Europe Push-Pull Market Size, Share, Trends, and Growth Analysis Report, Segmented by Component, Application, Material, and Country – Industry Forecast From 2026 to 2034

Europe Push-Pull Market Report Summary

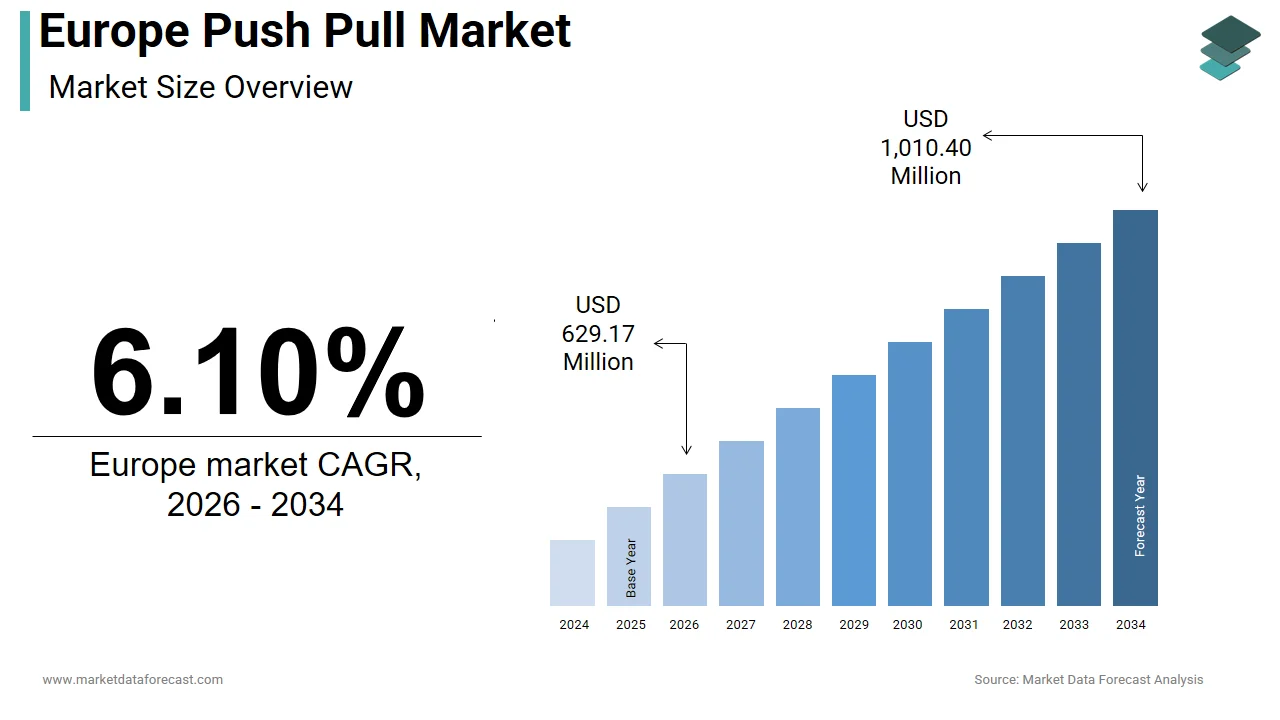

The Europe push-pull market was valued at USD 593 million in 2025, is estimated to reach USD 629.17 million in 2026, and is projected to reach USD 1,010.40 million by 2034, growing at a CAGR of 6.10% from 2026 to 2034. Market growth is driven by increasing demand for convenient and ergonomic access solutions across residential, commercial, and industrial applications. Push-pull mechanisms are widely used in cabinetry, furniture, automotive components, and industrial enclosures due to their simplicity, durability, and user-friendly design. Additionally, the rising adoption of modern interior designs and space-saving solutions is further boosting market demand across Europe.

Key Market Trends

- Growing demand for ergonomic and user-friendly hardware solutions.

- Increasing adoption in furniture and cabinetry applications.

- Rising focus on modern interior design and aesthetics.

- Expansion of automotive and industrial applications.

- Technological advancements in durable and lightweight materials.

Segmental Insights

- Based on component, the mechanical segment dominated the Europe push-pull market in 2025, driven by its reliability and cost-effectiveness.

- Based on application, the residential segment accounted for 23.4% share in 2025, supported by increasing demand for modern furniture solutions.

