U.S Warehouse Market Size, Share, Trends & Growth Forecast Report Segmented By Warehouse Type (General Warehousing, Specialized Warehousing), End Use And Country (California, Washington, Oregon, New York & Rest of The United States) – Industry Analysis And Forecast, 2026 To 2034

U.S. Warehouse Market Report Summary

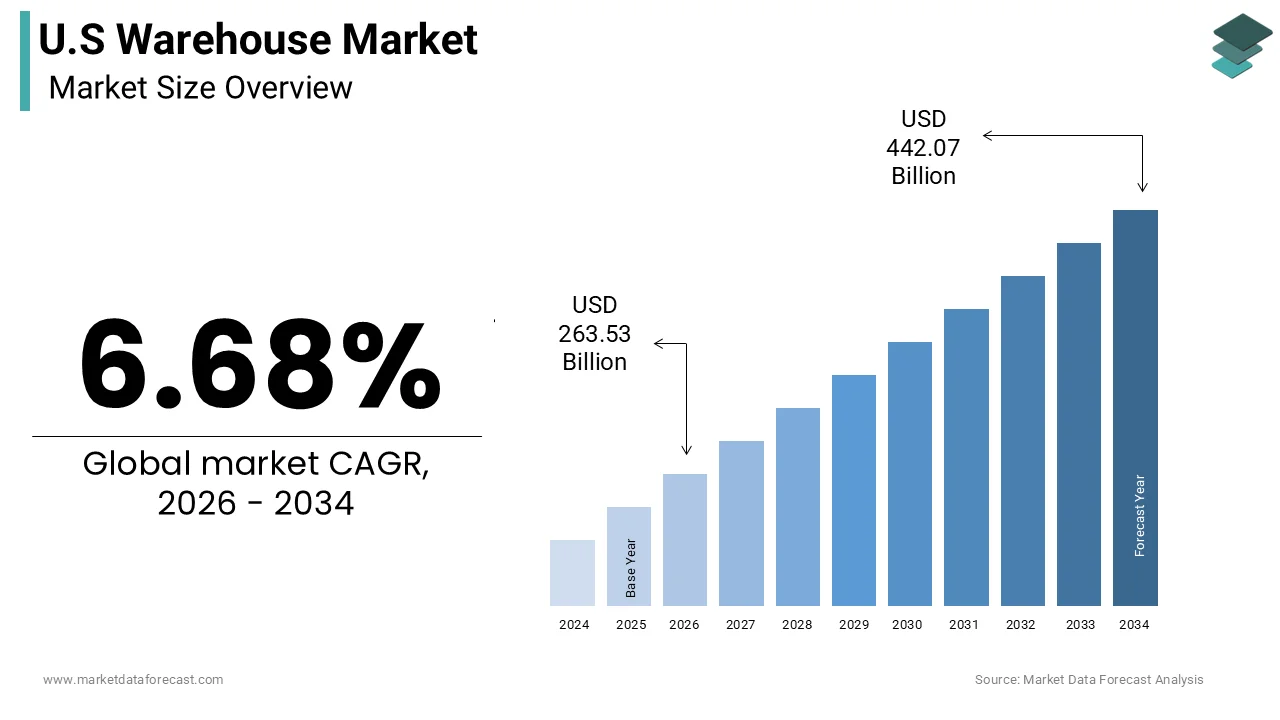

The United States warehouse market was valued at USD 247.03 billion in 2025 and is projected to reach USD 442.07 billion by 2034, growing from USD 263.53 billion in 2026 at a CAGR of 6.68% during the forecast period. Market growth is driven by the rapid expansion of e-commerce, increasing demand for efficient supply chain management, and rising investments in logistics infrastructure. The shift toward omnichannel retailing, same-day delivery expectations, and automation in warehousing is further accelerating the growth of the U.S. warehouse market.

Key Market Trends

- Rapid growth of e-commerce and omnichannel retail

- Increasing adoption of warehouse automation and robotics

- Rising demand for cold storage and specialized warehouses

- Expansion of last-mile delivery infrastructure

- Integration of AI, IoT, and data analytics in warehouse operations

Segmental Insights

- Based on warehouse type, the general warehousing segment dominated the U.S. warehouse market in 2025 due to its flexibility in handling diverse goods such as electronics, automotive parts, and consumer products.

