Europe Garden Seed Market Size, Share, Trends, and Growth Analysis Report, Segmented by Type, Form, End Use, Distribution Channel, and Country – Industry Forecast From 2026 to 2034

Europe Garden Seed Market Report Summary

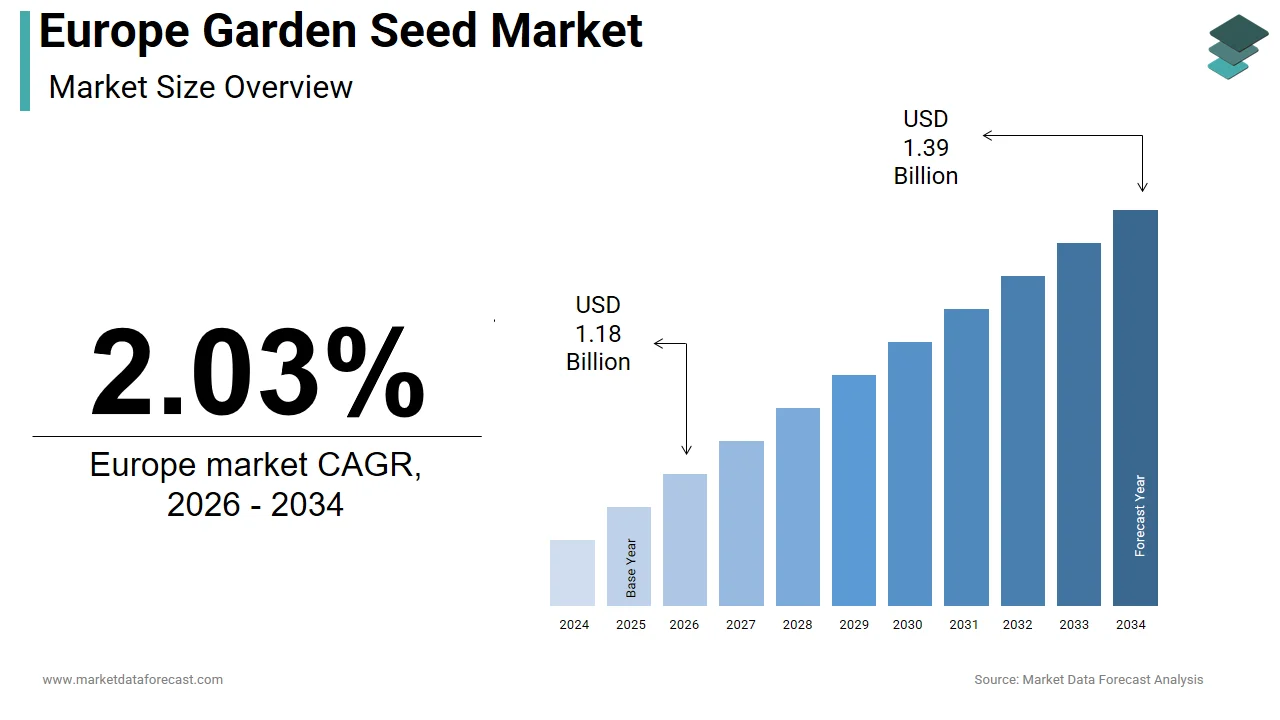

The Europe garden seed market was valued at USD 1.16 billion in 2025, is estimated to reach USD 1.18 billion in 2026, and is projected to reach USD 1.39 billion by 2034, growing at a CAGR of 2.03% from 2026 to 2034. The market is experiencing steady growth, driven by increasing interest in home gardening, organic produce cultivation, and sustainable living practices. The rising popularity of urban gardening, kitchen gardens, and hobby farming is contributing to demand. Additionally, growing awareness about healthy eating habits and locally sourced food is further supporting market expansion across Europe.

Key Market Trends

- Increasing adoption of home gardening and urban farming.

- Rising demand for organic and non-GMO seeds.

- Growing consumer focus on healthy and locally grown food.

- Expansion of hobby gardening and landscaping activities.

- Increasing availability through retail and online channels.

Segmental Insights

- Based on type, the vegetable seeds segment dominated the Europe garden seed market by capturing 45.3% share in 2025, driven by demand for home-grown food.

