong performance is driven by a well-established boating culture, extensive waterway infrastructure, and a robust manufacturing and retail ecosystem. Additionally, the post-pandemic shift toward outdoor recreation has significantly boosted demand. The U.S. government has also supported industry growth through initiatives such as the Marine Retailers Association of the Americas (MRAA) certification programs and the EPA’s Clean Boating Campaign, which promotes responsible boating practices.

Canada Recreational Boating Market Insights

Canada witnessed a steady growth in the North America recreational boating market. This growth is attributed to Canada’s vast freshwater resources, including the Great Lakes, thousands of inland lakes, and extensive river systems that support both freshwater and coastal boating. Additionally, the rise of eco-tourism and outdoor recreation has contributed to increased boating participation, particularly in provinces such as Ontario, Quebec, and British Columbia. The Canadian Safe Boating Campaign, led by Transport Canada, has also played a role in promoting safety and encouraging responsible boating, which has helped boost consumer confidence.

Rest of North America Recreational Boating Market Insights

The Rest of North America, including Mexico and Central American territories, holds a relatively small but growing share of the regional recreational boating market. While the market remains underdeveloped compared to the U.S. and Canada, it is showing signs of gradual expansion, particularly in coastal tourism-driven regions such as Cancun, Cozumel, and the Yucatán Peninsula. The Mexican government has taken steps to improve maritime infrastructure, including investments in new marinas and the expansion of the “Paseo del Mar” coastal development initiative, which aims to boost marine tourism. Additionally, the Caribbean region, particularly in territories such as the Cayman Islands and the Bahamas, has seen increased interest in recreational boating due to the expansion of luxury yachting and charter services. While still a niche market, the Rest of North America presents long-term growth opportunities as infrastructure and tourism development continue to evolve.

COMPETITIVE LANDSCAPE

The competitive landscape of the North America recreational boating market is characterized by a mix of established manufacturers, specialized boat builders, and emerging players focused on innovation and market expansion. While large firms dominate through brand recognition and extensive distribution networks, smaller companies are carving out niches by offering specialized vessels tailored to specific activities such as fishing, watersports, or luxury cruising. The market is witnessing increased collaboration between boat builders and technology providers to integrate smart systems and improve vessel performance. Additionally, the growing emphasis on sustainability is pushing manufacturers to explore alternative materials and cleaner propulsion technologies. As consumer preferences shift toward convenience, digital engagement, and environmental responsibility, companies are adapting their strategies to maintain relevance and drive long-term growth in a dynamic and evolving industry.

KEY MARKET PLAYERS

Noteworthy Companies dominating the North America recreational boating market profiled in the report are

- Brunswick Corporation

- Groupe Beneteau

- Azimut Benetti Group

- Ferretti Group

- Malibu Boats Inc.

TOP LEADING PLAYERS IN THE MARKET

- Brunswick Corporation is a leading force in the North America recreational boating industry, known for its diverse portfolio of boat brands and marine technologies. The company operates through its Boat and Marine Engine segments, offering a wide range of products from fishing boats to luxury yachts. Brunswick's strong dealer network and continuous innovation in boat design and propulsion systems have reinforced its market leadership. The company also invests heavily in sustainability initiatives and digital integration, enhancing the overall boating experience.

- Yamaha Motor Corporation is a major player in the marine industry, particularly known for its reliable outboard engines and personal watercraft. The company's commitment to performance, fuel efficiency, and environmental responsibility has earned it a strong consumer base. Yamaha's strategic partnerships with boat builders and its focus on advanced marine electronics have further solidified its presence in the North American market.

- MasterCraft is a premium brand specializing in performance ski and wake boats, catering to the high-end watersports segment. The company's emphasis on engineering excellence, customer experience, and product customization has established it as a leader in specialized boating. MasterCraft's strong brand loyalty and focus on innovation continue to drive its success in the competitive North American recreational boating landscape.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Product Innovation and Customization Leading players in the North America recreational boating market prioritize continuous product innovation to meet evolving consumer preferences. Companies are introducing advanced hull designs, smart navigation systems, and customizable interiors to enhance user experience and differentiate their offerings in a competitive landscape.

Sustainability and Electrification Initiatives To align with global environmental goals and regulatory requirements, key players are investing in sustainable manufacturing processes and developing electric and hybrid propulsion systems. These initiatives not only reduce environmental impact but also attract eco-conscious consumers seeking greener boating options.

