U.S. Health Insurance Market Size, Share, Trends, and Growth Analysis Report, Segmented by Type, Payor, User, Mode, Distribution Channel, and Country – Industry Forecast From 2026 to 2034

U.S. Health Insurance Market Report Summary

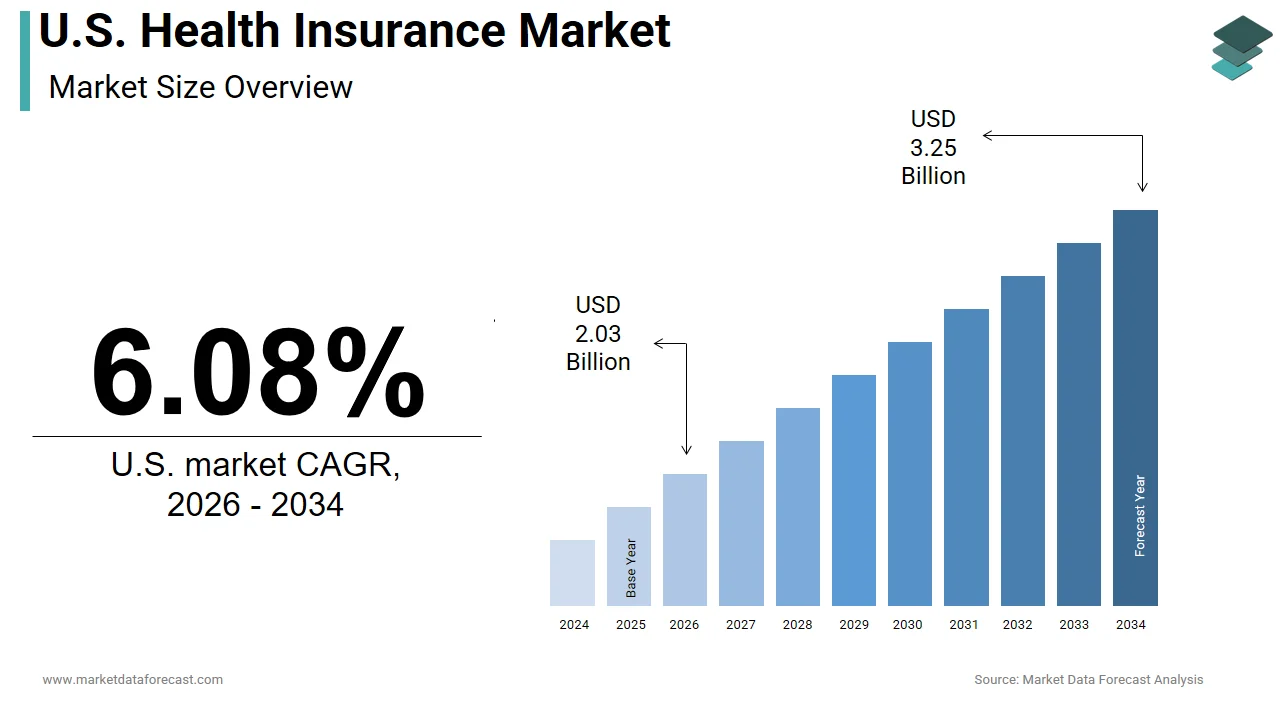

The U.S. health insurance market was valued at USD 1.91 trillion in 2025, is estimated to reach USD 2.03 trillion in 2026, and is projected to reach USD 3.25 trillion by 2034, growing at a CAGR of 6.08% from 2026 to 2034. Market growth is driven by rising healthcare costs, increasing demand for comprehensive coverage, and the expansion of employer-sponsored and government-backed insurance programs. The ongoing shift toward value-based care, digital health integration, and personalized insurance plans is reshaping the industry. Additionally, advancements in telehealth, data analytics, and preventive care are enhancing service delivery and operational efficiency.

Key Market Trends

Rising healthcare expenditure and demand for comprehensive coverage plans.

- Increasing adoption of value-based care models.

- Growth in digital health and telehealth integration.

- Expansion of employer-sponsored insurance programs.

- Focus on personalized and preventive healthcare solutions.

Segmental Insights

- Based on type, the preferred provider organization (PPO) segment dominated the U.S. health insurance market in 2025, driven by flexibility in provider choice.

- Based on payor, the private payors segment held the largest share in 2025, supported by strong participation from private insurers.

- Based on user, the group segment led the market, driven by employer-sponsored insurance coverage.

