Europe Electric Aircraft Market Size, Share, Trends, and Growth Analysis Report, Segmented by Take-off Type, Component, End Use, Platform, and Country – Industry Forecast From 2026 to 2034

Europe Electric Aircraft Market Report Summary

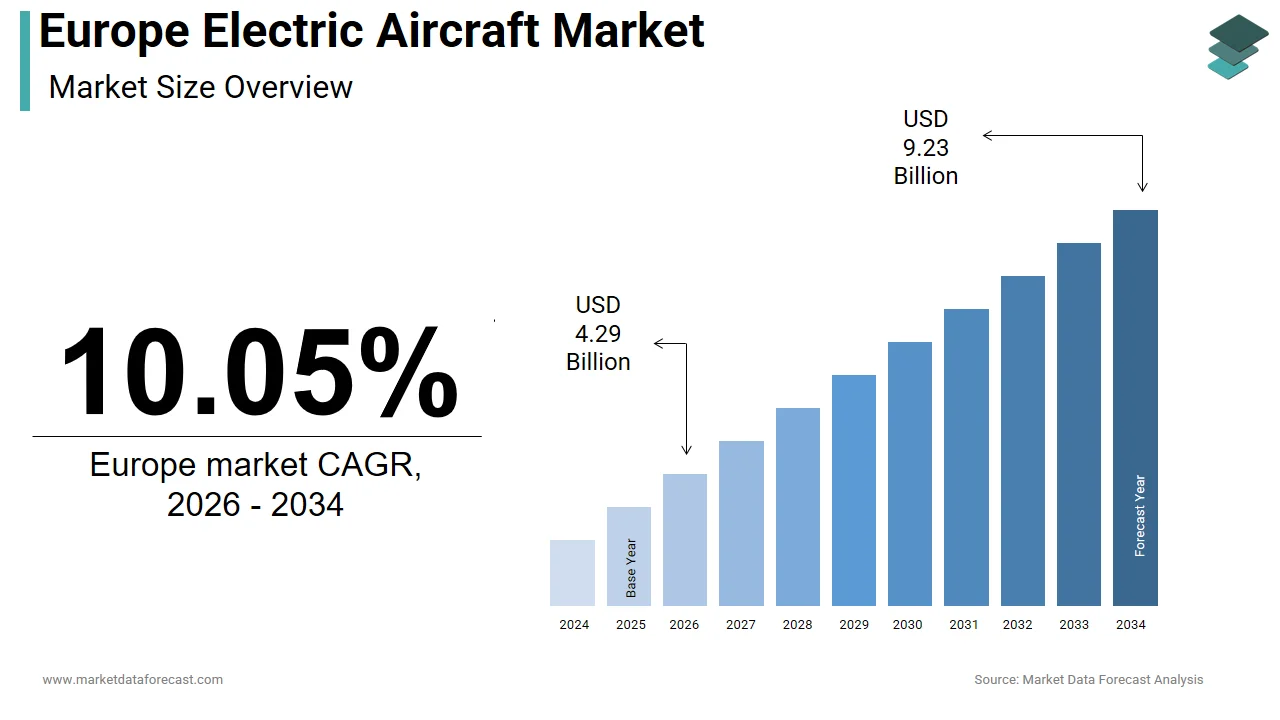

The Europe electric aircraft market was valued at USD 3.90 billion in 2025, is estimated to reach USD 4.29 billion in 2026, and is projected to reach USD 9.23 billion by 2034, growing at a CAGR of 10.05% from 2026 to 2034. Market growth is driven by increasing focus on reducing carbon emissions in aviation, advancements in battery technologies, and strong government support for sustainable aviation initiatives. The push toward zero-emission aircraft, coupled with rising investments in electric propulsion systems and urban air mobility solutions, is accelerating market development. Additionally, collaborations between aerospace companies and technology firms are fostering innovation and the commercialization of electric aircraft across Europe.

Key Market Trends

- Rising demand for zero-emission and sustainable aviation solutions.

- Advancements in battery technology and electric propulsion systems.

- Increasing investments in urban air mobility (UAM) and eVTOL aircraft.

- Strong government support for green aviation initiatives.

- Strategic partnerships between aerospace and technology companies.

Segmental Insights

- Based on take-off type, the conventional take-off and landing segment dominated the Europe electric aircraft market by capturing 46.4% share in 2025, driven by compatibility with existing airport infrastructure.

- Based on component, the batteries segment led the market with 36.3% share in 2025, supported by their critical role in powering electric aircraft systems.

- Based on end use, the commercial segment held the largest share of 64.4% in 2025, driven by increasing adoption in passenger and cargo transport applications.

Regional Insights

The Europe electric aircraft market is witnessing strong growth across key aerospace hubs.

- Germany led the market in 2025 with 23.6% share, driven by strong industrial capabilities and investments in electric aviation technologies.

- France followed as the second-largest market, supported by a state-led aerospace strategy and a robust manufacturing ecosystem.

