Europe Drone as a Service Market Size, Share, Trends, and Growth Analysis Report, Segmented by Service Type, End User Industry, Drone Type, Operating Range, and Country – Industry Forecast From 2026 to 2034

Europe Drone as a Service Market Report Summary

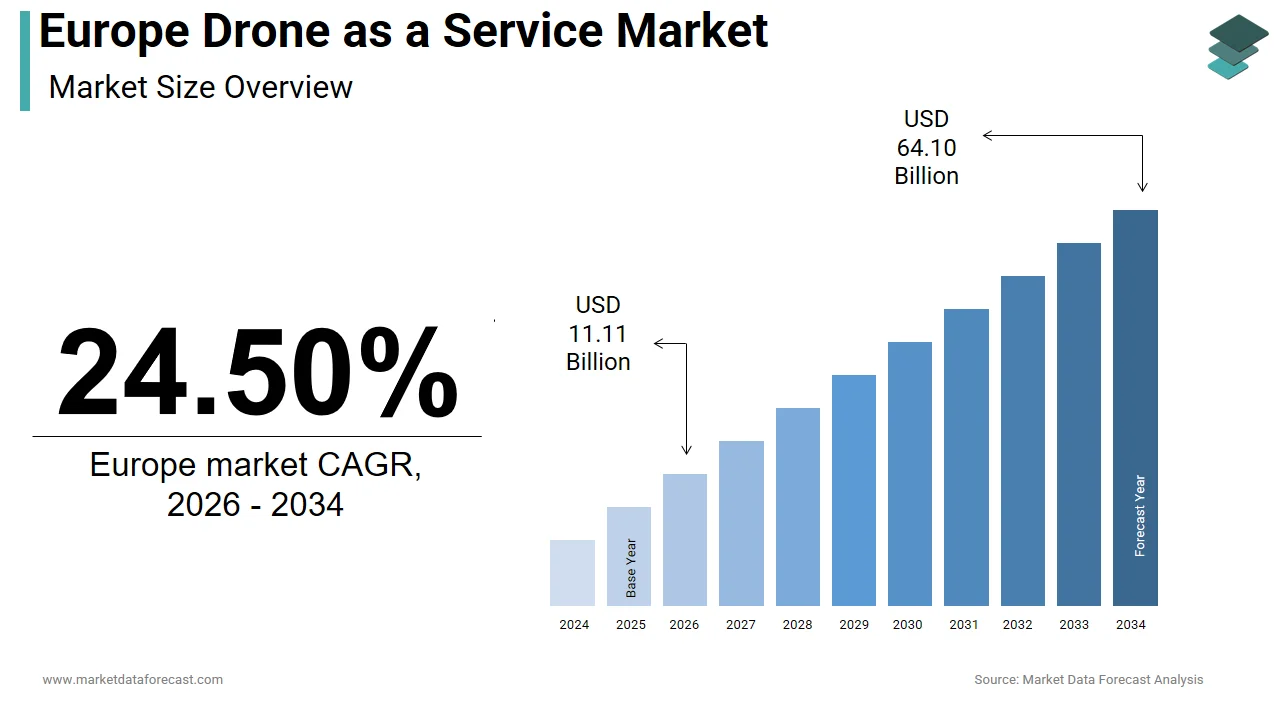

The Europe drone-as-a-service (DaaS) market was valued at USD 8.92 billion in 2025, is estimated to reach USD 11.11 billion in 2026, and is projected to reach USD 64.10 billion by 2034, growing at a CAGR of 24.50% from 2026 to 2034. Market growth is driven by increasing adoption of drone technology for aerial data collection, monitoring, and inspection across industries such as construction, agriculture, energy, and logistics. Drone as a service enables organizations to access drone capabilities without investing in hardware, pilots, or operational infrastructure. The rising demand for real-time data analytics, infrastructure monitoring, and precision agriculture, along with supportive regulatory frameworks for commercial drone operations, is further accelerating market expansion across Europe.

Key Market Trends

- Increasing adoption of drone-based data analytics and aerial monitoring solutions.