- Based on end-use sector, the retail and e-commerce segment held the largest share in 2025, driven by the surge in online shopping and fulfillment center demand.d

Regional Insights

- United States accounted for 40.6% of the global warehouse market share in 2025, making it the most prominent regional market due to its advanced logistics ecosystem and strong consumer demand.

Competitive Landscape

- The U.S. warehouse market is highly competitive, with companies focusing on automation, network expansion, and integrated logistics solutions. Market players are investing in smart warehouses, robotics, and digital supply chain platforms to enhance efficiency and scalability.

- Prominent players in the U.S. warehouse market include Amazon.com Inc, DHL Supply Chain, Ryder Supply Chain Solutions, GXO Logistics, NFI Industries, Lineage Logistics, GEODIS, Americold Realty Trust, Kenco Group, FedEx Logistics, Saddle Creek Logistics Services, Penske Logistics, CJ Logistics America, XPO Logistics, and Prologis Inc.

U.S Warehouse Market Size

The U.S warehouse market size was calculated to be USD 247.03 billion in 2025 and is anticipated to be worth USD 442.07 billion by 2034, from USD 263.53 billion in 2026, growing at a CAGR of 6.68% during the forecast period.

A warehouse is a large commercial building specifically designed for storing goods and raw materials. This market has evolved from static storage units into dynamic fulfillment centers that facilitate rapid order processing and last-mile delivery. High ceilings, automated sorting systems, and strategic locations near major transportation hubs characterize the modern warehouse. According to the US Census Bureau's 2022 Annual Wholesale Trade Survey (released January 2024), the total value of merchant wholesalers' durable and nondurable goods sales reached approximately $11.4 trillion, underscoring the massive volume of goods flowing through these facilities. The shift toward omnichannel retail has fundamentally altered warehouse design requirements, necessitating larger footprints to accommodate inventory diversity and faster turnover rates. As per the Bureau of Labor Statistics (BLS) March 2026 "Employment Situation" report, employment in transportation and warehousing has declined, dropping by 139,000 jobs since reaching a peak in February 2025, reflecting a cooling labor market in logistics following a period of rapid pandemic-era expansion. The physical infrastructure supports a complex network of suppliers, manufacturers, and retailers, ensuring product availability across the continent. Recent trends indicate a preference for modern Class A facilities equipped with advanced technology and sustainability features. The market is deeply influenced by consumer expectations for speed and reliability, which drive continuous investment in facility upgrades and expansion. This ecosystem plays a pivotal role in economic stability by enabling efficient goods movement and reducing supply chain bottlenecks. The definition of the market now includes specialized cold storage and hazardous material handling facilities, reflecting the diversification of stored commodities.

MARKET DRIVERS

Explosive Growth of E-Commerce and Omnichannel Retail

The explosive growth of e-commerce and the adoption of omnichannel retail strategies serve as primary drivers for the United States warehouse market. Consumers increasingly prefer online shopping for its convenience and variety, leading to a surge in parcel volumes that require extensive storage and sorting capacity. According to the US Department of Commerce, e-commerce sales accounted for 15.6 percent of total retail sales in the fourth quarter of 2023, demonstrating the sustained dominance of digital purchasing channels. This shift necessitates a decentralized network of fulfillment centers located closer to urban populations to enable same-day or next-day delivery. As per McKinsey & Company, supply chain complexity is rising, with inventory holding costs estimated at 20 to 30 percent of inventory value, driving retailers to optimize, rather than simply expand, their logistics networks. The need for reverse logistics infrastructure has further amplified demand for warehouse space, as returns processing requires dedicated areas and labor. Traditional brick-and-mortar stores are also integrating online orders into their operations, using local warehouses as pickup points. This hybrid model increases the utilization rate of existing facilities and drives the construction of new ones in suburban areas. The pressure to reduce delivery times compels companies to maintain higher safety stock levels, which directly translates to increased square footage requirements. Thus, the relentless expansion of digital retail continues to fuel robust demand for modern warehouse facilities across the nation.