- Based on distribution channel, the brokers and agents segment dominated in 2025, supported by their role in plan selection and advisory services.

Country-Level Insights

- The United States continues to dominate the global health insurance landscape and is expected to maintain its leadership over the forecast period. Growth is supported by a highly developed healthcare system, widespread insurance coverage, and ongoing transformation toward integrated digital platforms and value-based healthcare models.

Competitive Landscape

The U.S. health insurance market is highly competitive, with major players focusing on digital transformation, mergers and acquisitions, and expansion of service offerings. Companies are investing in data analytics, care management, and customer-centric insurance solutions to strengthen their market position.

Prominent companies operating in the U.S. health insurance market include UnitedHealth Group, AXA, The Cigna Group, CVS Health, Ping An Insurance Group, Centene Corporation, AIA Group Limited, Bupa Global, Elevance Health, and Allianz.

U.S. Health Insurance Market Size

The size of the U.S. health insurance market was worth USD 1.91 trillion in 2025. The market is anticipated to grow at a CAGR of 6.08% from 2026 to 2034 and be worth USD 3.25 trillion by 2034 from USD 2.03 trillion in 2026.

According to data from the Centers for Medicare and Medicaid Services, national health expenditures reached 4.5 trillion U.S. dollars in 2023, which accounts for approximately 17.6% of the gross domestic product, which underscores the massive economic scale of healthcare financing. The market is characterized by its reliance on risk pooling mechanisms, where premiums collected from healthy individuals subsidize the high costs incurred by those with significant medical needs. As per the U.S. Census Bureau, approximately 92% of the U.S. population held some form of health insurance coverage in 2023, reflecting the widespread penetration of these financial products despite ongoing affordability concerns. The regulatory landscape is heavily influenced by federal legislation, including the Affordable Care Act, which mandates essential health benefits and prohibits denial of coverage based on pre-existing conditions. Employers remain the primary source of coverage for non-elderly Americans, with roughly 156 million people enrolled in employer-sponsored plans as per Kaiser Family Foundation statistics. This structure creates a dynamic interplay between labor markets, demographic trends, and policy decisions. The market continues to evolve with the integration of value-based care models and digital health technologies, aiming to improve outcomes while controlling the escalating costs that define the American healthcare experience.

MARKET DRIVERS

Aging Demographics and Increased Chronic Disease Prevalence

The rapidly aging population in the U.S. is primarily fuelling the growth of the U.S. health insurance market. As per the U.S. Census Bureau, individuals aged 65 and older are projected to constitute nearly 21% of the total population by 2030, which is significantly increasing the pool of beneficiaries requiring extensive healthcare interventions. This demographic shift directly correlates with a higher incidence of chronic conditions such as diabetes, cardiovascular disease, and arthritis, which necessitate long-term management and frequent medical attention. The Centers for Disease Control and Prevention indicate that six in ten adults in the U.S. have at least one chronic disease, driving up utilization rates for hospital stays, prescription drugs, and outpatient services. Insurers respond to this trend by expanding their Medicare Advantage offerings and developing tailored plans that address the specific needs of senior citizens. The financial burden of managing multiple chronic conditions often exceeds the capacity of individual savings, making insurance coverage indispensable for this segment. Furthermore, the prevalence of age-related cognitive disorders such as Alzheimer’s disease requires specialized care facilities and support services, further amplifying the demand for robust insurance products. As life expectancy continues to rise, the duration of coverage needed extends, ensuring a stable and growing revenue stream for insurers who can effectively manage the risk associated with an older enrollee base. This demographic inevitability ensures that the health insurance market remains resilient and expansionary.

Regulatory Mandates and Employer-Sponsored Coverage Stability

Regulatory frameworks and the entrenched system of employer-sponsored insurance are further propelling the expansion of the U.S. health insurance market, which is ensuring broad participation and consistent premium inflows. The Affordable Care Act established individual mandates and employer responsibilities that compel millions of Americans to secure coverage, thereby reducing the number of uninsured individuals. As per Internal Revenue Service data, penalties and tax incentives associated with health coverage continue to influence consumer behavior and corporate decision-making regarding benefit packages. Most large employers view health insurance as a critical component of their compensation strategy to attract and retain talent in a competitive labor market. The Kaiser Family Foundation reports that 94% of firms with fifty or more employees offer health benefits to their workers, demonstrating the institutional commitment to providing coverage. This stability is reinforced by tax advantages that allow employers to deduct premium contributions and employees to pay their share with pre-tax dollars. Additionally, state-level regulations often impose additional coverage requirements and consumer protections that expand the scope of insured services. The legal requirement for insurers to cover essential health benefits ensures that policies provide meaningful value, encouraging enrollment among individuals who might otherwise opt out. These regulatory and structural factors create a predictable environment for insurers, allowing them to forecast enrollment trends and manage risk pools effectively. The interplay between federal laws and corporate practices sustains the dominance of the group insurance segment within the broader market.