- Based on material, the stainless steel segment led the market with 22.3% share in 2025, owing to its durability and corrosion resistance.

Regional Insights

The Europe push-pull market is witnessing steady growth across major industrial and consumer markets.

- Germany led the market in 2025 with approximately 22% share, driven by strong manufacturing and furniture industries.

- France followed with 19.1% share, supported by diverse industrial applications and interior design trends.

- The United Kingdom is experiencing growth due to demand from the automotive aftermarket and industrial machinery sectors.

Competitive Landscape

The Europe push-pull market is moderately competitive, with companies focusing on product innovation, quality, and expanding application areas. Strategic partnerships and design innovation are key competitive strategies.

Prominent companies operating in the Europe push-pull market include Häfele Group, Hettich Group, Blum, Sugatsune Kogyo Co., Ltd., Southco Inc., ASSA ABLOY AB, Allegion plc, DIRAK GmbH, Essentra plc, and Godrej & Boyce Manufacturing Company.

Europe Push Pull Market Size

The Europe push-pull market was valued at USD 593 million in 2025, is estimated to reach USD 629.17 million in 2026, and is projected to reach USD 1,010.40 million by 2034, growing at a CAGR of 6.10% from 2026 to 2034.

The push-pull is a hardware mechanism designed to facilitate the opening and closing of doors, cabinets, and drawers through linear motion rather than rotational movement. These systems are integral components in modern architectural, joinery furniture manufacturing, and industrial enclosure designs across the continent. The fundamental utility lies in their ability to provide seamless access while maintaining aesthetic minimalism and ergonomic efficiency. In contemporary European interiors, the demand for sleek handle-less designs has propelled the adoption of these mechanical solutions. Furthermore, the European Furniture Industries Confederation states that the furniture sector in Europe employs approximately 950000 people and generates an annual turnover exceeding 130 billion euros. This substantial economic footprint underscores the critical role of component suppliers, including those specializing in push-pull mechanisms. The integration of these devices into high-traffic commercial spaces and residential properties reflects a broader trend towards functional elegance. Regulatory standards such as the European Norm EN 1935 for single-axis hinges also influence the quality benchmarks for associated hardware. The market is characterized by a shift towards durable materials like stainless steel and zinc alloy to withstand frequent usage.

MARKET DRIVERS

Rising Preference for Minimalist and Handle-Less Interior Designs Drives Component Adoption

The aesthetic evolution of European living and working spaces has significantly favored minimalist architectures that eliminate visual clutter, which is escalating the growth of the Europe push-pull market. This design philosophy prioritizes clean lines and uninterrupted surfaces, which directly necessitates the use of push-pull mechanisms instead of traditional protruding handles. The trend is particularly pronounced in urban centers, such as Berlin, Paris, and Milan, where space optimization and modern aesthetics converge. The psychological appeal of uncluttered environments has driven consumers to seek hardware that remains invisible until activated. Push-pull latches and catches allow doors and drawers to open with a simple press, thereby preserving the sleek facade of furniture units. Data from the German Furniture Institute indicates that sales of minimalist furniture collections rose by 18% in 2024, reflecting this consumer shift. Manufacturers are responding by developing low-profile mechanisms that require minimal installation depth yet offer reliable performance. The hospitality sector also contributes to this demand as hotels and restaurants aim for sophisticated interiors that enhance guest experience through subtle functionality. As architects and designers specify these details in early planning stages, the volume of push-pull hardware procurement increases proportionally.

Expansion of the Modular Furniture and Customized Storage Solutions Sector Fuels Demand

The consumers increasingly seek adaptable and personalized storage solutions, which is additionally promoting the growth of the Europe push pull market. Push-pull mechanisms are essential components in these systems, enabling seamless integration of various modules without the visual disruption of external handles. Customized wardrobes and kitchen units often feature complex configurations where traditional handles may impede movement or clash with adjacent modules. The push-pull system offers a universal solution that accommodates diverse door weights and sizes ranging from lightweight glass panels to heavy wooden fronts. The surge is attributed to rising disposable incomes and a greater emphasis on home organization post-pandemic. The flexibility of push-pull hardware allows for easy adjustment and reconfiguration of modular units, which aligns with the dynamic lifestyle of modern European households. Furthermore, the commercial office sector is adopting modular workstations that utilize these mechanisms for privacy screens and storage compartments. The scalability of modular designs ensures a consistent demand for standardized yet versatile hardware components. Manufacturers benefit from this trend as it encourages bulk procurement for large-scale residential and commercial projects.