Supply Chain Resilience and Nearshoring Initiatives

Supply chain resilience and nearshoring initiatives have emerged as significant accelerators for the United States warehouse market. Companies are pursuing these strategies to mitigate risks associated with global disruptions. The pandemic exposed vulnerabilities in long-distance supply chains, prompting businesses to shorten their logistical networks and bring production closer to end markets. According to the Federal Reserve Bank of Dallas, while nearshoring is a growing trend, it has 'yet to yield big investment,' and manufacturing output in Mexico has remained volatile rather than showing a sustained surge. This regionalization of production requires substantial warehouse capacity to store raw materials and finished goods before distribution. As per various sources, firms are adopting a China Plus One strategy to diversify sourcing locations, while separately shifting toward 'Just-in-Case' inventory management to build resilience against disruptions. The desire to reduce lead times and avoid port congestion has accelerated the development of inland distribution hubs connected by rail and truck. Companies are investing in larger warehouses to hold more inventory locally, moving away from just-in-time models that proved fragile during crises. This strategic shift ensures business continuity and enhances responsiveness to market fluctuations. Furthermore, government incentives for domestic manufacturing under legislation like the CHIPS Act are stimulating industrial construction and subsequent warehousing needs. The focus on security and reliability thus sustains high demand for warehouse space as organizations rebuild their logistical frameworks to withstand future shocks.

MARKET RESTRAINTS

Land Scarcity and Zoning Regulatory Hurdles

Land scarcity and stringent zoning regulations pose significant restraints on the United States warehouse market. This limits the availability of suitable sites for new construction. Prime locations near major population centers and transportation hubs are increasingly scarce, driving up land costs and complicating acquisition processes. According to the National Association of Realtors, vacancy rates for industrial properties have risen from their historic lows, as new supply outpaces absorption in key markets. Local governments often impose strict zoning laws that restrict industrial development in favor of residential or commercial projects, slowing down the approval process for new warehouses. As per the Urban Land Institute, community opposition to large distribution centers due to concerns about traffic congestion and noise pollution further delays project timelines. These regulatory hurdles increase development costs and extend the time required to bring new supply online. The lack of contiguous land blocks suitable for mega facilities forces developers to consider less optimal locations, which may increase transportation costs for tenants. In densely populated regions, the conversion of existing industrial sites is often hindered by environmental remediation requirements and heritage preservation rules. This constrained supply landscape limits the market's ability to respond quickly to surging demand. Consequently, landlords can command higher rents, but the overall growth of the market is capped by physical and regulatory limitations. The difficulty in securing approved sites remains a persistent bottleneck for expansion.

High Construction Costs and Material Volatility

High construction costs and volatility in material prices act as major barriers to the United States warehouse market. This impacts the financial viability of new developments. The cost of building materials such as steel, concrete, and lumber has fluctuated significantly due to supply chain disruptions and inflationary pressures. According to the US Bureau of Labor Statistics, the producer price index for inputs to construction rose by approximately 2.1 to 3% in the past year (specifically, commercial/nonresidential inputs rose ~3.1%), reflecting a moderation in material cost inflation. Labor shortages in the construction sector further exacerbate these costs, as skilled workers are in high demand and command higher wages. As per sources, the average cost per square foot for industrial construction has increased substantially, forcing developers to reassess project feasibility and potentially delay cancellations. Higher interest rates also elevate financing costs, making it more expensive to fund large-scale developments. These financial pressures can lead to a reduction in the pipeline of new warehouse supply, creating a mismatch between demand and availability. Developers may pass these costs onto tenants through higher rents, which could dampen leasing activity if businesses face budget constraints. The uncertainty surrounding material availability and pricing makes long-term planning difficult for construction firms. This economic environment restrains the rapid expansion of warehouse inventory, limiting the market's ability to meet growing logistical needs efficiently.

MARKET OPPORTUNITIES

Integration of Automation and Robotics Technology

The integration of automation and robotics technology offers a great opportunity for the United States warehouse market. This improves operational efficiency and addresses labor shortages. Automated guided vehicles, robotic picking systems, and artificial intelligence-driven inventory management solutions are transforming traditional warehouses into smart facilities. According to the International Federation of Robotics (IFR) World Robotics 2024 report, the sales of professional service robots in the transportation and logistics sector grew by 35% in 2023, reflecting the increasing adoption of mobile robot solutions. These technologies enable faster order processing, reduced error rates, and optimized space utilization, making warehouses more attractive to tenants seeking high performance. As per Deloitte, companies that invest in automation report a 20 percent increase in productivity and a significant reduction in operational costs. The demand for modern facilities equipped with high power capacity and reinforced floors to support heavy machinery is rising, creating a niche for specialized warehouse developments. Providers who offer built-to-suit options with pre-installed automation infrastructure can command premium rents and secure long-term leases. The transition to Industry 4.0 standards also opens opportunities for software providers and system integrators to partner with real estate developers. This technological evolution allows warehouses to handle higher volumes of goods with greater precision, meeting the expectations of e-commerce giants. The warehouse market can overcome labor constraints and improve service quality by embracing automation. As a result, this drives sustained growth and innovation.