MARKET RESTRAINTS

Escalating Healthcare Costs and Premium Affordability Issues

The relentless rise in healthcare costs is a major restraint for the U.S. health insurance market. Medical inflation consistently outpaces general economic growth, driven by high prices for pharmaceuticals, advanced medical technologies, and specialist services. As per the Centers for Medicare and Medicaid Services, hospital care expenses alone accounted for 30% of national health spending in 2022, placing immense pressure on insurance premiums. Insurers must pass these increased costs onto consumers in the form of higher premiums, deductibles, and copayments, which can make coverage prohibitively expensive for many households. The Commonwealth Fund notes that nearly half of American adults struggle to afford their healthcare costs, leading some to delay necessary treatments or skip medications. This financial strain results in higher churn rates as individuals drop coverage when they cannot sustain the payments, destabilizing risk pools and forcing further premium increases. Small businesses are particularly vulnerable, often unable to compete with larger corporations in offering attractive benefit packages due to the sheer cost of group plans. The lack of price transparency in the healthcare system exacerbates this issue, making it difficult for insurers to negotiate favorable rates with providers. Consequently, the affordability crisis undermines the fundamental purpose of insurance by leaving significant portions of the population underinsured or uninsured. This economic barrier restricts market growth and invites intense scrutiny from policymakers and consumer advocacy groups demanding cost containment measures.

Administrative Complexity and Operational Inefficiencies

Administrative complexity and operational inefficiencies within the U.S. healthcare system are further hampering the health insurance market in the U.S. The fragmented nature of the system, with multiple payers, varying benefit designs, and disparate billing codes, creates a burdensome administrative landscape for insurers and providers alike. As per a study published in Health Affairs, administrative costs account for approximately 15% to 30% of total healthcare spending in the U.S., which is a figure substantially higher than in other developed nations. Insurers must invest heavily in claims processing, prior authorization systems, and compliance monitoring to navigate this complex environment. These administrative burdens slow down reimbursement processes and create friction between providers and payers, often leading to disputes and delayed care for patients. The need to maintain large administrative workforces increases operational expenses, which are ultimately reflected in higher premiums for consumers. Furthermore, the lack of standardized data exchange protocols hinders interoperability, making it difficult to share patient information efficiently across different platforms. This inefficiency not only increases costs but also contributes to provider burnout and dissatisfaction among insured individuals who face cumbersome paperwork and approval hurdles. The regulatory requirement to adhere to varying state and federal rules adds another layer of complexity, requiring constant adaptation and legal oversight. Until significant standardization and simplification efforts are realized, administrative waste will continue to restrain the efficiency and affordability of the health insurance market.

MARKET OPPORTUNITIES

Integration of Digital Health and Telemedicine Services

The integration of digital health technologies and telemedicine services is a substantial opportunity for the U.S. health insurance market to enhance its value proposition and reduce long-term costs. The rapid adoption of remote monitoring tools, virtual consultations, and mobile health applications allows insurers to engage members more proactively and manage chronic conditions more effectively. According to the American Medical Association, the percentage of physicians using tele-visits increased from 14% in 2016 to 80% in 2022, indicating a permanent shift in consumer preferences for convenient care access. Insurers are leveraging these technologies to offer personalized wellness programs and real-time health coaching, which can prevent costly emergency room visits and hospitalizations. By incorporating digital therapeutics into their coverage plans, insurers can address mental health and behavioral issues more efficiently, expanding their service offerings beyond traditional medical care. Partnerships with tech companies enable the development of innovative platforms that track health metrics and provide actionable insights to users. This data-driven approach facilitates early intervention and improves health outcomes, which translates into lower claim costs over time. Furthermore, digital solutions appeal to younger demographics who prioritize convenience and technological integration in their healthcare experiences. Insurers who successfully embed these tools into their ecosystems can differentiate themselves in a crowded market and improve member retention. The potential for artificial intelligence to analyze health data and predict risk factors further enhances the strategic value of digital health investments, positioning insurers as holistic health partners rather than mere payers.