- Based on distribution channel, the retail stores segment led the market with 55.4% share in 2025, supported by easy accessibility and wide product availability.

Regional Insights

The Europe garden seed market shows steady growth across key countries with strong gardening culture.

- Germany led the market in 2025 with 20.4% share, driven by a well-established gardening culture and consumer interest in sustainability.

- The United Kingdom followed with 18.2% share, supported by high adoption of home gardening and landscaping trends.

- France is expected to witness the fastest growth due to its strong culinary traditions and increasing interest in organic farming.

Competitive Landscape

The Europe garden seed market is moderately competitive, with companies focusing on product quality, organic seed varieties, and expanding distribution networks. Innovation in hybrid seeds and sustainable agricultural practices is shaping competition.

Prominent companies operating in the Europe garden seed market include Bayer Crop Science, Syngenta, Monsanto, Sakata Seed Corporation, Burgess Seed & Plant Co., Johnny's Selected Seeds, Harris Seeds, Enza Zaden, Renee's Garden Seeds, and Seeds of Change.

Europe Garden Seed Market Size

The size of the Europe garden seed market was worth USD 1.16 billion in 2025. The regional market is anticipated to grow at a CAGR of 2.03% from 2026 to 2034 and be worth USD 1.39 billion by 2034 from USD 1.18 billion in 2026.

The garden seed is the breeding, production, and distribution of seeds intended for non-commercial horticultural use, including vegetables, ornamentals, herbs, and fruits for home gardens, balconies, and community plots. As per Eurostat data from 2024, approximately 52% of households in the European Union engaged in gardening activities, with a significant portion dedicating space to edible plants. This widespread participation underscores the cultural and economic significance of home gardening across the continent. According to the Food and Agriculture Organization of the United Nations, urban and peri-urban agriculture contributes to food security and mental well-being for millions of Europeans. The European Commission’s Biodiversity Strategy for 2030 emphasizes the importance of diverse plant genetics, encouraging the cultivation of native and resilient species. Climate change adaptation has also influenced seed selection, with growers seeking drought-resistant and heat-tolerant varieties. Regulatory frameworks such as the European Union’s Organic Regulation strictly govern the labeling and certification of organic seeds, ensuring transparency for consumers. This landscape defines a market driven by environmental consciousness, health awareness, and the desire for self-sufficiency in an increasingly urbanized society.

MARKET DRIVERS

Rising Urbanization and Demand for Home-Grown Produce

The accelerating trend of urbanization, coupled with a growing desire for self-sufficiency and food security, is driving the growth of Europe garden seed market. As more Europeans reside in cities with limited access to fresh produce, many turn to balcony containers and vertical gardening to cultivate their own food. As per the European Environment Agency, over 75% of the EU population lives in urban areas, creating a substantial base for compact gardening solutions. The pandemic accelerated this trend with many individuals discovering the therapeutic and practical benefits of growing vegetables and herbs at home. Consumers are particularly interested in high-value crops such as tomatoes, peppers, and leafy greens, which offer immediate gratification and nutritional benefits. The rise of microgreens and sprouting seeds further caters to space-constrained environments requiring minimal soil and light. Government initiatives promoting green cities and urban farming provide additional impetus. For instance, the City of Amsterdam launched a program in 2023 supporting rooftop gardens, which boosted local seed purchases. The psychological benefit of connecting with nature in concrete jungles also drives demand. Retailers respond by offering specialized seed kits for small spaces.

Increasing Consumer Preference for Organic and Heirloom Varieties

The shifting consumer preference toward organic and heirloom seed varieties significantly propels the Europe garden seed market,s fuelling the growth of Europe garden seed market. Gardners are increasingly aware of the environmental impact of conventional agriculture and seek seeds that align with sustainable and chemical-free gardening practices. As per the Research Institute of Organic Agriculture, the area under organic management in Europe reached 16.9 million hectares in 2023, influencing home gardeners to adopt similar principles. Organic seeds are perceived as healthier and more environmentally friendly, driving their adoption among eco-conscious consumers. Heirloom varieties, which are open-pollinated and historically significant, appeal to gardeners interested in preserving biodiversity and unique flavors. These varieties often offer superior taste and nutritional profiles compared to commercial hybrids. The European Union’s support for agrobiodiversity through funding and research encourages the availability of rare and local seeds. Seed swap events and heritage seed libraries have gained popularity, fostering a community around preservation. In 2023, over 500 seed swapping events were recorded across Europe, as noted by the European Heritage Seed Network. This cultural movement values genetic diversity and resilience against climate change. Retailers expand their organic and heirloom offerings to meet this niche but growing demand.