Expansion of Cold Storage and Specialized Facilities

The expansion of cold storage and specialized facilities provides a lucrative prospect for the United States warehouse market. This expansion is driven by changing consumer preferences and regulatory requirements. The demand for fresh food, pharmaceuticals, and temperature-sensitive goods is increasing, necessitating advanced refrigerated storage solutions. According to the Global Cold Chain Alliance (GCCA), the capacity of the top temperature-controlled warehousing providers in North America increased by approximately 14% (adding ~629 million cubic feet) in the most recent reporting year, as demand for cold storage continues to outstrip supply. The growth of meal kit services and online grocery shopping has further accelerated the need for temperature-controlled logistics infrastructure. As per the Food Marketing Institute (FMI) U.S. Grocery Shopper Trends 2024, while occasional online shopping remains elevated, frequent online grocery shopping has declined to pre-pandemic levels, indicating a shift in consumer reliance on cold chain fulfillment. Pharmaceutical companies also require strict temperature monitoring for vaccine and medication distribution, creating a stable demand for specialized warehouses. Developers can capitalize on this trend by converting existing industrial spaces into cold storage facilities or constructing new ones with energy-efficient refrigeration systems. The higher barrier to entry due to technical complexity allows for stronger pricing power and longer lease terms. Additionally, government investments in healthcare infrastructure and food security initiatives support the growth of this segment. By focusing on specialized storage, market participants can differentiate themselves and capture high-value clients who prioritize reliability and compliance. This niche represents a robust avenue for revenue growth and market diversification.

MARKET CHALLENGES

Labor Shortages and Workforce Retention Issues

Labor shortages and workforce retention issues are among the major hurdles for the United States warehouse market. This hinders operational efficiency and increases costs. The warehousing sector relies heavily on manual labor for picking, packing, and shipping, but finding qualified workers has become increasingly difficult. According to the Bureau of Labor Statistics, the quit rate in the transportation and warehousing sector remains elevated, indicating high turnover and dissatisfaction among employees. This instability forces companies to invest heavily in recruitment and training, which strains resources and disrupts workflows. As per the American Trucking Associations (ATA), the trucking sector faces a persistent shortage estimated between 60,000 and 80,000 drivers in 2025, which impacts the broader supply chain and warehouse throughput. The physical demands of warehouse work and irregular shifts contribute to recruitment challenges, particularly among younger demographics who seek more flexible employment options. Wage inflation is another consequence, as employers compete for limited talent by offering higher pay and benefits. This increased labor cost reduces profit margins for warehouse operators and tenants. The inability to staff facilities adequately can lead to delayed shipments and customer dissatisfaction, damaging reputations. While automation offers a partial solution, the transition requires time and capital, leaving many facilities vulnerable in the interim. Addressing the human capital crisis remains a critical challenge for the industry to maintain service levels and support growth.

Environmental Sustainability and Carbon Footprint Regulations

Environmental sustainability and carbon footprint regulations further impede the expansion of the United States warehouse market. This imposes new compliance requirements and operational costs. Governments and consumers are increasingly demanding greener logistics solutions, pressuring warehouse operators to reduce energy consumption and emissions. According to the Environmental Protection Agency, buildings account for a substantial portion of energy use and greenhouse gas emissions, prompting stricter building codes and efficiency standards. Retrofitting older warehouses with solar panels, LED lighting, and electric vehicle charging stations requires significant capital investment. As per the Green Building Council, achieving LEED certification or other sustainability benchmarks involves complex processes and ongoing monitoring, which can be burdensome for smaller operators. Tenants are also prioritizing eco-friendly facilities, forcing landlords to upgrade properties to remain competitive. The transition to electric fleet vehicles for last-mile delivery requires infrastructure upgrades that many existing warehouses lack. Failure to adapt to these environmental standards can result in penalties and loss of business to more sustainable competitors. The pressure to balance profitability with sustainability creates a complex operational challenge. Additionally, the lack of standardized metrics for measuring carbon footprints in logistics complicates compliance efforts. Navigating this evolving regulatory landscape requires strategic planning and investment, challenging the traditional operating models of the warehouse market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.68% |