Expansion of Value-Based Care Models

The expansion of value-based care models offers a significant opportunity for the U.S. health insurance market to align financial incentives with quality health outcomes. Unlike traditional fee-for-service arrangements that reward volume, value-based care focuses on paying providers for the quality and effectiveness of the care they deliver. As per the Centers for Medicare and Medicaid Services, approximately 25% of Medicare spending is currently tied to value-based payment models, demonstrating the scalability of this approach. Commercial insurers are increasingly adopting similar models, negotiating contracts with provider networks that share financial risk and reward improvements in patient health. This shift encourages preventive care, care coordination, and the management of chronic diseases, which can significantly reduce unnecessary medical procedures and hospital readmissions. Insurers benefit from lower overall claim costs and improved member satisfaction when health outcomes are prioritized. The use of data analytics enables insurers to identify high-risk populations and target interventions more precisely, enhancing the efficiency of care delivery. Additionally, value-based contracts foster stronger collaborations between payers and providers, reducing adversarial relationships and promoting shared goals. As healthcare stakeholders recognize the limitations of volume-driven reimbursement, the transition to value-based models accelerates. Insurers who lead this transformation can achieve sustainable cost savings and establish themselves as leaders in quality-driven healthcare financing, capturing market share from competitors still reliant on outdated payment structures.

MARKET CHALLENGES

Cybersecurity Threats and Data Privacy Vulnerabilities

Cybersecurity threats and data privacy vulnerabilities are a significant challenge to the U.S. health insurance market, as insurers hold vast amounts of sensitive personal and medical information. The digitization of health records and the increasing reliance on interconnected systems have made insurance companies prime targets for cybercriminals seeking to exploit valuable data for financial gain or identity theft. As per the Department of Health and Human Services, the healthcare sector experienced a 256% increase in large breaches reported to the Office for Civil Rights over the last five years, affecting millions of individuals and costing the industry billions of dollars in remediation and legal fees. These breaches erode consumer trust and can lead to significant reputational damage for insurers, resulting in member attrition and regulatory penalties. The complexity of IT infrastructure, often involving legacy systems integrated with modern cloud platforms, creates numerous entry points for attackers. Insurers must continuously invest in advanced security protocols, encryption technologies, and employee training to mitigate these risks. However, the evolving nature of cyber threats requires constant vigilance and adaptation, straining operational budgets. Furthermore, strict regulatory requirements such as the Health Insurance Portability and Accountability Act impose heavy compliance burdens, with severe consequences for failures. The fear of data breaches also hinders the seamless sharing of information necessary for coordinated care, potentially impacting health outcomes. Balancing the need for data accessibility with robust security measures remains a persistent challenge. As cyber-attacks become more sophisticated, the health insurance industry must prioritize cybersecurity as a core business function to protect its assets and maintain the confidence of its members.

Provider Network Adequacy and Access Disparities

Provider network adequacy and access disparities are another promising challenge to the U.S. health insurance market, affecting the ability of insured individuals to receive timely and appropriate care. Insurers face difficulties in maintaining broad and diverse networks of physicians, specialists, and hospitals, particularly in rural and underserved areas where provider shortages are acute. As per the Association of American Medical Colleges, the U.S. is projected to face a shortage of between 37,800 and 124,000 physicians by 2034, exacerbating access issues for millions of patients. Narrow networks, designed to control costs by limiting the number of participating providers, often restrict patient choice and lead to longer wait times for appointments. This limitation can result in dissatisfaction among members and regulatory scrutiny regarding compliance with network adequacy standards. Rural hospitals are closing at an alarming rate, further reducing access to emergency and specialized services for insured populations in these regions. Insurers must navigate complex negotiations with provider groups to ensure fair reimbursement rates while keeping premiums affordable. The tension between cost containment and network breadth creates a delicate balance that is difficult to maintain. Additionally, disparities in access based on socioeconomic status and geography persist, undermining the equity goals of health insurance coverage. Addressing these structural issues requires collaborative efforts between insurers, providers, and policymakers to incentivize practice in underserved areas and support the financial viability of safety net institutions. Until these access barriers are resolved, the effectiveness of health insurance in delivering comprehensive care remains compromised.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Payor, User, Mode, Distribution Channel, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled |

|

SEGMENTAL ANALYSIS

By Type Insights

The preferred provider organization segment dominated the market by holding the leading share of the U.S. market in 2025. The dominance of the preferred provider organization segment in the U.S. market is primarily attributed to its unparalleled flexibility in provider selection and extensive network breadth. Unlike more restrictive plans, PPOs allow members to visit any healthcare provider without a referral, whether in or out of network, although staying within the network results in lower out-of-pocket costs. This autonomy is highly valued by consumers who prioritize choice and convenience in their healthcare journey. As per data from the Kaiser Family Foundation, approximately 48% of covered workers in the U.S. are enrolled in PPO plans, making it the most common type of employer-sponsored coverage. The ability to access specialists directly without primary care gatekeeping appeals to individuals with complex medical needs or those who travel frequently. Employers also favor PPOs as a competitive benefit offering that attracts top talent seeking comprehensive coverage options. The broad network of participating providers ensures that members can find care easily, reducing barriers to access. Furthermore, the portability of PPO coverage across state lines supports a mobile workforce, enhancing its appeal in a dynamic labor market. This structural advantage sustains the dominance of PPOs despite higher premium costs compared to other plan types. The segment’s resilience is further supported by the established relationships between insurers and large hospital systems, which facilitate negotiated rates and seamless service delivery. Consequently, the PPO model remains the benchmark for comprehensive health insurance in the U.S.

On the other hand, the health maintenance organization segment is experiencing the fastest growth in the U.S. health insurance market and is anticipated to record a healthy CAGR in the U.S. market during the forecast period, owing to the intense cost containment pressures and the need for affordable coverage solutions. HMOs require members to select a primary care physician who coordinates all care and provides referrals for specialists, which significantly reduces unnecessary medical procedures and controls spending. As per the Centers for Medicare and Medicaid Services, the shift towards managed care models has helped slow the rate of healthcare expenditure growth, with HMOs playing a central role in this trend. The lower premium structures of HMOs make them increasingly attractive to small businesses and individual consumers facing rising living costs. The Affordable Care Act marketplace has seen a surge in HMO enrollment as subsidy-eligible individuals seek to maximize their benefits while minimizing monthly payments. As per enrollment data from the Department of Health and Human Services, roughly 56% of HealthCare.gov enrollees selected an HMO plan for the 2024 plan year. The capitated payment model used by HMOs aligns financial incentives with preventive care, encouraging early intervention and reducing the incidence of costly chronic conditions. This efficiency appeals to employers looking to stabilize their benefit costs in an unpredictable economic environment. Furthermore, the integration of digital health tools within HMO frameworks enhances care coordination and member engagement, adding value beyond cost savings. As affordability becomes a paramount concern for Americans, the HMO model offers a sustainable path to comprehensive coverage, driving its rapid expansion in the market.

By Payor Insights

The private payors segment held the leading position in the U.S. health insurance market with the largest share of the U.S. market in 2025. The growth of the private payors segment in the U.S. market is attributed to the entrenched system of employer-sponsored insurance, which covers the majority of the non-elderly population. Large and small businesses alike provide health benefits as a standard part of employee compensation, creating a massive and stable revenue base for private insurance companies. As per the U.S. Census Bureau, approximately 64% of the U.S. population was covered by private health insurance in 2023, with the vast majority obtaining it through their workplace. This segment benefits from the tax advantages associated with employer contributions, which exclude these benefits from taxable income for both employers and employees. The collective bargaining power of large employer groups allows private insurers to negotiate favorable rates and spread risk across large pools of healthy and young workers. Private payors also offer a wide range of plan designs and supplemental products that cater to diverse consumer preferences, from high-deductible plans to comprehensive coverage. The innovation capacity of private insurers enables them to rapidly adopt new technologies and care models, enhancing their competitive edge. Furthermore, the administrative infrastructure supporting private insurance is highly developed, facilitating efficient claims processing and customer service. The reliance of the American healthcare system on private funding ensures that this segment remains the cornerstone of the market. Despite challenges from public programs, the deep integration of private insurance with the employment sector sustains its leadership position.

On the other hand, the public payors segment is anticipated to register the fastest CAGR in the U.S. market during the forecast period due to the Medicaid expansion and significant enrollment surges following policy changes and economic shifts. The Affordable Care Act allowed states to expand Medicaid eligibility to low-income adults, resulting in millions of newly insured individuals. As per the Centers for Medicare and Medicaid Services, total Medicaid and CHIP enrollment was over 87 million individuals in September 2023, reflecting the program’s critical role in providing safety net coverage. The continuous enrollment provisions during the public health emergency further boosted numbers, although subsequent unwinding processes have led to some fluctuations. Nevertheless, the structural expansion of Medicaid in numerous states has created a lasting increase in the public payor base. Economic downturns and rising healthcare costs have also driven more individuals to seek public assistance as private coverage becomes unaffordable. State governments are increasingly recognizing the cost-effectiveness of Medicaid in managing population health, leading to broader eligibility criteria and enhanced benefits. The federal matching funds provide a strong financial incentive for states to maintain and expand their programs. As social determinants of health gain prominence, Medicaid is evolving to cover non-medical services such as housing and nutrition support, increasing its appeal and utility. This broadening scope and expanding eligibility ensure that public payors continue to grow at a faster rate than private counterparts, capturing a larger share of the vulnerable population.