- Growing demand for infrastructure inspection, surveying, and mapping services.

- Rising integration of AI, machine learning, and advanced imaging technologies in drone operations.

- Expansion of precision agriculture and environmental monitoring applications.

- Supportive regulatory frameworks promoting commercial drone operations and innovation.

Segmental Insights

- Based on service type, the data analytics and processing services segment held a dominant share of the Europe drone as a service market in 2025, driven by growing demand for actionable insights derived from aerial imagery and geospatial data.

- Based on end-user industry, the construction and infrastructure sector accounted for a significant share in 2025, supported by the increasing use of drones for site surveying, progress monitoring, and structural inspections.

- Based on drone type and operating range, the rotary-wing drone segment dominated the market in 2025, owing to the versatility of multirotor drones that offer vertical takeoff and landing capabilities, making them ideal for urban environments and complex industrial sites.

Regional Insights

The Europe drone as a service market is witnessing rapid growth across major countries, supported by increasing industrial adoption of drone technology and favorable regulatory policies.

- The United Kingdom led the regional market in 2025, supported by a proactive regulatory framework established by the Civil Aviation Authority and strong adoption of drone services in the infrastructure and energy sectors.

- Germany held the second-largest position in the market, driven by strong industrial demand for drone-based inspection and monitoring solutions in manufacturing, energy, and logistics sectors.

- France is experiencing strong market growth due to its dual focus on defense applications and large-scale agricultural monitoring through advanced drone technologies.

Competitive Landscape

The Europe drone-as-a-service market is characterized by specialized drone service providers, aerospace companies, and technology firms competing through innovation and service expansion. Market players are focusing on integrating advanced analytics platforms, AI-based image processing, and autonomous flight capabilities to enhance service efficiency. Strategic partnerships with infrastructure companies, energy providers, and government agencies are shaping competitive dynamics across the region.

Prominent companies operating in the Europe drone as a service market include Cyberhawk Innovations Limited, Sky Futures Partners Limited, DroneDeploy, Inc., Airbus SE, Parrot SA, Terra Drone Corporation, Aerodyne Group, and Wingcopter GmbH.

Europe Drone as a Service Market Size

The Europe drone-as-a-service market was valued at USD 8.92 billion in 2025, is estimated to reach USD 11.11 billion in 2026, and is projected to reach USD 64.10 billion by 2034, growing at a CAGR of 24.50% from 2026 to 2034.

The drone as a service is a transformative operational model, where organizations access unmanned aerial vehicle capabilities, data analytics, and specialized pilot expertise through subscription or on-demand contracts rather than owning physical assets. The definition encompasses end-to-end solutions including flight planning, real-time data transmission, and post-processing analytics delivered by specialized providers. According to Eurostat, the agricultural sector in the European Union utilizes over 157 million hectares of land, creating a vast addressable area for precision farming services that drive demand for aerial monitoring. As per the European Union Aviation Safety Agency, the number of registered drone operators in Europe surpassed 500,000 in 2024, reflecting a burgeoning ecosystem of service providers and skilled pilots. In 2025, the market witnessed a significant pivot towards beyond visual line of sight operations, enabled by new regulatory frameworks that permit autonomous flights over populated areas under strict conditions.

MARKET DRIVERS

Stringent Regulatory Frameworks Enabling Beyond Visual Line of Sight Operations

The implementation of comprehensive regulations by the European Union Aviation Safety Agency by legally permitting complex autonomous operations that were previously restricted. The stringent regulatory frameworks enabling beyond visual line of sight operations is ascribed in boosting the growth of Europe drone as a service market. The specific category framework allows operators to conduct flights beyond visual line of sight provided they meet rigorous safety objectives, thereby unlocking lucrative use cases in long-distance infrastructure inspection and delivery. According to the European Commission, the adoption of the U-space regulation has created a standardized digital airspace management system across member states, facilitating seamless cross-border drone services. This regulatory clarity reduces legal uncertainty for service providers, encouraging them to invest in advanced fleets and automated software platforms. Furthermore, the requirement for remote identification and geo-awareness systems has enhanced public trust by making municipalities more willing to procure drone services for urban monitoring. The harmonization of rules across the bloc eliminates the need for service providers to navigate disparate national laws by enabling scalability.