MARKET RESTRAINTS

Stringent Regulatory Frameworks and Certification Costs

The strict regulatory frameworks governing seed marketing and certification are restricting the growth of Europe garden seed market. The European Union maintains rigorous standards for seed quality, purity, and germination rates, which require extensive testing and documentation. As per the European Commission’s Plant Reproductive Material Law, only varieties listed in the Common Catalogue can be marketed across member states. This listing process is time-consuming and expensive, particularly for small breeders and niche varieties. These high barriers to entry limit innovation and reduce the diversity of seeds available to consumers. Small-scale producers often struggle to comply with complex labeling and packaging regulations, which vary slightly between countries. The requirement for distinctness, uniformity, and stability testing favors large commercial breeds over heterogeneous landraces. This regulatory environment stifles the introduction of novel and adaptive varieties that could benefit home gardeners. Additionally, the restrictions on the exchange of non-certified seeds among hobbyists hinder community-based conservation efforts. In 2024, several grassroots seed networks faced legal challenges for distributing unlisted varieties, as reported by the European Civil Society Platform. These legal uncertainties discourage informal seed sharing and limit market dynamism. The burden of compliance disproportionately affects small enterprises, reducing competition and choice.

Climate Change-Induced Supply Chain Volatility

The climate change-induced volatility in seed production and supply chains is additionally hindering the growth of Europe garden seed market. Extreme weather events, such as droughts, floods, and heatwaves, disrupt seed cultivation in key producing regions, leading to shortages and price increases. As per the European Environment Agency, the frequency of extreme weather events in Europe has doubled since 1980, affecting agricultural output. Many vegetable seeds are produced in Southern Europe, where water scarcity is becoming critical. These disruptions force suppliers to source from distant regions, increasing transportation costs and carbon footprints. The unpredictability of harvests makes it difficult for companies to maintain consistent inventory levels. Gardeners face limited choices and higher prices during peak planting seasons. In 2024, the average price of tomato seeds in Italy increased by 12% due to supply constraints as noted by the Italian Agricultural Confederation. The reliance on specific climatic conditions for seed maturation limits the ability to shift production quickly. Additionally, changing pest and disease patterns require continuous breeding efforts, which are costly and slow. The lack of climate-resilient infrastructure in seed production exacerbates these issues.

MARKET OPPORTUNITIES

Expansion of Digital Gardening Platforms and Education

The expansion of digital gardening platforms and online educational resources offers a significant opportunity for the Europe garden seed market. Digital tools such as mobile apps, online courses, and virtual communities empower novice gardeners with knowledge and confidence to start growing. These platforms often integrate seed recommendations, planting calendars, and troubleshooting guides, creating a seamless user experience. Seed companies leverage these channels to reach younger demographics who prefer digital interaction over traditional retail. Subscription-based seed boxes tailored to seasonal needs and skill levels provide recurring revenue streams. Virtual workshops and webinars hosted by experts foster community engagement and brand loyalty. The integration of augmented reality allows users to visualize plant growth in their spaces, enhancing purchase decisions. Social media influencers play a crucial role in promoting specific varieties and techniques, driving trends. The accessibility of information reduces the barrier to entry for beginners. Companies that invest in digital content and user-friendly interfaces gain a competitive edge.