Digital Transformation and Direct-to-Consumer Engagement Manufacturers are leveraging digital tools to streamline sales, improve customer service, and enhance after-sales support. Online configurators, virtual showrooms, and digital financing options are being adopted to meet the expectations of tech-savvy buyers and improve the overall purchasing journey.

RECENT MARKET DEVELOPMENTS

- In January 2023, Brunswick Corporation launched a new line of electric outboard motors under its Mercury Marine brand, marking a strategic move into sustainable propulsion technologies and reinforcing its commitment to reducing the environmental footprint of recreational boating.

- In August 2023, Yamaha Motor Corporation expanded its marine division by forming a partnership with a leading U.S.-based boat builder to integrate Yamaha engines into a broader range of recreational vessels, enhancing performance and reliability for end users.

- In March 2024, MasterCraft Boat Holdings introduced an AI-powered boat configurator on its website, allowing customers to customize their boats with real-time visualizations and feature selections, significantly improving the online purchasing experience.

- In October 2023, Sea-Doo, a division of BRP Inc., announced a new line of personal watercraft equipped with hybrid propulsion systems, targeting environmentally conscious consumers while maintaining high-performance standards.

- In May 2024, Beneteau Group opened a new North American distribution and service center in Florida, aimed at improving logistics efficiency and after-sales support for its growing customer base in the U.S. recreational boating market.

MARKET SEGMENTATION

This North America recreational boating market research report is segmented and sub-segmented into the following categories.

By Boat Type

- Inboard & Sterndrive Boats

- Outboard Powerboats

- Personal Watercraft (PWC)

- Sailboats

- Yachts (30–120 ft)

- Inflatable & RIB Boats

By Hull Material

- Fiberglass / GRP

- Aluminum

- Wood

- Steel

- Composites (Carbon, Kevlar)

By Length

- Less than 20 ft

- 20–50 ft

- Greater than 50 ft

By Power Source

- Internal Combustion Engine

- Electric / Hybrid

- Sail-Propelled

By Activity / Application

- Watersports

- Angling / Fishing

- Cruising & Coastal Tourism

- Dive & Charter Operations

By Distribution Channel

- Dealer / Showroom (OEM)

- Online Direct-to-Consumer

By Country

- United States

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

1. What are the key drivers for growth in the North America Recreational Boating Market?

Growth is fueled by rising disposable incomes, millennial and Gen-Z participation, boat-club and fractional ownership models, tourism expansion, and increasing demand for various recreational boat types.

2. Which boat types are most popular in the North America Recreational Boating Market?

Used leisure boats dominate in revenue share, with strong sales in motorboats, pontoon boats, personal watercraft, sailboats, and emerging electric and hybrid models.

3. How do boating clubs and fractional ownership influence the market?

Boat-club memberships and fractional ownership models lower entry barriers for first-time boaters, increase boat utilization, and boost overall demand for recreational boats.

4. What technological trends are shaping the North America Recreational Boating Market?

Emerging trends include hybrid-electric propulsion, digital direct-to-consumer sales platforms, telematics for connected boats, and advanced onboard entertainment systems.

5. Which North American states are the biggest contributors to recreational boating?

Florida, California, and Texas are major contributors due to their favorable climates, extensive waterways, and large populations of boating enthusiasts.

6. How is sustainability impacting the North America Recreational Boating Market?

Sustainability trends are encouraging the development and adoption of low-emission boats, recyclable materials, and electric propulsion systems to reduce environmental impact.

7. What role do millennials and younger generations play in market growth?

Younger generations increasingly value experiential and outdoor lifestyles, driving interest in boating through new ownership models, social activities, and technology integration.

8. What challenges does the North America Recreational Boating Market face?

Challenges include high raw material costs, supply chain disruptions, weather seasonality, and regulatory compliance related to safety and environmental standards.

9. How significant is the used boat segment in the North America Recreational Boating Market?

The used boat segment accounts for a large share of revenues and growth, offering affordability and accessibility that attract many buyers in the region.

10. What are the common applications for recreational boats in North America?

Applications include cruising, fishing, water sports, tourism charters, and personal leisure use on lakes, rivers, and coastal waters.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com