Escalating Demand for Cost-Efficient Infrastructure Inspection and Maintenance

The urgent need for cost-effective and high-frequency inspection of aging infrastructure as a powerful driver for the adoption of drone as a service models. The escalating demand for cost-efficient infrastructure inspection and maintenance is greatly influencing the growth of Europe drone as a service market. With billions of euros allocated annually for maintaining bridges, railways, and energy grids, asset owners seek alternatives to traditional manned helicopter surveys or dangerous manual climbs that are both expensive and risky. Drone service providers offer high-resolution thermal imaging and LiDAR scanning capabilities that detect structural defects with greater precision than conventional methods by reducing downtime and preventing catastrophic failures. Industry analysis reveals that using drones for wind turbine inspections can reduce costs by up to 50% compared to rope access techniques with a compelling economic argument for energy companies. The ability to deploy specialized drones on demand allows utilities to respond rapidly to emergencies without maintaining idle fleets. Furthermore, the integration of artificial intelligence in service packages enables automated defect recognition, delivering actionable insights faster than human analysts.

MARKET RESTRAINTS

Public Concerns Regarding Privacy and Data Protection Compliance

Persistent public anxiety surrounding privacy infringement and the strict enforcement of data protection laws act as a significant restraint on the widespread adoption of drone as a service solutions in Europe. The public concerns regarding privacy and data protection compliance is limiting the growth of Europe drone as a service market. The General Data Protection Regulation imposes rigorous requirements on the collection, storage, and processing of personal data captured inadvertently by drone cameras, creating complex compliance hurdles for service providers. According to a survey by the European Data Protection Board, over 65% of European citizens express concern about unauthorized surveillance by drones, leading to local opposition against drone operations in residential areas. This sentiment forces municipalities and private clients to hesitate before contracting drone services due to fear of reputational damage or legal liabilities. Service providers must invest heavily in privacy-by-design technologies such as automatic face blurring and geofencing to mitigate risks, increasing operational costs. The ambiguity regarding liability when data breaches occur further complicates contract negotiations, often delaying project initiation. Additionally, varying interpretations of privacy laws across different member states create a fragmented operational landscape, hindering the scalability of pan-European service offerings. Until robust technical safeguards become standard and public perception shifts through successful transparent deployments, privacy concerns will continue to limit market expansion and restrict flight zones in densely populated regions.

Limitations in Battery Technology and Payload Capacity

The current technological constraints regarding battery energy density and payload limitations serve on the operational efficiency and range of drone as a service offerings in Europe. These limitations in battery technology are also degrading the growth of Europe drone as a service market. Most commercial drones available for service contracts suffer from short flight times, typically ranging between 20 to 30 minutes, which restricts the area they can cover in a single mission and necessitates frequent battery swaps or recharging. According to the Joint Research Centre of the European Commission, advancements in battery chemistry have lagged behind the growing demands for longer endurance missions for heavy-lift applications like cargo delivery or extended surveillance. This limitation increases the logistical complexity and cost of service delivery, as multiple drones and pilots are required to complete tasks that could be handled by a single manned aircraft. The inability to carry heavier sensors or multiple payloads simultaneously reduces the versatility of drone services for complex industrial inspections requiring diverse data types. Furthermore, extreme weather conditions common in Northern Europe can significantly degrade battery performance, leading to mission cancellations and unreliable service levels. While research into hydrogen fuel cells and solid-state batteries is ongoing, the current reliance on lithium-ion technology caps the potential scope of services.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence for Autonomous Data Analytics