Development of Climate Resilient and Native Seed Varieties

The development and promotion of climate-resilient and native seed varieties is gaining huge traction over the growth of Europe garden seed market. As weather patterns become more unpredictable, gardeners seek plants that can withstand drought, heat, and pests without excessive chemical inputs. As per the European Biodiversity Strategy 2030, there is a strong policy push to restore native plant populations and enhance ecosystem resilience. Breeders are focusing on developing varieties with deeper root systems and improved water use efficiency. In 2023, the number of drought-tolerant vegetable varieties registered in the EU increased by 10% according to the Community Plant Variety Office. Native wildflower mixes are gaining popularity for supporting pollinators and improving soil health. These products appeal to environmentally conscious consumers who want to contribute to local ecosystems. Government grants and subsidies support research into adaptive traits, accelerating innovation. Collaborations between public research institutions and private seed companies facilitate knowledge transfer. Schools and municipalities incorporate these seeds into educational and landscaping projects.

MARKET CHALLENGES

Intellectual Property Rights and Patent Disputes

The intellectual property rights and patent disputes for small breeders and open source initiatives are one of the challenges for the growth of Europe garden seed market. Large multinational corporations often hold patents on specific genetic traits, limiting access for independent developers. These legal protections can restrict the ability of smaller companies to innovate or distribute certain varieties. High licensing fees and litigation costs create barriers to entry for startups. In 2024, a notable lawsuit involving a patented tomato variety restricted its use by small seed savers, as reported by the European Civil Society Platform. This legal uncertainty discourages collaboration and the sharing of genetic resources. The complexity of navigating intellectual property laws varies across member states, adding to the burden. Open-source seed initiatives argue that patents hinder biodiversity and farmer rights. The tension between corporate interests and public good creates a fragmented regulatory landscape. Gardeners may face limited choices if popular varieties are exclusively controlled. The lack of clear guidelines for traditional breeding methods versus biotechnological innovations adds confusion. Resolving these disputes requires balanced policies that protect innovation while ensuring access.

Counterfeit and Mislabelled Seed Products

The prevalence of counterfeit and mislabelled seed products undermines consumer trust and safety is additionally impedes the growth of Europe garden seed market. Online marketplaces and unauthorized sellers often distribute seeds that do not match their descriptions or contain prohibited substances. These fraudulent products may fail to germinate or introduce invasive species and diseases into local ecosystems. In 2024, customs authorities in the Netherlands seized 5 tons of mislabelled seeds from non-EU sources, according to the Dutch Food and Consumer Product Safety Authority. The lack of stringent verification on third-party platforms allows counterfeiters to operate with impunity. Genuine seed companies suffer reputational damage and financial losses when customers blame them for poor performance. The difficulty in tracing the origin of seeds complicates enforcement efforts. Consumers often struggle to distinguish between authentic and fake products, especially when prices are significantly lower. Regulatory bodies face resource constraints in monitoring the vast online marketplace. The spread of incorrect varieties disrupts breeding programs and conservation efforts. Educational campaigns are necessary to inform buyers about reputable sources. However, the sheer volume of online transactions makes comprehensive oversight difficult. This issue erodes confidence in the market and poses ecological risks. Strengthening digital surveillance and international cooperation is essential to combat this challenge.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Form, End Use, Distribution Channel, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled |

|

SEGMENTAL ANALYSIS

By Type Insights

The vegetable seeds segment accounted for 45.3% of the Europe garden seed market share in 2025, owing to heightened consumer awareness of food security and the desire for fresh, organic produce. The recent global supply chain disruptions and inflationary pressures have motivated households to cultivate their own vegetables to reduce grocery bills and ensure food quality. As per Eurostat data from 2023, over 30 million households in the European Union reported growing vegetables at home, representing a significant increase from previous years. Popular crops such as tomatoes, peppers, and leafy greens are favored due to their high yield and relatively short growth cycles. The psychological benefit of self-sufficiency also plays a crucial role as gardeners derive satisfaction from harvesting their own food. Urban farming initiatives supported by local governments further encourage vegetable cultivation in limited spaces. Community gardens and school projects prioritize edible plants, fostering a culture of homegrown nutrition. Retailers respond by offering diverse vegetable seed packs tailored to different skill levels and climatic zones. This sustained interest in edible gardening ensures that vegetable seeds remain the cornerstone of the market. The integration of vertical gardening systems has also made vegetable cultivation accessible to apartment dwellers, expanding the consumer base.