By User Insights

The group user segment led the market by holding the major share of the U.S. health insurance market in 2025. The growth of the group users segment in the U.S. market is driven by employer mandates and the collective bargaining power of large organizations. The majority of Americans receive health insurance through their employers, a system that leverages the size of employee pools to negotiate lower premiums and better benefits. As per the Agency for Healthcare Research and Quality, employer-sponsored insurance covered 48.7% of the total population in 2022, demonstrating the scale of this segment. Large corporations use their purchasing power to secure favorable contracts with insurers, passing on some of the savings to employees in the form of subsidized premiums. The legal framework, including the Employer Shared Responsibility Payment provisions, encourages large firms to offer coverage to avoid penalties. This structural support ensures a stable and large base of group-insured individuals. Group plans also benefit from adverse selection protection, as the risk pool includes both healthy and sick individuals, stabilizing costs. The administrative efficiency of enrolling employees through payroll deductions simplifies the process for both insurers and participants. Furthermore, group insurance is often seen as a key retention tool, prompting employers to maintain and even enhance their offerings. The prevalence of union-negotiated health benefits in certain industries further solidifies the dominance of the group segment. As long as employment remains the primary source of coverage, the group user segment will continue to lead the market in terms of enrollment volume and premium revenue.

However, the individual user segment is the fastest-growing component of the U.S. health insurance market and is estimated to record a promising CAGR in the U.S. market during the forecast period, owing to the expansion of the gig economy and the rise of freelance work. As more Americans move away from traditional employment, they lose access to employer-sponsored coverage and must seek insurance on their own. According to a study by Upwork, 38% of the U.S. workforce, or 64 million Americans, performed freelance work in 2023, with many relying on individual market plans for coverage. This shift creates a new and expanding customer base for insurers offering individual policies. The flexibility of individual plans allows freelancers to choose coverage that fits their specific needs and budget, unlike one-size-fits-all group plans. Online marketplaces and direct-to-consumer sales channels have made it easier for individuals to compare and purchase policies, reducing friction in the enrollment process. The portability of individual coverage is also a key advantage for workers who change jobs frequently or have irregular income streams. Insurers are responding by developing flexible products with varying levels of coverage and cost-sharing options. The growth of the creator economy and remote work further accelerates this trend, as geographical boundaries become less relevant to employment. As the nature of work continues to evolve, the demand for individual health insurance will continue to rise, making it the fastest-growing segment in the market.

By Distribution Channel Insights

The brokers and agents segment occupied the leading distribution channel in the U.S. health insurance market in 2025 due to the rising need for expert guidance and personalized service in navigating complex insurance products. Health insurance plans involve intricate details regarding networks, deductibles, and coverage limits, which can be overwhelming for consumers and small business owners. Brokers provide valuable assistance in comparing options and selecting plans that best fit specific needs and budgets. As per industry surveys, roughly 75% of small group insurance buyers use a broker to help navigate the market, citing the time savings and expertise provided as key reasons. Agents also play a crucial role in the individual market, helping consumers understand subsidy eligibility and enrollment procedures. The trust relationship between clients and brokers fosters loyalty and repeat business, ensuring a steady flow of commissions for insurers. Brokers often serve as ongoing advocates for clients, assisting with claims issues and plan changes throughout the year. This level of service is difficult to replicate through automated channels, maintaining the relevance of human intermediaries. The regulatory requirement for licensed agents in many transactions further reinforces their importance. Insurers rely on broker networks to reach dispersed markets and diverse customer segments efficiently. The ability of brokers to tailor recommendations and provide peace of mind makes them an indispensable part of the distribution ecosystem. Consequently, the broker and agent channel remains the dominant force in selling health insurance policies across the U.S.