- The United Kingdom is expected to register a promising CAGR during the forecast period due to advanced research capabilities and supportive regulatory frameworks.

Competitive Landscape

The Europe electric aircraft market is highly dynamic, with a mix of established aerospace giants and emerging electric aviation startups. Market players are focusing on innovation in propulsion systems, battery efficiency, and aircraft design to gain a competitive advantage. Strategic collaborations, pilot projects, and funding initiatives are shaping the competitive landscape.

Prominent companies operating in the Europe electric aircraft market include Lilium, Airbus, Elbit Systems Ltd., ZeroAvia, EHang Holdings Ltd., Heart Aerospace, Wright Electric, Inc., Ampaire Inc., Embraer S.A., AeroVironment, Inc., Eviation, Rolls-Royce plc, Joby Aviation, Volocopter GmbH, Pipistrel d.o.o., and Duxion.

Europe Electric Aircraft Market Size

The Europe electric aircraft market was valued at USD 3.90 billion in 2025, is estimated to reach USD 4.29 billion in 2026, and is projected to reach USD 9.23 billion by 2034, growing at a CAGR of 10.05% from 2026 to 2034.

An electric aircraft is an aviation platform powered by electric propulsion systems, including battery electric, hybrid electric, and hydrogen fuel cell configurations. This sector represents a pivotal shift from conventional fossil fuel dependency toward sustainable aerial mobility solutions across short-haul, regional, and urban air mobility segments. The strategic imperative for this transition is deeply rooted in the European Union’s aggressive climate neutrality goals, which mandate substantial reductions in greenhouse gas emissions across all transport modes. Aviation currently accounts for approximately 3% of total European Union carbon dioxide emissions, as per the European Environment Agency. Furthermore, the International Civil Aviation Organization states that international aviation emissions could triple by 2050 if no action is taken. In response, the European Commission has outlined the Flightpath 2050 vision, which aims for a 75% reduction in carbon dioxide emissions per passenger-kilometer compared to 2000 levels. The regulatory landscape is further shaped by the ReFuelEU Aviation initiative, which mandates increasing shares of sustainable aviation fuels yet explicitly supports technological innovation in zero-emission aircraft. According to Eurocontrol, air traffic movements in Europe reached 9.9 million flights in 2023, indicating a robust recovery post pandemic and underscoring the urgent need for scalable decarbonization technologies. The integration of electric propulsion offers a viable pathway to meet these stringent environmental targets while maintaining the connectivity essential for the European single market.

MARKET DRIVERS

Stringent Environmental Regulations and Carbon Neutrality Mandates

The rigorous regulatory framework enforced by the European Union aimed at achieving climate neutrality by 2050 is primarily driving the growth of the Europe electric aircraft market. The European Green Deal serves as the overarching policy driver compelling the aviation sector to drastically reduce its carbon footprint. According to the European Commission, the Fit for 55 package includes specific measures to reduce net greenhouse gas emissions by at least 55% by 2030 compared to 1990 levels. This legislative pressure translates into direct operational constraints for traditional airlines, thereby accelerating investment in zero-emission technologies. The ReFuelEU Aviation regulation mandates that 2% of fuel supplied at European Union airports must be sustainable by 2025, rising to 70% by 2050. While sustainable aviation fuels are part of the solution, they do not eliminate non-carbon dioxide effects such as contrails and nitrogen oxides. Electric aircraft offer a complete elimination of tailpipe emissions during flight. As per the European Environment Agency, aviation contributed 13% of total transport-related greenhouse gas emissions in the European Union in 2022. The inability of conventional jet fuel to meet long-term sustainability criteria forces manufacturers and operators to explore electric alternatives. Additionally, the European Union Emissions Trading System imposes a cost on carbon emissions, making electric propulsion increasingly economically attractive. The regulatory certainty provided by these mandates reduces risks in investment in electric aircraft development, ensuring sustained market growth driven by compliance rather than mere voluntary adoption.

Rising Urbanization and Demand for Urban Air Mobility Solutions

The rapid urbanization across Europe, coupled with increasing congestion in major metropolitan areas, which creates a fertile ground for urban air mobility solutions, is further fuelling the Europe electric aircraft market expansion. According to Eurostat, 75% of the European Union population lived in urban areas in 2023, a figure projected to rise significantly by 2050. This demographic shift intensifies pressure on existing ground transportation infrastructure, leading to severe traffic congestion and prolonged commute times. Electric vertical takeoff and landing aircraft present a viable solution for intra-city and inter-city connectivity, offering faster travel times without the need for extensive runway infrastructure. The European Institute of Innovation and Technology notes that urban air mobility could reduce travel time by up to 70% for certain routes in densely populated areas. Cities such as Paris, London, and Berlin are actively exploring air taxi services to alleviate ground traffic. The demand for point-to-point air travel within regions is growing as business travelers and tourists seek efficient alternatives to high-speed rail and road transport. According to the European Union Aviation Safety Agency, over 100 urban air mobility projects are currently underway in Europe, indicating strong stakeholder interest. The ability of electric aircraft to operate quietly and with zero local emissions makes them suitable for urban environments where noise pollution and air quality are critical concerns. This convergence of demographic trends and technological capability drives substantial investment in electric aircraft tailored for short-distance urban operations.