The emergence of drone hardware with advanced artificial intelligence algorithms to evolve from simple data collection to intelligent decision-making platforms is creating the new opportunities for the growth of Europe drone as a service market. Service providers can leverage machine learning models to process vast amounts of aerial imagery in real time, automatically identifying anomalies, counting assets, or predicting equipment failures without human intervention. This capability allows drone service firms to offer premium analytics subscriptions that deliver immediate actionable insights, drastically reducing the turnaround time for clients in sectors like agriculture and construction. For instance, AI-driven services can instantly calculate crop health indices or detect micro-cracks in bridge structures, adding immense value beyond raw video footage. The automation of data processing also lowers operational costs by reducing the need for large teams of manual analysts, improving profit margins for providers. Furthermore, the ability to train models on specific European infrastructure types creates a competitive moat for local service providers. As AI technology matures, the shift towards fully autonomous insight generation will redefine the value proposition of drone services, opening new revenue streams and deepening client dependencies.

Expansion of Urban Air Mobility and Last-Mile Delivery Networks

The emerging sector of urban air mobility and the pressing need for efficient last-mile logistics create a lucrative opportunity for the Europe drone as a service market to revolutionize supply chains in dense metropolitan areas. As e-commerce volumes continue to swell and traffic congestion worsens, retailers and logistics companies are increasingly seeking aerial solutions to bypass ground bottlenecks and deliver goods rapidly. According to the European Court of Auditors, urban freight transport accounts for nearly 25% of CO2 emissions in cities, driving a policy push towards electric vertical takeoff and landing vehicles for sustainable delivery. Drone service providers can establish networks of automated hubs to facilitate on-demand delivery of medical supplies, food, and small parcels, operating under the new U-space frameworks designed for high-density airspace. Pilot projects in cities like Helsinki and Paris have demonstrated the feasibility of these operations, paving the way for commercial scaling. The opportunity extends to emergency medical services, where drones can transport blood samples or defibrillators faster than ambulances in gridlocked traffic.

MARKET CHALLENGES

Complexity of Integrating into Congested Airspace Management Systems

The technical and operational difficulty of integrating thousands of autonomous drones into already congested and highly regulated European airspace without compromising safety. The complexity of integrating into congested airspace management systems is one of the challenges for the growth of Europe drone as a service market. The coexistence of manned aviation, military exercises, and emerging drone traffic requires sophisticated uncrewed traffic management systems that are still in developmental stages across many member states. According to Eurocontrol, European airspace is among the busiest in the world, with over 30,000 flights daily, leaving limited room for error in drone integration. Service providers must navigate complex dynamic no-fly zones and coordinate with air traffic control in real time, which demands high levels of connectivity and interoperability that current infrastructure often lacks. The lack of a fully unified digital sky across all EU nations means that service providers face fragmented technical requirements when operating cross-border, increasing complexity and costs. Furthermore, the risk of signal interference in urban environments can lead to loss of control incidents, posing severe safety hazards. Developing robust detect-and-avoid systems that function reliably in all weather conditions remains an engineering hurdle.

Acute Shortage of Certified Pilots and Technical Specialists

The severe scarcity of professionally certified drone pilots and technical specialists capable of managing complex unmanned systems is also acting as a barrier for the growth of the Europe drone as a service market. As demand for specialized services surges, the supply of qualified personnel who possess both flight skills and domain expertise in data analysis fails to keep pace, leading to project delays and inflated labor costs. According to the European Skills Index, the deficit of digital and technical skills in the EU workforce has widened, with specific shortages in emerging technologies like robotics and remote sensing. Operating advanced drones under the specific category regulations requires extensive training and certification, creating a high barrier to entry for new talent. Many service providers struggle to recruit staff who can handle emergency scenarios, perform maintenance, and interpret complex sensor data simultaneously. The rapid evolution of drone technology also necessitates continuous upskilling, which many smaller service firms cannot afford. This talent gap limits the capacity of providers to scale their operations and accept larger contracts, stifling market potential.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Service Type, End User Industry, Drone Type, Operating Range, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Cyberhawk Innovations Limited, Sky Futures Partners Limited, DroneDeploy, Inc., Airbus SE, Parrot SA, Terra Drone Corporation, Aerodyne Group, Wingcopter GmbH, and Others. |