The herb seeds segment is projected to expand at a CAGR of 7.5% from 2026 to 2034, with the increasing culinary diversity and the consumer preference for fresh, flavorful ingredients in home cooking. Herbs such as basil, rosemary, thyme, and cilantro are essential in various international cuisines, which have gained popularity across Europe. As per the European Culinary Institute, the usage of fresh herbs in home cooking increased by 25% in 2023 as people experimented with global recipes. Growing herbs at home ensures immediate access to fresh flavors, which dried or store-bought herbs often lack. Compact herb gardens fit well in small urban spaces such as kitchen windowsills and balconies, making them accessible to apartment dwellers. The low cost and high yield of herb seeds make them an attractive entry point for novice gardeners. Cooking shows and online tutorials frequently highlight the use of fresh herbs, inspiring viewers to grow their own. Retailers offer curated herb seed collections targeting specific cuisines, enhancing appeal.

By Distribution Channel Insights

The retail stores segment accounted in holding 55.4% of the Europe garden seed market share in 2025, owing to the immediate availability of seeds and the tangible shopping experience that allows customers to inspect product quality before purchase. Garden centers, supermarkets, and hardware stores provide convenient access to a wide variety of seeds, especially during peak planting seasons. The tactile nature of seed packets allows buyers to check expiration dates and variety details easily. In Germany, foot traffic to garden centers increased by 10% in spring 2024, according to the German Garden Industry Association. Seasonal displays and promotional offers in retail outlets attract impulse buyers and casual gardeners. The trust established with local retailers fosters customer loyalty and repeat business. Physical stores also offer complementary products such as soil pots and tools, enabling one-stop shopping. The social aspect of visiting garden centers provides inspiration and community engagement. For older demographics who may be less comfortable with online shopping, retail stores remain the primary channel. The widespread network of retail outlets across urban and rural areas ensures broad market coverage.

The online stores segment is expected to expand at a CAGR of 9.2% from 2026 to 2034, owing to the convenience of home delivery and the wide variety of seeds available online compared to physical stores. E-commerce platforms allow customers to access rare heirloom and exotic varieties that are not typically stocked in local retailers. The ability to compare prices, read reviews, and access detailed planting information enhances the shopping experience. In the Netherlands, online seed sales grew by 30% in 2024, according to the Dutch E-Commerce Association. Subscription services offering seasonal seed boxes provide recurring revenue and convenience for busy consumers. Digital marketing and social media campaigns drive traffic to online stores by showcasing successful gardening projects. The ease of browsing and ordering from mobile devices appeals to younger demographics. Online retailers often provide personalized recommendations based on user preferences and location.

COUNTRY-LEVEL ANALYSIS

Germany Garden Seed Market Analysis

Germany was the top performer in the Europe garden seed market by accounting for 20.4% of the share in 2025. The strong tradition of allotment gardening and a high prevalence of private gardens are elevating the growth of the market in this country. As per the German Allotment Gardeners Federation, there are over 1 million allotment gardens in Germany providing a stable base for seed consumption. The German population places a high value on sustainability and organic produce, driving demand for eco-friendly seeds. In 2024, sales of organic vegetable seeds in Germany increased by 18% according to the German Organic Farmers Association. The well-developed retail infrastructure, including specialized garden centers and supermarkets, ensures wide availability. Government initiatives promoting urban greening and biodiversity support the market. German consumers are willing to pay premium prices for high-quality and certified seeds. The presence of major seed breeding companies in the country fosters innovation and variety development. Climate change adaptation has led to increased interest in drought-resistant varieties. The strong DIY culture encourages home improvement and gardening projects. Germany’s economic stability supports discretionary spending on hobbies.

United Kingdom Garden Seed Market Analysis

The United Kingdom garden seed market was ranked second by capturing 18.2% of the Europe garden seed market share in 2025. The deep-rooted gardening culture and a high participation rate in horticultural activities. The popularity of flower shows and gardening competitions stimulates interest in ornamental and vegetable seeds. The trend toward growing edible flowers and heritage vegetables has gained momentum among younger gardeners. Online retailing has expanded significantly, reaching rural and urban customers alike. The UK government’s support for community gardens and green spaces enhances market opportunities. Consumers are increasingly seeking native plant species to support local wildlife. The influence of media personalities and gardening programs inspires nationwide trends. Economic factors such as inflation have encouraged more people to grow their own food. The diverse climate allows for a wide range of crops to be cultivated. The strong community aspect of gardening fosters knowledge sharing and seed swapping. The UK’s vibrant gardening scene ensures its prominent position in the European market.