MARKET RESTRAINTS

Volatility in Raw Material Prices Impacts Manufacturing Cost Structures and Margins

The production of push-pull mechanisms relies heavily on metals, such as stainless steel, zinc alloy, and aluminum, which are subject to significant price fluctuations, limiting the growth of Europe push pull market. These raw material costs constitute a substantial portion of the total manufacturing expense, making producers vulnerable to volatility. According to the European Metal Trade Association, the price of zinc increased by 15% in 2024 due to supply chain disruptions and energy cost spikes in smelting operations. Such fluctuations directly affect the profit margins of hardware manufacturers, who often operate on thin margins due to intense competition. The energy crisis in Europe has further exacerbated these costs as metal processing is energy-intensive. This persistent cost pressure forces manufacturers to either absorb the expenses or pass them on to customers, both of which carry risks. Absorbing costs reduces profitability and limits investment in research and development, while passing them on may reduce competitiveness against cheaper imports. Small and medium-sized enterprises are particularly affected as they lack the bargaining power to secure long-term fixed price contracts with suppliers. The uncertainty in raw material availability also leads to inventory management challenges requiring companies to hold larger stock buffers, which ties up capital. Additionally, the transition towards sustainable sourcing adds another layer of complexity and cost as recycled metals often command premium prices. These financial pressures constrain the ability of manufacturers to innovate and expand their product portfolios, thereby slowing down market growth potential in the short to medium term.

Stringent Environmental Regulations and Compliance Requirements Increase Operational Complexity

The European Union enforces rigorous environmental standards that govern the production, disposal, and recycling of metal hardware components, which is additionally inhibits the growth of the Europe push pull market. Regulations, such as the Registration Evaluation Authorization and Restriction of Chemicals framework, impose strict limits on hazardous substances used in plating and coating processes. Compliance with these regulations requires significant investment in advanced manufacturing technologies and waste management systems. As per the European Environment Agency, industries spent an estimated 8 billion euros on environmental protection measures in 2024, with the metal processing sector accounting for a notable share. For push-pull manufacturers, this means adhering to specific guidelines regarding lead, cadmium, and other toxic elements commonly found in traditional alloys. The Circular Economy Action Plan further mandates that products must be designed for durability, repairability, and recyclability. This necessitates redesigning existing mechanisms to ensure they can be easily disassembled and recycled at the end of their life cycle. The administrative burden of documenting compliance and undergoing regular audits adds to operational costs. Small manufacturers often struggle to meet these requirements due to limited resources and technical expertise. Furthermore, the Carbon Border Adjustment Mechanism introduced by the EU affects the cost of imported raw materials, aiming to prevent carbon leakage but increasing input costs for domestic producers. These regulatory hurdles create barriers to entry for new players and force existing ones to continuously adapt their processes. Failure to comply can result in hefty fines and reputational damage, making regulatory adherence a critical yet challenging aspect of market participation.

MARKET OPPORTUNITIES

Integration of Smart Home Technologies Presents New Avenues for Product Innovation

The rapid adoption of smart home ecosystems for the evolution of push-pull mechanisms into intelligent access solutions is setting up new opportunities for the growth of Europe push pull market. Consumers are increasingly seeking connected devices that enhance convenience, security, and energy efficiency within their homes. Traditional mechanical push-pull latches can be upgraded with sensors and actuators to enable automated opening and closing functions. This integration allows for features such as remote access, voice control, and activity monitoring, which appeal to tech-savvy homeowners. For instance, a smart push-pull system can detect when a user approaches and automatically unlock a cabinet or door, enhancing accessibility for elderly or disabled individuals. This trend creates a demand for hardware components that are compatible with standard communication protocols, such as Zigbee and Wi Fi. Manufacturers who invest in developing electronic push-pull mechanisms can differentiate themselves in a crowded market. Additionally, the commercial sector benefits from these innovations through improved asset tracking and security management in offices and retail spaces. The ability to collect data on usage patterns also provides valuable insights for predictive maintenance and user experience optimization.