| Segments Covered | By Warehouse Type, End Use, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Amazon.com Inc., DHL Supply Chain, Ryder Supply Chain Solutions, GXO Logistics, NFI Industries, Lineage Logistics, GEODIS North America, Americold Realty Trust, Kenco Group, FedEx Logistics, Saddle Creek Logistics Services, Penske Logistics, CJ Logistics America, XPO Logistics, Prologis Inc. |

SEGMENTAL ANALYSIS

By Warehouse Type Insights

In 2025, the general warehousing segment led the United States market. Its inherent versatility in accommodating a wide array of goods, ranging from consumer electronics to automotive parts, contributed to the leading position of this segment. These facilities are designed with flexible layouts that allow tenants to adapt storage configurations based on fluctuating inventory levels and seasonal demands. The ability to store nondurable and durable goods without specialized temperature or humidity controls makes these facilities cost-effective for a broad spectrum of industries. Moreover, the standardization of building specifications, such as clear heights and dock door ratios, facilitates easy turnover between tenants, reducing vacancy periods. This flexibility is crucial in an economic environment where businesses prioritize agility and rapid response to market changes. Furthermore, the integration of general warehouses into larger logistics parks allows for shared resources and improved transportation connectivity. The widespread availability of these structures in key logistical corridors ensures that they remain the preferred choice for companies seeking scalable storage solutions. The consistent demand from third-party logistics providers who manage diverse client portfolios further solidifies the leading position of general warehousing in the market. Besides this, the cost efficiency and broad geographic availability of general warehousing facilities drive their dominance in the US market. Compared to specialized structures, general warehouses require lower initial capital investment and maintenance costs, making them accessible to small and medium-sized enterprises. This economic advantage translates into competitive rental rates that attract a wide tenant base. The abundance of existing stock allows companies to lease space quickly without waiting for new construction, which is vital during periods of sudden demand spikes. The modular nature of these buildings enables easy expansion or contraction of leased space, aligning with business growth trajectories. Additionally, the lower energy requirements for lighting and climate control contribute to reduced operational expenses for tenants. This financial predictability is highly valued by CFOs and supply chain managers who aim to minimize fixed costs. The extensive network of general warehouses also supports intermodal transportation by locating facilities near rail yards and highways. This combination of affordability and accessibility ensures that general warehousing remains the backbone of the US logistics infrastructure.

The specialized warehousing segment is estimated to register the fastest CAGR in the US market from 2026 to 2034 due to the surging demand for temperature-controlled logistics in the food and pharmaceutical sectors. The expansion of online grocery shopping and the need for vaccine distribution have created an urgent requirement for refrigerated and frozen storage capabilities. According to the Global Cold Chain Alliance (GCCA) and Custom Market Insights (CMI), the public cold storage market in the United States is projected to grow at a 12.94% CAGR from 2026 to 2035, significantly outpacing previous estimates as e-commerce grocery and pharmaceutical needs expand. This expansion is fueled by consumer preferences for fresh and perishable goods that require strict temperature management throughout the supply chain. As per FMI – The Food Industry Association, online grocery sales are the primary driver of market growth, contributing to 72% of total category growth in 2025 and necessitating integrated omnichannel cold chain capabilities to sustain this 11.6% annual acceleration through 2028. Pharmaceutical companies are also investing heavily in specialized warehouses to comply with stringent regulatory standards for drug storage. The complexity of handling temperature-sensitive products creates higher barriers to entry, resulting in premium rental rates and longer lease terms. Developers are responding by constructing state-of-the-art facilities with advanced monitoring systems and energy-efficient refrigeration technologies. The critical nature of these services ensures steady demand even during economic downturns. Furthermore, the rise of meal kit delivery services adds another layer of demand for precise temperature control. This specialized segment offers significant growth potential as businesses prioritize supply chain integrity and product safety. Regulatory compliance and the need for secure storage of high-value inventory are key factors accelerating the growth of the specialized warehousing segment. Industries such as healthcare, aerospace, and chemicals face strict government regulations regarding the storage and handling of their products, necessitating specialized facilities. These regulatory requirements create a captive market for specialized warehouses that can offer certified compliance and risk mitigation. The high value of goods stored in these facilities, such as semiconductors and medical devices, justifies the higher costs associated with specialized infrastructure. Companies are willing to pay a premium for enhanced security features, including biometric access and 24/7 surveillance. The liability risks associated with improper storage further incentivize businesses to partner with specialized providers who possess the necessary expertise and insurance coverage. This trend is reinforced by increasing consumer awareness of product safety and quality. The specialized segment thus benefits from a structural shift toward higher standards in logistics operations. The inability of general warehouses to meet these rigorous demands ensures that specialized facilities continue to experience rapid growth and increased market share.