MARKET RESTRAINTS

Limitations in Battery Energy Density and Range Constraints

A major restraint hindering the widespread adoption of electric aircraft in Europe is the current limitation in battery energy density, which directly impacts flight range and payload capacity. Contemporary lithium-ion batteries possess an energy density of approximately 250 to 300 watt-hours per kilogram, whereas conventional jet fuel offers around 12000 watt-hours per kilogram, as per the National Aeronautics and Space Administration. This disparity means that electric aircraft require significantly heavier power sources to achieve comparable performance, limiting their viability to short-haul routes. For regional flights exceeding 500 kilometers, the weight penalty becomes prohibitive, reducing the number of passengers or cargo that can be carried. The European Battery Alliance acknowledges that while battery technology is improving, annual improvements of 5% to 8% are insufficient to match the energy requirements of long-haul aviation in the near term. Current electric aircraft prototypes, such as those developed by Heart Aerospace, target ranges of 400 kilometers with reserves, which restricts their operational utility to niche regional markets. The lack of breakthroughs in solid-state battery commercialization further delays the potential for extended-range electric flight. According to the International Energy Agency, battery electric aircraft are currently limited to very short flights, typically under 200 kilometers for practical commercial operations. This technological bottleneck prevents electric aircraft from competing with turboprop and jet aircraft on most European routes, thereby constraining market penetration. Until energy density improves substantially, the economic case for electric aviation remains weak for all but the shortest distances.

High Initial Capital Expenditure and Infrastructure Deficits

The substantial initial capital expenditure required for both aircraft acquisition and the development of supporting charging infrastructure is further hampering the expansion of the Europe electric aircraft market. Electric aircraft involve novel materials and complex propulsion systems that result in higher manufacturing costs compared to mature conventional aircraft designs. According to the European Commission, the transition to zero-emission aviation requires estimated investments of hundreds of billions of euros by 2050. A significant portion of this cost is attributed to the establishment of high-power charging networks at airports. Most European airports currently lack the electrical grid capacity to support simultaneous charging of multiple electric aircraft, particularly during peak hours. Upgrading grid infrastructure involves considerable time and financial outlay. According to various airport infrastructure studies, the average cost of installing a high-power charging station at an airport can exceed 500,000 euros, depending on grid connection requirements. Furthermore, the uncertainty regarding residual values of electric aircraft due to rapid technological obsolescence discourages leasing companies and airlines from making large upfront investments. The absence of standardized charging interfaces across different manufacturers adds to the complexity and cost of infrastructure deployment. Small regional airports, which are primary candidates for early electric aircraft adoption, often face budgetary constraints that limit their ability to invest in necessary upgrades. This financial barrier slows down the rollout of electric aviation services, creating a chicken-and-egg situation where limited infrastructure discourages aircraft procurement and vice versa.

MARKET OPPORTUNITIES

Integration of Advanced Air Mobility into Existing Airspace

The integration of advanced air mobility vehicles into the existing European airspace management framework through the Single European Sky ATM Research program is a promising opportunity for the Europe electric aircraft market. The modernization of air traffic management systems enables the safe and efficient handling of a high volume of low-altitude flights characteristic of electric vertical takeoff and landing operations. According to the European Union Aviation Safety Agency, the implementation of U-space regulations provides a structured framework for unmanned aircraft systems, facilitating the entry of electric air taxis into commercial service. This regulatory clarity opens new revenue streams for operators targeting urban and suburban connectivity. The European Commission estimates that the urban air mobility market could reach 4 billion euros by 2035 in Europe. By leveraging digital twin technologies and artificial intelligence for traffic management, stakeholders can optimize flight paths and reduce congestion. This integration allows electric aircraft to serve underserved regions, improving regional connectivity without the environmental impact of traditional aviation. Companies such as Volocopter and Lilium are partnering with city authorities to establish vertiports, demonstrating the feasibility of integrated operations. The opportunity extends to emergency medical services, cargo delivery, and surveillance, where electric aircraft offer cost-effective and rapid response capabilities. According to the European Organisation for the Safety of Air Navigation, the digitization of air traffic services will support a significant increase in drone and electric aircraft flights by 2030. This scalable infrastructure creates a robust ecosystem for electric aircraft proliferation.