France Garden Seed Market Analysis

France garden seed market is expected to witness the fastest CAGR from 2026 to 2034, with a strong culinary tradition and a growing interest in organic farming. French consumers prioritize flavor and quality, leading to high demand for heirloom and specialty vegetable seeds. The concept of potager or kitchen garden is deeply embedded in French culture, driving seasonal seed purchases. Local markets and artisanal seed producers play a significant role in the distribution network. Government policies supporting agroecology encourage sustainable gardening practices. The rise of urban farming in cities like Paris and Lyon expands the consumer base. French gardeners are increasingly aware of biodiversity issues, preferring native and pollinator-friendly plants. The aesthetic appeal of gardens also drives sales of ornamental seeds. Tourism and rural lifestyle trends boost interest in country living and gardening.

Italy Garden Seed Market Analysis

Italy garden seeds market is growing steadily in the coming years. The favorable climate for year-round gardening and a strong emphasis on fresh ingredients are amplifying the growth of the market. As per the Italian National Institute of Statistics, many Italian households engage in gardening activities. The demand for tomato pepper and basil seeds is particularly high due to their importance in Italian cuisine. The trend toward organic and non-GMO seeds is gaining traction among health-conscious consumers. Small-scale family gardens remain a common feature in both urban and rural areas. Government incentives for green roofs and vertical gardens support urban cultivation. Italian consumers value traditional varieties preserving regional agricultural heritage. The tourism sector influences landscaping trends, increasing demand for ornamental seeds. Economic challenges have prompted more households to grow food for cost savings. The social aspect of gardening is strong, with community plots becoming more popular.

Spain Garden Seed Market Analysis

Spain's garden seed market growth is propelled by the growing interest in sustainable agriculture and water-efficient gardening. Water scarcity issues have driven demand for drought-tolerant vegetable and ornamental seeds. The Mediterranean climate allows for extended growing seasons, encouraging multiple planting cycles. Consumer awareness of food safety has boosted the popularity of homegrown produce. Local governments support community gardening projects to enhance social cohesion. The rise of eco-tourism promotes natural landscaping and native plant usage. Spanish consumers are increasingly adopting organic gardening methods. Retail expansion in suburban areas improves access to gardening supplies. The influence of international gardening trends via digital media stimulates innovation. Economic recovery has increased disposable income for hobby gardening.

COMPETITIVE LANDSCAPE

The competition in the Europe garden seed market is characterized by a mix of multinational corporations, regional breeders, and specialized niche providers vying for dominance through innovation and quality. Major players compete based on seed variety performance, sustainability credentials, and brand reputation rather than price alone. Established companies leverage their extensive research and development capabilities to introduce new varieties that resist climate stresses. Smaller niche players focus on localized and rare seeds appealing to environmentally conscious consumers. Regulatory compliance regarding seed certification and labeling serves as a significant barrier to entry, ensuring that only reputable firms can thrive. Collaborative efforts between breeders and retailers are common to optimize distribution and marketing. The rise of online sales channels adds another layer of competition, allowing direct-to-consumer brands to bypass traditional retail.

KEY MARKET PLAYERS

The leading companies operating in the Europe garden seed market include:

- Bayer Crop Science

- Syngenta

- Monsanto

- Sakata Seed Corporation

- Burgess Seed & Plant Co.

- Johnny's Selected Seeds

- Harris Seeds

- Enza Zaden

- Renee's Garden Seeds

- Seeds of Change

TOP PLAYERS IN THE MARKET

- Bayer AG is a global life science company with a significant presence in the Europe garden seed market through its subsidiary Seminis and other vegetable seed brands. The company contributes to the global market by developing high-quality vegetable and flower seeds that offer superior yield and disease resistance. Bayer focuses on sustainable agriculture and recently launched new drought-tolerant varieties suitable for European climates. The company has invested in digital gardening platforms to provide consumers with planting advice and support. These initiatives strengthen its market position by enhancing customer engagement and product performance. Bayer continues to lead through innovation and commitment to sustainability, ensuring long-term growth and trust among European home gardeners who value reliability and environmental responsibility in their gardening choices.