SEGMENTAL ANALYSIS

By Service Type Insights

The data analytics and processing services segment was accounted in holding a dominant share of the Europe drone as a service market in 2025 owing to the fundamental shift in client expectations where raw aerial imagery is no longer sufficient, where organizations demand actionable insights derived from complex datasets. The primary factor fueling this dominance is the increasing reliance on artificial intelligence and machine learning algorithms to interpret vast volumes of geospatial data automatically by reducing the need for manual analysis. According to the European Commission, the volume of geospatial data generated by unmanned systems in the EU is projected to grow by 35% annually, creating an immense need for sophisticated processing capabilities. Furthermore, industries such as agriculture and energy require precise metrics like crop health indices or thermal anomaly detection, which can only be delivered through advanced analytical software bundled with flight services. The integration of cloud-based platforms allows for real-time data sharing and collaborative decision-making, further cementing the value of analytics services.

The autonomous flight operations segment is emerging as the fastest CAGR of 24.8% from 2026 to 2034 with the maturation of Beyond Visual Line of Sight regulations and the urgent industry need to scale operations without proportionally increasing pilot headcount. A key driving factor is the deployment of U-space infrastructure across major European cities, which enables safe, automated drone traffic management in dense environments without constant human intervention. According to the Single European Sky ATM Research initiative, over 200 autonomous flight corridors are scheduled to become operational by 2026, which is directly facilitating the expansion of fully automated service models. The ability to conduct repetitive missions, such as perimeter security patrols or pipeline inspections with minimal human oversight significantly reduces operational costs and enhances efficiency for service providers. Additionally, advancements in detect-and-avoid technologies have increased safety confidence, allowing regulators to approve more complex autonomous scenarios.

By End User Industry Insights

The construction and infrastructure sector was accounted in holding 31.2% of the Europe drone as a service market share in 2024 owing to the need to monitor large-scale projects, ensure regulatory compliance, and enhance worker safety in an industry plagued by labor shortages and tight margins. The growth of the segment is majorly driven by the mandatory requirement for detailed progress reporting and Building Information Modeling integration, which drones facilitate through high-resolution 3D mapping and volumetric analysis. Drone services offer a cost-effective alternative to traditional surveying methods by reducing inspection times by up to 70%, while providing real-time data to project managers. Furthermore, the aging infrastructure across Europe, including bridges and railways, requires frequent structural health assessments that are dangerous for humans but ideal for unmanned systems. The ability to detect defects early using thermal and LiDAR sensors prevents costly failures, making drone services indispensable for asset owners.

The agriculture and forestry segment is anticipated to register a CAGR of 22.5% throughout the forecast period with the intensifying pressure to maximize crop yields and optimize resource usage amidst climate change challenges and stringent environmental regulations. The widespread adoption of precision farming techniques supported by the European Common Agricultural Policy, which incentivizes farmers to use data-driven approaches for fertilizer and pesticide application. According to Eurostat, agricultural land in the EU covers over 157 million hectares, representing a massive addressable market for aerial monitoring services that can cover vast areas efficiently. Drone services provide multispectral imaging that reveals plant stress levels invisible to the naked eye by enabling targeted interventions that reduce chemical runoff and improve sustainability. The rising cost of inputs and labor shortages in rural areas further compel farmers to outsource aerial scouting to specialized service providers rather than investing in their own fleets.

By Drone Type and Operating Range Insights

The rotary-wing drone segment was the largest by capturing 58.2% of the Europe drone as a service market share in 2024 with the unparalleled versatility of multirotor configurations, which offer vertical takeoff and landing capabilities essential for operating in confined urban spaces and complex industrial sites. The ability of rotary-wing drones to hover stationary for extended periods, a requirement for detailed infrastructure inspections, thermal scanning, and close-up photography. These drones are indispensable for inspecting wind turbines, power lines, and building facades where fixed-wing aircraft cannot operate safely or effectively. Furthermore, the lower entry barrier for pilots and the availability of robust, off-the-shelf models make rotary-wing services more accessible and cost-effective for a wide range of applications. The continuous improvement in battery life and payload capacity for multirotors further extends their utility, ensuring they remain the workhorse of the European drone service industry despite the emergence of other configurations.