Strategic Partnerships and Cross-Sector Collaborations

Another vital opportunity emerges from strategic partnerships between aerospace manufacturers, energy providers, and technology firms, which accelerate innovation and risk sharing. The complexity of electric aircraft development necessitates cross-sector collaboration to address challenges in battery technology, software integration, and supply chain resilience. According to the Clean Aviation Joint Undertaking, public-private partnerships have mobilized over 4 billion euros in total research and innovation funding for next-generation aircraft technologies. These collaborations facilitate the transfer of expertise from the automotive sector, where electric vehicle technology is more mature, to the aviation industry. For instance, partnerships between Airbus and various battery manufacturers aim to develop high-energy-density cells specifically for aviation applications. Such alliances reduce development timelines and costs, enabling faster commercialization. The European Battery Alliance fosters cooperation across the value chain, ensuring a secure supply of critical raw materials. According to the European Commission, billions of euros are supported under the Horizon Europe program, focusing on sustainable aviation technologies. These initiatives create a conducive environment for startups and established players to co-develop solutions. Furthermore, collaborations with renewable energy providers ensure that electric aircraft are charged using green electricity, maximizing their environmental benefits. This synergistic approach strengthens the European position in the global electric aviation market and drives technological leadership.

MARKET CHALLENGES

Certification and Regulatory Standardization Hurdles

A primary challenge facing the Europe electric aircraft market is the complex and evolving certification process for novel propulsion systems and aircraft configurations. The European Union Aviation Safety Agency must establish new standards for electric propulsion, batteries, and software-intensive systems, which differ significantly from conventional aviation regulations. According to the European Union Aviation Safety Agency, certifying a new aircraft type is a multi-year process that can cost hundreds of millions of euros. The lack of precedents for electric vertical take-off and landing aircraft creates uncertainty for manufacturers regarding compliance requirements. Each innovative design may require bespoke certification pathways, delaying market entry. The safety assessment of high-voltage systems and thermal runaway risks in batteries adds layers of complexity to the approval process. According to the International Air Transport Association, regulatory harmonization across different jurisdictions remains incomplete, causing additional burdens for manufacturers seeking global market access. The dynamic nature of electric aircraft technology means that regulations must continuously adapt, potentially leading to retroactive compliance costs. Manufacturers face the challenge of designing aircraft that meet current standards while anticipating future regulatory changes. This uncertainty increases development risks and deters investment. The need for specialized testing facilities and expertise further complicates the certification landscape. Until a stable and predictable regulatory framework is fully established, the pace of commercial deployment will remain constrained by procedural delays.

Supply Chain Vulnerabilities for Critical Raw Materials

The vulnerability of the supply chain for critical raw materials essential for electric aircraft production, particularly lithium, cobalt, and nickel, is further challenging the growth of the Europe electric aircraft market. Europe relies heavily on imports for these materials, with limited domestic extraction and processing capabilities. According to the European Commission, the European Union imports 97% of its magnesium and 100% of its heavy rare earth elements. This dependency exposes manufacturers to geopolitical risks, price volatility, and potential supply disruptions. The increasing global demand for electric vehicles and energy storage systems competes for the same raw materials, driving up costs and creating shortages. The Critical Raw Materials Act aims to reduce dependency, but full implementation will take years. According to the International Energy Agency, the demand for lithium could increase significantly by 2040, straining existing supply chains. Ethical sourcing and environmental standards further complicate procurement processes. Manufacturers must ensure that their supply chains comply with strict European Union sustainability criteria, adding administrative and financial burdens. The concentration of processing capabilities in a few countries outside Europe creates strategic vulnerabilities. Any disruption in these supply chains can halt production lines and delay deliveries. Securing a resilient and sustainable supply of critical materials remains a formidable challenge for the Europe electric aircraft market, requiring diversified sourcing strategies and investment in recycling technologies.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Take-off Type, Component, End Use, Platform, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Lilium, Airbus, Elbit Systems Ltd., ZeroAvia, EHang Holdings Ltd., Heart Aerospace, Wright Electric, Inc., Ampaire Inc., Embraer SA, AeroVironment, Inc., Eviation, Rolls-Royce Plc, Joby Aviation, VOLOCOPTER GMBH, PIPISTREL d.o.o., Duxion. |

SEGMENTAL ANALYSIS

By Take-off Type Insights

The conventional take-off and landing segment dominated the market by accounting for46.4% of the regional market share in 2025. This dominance is primarily driven by the compatibility of this configuration with existing airport infrastructure, which minimizes the need for costly capital expenditures on new facilities. The primary factor driving the dominance of conventional takeoff and landing electric aircraft is their seamless integration into the current aviation ecosystem. Unlike vertical or short takeoff variants, these aircraft utilize standard runways, taxiways, and gate structures that are already present at thousands of airports across Europe. According to Eurocontrol, there are over 500 certified commercial airports in the European Union, many of which have capacity for regional operations. This existing infrastructure significantly lowers the barrier to entry for airlines adopting electric propulsion, as they do not need to invest in specialized vertiports or reinforced pads. The European Commission notes that using existing regional airports for electric operations is more cost-effective than building new vertical takeoff facilities. Furthermore, pilots require minimal retraining to operate conventional electric aircraft, as the flight dynamics during takeoff and landing remain similar to traditional turboprops. According to the European Union Aviation Safety Agency, certification processes for conventional configurations can leverage established frameworks, reducing regulatory uncertainty. This operational familiarity encourages regional carriers to pilot electric conversions for short-haul routes. The ability to leverage ground handling equipment, maintenance hangars, and air traffic control procedures without modification ensures a smoother transition. Consequently, the lower operational disruption and capital risk make conventional takeoff and landing the preferred choice for initial market penetration in the European regional aviation sector.