- Sakata Seed Corporation is a leading Japanese seed company with a strong footprint in the Europe garden seed market. The company plays a vital role in providing diverse flower and vegetable seeds known for their vibrant colors and robust growth. Sakata contributes to the global market by breeding innovative varieties that meet changing consumer preferences and climatic conditions. Recent actions include the introduction of new ornamental flower series specifically designed for European gardens. The company has also expanded its distribution networks to ensure wider availability of its products. These efforts strengthen its market position by offering unique and high-quality seeds that appeal to both amateur and professional gardeners. Sakata focuses on research and development to maintain its competitive edge.

- Enza Zaden is a prominent vegetable seed breeder with a significant presence in the Europe garden seed market. The company is involved in developing high-performance vegetable seeds for home gardeners, focusing on taste, yield, and ease of cultivation. Enza Zaden contributes to the global market by promoting sustainable farming practices and organic seed options. Recent actions include the launch of new organic vegetable varieties that are resistant to common pests and diseases. The company has also enhanced its online presence to connect directly with consumers and provide educational resources. These strategies strengthen its market position by meeting the growing demand for organic and resilient garden crops. Enza Zaden emphasizes collaboration with growers and retailers to ensure product success.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe garden seed market primarily employ product innovation and digital engagement to maintain a competitive advantage. Companies invest heavily in breeding programs to develop resilient and high-yielding varieties that suit diverse European climates. This strategy ensures differentiation and meets the evolving needs of home gardeners. Another major strategy involves expanding e-commerce platforms and digital tools to enhance customer experience and accessibility. Manufacturers utilize social media and online communities to build brand loyalty and provide gardening support. Strategic partnerships with local retailers and garden centers help secure shelf space and increase visibility. Additionally, companies focus on sustainability by offering organic and non-GMO seed options.

MARKET SEGMENTATION

This research report on the Europe garden seed market has been segmented and sub-segmented into the following categories.

By Type

- Flower Seeds

- Vegetable Seeds

- Herb Seeds

- Fruit Seeds

By Form

- Pelleted Seeds

- Non-Pelleted Seeds

- Organic Seeds

By End Use

- Home Gardens

- Commercial Gardens

- Public Parks

By Distribution Channel

- Retail Stores

- Online Stores

- Wholesale

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe garden seed market?

The Europe garden seed market covers suppliers of vegetable, flower, and herb seeds for home and urban gardens across the continent.

Why choose organic seeds in the Europe garden seed market?

Organic seeds in the Europe garden seed market support sustainable practices and appeal to eco-conscious gardeners in countries like Germany and France.

Which countries lead the Europe garden seed market?

Germany, France, and the UK dominate the Europe garden seed market due to strong retail networks and demand for hybrid varieties.

Are hybrid seeds popular in the Europe garden seed market?

Hybrid seeds lead the Europe garden seed market for their reliability in commercial and home gardening across Western Europe.

How has urban gardening affected the Europe garden seed market?

Urban gardening boosts the Europe garden seed market by increasing demand for compact, high-yield seed varieties in cities.

What trends shape the Europe garden seed market?

Sustainability and EU policies drive the Europe garden seed market toward organic and climate-resilient seed options.

Where to buy seeds in the Europe garden seed market?

E-commerce and garden centers serve the Europe garden seed market, offering diverse options from local suppliers.

Do regulations impact the Europe garden seed market?

EU rules on GMO and organic certification shape the Europe garden seed market, favoring non-GMO and hybrid seeds.

What vegetable seeds thrive in the Europe garden seed market?

Tomato, lettuce, and carrot seeds are staples in the Europe garden seed market for home growers.

Is the Europe garden seed market growing for heirloom varieties?

Heirloom seeds gain traction in the Europe garden seed market amid interest in biodiversity and tradition.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com