On the other end, the direct sales channel is the fastest-growing distribution segment in the U.S. health insurance market, propelled by digital transformation and the proliferation of online enrollment platforms. Consumers increasingly prefer the convenience and transparency of purchasing insurance directly from carriers via websites and mobile apps, bypassing intermediaries. According to industry data, the share of individuals purchasing health insurance directly through government exchanges or carrier websites has increased significantly over the last decade, reflecting the shift towards self-service models. Direct channels allow insurers to control the customer experience and brand messaging entirely, fostering stronger relationships with policyholders. The use of interactive tools and calculators helps users estimate costs and coverage needs instantly, simplifying the decision-making process. Insurers are investing heavily in user-friendly interfaces and seamless integration with payment systems to reduce friction. The ability to update personal information and manage policies online enhances customer satisfaction and retention. Direct sales also enable insurers to collect valuable data on consumer behavior, which can be used to refine products and marketing strategies. The reduction in commission payments to brokers improves profit margins for insurers, allowing them to offer more competitive pricing. As digital literacy increases among all age groups, the preference for direct interactions continues to rise. This technological empowerment ensures that the direct sales channel will continue to expand rapidly, capturing market share from traditional intermediaries.

COUNTRY LEVEL ANALYSIS

The U.S. is likely to maintain its position as the global leader in health insurance for the next few years as the market transitions further towards integrated digital platforms and value-based outcomes. The U.S. holds the largest share of the global health insurance market, accounting for roughly 45% of worldwide health insurance premiums, reflecting its unique mixed public-private system. As per global health expenditure data, the U.S. spends more on healthcare per capita than any other nation, with insurance mechanisms facilitating the majority of these transactions. The market status is characterized by high complexity, significant regulatory oversight, and a diverse array of payors and providers. The absence of a single-payer system creates a fragmented landscape where private insurers compete alongside government programs like Medicare and Medicaid. This structure drives innovation in product design and care management but also contributes to high administrative costs and access disparities. The U.S. market is a leader in adopting value-based care models and digital health technologies, setting trends for other countries. The robust pharmaceutical and medical device industries further influence insurance coverage decisions and pricing dynamics. Regulatory changes at both the federal and state levels continuously reshape the market, requiring constant adaptation from stakeholders. The high level of healthcare utilization and advanced medical capabilities ensure strong demand for comprehensive insurance products. Despite challenges related to affordability and equity, the U.S. remains the central hub for health insurance innovation and investment globally. Its market dynamics influence global insurance practices and policy debates, maintaining its preeminent position in the international healthcare finance landscape.

COMPETITIVE LANDSCAPE

The competition in the U.S. health insurance market is intense and characterized by consolidation among major players seeking economies of scale and broader service offerings. Large national insurers compete with regional plans and specialized entities focusing on specific demographics such as seniors or low income individuals. Differentiation increasingly relies on technology integration and value-based care models rather than price alone. Companies strive to offer seamless digital experiences and personalized health management tools to attract and retain members. Regulatory pressures regarding pricing transparency and coverage requirements shape competitive dynamics significantly. Insurers must navigate complex compliance landscapes while innovating to meet evolving consumer expectations. The rise of retail health entrants and tech giants adds further pressure on traditional insurers to adapt quickly. Mergers and acquisitions remain common strategies to expand geographic reach and service capabilities. Competitive advantage is often determined by the ability to manage medical loss ratios effectively and deliver superior customer service. As healthcare costs continue to rise, insurers face the dual challenge of maintaining profitability while ensuring affordability for members. This dynamic environment requires continuous strategic adaptation and investment in innovation to sustain market relevance and growth potential in the U.S.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. health insurance market include

- UnitedHealth Group

- AXA

- The Cigna Group

- CVS Health

- Ping An Insurance Group

- Centene Corporation

- AIA Group Limited

- Bupa Global

- Elevance Health

- Allianz

TOP PLAYERS IN THE MARKET

- UnitedHealth Group Incorporated stands as a diversified healthcare leader with significant influence on global health services through its Optum division. The company integrates insurance coverage with direct care delivery and pharmacy benefit management to create a cohesive ecosystem. Recent actions include strategic acquisitions of home health and behavioral health providers to expand value based care capabilities. UnitedHealth actively invests in artificial intelligence technologies to streamline claims processing and enhance predictive analytics for patient outcomes. These initiatives strengthen its market position by improving operational efficiency and member satisfaction. The company also focuses on expanding its Medicare Advantage offerings to capture the growing senior demographic. By leveraging data-driven insights, UnitedHealth optimizes risk management and cost containment strategies. Its global footprint allows it to implement best practices across international markets while maintaining dominance in the U.S.. This comprehensive approach ensures sustained growth and resilience against regulatory changes.