However, the vertical takeoff and landing segment is another major segment and is estimated to grow at a CAGR of 27.7% of the European market over the forecast period. The exponential growth of the vertical takeoff and landing segment is primarily attributed to the escalating demand for urban air mobility to alleviate severe traffic congestion in major European cities. According to Eurostat, urban areas in Europe are expected to house over 80% of the population by 2050, intensifying the strain on ground transportation networks. Vertical takeoff and landing aircraft offer a transformative solution by utilizing the third dimension for transport, thereby bypassing road bottlenecks. According to the projections of the European Institute of Innovation and Technology, urban air mobility could create thousands of jobs and significant economic value by 2035. Cities like Paris, London, and Munich are actively developing vertiport networks to support this emerging mode of transport. According to the European Union Aviation Safety Agency, numerous urban air mobility trials have been conducted in Europe, demonstrating technical feasibility and public acceptance. The ability of these aircraft to operate from rooftops, parking garages, and small open spaces eliminates the need for large land acquisitions. This flexibility appeals to real estate developers and city planners seeking to enhance connectivity without expanding physical infrastructure. Furthermore, the tourism sector in Europe is increasingly adopting air taxis for scenic tours and premium transfers, creating a lucrative early revenue stream. According to various tourism research groups, luxury travel segments are growing steadily, providing a viable customer base for high-cost initial services. This robust demand pipeline drives aggressive investment and fleet expansion among vertical takeoff and landing operators.

By Component Insights

The batteries segment accounted for the leading share of 36.3% of the European market in 2025. The leading position of batteries segment in the European market is attributed to the critical role batteries play in determining aircraft performance, and the high cost associated with advanced aviation-grade energy storage systems. Aviation-grade lithium-ion batteries require rigorous safety standards, including thermal management systems and redundant cell architectures to prevent catastrophic failures. According to the European Battery Alliance, the cost of high-performance aviation batteries is significantly higher than that of automotive batteries due to lower production volumes and more stringent quality controls. Each electric aircraft requires multiple battery packs to ensure sufficient range and power density, further amplifying the segment value. According to the International Energy Agency, battery systems account for a large portion of the empty weight of current electric aircraft prototypes, making them the most critical and expensive component. The need for continuous innovation to improve energy density while maintaining safety drives substantial research and development expenditure. Manufacturers must source specialized cells from limited suppliers capable of meeting aviation certifications. According to the European Commission, the supply chain for critical battery materials is a strategic priority, adding to procurement focus. Furthermore, the replacement cycle for aviation batteries is shorter than for structural components due to degradation from high discharge rates. This recurring revenue stream sustains the market dominance of the battery segment. According to industry analysis, the aftermarket for battery maintenance and replacement in electric aviation is expected to grow significantly, reinforcing the segment's leading financial contribution.

On the other hand, the electric motors segment is anticipated to register the highest CAGR of 27.1% over the forecast period. The electric motors segment is experiencing rapid growth due to significant technological advancements in power density and operational efficiency, which are essential for viable electric flight. Modern axial flux and radial flux motors are achieving high power densities, a critical threshold for practical aviation applications. According to the European Space Agency, developments in superconducting materials and lightweight magnetic alloys have enabled motors to deliver higher torque with reduced weight. This improvement allows aircraft designers to integrate multiple motors into distributed propulsion systems, enhancing aerodynamic efficiency and redundancy. According to the Institute of Electrical and Electronics Engineers, the efficiency of advanced electric motors is extremely high, minimizing energy loss during conversion. This high efficiency is vital for maximizing the limited energy stored in batteries. The shift towards advanced cooling systems further reduces maintenance requirements and improves reliability. According to various aviation research networks, investment in motor cooling technologies has increased steadily. These innovations enable the design of quieter and more compact propulsion units suitable for urban air mobility vehicles. The ability to scale motor size for different aircraft classes, from small drones to regional airliners, expands the addressable market. According to the International Council on Clean Transportation, the adoption of high-power-density motors is expected to significantly increase the capability of electric aircraft by 2030. This technological progress drives strong demand for specialized electric motors across the European aviation sector.