By End-Use Sector Insights

The retail and e-commerce segment captured the majority share of the US warehouse market in 2025. This supremacy of the segment is attributed to the widespread adoption of omnichannel retail strategies that require extensive logistical support. Retailers are integrating online and offline channels to provide seamless shopping experiences, which necessitates a network of fulfillment centers and distribution hubs. According to the National Retail Federation (NRF) 2025 Forecast, e-commerce and non-store sales are projected to grow between 7% and 9% annually, reaching approximately $1.47 trillion, which still necessitates warehouse expansion but at a more measured pace than the previous decade. The need for fast delivery options, such as same-day and next-day shipping, has decentralized supply chains, leading to the development of last-mile delivery facilities in urban areas. As per a study, retailers are investing billions in logistics infrastructure to reduce delivery times and improve customer satisfaction. The complexity of managing returns, known as reverse logistics, also requires dedicated warehouse space for processing and restocking items. This operational complexity drives demand for modern facilities equipped with automation and sorting technology. The shift from bulk storage to piece picking operations has transformed warehouse design, requiring higher ceilings and more sophisticated layout configurations. Major retail giants are setting the standard for logistics efficiency, forcing competitors to follow suit. The continuous evolution of consumer expectations ensures that the retail sector remains the primary driver of warehouse demand. The integration of physical stores as mini fulfillment centers further blurs the lines between retail and logistics, reinforcing the sector's dominance. Inventory buffering and the focus on supply chain resilience are significant drivers of warehouse demand within the retail sector. The disruptions caused by global events have prompted retailers to move away from just-in-time inventory models toward holding larger safety stocks. According to the Institute for Supply Management (ISM) 2025 Report on Business, rather than carrying 20–30% excess, retailers have shifted to a "Just-in-Case 2.0" model that emphasizes leaner, high-velocity inventory, with the Retail Inventory-to-Sales Ratio stabilizing near 1.30 as of early 2026. This strategic shift requires additional warehouse space to store excess goods closer to end markets. As per Deloitte, the emphasis on supply chain visibility and agility has led to the creation of regional distribution centers that can quickly respond to local demand fluctuations. Retailers are also diversifying their supplier base, which increases the variety of goods entering the country and necessitates broader storage capabilities. The need to manage seasonal peaks and promotional events further amplifies the requirement for flexible warehouse space. Third-party logistics providers play a crucial role in this ecosystem by offering scalable solutions that allow retailers to adjust capacity as needed. The financial impact of lost sales due to inventory shortages has made warehouse availability a critical competitive advantage. Consequently, retailers are securing long-term leases for prime warehouse locations to ensure operational continuity. This focus on resilience ensures sustained demand for warehouse space across the retail landscape.