- Elevance Health Incorporated operates as a major health benefits company serving millions of members through its diverse portfolio of insurance brands. The organization emphasizes whole-person health by integrating medical, pharmacy, dental, and vision services into unified plans. Recent strategies involve expanding digital health platforms and telehealth services to improve accessibility and convenience for members. Elevance Health has invested heavily in social determinants of health programs to address non-medical factors affecting well-being. The company strengthens its position by partnering with local community organizations and healthcare providers to deliver coordinated care. It also focuses on enhancing employer-sponsored solutions with customized wellness tools and data analytics. These efforts help retain corporate clients and attract individual consumers seeking holistic health support. Elevance Health continues to innovate in payment models that reward quality and efficiency. Its commitment to health equity and technological advancement solidifies its role as a key player in the evolving U.S. health insurance landscape.

- Centene Corporation specializes in providing managed care services to government-sponsored healthcare programs, including Medicaid and Medicare. The company plays a critical role in serving underserved populations by offering tailored health solutions that address specific community needs. Recent actions include expanding its footprint in the individual marketplace through the Affordable Care Act exchanges and acquiring regional health plans to broaden its network. Centene invests in innovative care models such as integrated behavioral health and long-term services and supports. The company leverages technology to improve care coordination and reduce hospital readmissions among high-risk members. It also focuses on workforce development and provider partnerships to ensure adequate access to care. These strategies enhance its reputation as a reliable partner for state governments and federal agencies. Centene’s ability to adapt to regulatory changes and manage complex populations strengthens its competitive position. Its focus on affordability and accessibility drives growth in the public sector insurance segment.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the U.S. health insurance market primarily focus on vertical integration to control costs and improve care quality. Companies acquire healthcare providers and pharmacy benefit managers to create closed-loop systems that enhance efficiency. Another major strategy involves expanding value-based care arrangements where payments are linked to patient outcomes rather than service volume. Insurers invest heavily in digital health technologies such as telemedicine and remote monitoring to engage members proactively. Diversification into adjacent sectors like home health and behavioral care allows firms to address broader health needs. Strategic partnerships with tech companies facilitate data analytics and personalized health interventions. These approaches help participants manage risk effectively while delivering comprehensive and affordable coverage solutions in a competitive environment.

MARKET SEGMENTATION

This research report on the U.S. health insurance market has been segmented and sub-segmented into the following categories.

By Type

- Health Maintenance Organization (HMO)

- Preferred Provider Organization (PPO)

- Exclusive Provider Organization (EPO)

- Others

By Payor

- Private

- Public

By User

- Individual

- Group

By Mode

- Offline

- Online

By Distribution Channel

- Direct Sales

- Agents

- Brokers

- Banks

- Others

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

What is the U.S. health insurance market?

The U.S. health insurance market provides coverage for medical care, prescriptions, and hospital services through private, employer, and public plan options in the country.

How does the U.S. health insurance market function?

The U.S. health insurance market functions by pooling risk, collecting premiums, paying claims, and negotiating provider access across private and public coverage channels.

What drives growth in the U.S. health insurance market?

The U.S. health insurance market grows due to aging populations, rising medical costs, Medicare Advantage demand, and ongoing need for broad coverage access.

Which segments lead the U.S. health insurance market?

The U.S. health insurance market is led by employer-sponsored plans, Medicare Advantage, individual plans, and other private coverage products.

What types define the U.S. health insurance market?

The U.S. health insurance market includes private insurance, public insurance, individual plans, family plans, group plans, and managed care offerings.

What is employer-sponsored coverage in the U.S. health insurance market?

Employer-sponsored coverage is a major part of the U.S. health insurance market, where employers help provide medical benefits to workers and their families.

How does Medicare Advantage fit the U.S. health insurance market?

Medicare Advantage is a fast-growing part of the U.S. health insurance market, especially among older adults seeking bundled medical coverage options.

What role do ACA plans play in the U.S. health insurance market?

ACA plans are important in the U.S. health insurance market because they expand access, require essential benefits, and protect consumers from discrimination.

How does market concentration affect the U.S. health insurance market?

The U.S. health insurance market is highly concentrated, with major carriers holding strong positions and limiting competition in many regional markets.

What challenges face the U.S. health insurance market?

The U.S. health insurance market faces rising premiums, cost inflation, regulatory pressure, limited competition, and complexity in plan selection.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com