By End Use Insights

The commercial segment dominated the market by commanding for 64.4% of the regional market share in 2025. The dominance of the commercial segment in the European market is driven by the intense pressure on commercial airlines to reduce operating costs and comply with stringent environmental regulations. The dominance of the commercial segment is primarily driven by the compelling economic case for electric propulsion in reducing operating costs and eliminating fuel dependency for short-haul flights. Fuel accounts for a significant portion of airline operating expenses, according to the International Air Transport Association. Electric aircraft offer lower energy costs per flight hour as electricity is often cheaper and more price stable than jet fuel. According to the European Commission, the price of aviation fuel in Europe can be volatile, creating financial uncertainty for carriers. Electric propulsion mitigates this volatility, providing predictable operating expenses. Additionally, electric motors have fewer moving parts than turbine engines, resulting in lower maintenance costs. According to leading engine manufacturers, maintenance costs for electric propulsion systems can be significantly lower than for conventional gas turbines. This cost advantage is particularly attractive for regional airlines operating high-frequency short-haul routes where turnaround times are critical. The ability to charge aircraft overnight using off peak electricity further enhances economic efficiency. According to Eurocontrol, short regional flights constitute a large portion of all European flights, representing a vast addressable market for cost-effective electric solutions. Airlines such as SAS and KLM have announced initiatives for electric regional flights to test these economic benefits. The combination of lower fuel and maintenance costs creates a strong business case for commercial operators to adopt electric aircraft, thereby driving the segment's market leadership.

However, the military segment is projected to be the fastest-growing end-use sector and record a CAGR of 23.9% over the forecast period in the European market. The military segment is growing rapidly due to the strategic imperative for stealth capabilities and reduced acoustic signatures in modern defense operations. Electric propulsion systems are inherently quieter than combustion engines, providing a significant tactical advantage for surveillance and special operations missions. According to the European Defence Agency, low-observable platforms are critical for penetrating contested airspace. Electric aircraft produce minimal heat signatures and noise, making them ideal for intelligence, surveillance, and reconnaissance roles. According to the North Atlantic Treaty Organization, recent exercises have highlighted the effectiveness of silent unmanned systems in gathering real-time battlefield data. The European Union Permanent Structured Cooperation framework has prioritized the development of unmanned electric systems for various security roles. Countries such as France and Germany are investing in electric vertical takeoff and landing drones for troop logistics and medical evacuation in hostile environments. According to the Stockholm International Peace Research Institute, European military spending on unmanned aerial systems has seen steady increases. The ability to operate from unprepared surfaces without revealing position enhances mission flexibility. Furthermore, electric propulsion reduces the logistical burden of fuel transport in forward operating bases. According to the European Defence Fund, several projects focused on hybrid electric propulsion for tactical aircraft have received significant funding. These strategic advantages drive robust demand for electric military aircraft across European armed forces.

COUNTRY LEVEL ANALYSIS

Germany Electric Aircraft Market Analysis

Germany held the leading position in the Europe electric aircraft market with 23.6% of the regional market share in 2025 due to its robust aerospace industry and strong government support for green technologies. The country is home to major aerospace manufacturers and a vibrant startup ecosystem focused on electric propulsion. According to the German Aerospace Center, the national government has allocated over 1 billion euros for research into sustainable aviation technologies, including electric aircraft. Bavaria and Baden-Württemberg have emerged as hubs for electric aviation innovation, hosting companies such as Lilium and Volocopter. The German Federal Ministry for Economic Affairs and Climate Action supports these initiatives through various funding programs, which prioritize zero-emission flight technologies. According to the German Industry Association for Aerospace, the country accounts for a significant portion of all European patents filed for electric aviation technologies. The presence of world-class engineering talent and research institutions, such as the Technical University of Munich, accelerates technological breakthroughs. Germany’s strong automotive sector also contributes expertise in battery technology and electric motors, facilitating cross-industry collaboration. According to Eurostat, Germany has one of the highest numbers of registered electric vehicle charging stations in Europe, providing a foundation for aviation charging infrastructure. The country’s commitment to energy transition policies aligns with the decarbonization of aviation, creating a favorable regulatory environment. Furthermore, major airports such as Frankfurt and Munich are piloting electric ground support equipment, paving the way for aircraft electrification. This combination of industrial strength, policy support, and technological leadership solidifies Germany’s dominant market position.

France Electric Aircraft Market Analysis

France occupied the second largest share of the Europe electric aircraft market due to its state-led aerospace strategy and strong industrial base. The country leverages its position as a global aerospace leader to drive electric aviation innovation through strategic public-private partnerships. According to the French Ministry of Ecological Transition, the France 2030 investment plan includes 1.5 billion euros specifically for decarbonizing aviation. Airbus, headquartered in Toulouse, plays a pivotal role in developing hybrid and electric aircraft concepts. The French government supports these efforts through the Directorate General for Civil Aviation, which facilitates regulatory sandboxes for testing new technologies. According to the French Aerospace Industries Association, the sector employs hundreds of thousands of people, many of whom are engaged in research and development for sustainable flight. France is also home to innovative startups developing hybrid electric regional aircraft. The country’s strong energy sector provides a reliable source of low-carbon electricity essential for charging electric aircraft. According to Réseau de Transport d’Électricité, France generates a majority of its electricity from nuclear power, ensuring a low-carbon grid for aviation. The French Air and Space Force is actively exploring electric drones for surveillance, enhancing military demand. Furthermore, the Paris region is preparing for urban air mobility services. This strategic alignment of industrial capability, energy policy, and government funding maintains France’s strong market standing.