The food and beverages segment is anticipated to witness the fastest CAGR in the US warehouse market during the forecast period, owing to the rapid expansion of online grocery and fresh food delivery services. Consumers are increasingly purchasing perishable items online, requiring sophisticated cold chain infrastructure to maintain freshness and safety. According to sources, online grocery sales have grown significantly and are expected to capture a larger share of total food retail in the coming years. This trend necessitates the construction of specialized distribution centers equipped with refrigeration and freezing capabilities. Food retailers are partnering with third-party logistics providers to establish dedicated cold storage networks that can support rapid delivery schedules. The short shelf life of many food products requires efficient inventory turnover and precise temperature control, driving investment in advanced warehouse technologies. The rise of meal kit services and direct-to-consumer food brands further contributes to this growth by creating new distribution channels that rely on specialized warehousing. The need to comply with food safety regulations also mandates high standards for facility hygiene and monitoring. This sector's growth is supported by changing consumer lifestyles and the convenience of home delivery. The continuous innovation in food logistics ensures that the food and beverages segment remains a dynamic and rapidly expanding component of the warehouse market. Strict regulatory standards and traceability requirements are key factors propelling the growth of the food and beverages segment in the warehouse market. The Food Safety Modernization Act imposes rigorous guidelines on the storage and handling of food products to prevent contamination and ensure public health. These technologies require specialized infrastructure and data management capabilities that general warehouses may not possess. The complexity of managing expiration dates and batch numbers necessitates advanced inventory management systems that integrate seamlessly with warehouse operations. Retailers and distributors are investing in facilities that can provide real-time visibility into product status and location. The liability risks associated with foodborne illnesses make compliance a top priority, driving demand for certified storage providers. Furthermore, the globalization of food supply chains increases the need for facilities that can handle imported goods with varying regulatory requirements. The focus on transparency and safety ensures that food and beverage companies prioritize specialized warehousing solutions. This regulatory environment creates a strong tailwind for the growth of this segment as companies seek to mitigate risks and enhance consumer trust.

REGIONAL ANALYSIS

United States Warehouse Market Analysis

The United States was the prominent player in the warehouse market and accounted for a 40.6% share in 2025. Factors such as a vast geographic landscape, robust consumer spending, and a highly developed transportation network fuel the growth of the US market. According to the U.S. Census Bureau, the total value of wholesale trade sales exceeds $8 trillion annually, highlighting the massive scale of goods movement that relies on warehouse infrastructure. The market status is characterized by high occupancy rates and rising rental prices, particularly in key logistics hubs such as Los Angeles, Chicago, and New Jersey. As per JLL, the vacancy rate for industrial properties in the United States has risen to 6.4% as of early 2026, reflecting a normalization of the market as record levels of new construction are delivered. The country benefits from extensive interstate highway systems and major ports that facilitate efficient domestic and international trade. The presence of leading e-commerce companies and third-party logistics providers drives continuous innovation in warehouse design and automation. Government initiatives to upgrade infrastructure further support market growth by improving connectivity and reducing transportation bottlenecks. The United States also leads in the adoption of sustainable building practices, with many new developments targeting LEED certification. The mature financial markets provide ample capital for real estate investment trusts and developers to fund large-scale projects. This combination of scale, efficiency, and innovation ensures that the United States remains the central pillar of the global warehouse industry, setting trends that influence markets worldwide.

COMPETITION OVERVIEW

The competition in the United States warehouse market is intense and characterized by the presence of large real estate investment trusts, specialized logistics providers, and emerging technology-driven firms. Major players compete based on location portfolio quality, technological integration, and sustainability features to attract premium tenants. The scarcity of land in key logistics hubs has intensified competition for development sites and existing properties, driving up acquisition costs. Companies differentiate themselves by offering value-added services such as automated sorting systems and energy-efficient building designs. The rise of e-commerce has increased demand for last-mile facilities, prompting investors to focus on urban infill projects. Strategic partnerships with technology providers enable firms to offer smart warehouse solutions that improve operational efficiency for clients. Labor availability and cost also influence competitive dynamics as companies seek locations with accessible workforces. Regulatory environments vary by state,e affecting development timelines and operational costs. The market sees frequent consolidation through mergers and acquisitions as larger entities seek to achieve scale and diversify their geographic presence. This dynamic landscape requires continuous innovation and strategic agility to maintain market leadership and satisfy evolving customer expectations in a rapidly changing logistics environment.

KEY MARKET PLAYERS

A few major players of the United States warehouse market include

- Amazon.com Inc

- DHL Supply Chain

- Ryder Supply Chain Solutions

- GXO Logistics

- NFI Industries

- Lineage Logistics

- GEODIS North America

- Americold Realty Trust

- Kenco Group

- FedEx Logistics

- Saddle Creek Logistics Services

- Penske Logistics

- CJ Logistics America

- XPO Logistics

- Prologis Inc

Leading Players in the Market

- Prologis Inc is a global leader in logistics real estate with a dominant presence in the United States warehouse market. The company owns and operates high-quality distribution facilities that serve a diverse customer base, including e-commerce retailers and third-party logistics providers. Prologis focuses on strategic locations near major population centers and transportation hubs to maximize supply chain efficiency. Recent actions include the acquisition of Duke Realty, which significantly expanded its portfolio and enhanced its scale in key US markets. The company also invests heavily in sustainability initiatives such as solar power installation and electric vehicle charging infrastructure to meet tenant demands for green buildings. Prologis leverages its proprietary technology platform to optimize facility management and provide data-driven insights to customers. These efforts strengthen its market position by offering superior service and modern infrastructure that support the evolving needs of global commerce.