Growth in the Healthcare and Assisted Living Infrastructure Sectors Expands Application Scope

The aging population is driving substantial investments in healthcare facilities and assisted living accommodations, which require specialized hardware solutions is additionally gearing up the growth of the Europe push-pull market. Push-pull mechanisms are particularly suitable for these environments due to their hygienic design and ease of use for individuals with limited mobility. Unlike traditional handles, they do not harbor bacteria in crevices and can be operated with minimal physical effort. As per Eurostat, the share of the population aged 65 and over in the EU is expected to reach 30% by 2050, necessitating expanded care infrastructure. Governments across Europe are allocating significant funds to upgrade hospitals and nursing homes to meet these demographic changes. These facilities prioritize infection control and accessibility, making push-pull systems an ideal choice for cabinet doors and medical equipment enclosures. The smooth surfaces of these mechanisms facilitate easy cleaning and disinfection, which is in preventing hospital acquired infections. Furthermore, the ergonomic benefit of push-to-open features assists patients and caregivers in accessing supplies without straining. The demand for age-friendly design principles is also influencing residential renovations where older adults prefer to remain in their own homes. This segment values safety and convenience, leading to increased retrofitting of existing furniture with accessible hardware. Manufacturers can capitalize on this trend by developing specialized products that meet medical-grade standards and offer enhanced durability.

MARKET CHALLENGES

Supply Chain Disruptions and Logistical Bottlenecks Hinder Timely Product Availability

The global supply chain instabilities that affect the timely delivery of raw materials and finished goods are one of the challenges for the growth of the Europe push-pull market. Geopolitical tensions and trade restrictions have disrupted established logistics routes, leading to delays and increased transportation costs. According to the European Logistics Association, average freight rates within Europe remained 12% higher in 2025 compared to historical averages due to fuel price volatility and driver shortages. These logistical disruptions impact the ability of manufacturers to maintain consistent inventory levels, resulting in stockouts and delayed order fulfillment. The reliance on imported components from Asia further exacerbates this vulnerability as port congestion and customs delays become more frequent. Such unpredictability complicates production planning and strains relationships with downstream customers, who expect just-in-time delivery. Companies are forced to diversify their supplier base and explore nearshoring options, which involve significant upfront investment and operational adjustments. The lack of visibility across multi-tier supply chains makes it difficult to anticipate and mitigate disruptions proactively. Additionally, the transition to green logistics initiatives, while necessary, adds complexity as companies adapt to new regulations regarding emissions and packaging. These challenges require robust risk management strategies and flexible operational models to ensure business continuity. Failure to address supply chain vulnerabilities can lead to lost sales and diminished market share in a competitive landscape.

Intense Competition from Low-Cost International Manufacturers Pressures Pricing Strategies

The intense competition from low-cost manufacturers primarily based in Asia, who offer comparable products at significantly lower prices, is expected to impede the growth of Europe push pull market. This price disparity puts considerable pressure on European producers, who face higher labor and regulatory compliance costs. According to the study, imports of metal furniture fittings from non-EU countries increased by 8% in 2024, with China remaining the largest source. These imports often benefit from economies of scale and subsidized production costs, allowing them to undercut local competitors. European manufacturers struggle to compete on price alone and must therefore differentiate through quality innovation and brand reputation. However, this strategy requires continuous investment in research and development, which may not always yield immediate returns. The presence of counterfeit products further complicates the landscape as they erode brand value and consumer trust. Small and medium-sized enterprises are particularly vulnerable as they lack the resources to engage in prolonged price wars or extensive legal battles. The consolidation of global supply chains also means that distributors may prioritize cheaper alternatives to maximize their own margins. This dynamic forces European companies to constantly justify their premium pricing through superior performance and service. Maintaining market share in this environment requires strategic partnerships and a strong focus on customer loyalty. The threat of substitution remains a constant challenge that influences long-term strategic planning and profitability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Component, Application, Material, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled |

|

SEGMENTAL ANALYSIS

By Component Insights

The mechanical segment was the largest by holding a dominant share of the Europe push pull market in 2025, with its widespread adoption in residential and commercial furniture applications. These devices operate without external power sources, relying on spring-loaded mechanisms or magnetic catches to secure and release doors. The durability of mechanical systems makes them ideal for high-traffic environments, such as schools, hospitals, and public offices, where electronic failures could disrupt operations. Data from the German Hardware Federation indicates that the average lifespan of a quality mechanical push-pull latch exceeds 50000 cycles, which aligns with the longevity expectations of European consumers. Furthermore, the absence of wiring simplifies retrofitting projects, allowing homeowners to upgrade existing cabinetry without extensive renovations. Manufacturers continue to innovate within this segment by improving corrosion resistance and smoothness of operation using advanced materials like nylon and stainless steel. The standardization of sizes and mounting patterns also facilitates easier replacement and inventory management for distributors. As economic uncertainty persists in certain regions, the preference for cost-effective and reliable solutions reinforces the dominance of mechanical push-pull systems.