United Kingdom Electric Aircraft Market Analysis

The United Kingdom is estimated to account for a promising share of the Europe electric aircraft market during the forecast period, owing to its advanced research capabilities and a supportive regulatory framework for innovation. Despite leaving the European Union, the UK remains a key player in electric aviation through its Jet Zero Strategy and strong academic institutions. According to the UK Department for Transport, the Jet Zero Council brings together government and industry to accelerate the development of zero-emission flight technologies. The UK government has committed significant investment, including up to £2.3 billion through the Aerospace Technology Institute (ATI) from 2025 to 2035, focusing on zero-carbon propulsion systems. Companies such as Rolls-Royce and BAE Systems are leading developments in electric motor technology and hybrid-electric architectures. As per the UK Civil Aviation Authority, the country has established a regulatory sandbox allowing for faster testing and certification of novel aircraft designs. The presence of world-renowned universities such as Imperial College London and Cranfield University fosters cutting-edge research in battery chemistry and aerodynamics. According to industry reports, the UK aerospace and defense market was valued at $28.7 billion in 2024, maintaining its competitive edge through continuous R&D. The country’s island geography makes it ideal for testing short-haul electric flights between the mainland and islands. Furthermore, the UK is investing in vertiport infrastructure in London and other major cities. This combination of research excellence, regulatory agility, and strategic investment sustains the UK’s prominent market position.

Sweden Electric Aircraft Market Analysis

Sweden is anticipated to hold a notable share of the Europe electric aircraft market during the forecast period, owing to its ambitious climate goals and pioneering electric aviation startups. The country is home to Heart Aerospace, a leading developer of regional electric aircraft that has secured substantial orders from major airlines. According to the Swedish Energy Agency, the government aims to achieve fossil-free domestic aviation by 2030, which is one of the most aggressive targets globally. This policy drive creates a strong domestic market for electric aircraft and stimulates innovation. Sweden’s abundant hydroelectric and wind power resources provide a clean energy grid essential for true zero-emission flight; in 2025, 99% of Sweden's electricity was generated from low-carbon sources. The Swedish Transport Administration is actively working on integrating electric aircraft into the national transport network, including planning for charging infrastructure at regional airports. Companies such as SAS have partnered with Heart Aerospace to pilot electric flights on domestic routes. The Swedish Innovation Agency, Vinnova, provides funding for research projects focused on sustainable aviation technologies. According to the Swedish Aerospace Industries Association, the sector has shown resilient growth, with aerospace exports reaching $1.1 billion in 2023. The country’s strong engineering tradition and commitment to sustainability attract international investment and talent. Furthermore, Sweden participates in Nordic collaborations to harmonize regulations for electric aviation. This supportive ecosystem of policy, resources, and innovation positions Sweden as a key market leader.

Spain Electric Aircraft Market Analysis

Spain is expected to exhibit a healthy CAGR in the Europe electric aircraft market over the forecast period. The growing aerospace cluster and favorable weather conditions for flight testing are propelling the Spanish market expansion. The country is emerging as a hub for electric aviation manufacturing and maintenance, leveraging its existing aerospace infrastructure. According to the Spanish Ministry of Industry, Trade, and Tourism, the PERTE Aerospace program aims to transform the sector toward sustainability with investments exceeding €1.5 billion. Spain is home to major aerospace suppliers such as Airbus Defence and Space, which are expanding their capabilities in electric propulsion components. The country’s sunny climate and extensive coastline provide ideal conditions for testing electric vertical takeoff and landing (eVTOL) aircraft and drones. As per the Spanish State Aviation Safety Agency, several projects for urban air mobility are underway in Madrid and Barcelona. The Spanish government is promoting the development of vertiports and charging infrastructure to support these initiatives. Tourism is a key driver for electric aviation in Spain, with potential applications for scenic flights and inter-island connectivity in the Balearic and Canary Islands. The aerospace sector is a significant employer, with companies like Airbus maintaining major sites in Getafe, Seville, and Albacete. Collaborations with European partners facilitate knowledge transfer and market access. Furthermore, Spain’s strategic location serves as a gateway for electric aviation technologies entering the European market from other regions. This combination of industrial capacity, favorable geography, and government support drives Spain’s growing market presence.

COMPETITIVE LANDSCAPE

The competition in the Europe electric aircraft market is characterized by intense rivalry among established aerospace giants, innovative startups, and technology specialists. Established players leverage their extensive resources, manufacturing capabilities, and regulatory experience to maintain leadership positions. They often engage in mergers and acquisitions to absorb emerging technologies and talent. Startups contribute agility and disruptive innovation, focusing on niche segments such as urban air mobility and regional electric flight. These smaller entities frequently secure venture capital and strategic investments to fund development. The competitive landscape is further shaped by cross-industry collaborations where automotive and energy companies enter the aviation sector. This convergence brings new expertise in battery technology and mass production. Regulatory compliance serves as a significant barrier to entry, favoring companies with strong relationships with aviation authorities. Intellectual property protection is critical as firms race to patent advanced propulsion systems and materials. Price competition remains limited due to the early stage of commercialization, but cost efficiency will become increasingly important. Differentiation through safety records, operational range, and passenger experience drives competitive advantage. The market is dynamic, with frequent announcements of partnerships and technological breakthroughs reshaping the competitive hierarchy continuously.