The hybrid vertical takeoff and landing (VTOL) drone segment is emerging as a fastest CAGR of 26.3% from 2025 to 2033 with the unique ability of hybrid drones to combine the vertical launch convenience of multirotors with the long-endurance flight characteristics of fixed-wing aircraft, addressing the range limitations of traditional platforms. According to the Joint Research Centre of the European Commission, hybrid VTOL technologies are identified as critical enablers for the future of urban air mobility and inter-city cargo delivery networks. These drones can cover distances of over 100 kilometers on a single charge by making them ideal for servicing remote assets without the need for multiple battery swaps or ground crew relocation. The regulatory push towards integrating drones into national airspace for extended operations favors hybrid designs that offer greater reliability and safety margins. Additionally, advancements in lightweight composite materials and efficient propulsion systems have reduced acquisition costs by making hybrid services more economically viable for providers.

COUNTRY-LEVEL ANALYSIS

United Kingdom Drone as a Service Market Analysis

The United Kingdom was the largest contributor of the Europe drone as a service market by occupying 23.3% of share in 2024 with its proactive regulatory framework established by the Civil Aviation Authority, which has been a global pioneer in approving Beyond Visual Line of Sight trials and urban drone operations. British enterprises across construction, energy, and media sectors have rapidly adopted drone services to enhance operational efficiency and safety standards. According to the UK Department for Transport, over 1,000 commercial drone operators are registered under the specific category, facilitating a robust ecosystem of service providers. The presence of leading aerospace research institutions and a vibrant startup scene in London and Bristol drives continuous innovation in autonomous flight and data analytics. The government's "Future of Flight" action plan provides significant funding for testing facilities and digital sky infrastructure by attracting international investment. Furthermore, the island's geography makes it an ideal testbed for maritime and coastal monitoring services. The strong collaboration between regulators and industry stakeholders ensures that new technologies can be deployed rapidly while maintaining high safety levels.

Germany Drone as a Service Market Analysis

Germany drone as a service market held second position by holding 19.3% of share in 2024 with its massive industrial base and rigorous engineering culture. German companies in the automotive, manufacturing, and renewable energy sectors, utilize drone services for highly precise quality control, factory site monitoring, and wind farm inspections. According to the German Federal Ministry for Economic Affairs and Climate Action, investments in industrial digitization have surged, with drone integration being a key component of Industry 4.0 strategies. The dense network of small and medium-sized enterprises creates a diverse demand for specialized aerial services tailored to specific industrial needs. Germany's central location in Europe also makes it a logistical hub for cross-border drone service trials and supply chain optimization projects. The government's support for developing urban air mobility concepts in cities like Munich and Stuttgart further stimulates market activity.

France Drone as a Service Market Analysis

France drone as a service market is lucratively growing with a strong dual focus on defense applications and large-scale agricultural monitoring. According to the French Civil Aviation Authority, the number of commercial drone activities related to surveillance and precision farming has doubled since 2023, driven by favorable subsidies and regulatory support. French service providers excel in offering integrated solutions that combine aerial data with advanced agronomic analysis by catering to the country's vast farmland. The presence of major aerospace manufacturers and defense contractors fosters a sophisticated ecosystem for high-end drone services used in border control and critical infrastructure protection. Additionally, France's active role in shaping European drone regulations ensures that domestic providers are well-prepared for continental expansion. The cultural acceptance of technology in rural areas and the strong cooperative structure of French agriculture facilitate rapid adoption of drone services among farmers.

Italy Drone as a Service Market Analysis

Italy drone as a service market growth is driven by the unique demand for drone services focused on cultural heritage preservation and infrastructure maintenance. The necessity to monitor thousands of historical sites, ancient ruins, and aging bridges that require non-invasive inspection methods, only drones can provide. According to the Italian National Institute of Statistics, the tourism and cultural sector contributes significantly to the economy, prompting extensive use of drones for 3D modeling and restoration planning. Furthermore, Italy's challenging geography, prone to earthquakes and landslides, creates a constant need for rapid aerial assessment services for disaster management and civil protection. Italian service providers have developed specialized expertise in operating in complex urban environments and rugged terrains by offering tailored solutions for local authorities and private owners. The government's incentives for digitalizing public administration and improving infrastructure resilience have boosted procurement of drone services.