The electronic segment is expected to witness the fastest CAGR of 8.2% during the forecast period, with modern smart home ecosystems and luxury interior designs. These systems utilize motor sensors and connectivity modules to provide automated access and enhanced functionality. Electronic push-pull mechanisms offer features, such as soft close, anti-pinch safety, and remote activation via smartphone applications. These capabilities are particularly valued in high-end residential properties and commercial spaces where user experience and convenience are prioritized. Although the initial cost is higher, the long-term benefits of energy efficiency and security drive adoption in these sectors. Technological advancements have reduced the size of electronic components, allowing for discreet installation within slim-profile furniture. The integration with voice assistants such as Amazon Alexa and Google Home further enhances appeal among tech-savvy consumers. Manufacturers are focusing on improving battery life and reducing power consumption to address operational concerns. The rise of USB-powered devices also simplifies installation by eliminating the need for complex electrical wiring.

By Application Insights

The residential application segment was the accounted in holding 23.4% of the Europe push pull market share in 2025. The ongoing home improvement activities and changing interior design preferences are escalating the growth of the segment. Homeowners are increasingly investing in kitchen and wardrobe upgrades to enhance functionality and aesthetic appeal. According to Eurostat, residential construction and renovation expenditures in the European Union reached 1.2 trillion euros in 2024, reflecting strong consumer confidence in property improvements. The trend towards open-plan living and minimalist kitchens has increased the demand for handle-less cabinetry, which relies heavily on push-pull mechanisms. The aging population also contributes to this demand as older adults seek ergonomic solutions that reduce physical strain when accessing storage. Retrofitting existing homes with modern hardware is a common practice as it offers a cost-effective way to update interiors without full-scale renovations. Online retail platforms have made it easier for consumers to purchase and install these components themselves, further boosting sales. The DIY culture in countries such as Germany and the Netherlands supports this trend, with hardware stores reporting increased footfall for interior fittings. Additionally, the rental market influences demand as landlords upgrade properties to attract tenants who value modern amenities.

The commercial application segment is growing steadily, driven by the modernization of office spaces and the expansion of the hospitality industry. Businesses are redesigning workspaces to promote collaboration and flexibility, which often involves modular furniture equipped with push-pull mechanisms. As per the study, corporate spending on office fit-outs increased by 10% in 2025 as companies returned to hybrid working models. Push-pull systems are preferred in commercial settings for their durability and ability to withstand frequent use in conference rooms, break areas, and reception desks. The hospitality sector, including hotels, restaurants, and cafes, also contributes significantly to this demand. Establishments aim to create sleek and uncluttered environments that enhance guest experience, leading to the adoption of handle-less designs in bars, counters, and storage units. Healthcare facilities represent another critical sub-segment where hygiene and accessibility are paramount. Push-pull mechanisms minimize contact points, reducing the risk of cross-contamination in hospitals and clinics. The public sector also utilizes these systems in libraries, museums, and government buildings, where aesthetic consistency and security are important.

By Material Insights

The stainless steel segment was the largest by holding 22.3% of the Europe push pull market share in 2025, owing to its superior strength and resistance to corrosion. This material is particularly suitable for humid environments such as kitchens and bathrooms, where exposure to moisture is common. According to the study, consumption of stainless steel in the hardware sector increased by 5% in 2024, driven by its longevity and low maintenance requirements. The aesthetic appeal of brushed or polished stainless steel also aligns with contemporary design trends, making it a popular choice for visible applications. Data from the Italian Metalworking Industry Federation shows that stainless steel accounts for 40% of all metal hardware production in Southern Europe. Its recyclability further enhances its attractiveness in an era of increasing environmental consciousness. Manufacturers prefer stainless steel for its ability to maintain structural integrity under heavy loads, ensuring reliable performance over time. The material is also compatible with various finishing techniques, allowing for customization to match different interior styles. Although it is more expensive than alternatives such as plastic or aluminum, the long-term cost benefits justify the initial investment for many consumers. The availability of different grades, such as 304 and 316, allows users to select the appropriate level of corrosion resistance for specific applications. Regulatory standards regarding food safety also favor stainless steel in kitchen environments where contact with food items may occur.