KEY MARKET PLAYERS

The leading companies operating in the Europe electric aircraft market include:

- Lilium

- Airbus

- Elbit Systems Ltd.

- ZeroAvia

- EHang Holdings Ltd.

- Heart Aerospace

- Wright Electric, Inc.

- Ampaire Inc.

- Embraer S.A.

- AeroVironment, Inc.

- Eviation

- Rolls-Royce plc

- Joby Aviation

- Volocopter GmbH

- Pipistrel d.o.o.

- Duxion

TOP PLAYERS IN THE MARKET

- Airbus SE stands as a pivotal force in the European electric aircraft landscape, leveraging its extensive aerospace expertise to pioneer sustainable aviation solutions. The company actively develops hybrid electric and fully electric propulsion systems through its ZeroE initiative, which aims to launch the world’s first zero-emission commercial aircraft by 2035. Airbus collaborates with various technology partners to integrate hydrogen fuel cell and battery electric technologies into regional and short-haul aircraft designs. Recent actions include successful flight tests of its E Fan X hybrid electric demonstrator and ongoing partnerships with engine manufacturers to optimize electric powertrains. By investing heavily in research and development, Airbus strengthens its position as a leader in next-generation aviation. The company also engages in regulatory discussions to shape certification standards for electric aircraft, ensuring a smoother path to commercialization. Its comprehensive approach combines technological innovation with strategic alliances to accelerate the transition toward sustainable air travel across Europe and globally.

- Heart Aerospace is a prominent Swedish startup specializing in the development of regional electric aircraft designed for short-haul routes. The company’s ES 30 aircraft features a hybrid electric propulsion system that offers significant range flexibility while reducing emissions and operating costs. Heart Aerospace has secured substantial orders and letters of intent from major airlines such as United Airlines and SAS, demonstrating strong market confidence in its technology. Recent actions include advancing the design phase of the ES 30 and establishing manufacturing partnerships to scale production capabilities. The company focuses on creating a viable business case for regional electric aviation by targeting routes under 400 kilometers. Heart Aerospace actively collaborates with airport authorities to develop the necessary charging infrastructure. By prioritizing practical operational requirements and environmental sustainability, Heart Aerospace contributes significantly to the decarbonization of regional air travel. Its innovative approach addresses both economic and ecological challenges, positioning it as a key player in the emerging electric aviation sector.

- Volocopter GmbH is a leading German developer of electric vertical takeoff and landing aircraft focused on urban air mobility solutions. The company’s VoloCity air taxi is designed for safe, quiet, and emission-free inner-city flights. Volocopter has conducted numerous successful flight trials in major European cities, including Paris, Helsinki, and Rome, showcasing the feasibility of its technology. Recent actions include achieving critical certification milestones with the European Union Aviation Safety Agency and partnering with local authorities to establish vertiport networks. The company collaborates with infrastructure providers to ensure seamless integration of air taxis into existing urban transport systems. Volocopter also engages in public awareness campaigns to build acceptance for urban air mobility. By focusing on safety, reliability, and user experience, Volocopter aims to revolutionize urban transportation. Its strategic partnerships and regulatory progress strengthen its market position as a pioneer in the electric vertical takeoff and landing segment, contributing to the broader adoption of sustainable aerial mobility in Europe.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe electric aircraft market primarily employ strategic partnerships and collaborations to accelerate technology development and mitigate financial risks. Companies frequently join forces with battery manufacturers, software developers, and infrastructure providers to create integrated solutions. Another major strategy involves securing government funding and grants to support research and development efforts. Many firms actively participate in public-private partnerships to leverage state resources and expertise. Regulatory engagement is also crucial as companies work closely with aviation authorities to shape certification standards for novel aircraft types. Additionally, key participants focus on pilot programs and demonstration projects to validate technology and build customer confidence. These initiatives help showcase operational viability and attract potential investors. Diversification of supply chains is another common strategy to ensure resilience against material shortages. Companies also invest in talent acquisition to secure specialized engineering skills. Finally, many players pursue international expansion to access broader markets and share development costs across regions.

MARKET SEGMENTATION

This research report on the Europe electric aircraft market has been segmented and sub-segmented into the following categories.

By Take-off Type

- Conventional Takeoff and Landing

- Short Takeoff and Landing

- Vertical Takeoff and Landing

By Component

- Batteries

- Electric Motors

- Aerostructures

- Avionics

- Others

By End Use

- Commercial

- Military

By Platform

- Fixed Wing

- Rotary Wing

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com