Netherlands Drone as a Service Market Analysis

The Netherlands drone as a service market growth with its role as a global logistics hub and a pioneer in smart city initiatives. Dutch corporations, particularly in the shipping, port management, and e-commerce sectors, require advanced drone services for inventory management, terminal surveillance, and last-mile delivery trials. The country's high population density and advanced digital infrastructure make it an ideal testing ground for urban drone operations and automated traffic management systems. According to Statistics Netherlands, the logistics sector handles a significant portion of European trade, necessitating real-time aerial monitoring to optimize supply chain efficiency. The Dutch government's progressive stance on aviation innovation has led to the establishment of dedicated drone zones and living labs in cities like Rotterdam and Amsterdam. Local service providers are at the forefront of developing solutions for water management and flood monitoring, critical issues for the low-lying nation. The strong collaboration between knowledge institutions, startups, and government bodies fosters a culture of experimentation and rapid deployment.

COMPETITIVE LANDSCAPE

The competition in the Europe drone as a service market is intensely fierce characterized by a dynamic mix of established aerospace conglomerates, agile specialized startups, and traditional surveying firms transitioning to aerial robotics. Market participants constantly innovate their autonomous capabilities and data analytics platforms to distinguish their offerings in a sector where hardware differentiation is becoming increasingly difficult. Price competition exists but is often secondary to the value provided through regulatory compliance, safety records, and the depth of actionable insights delivered to clients. The complex regulatory landscape involving the European Union Aviation Safety Agency creates high barriers to entry that favor incumbents with robust certification frameworks and proven operational histories. Strategic alliances with technology giants and logistics companies are common as firms seek to scale their operations and integrate seamlessly into existing digital ecosystems. The shift towards beyond visual line of sight operations has intensified the race to develop reliable detect-and-avoid systems and secure communication links. Vendors must balance technological advancement with rigorous safety standards to maintain trust among government and industrial clients.

KEY MARKET PLAYERS

The leading companies operating in the Europe drone as a service market include:

- Cyberhawk Innovations Limited

- Sky Futures Partners Limited

- DroneDeploy, Inc.

- Airbus SE

- Parrot SA

- Terra Drone Corporation

- Aerodyne Group

- Wingcopter GmbH

TOP PLAYERS IN THE MARKET

- Airbus SE stands as a global aerospace giant with a profound impact on the Europe drone as a service market through its specialized unmanned systems division. The company provides comprehensive aerial data solutions for infrastructure inspection, public safety, and defense applications across the continent. Their global contribution involves setting industry standards for heavy-lift capabilities and long-endurance autonomous flights that serve diverse international sectors. Recent actions to strengthen their market position include the launch of new fully automated drone-in-a-box solutions designed for continuous monitoring without pilot intervention. Airbus actively partners with European telecommunications firms to integrate 5G connectivity into their drone fleets, enabling real-time high-definition data transmission. They also focus on developing urban air mobility services that leverage their extensive aviation expertise to solve complex logistics challenges.

- Parrot SA operates as a leading European manufacturer and service provider specializing in professional drones for agriculture, construction, and public security sectors. The company enables businesses to access high-precision aerial imaging and mapping services through its network of certified partners and direct service offerings. Their global contribution lies in pioneering lightweight, portable drone technologies that democratize access to professional aerial data for small and medium enterprises worldwide. Recent strategic moves involve expanding their software ecosystem to include artificial intelligence-driven analytics platforms that automate crop health assessment and site progress tracking. Parrot strengthens its market position by forming alliances with agritech companies to offer bundled hardware and data services tailored to specific farming needs. They actively invest in research to enhance battery life and obstacle avoidance systems, ensuring safer operations in complex environments.