- Americold Logistics LLC is a leading provider of temperature-controlled warehousing and logistics services with a significant footprint in the United States. The company specializes in cold storage solutions for the food and beverage industry, ensuring product quality and safety through advanced refrigeration technologies. Americold operates a vast network of automated facilities that enable efficient inventory management and rapid order fulfillment. Recent actions include the expansion of its automation capabilities through partnerships with robotics firms to enhance operational efficiency and reduce labor costs. The company also pursues strategic acquisitions to increase its geographic reach and capacity in high-demand regions. Americold focuses on sustainability by implementing energy-efficient systems and reducing its carbon footprint across its operations. These initiatives reinforce its position as a critical partner for food producers and retailers seeking reliable and scalable cold chain solutions in a competitive market environment.

- Lineage Inc is a prominent player in the global cold storage and logistics industry with extensive operations in the United States warehouse market. The company provides integrated supply chain solutions, including temperature-controlled storage, transportation, and value-added services for perishable goods. Lineage leverages advanced technology and data analytics to optimize inventory visibility and improve decision-making for its clients. Recent actions include significant investments in automation and artificial intelligence to streamline warehouse operations and enhance productivity. The company also expands its network through strategic mergers and acquisitions that add capacity in key logistical corridors. Lineage prioritizes sustainability by adopting renewable energy sources and improving energy efficiency in its facilities. These efforts strengthen its market position by delivering innovative and environmentally responsible solutions that meet the growing demands of the food and pharmaceutical industries for reliable cold chain infrastructure.

Top Strategies Used by Key Market Participants

Key players in the United States warehouse market employ several major strategies to maintain competitiveness and drive growth. Strategic acquisitions are common as companies seek to expand their portfolios and gain access to prime locations in high-demand markets. Development of build-to-suit facilities allows providers to tailor warehouses to specific tenant requirements, fostering long-term relationships. Investment in automation and technology enhances operational efficiency and addresses labor shortages by reducing reliance on manual processes. Sustainability initiatives such as solar power and energy-efficient designs attract environmentally conscious tenants and comply with regulatory standards. Focusing on last-mile delivery networks enables faster response times to consumer demands in urban areas. Diversification into specialized sectors like cold storage provides higher margins and reduces dependency on general warehousing trends. These strategies ensure that market participants can adapt to changing logistics needs and maintain strong occupancy rates.

MARKET SEGMENTATION

This research report on the US warehouse market has been segmented and sub-segmented based on warehouse type, end use & region.

By Warehouse Type

- General Warehousing

- Specialized Warehousing

By End Use

- Retail

- Food & Beverages

By Region

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

1. What factors are driving growth in the U.S. warehouse market?

Growth is driven by e-commerce expansion, rising demand for faster delivery, and increasing supply chain optimization.

2. What are the main types of warehouses in the U.S.?

Key types include public warehouses, private warehouses, bonded warehouses, distribution centers, and cold storage facilities.

3. How does e-commerce impact the warehouse market?

E-commerce significantly boosts demand for fulfillment centers and last-mile delivery warehouses.

4. What role does automation play in warehouses?

Automation improves efficiency, reduces labor costs, and enhances inventory accuracy.

5. What technologies are used in modern warehouses?

Technologies include warehouse management systems (WMS), robotics, IoT, and AI-driven analytics.

6. What is cold storage warehousing?

Cold storage warehouses store temperature-sensitive goods like food and pharmaceuticals.

7. Who are the key end-users of warehouse services?

Major end-users include retail, e-commerce, manufacturing, healthcare, and food & beverage industries.

8. What challenges does the U.S. warehouse market face?

Challenges include labor shortages, high real estate costs, and supply chain disruptions

9. How is sustainability impacting warehouses?

Companies are adopting energy-efficient buildings, solar power, and green logistics practices.

10. What is the future outlook of the U.S. warehouse market?

The market is expected to grow steadily due to increasing trade and digital commerce.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com