- Wingcopter GmbH serves as a prominent innovator in the Europe drone as a service market with its unique hybrid vertical takeoff and landing aircraft designed for efficient delivery and survey missions. The company delivers specialized logistics and inspection services that bridge the gap between short-range multirotors and long-range fixed-wing aircraft. Their global contribution includes revolutionizing last-mile delivery networks in remote and urban areas through sustainable electric propulsion systems. Recent actions to solidify their standing involve securing major contracts with postal services and healthcare providers to establish automated medical supply chains across German regions. Wingcopter actively collaborates with regulatory bodies to define safety protocols for beyond visual line of sight operations, paving the way for broader commercial adoption. They have also enhanced their ground control software to manage large fleets autonomously, reducing operational costs for service providers.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe drone as a service market primarily focus on developing fully autonomous drone-in-a-box systems to enable continuous monitoring and reduce reliance on human pilots significantly. Companies aggressively pursue strategic partnerships with telecommunications providers to leverage fifth generation networks for real-time data transmission and enhanced connectivity. Major participants are investing heavily in artificial intelligence and machine learning algorithms to automate data analysis and provide actionable insights instantly to clients. Firms are expanding their service portfolios to include specialized industry solutions such as precision agriculture packages and infrastructure health monitoring tools. Additionally, market leaders are engaging proactively with regulatory authorities to shape policies that facilitate beyond visual line of sight operations and urban air mobility integration. These strategies aim to increase operational efficiency, ensure regulatory compliance, and capture emerging opportunities in automated aerial services.

MARKET SEGMENTATION

This research report on the Europe drone as a service market has been segmented and sub-segmented into the following categories.

By Service Type

- Drone Platform Services

- Piloting and Operations

- Data Analytics

- Data Processing

- Maintenance, Repair and Overhaul (MRO)

- Training and Simulation

By End User Industry

- Construction and Infrastructure

- Agriculture and Forestry

- Energy and Utilities

- Law Enforcement and Public Safety

- Medical and Parcel Delivery

- Others (Mining, Real Estate, Media)

By Drone Type

- Rotary-wing

- Fixed-wing

- Hybrid VTOL

By Operating Range

- Visual Line-of-Sight (VLOS)

- Beyond Visual Line-of-Sight (BVLOS)

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe drone as a service market?

The Europe drone as a service market provides turnkey drone operations for inspection and mapping. Subscription models eliminate capital costs for businesses adopting aerial solutions.

How does the Europe drone as a service market function?

The Europe drone as a service market functions through specialized providers handling flight planning and data analysis. Clients receive actionable insights without managing equipment.

What drives growth in the Europe drone as a service market?

Regulatory harmonization drives the Europe drone as a service market enabling cross-border BVLOS operations. Industry demand for cost-effective aerial monitoring accelerates adoption.

Which applications lead the Europe drone as a service market?

Infrastructure inspection dominates the Europe drone as a service market alongside precision agriculture. Energy utilities leverage drones for tower and pipeline assessments.

What regulations shape the Europe drone as a service market?

EASA standards govern the Europe drone as a service market standardizing BVLOS approvals. GDPR compliance ensures secure handling of aerial data collection.

Which countries lead the Europe drone as a service market?

UK and Germany lead the Europe drone as a service market through advanced infrastructure. Netherlands excels in agricultural drone applications regionally.

What technologies define the Europe drone as a service market?

AI analytics and 5G connectivity define the Europe drone as a service market enabling real-time data processing. Autonomous flight paths improve operational efficiency.

What trends influence the Europe drone as a service market?

Platform services shape the Europe drone as a service market integrating flight operations with cloud analytics. IoT sensors expand monitoring capabilities significantly.

What challenges face the Europe drone as a service market?

Airspace integration challenges the Europe drone as a service market though U-space systems help. Weather limitations impact outdoor inspection reliability.

How does agriculture utilize the Europe drone as a service market?

Precision farming leverages the Europe drone as a service market for crop health monitoring. Multispectral imaging guides variable rate fertilizer applications.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com