The zinc alloy and plastic materials are gaining huge traction by growing at a fastest CAGR of 11.2% from 2026 to 2034, and are gaining prominence in the push-pull market due to their cost-effectiveness and manufacturing versatility. Zinc alloy offers a good balance between strength and price, making it suitable for mid-range furniture applications. The material allows for intricate shapes and detailed finishes, which appeal to designers seeking decorative elements. Plastic components, particularly those made from high-impact polymers, are increasingly used in lightweight and budget-friendly installations. These materials are ideal for indoor applications where exposure to extreme conditions is limited. The ability to mold plastic into various colors and textures provides designers with greater creative freedom. Additionally, plastic mechanisms are lighter, reducing shipping costs and easing installation processes. The development of bio-based plastics also aligns with sustainability goals, attracting environmentally conscious buyers. While these materials may not offer the same longevity as stainless steel, they provide viable options for temporary or low-intensity usage scenarios. The combination of zinc alloy bodies with plastic internal components is a common strategy to optimize performance and cost.

COUNTRY-LEVEL ANALYSIS

Germany Push-Pull Market Analysis

Germany was the largest contributor in the Europe Push-Pull market by accounting for 22% of the regional share, driven by its robust automotive and industrial manufacturing sectors. The country serves as a central hub for original equipment manufacturers who require high-precision fastening solutions for vehicle interiors and machinery enclosures. According to the German Association of the Automotive Industry, vehicle production in Germany reached nearly 4 million units in 2023, sustaining strong demand for interior components, including latches and locking mechanisms. The presence of leading automotive suppliers, such as Bosch and Continental, further amplifies the need for reliable Push-Pull systems that meet stringent safety and durability standards. This growth directly translates to higher consumption of industrial-grade latches for control panels and access doors. Furthermore, the German government’s emphasis on Industry 4.0 initiatives encourages the adoption of smart locking solutions integrated with Internet of Things technologies. The strong focus on quality and innovation ensures that Germany remains the primary driver of technological advancements and volume consumption in the European Push-Pull latch market.

France Push-Pull Market Analysis

France's push-pull latch market was ranked second with 19.1% of share in 2025, with its diverse industrial base and strong aerospace sector. The country is home to major aerospace manufacturers such as Airbus, which utilize specialized lightweight and high-strength latches for aircraft interiors and cargo systems. According to the French Aerospace Industries Association, the aerospace sector generated revenue of over 70 billion EUR in 2023, driving demand for certified fastening solutions that comply with rigorous aviation safety regulations. The automotive industry also contributes substantially, with companies like Renault and Stellantis incorporating ergonomic Push-Pull latches in vehicle designs to enhance user experience. Additionally, the luxury goods sector in France demands high aesthetic and functional quality in packaging and display cases utilizing premium Push-Pull mechanisms. These diverse application areas ensure that France maintains a stable and growing position in the regional market landscape.

United Kingdom Push-Pull Market Analysis

The United Kingdom Push-Pull latch market growth is driven by a strong presence in the automotive aftermarket and industrial machinery sectors. Despite changes in trade dynamics, the UK remains a key player due to its advanced manufacturing capabilities and demand for replacement parts. According to the Society of Motor Manufacturers and Traders, the UK automotive sector produced over 900000 vehicles in 2023 by creating consistent demand for interior trim components, including latches. The industrial sector also drives growth with manufacturers requiring robust locking solutions for electrical enclosures and control cabinets. The rise in renewable energy installations, particularly in wind and solar farms, has increased the need for weather-resistant latches for equipment housing. As per the Department for Business and Trade, exports of mechanical power engines and parts increased by 6%, reflecting strong international demand for UK-manufactured components. Furthermore, the retail and furniture industries utilize Push-Pull latches in cabinetry and display units, contributing to steady domestic consumption.

Italy Push-Pull Market Analysis

Italy's push-pull latch market growth is driven by its strong furniture manufacturing and automotive design industries. The country is renowned for its high-quality furniture production, which extensively uses decorative and functional Push-Pull latches in kitchen cabinets, wardrobes, and office furniture. According to the Italian Federation of Wood and Furniture Industries, the furniture sector exported goods worth over 15 billion EUR in 2023. The automotive sector also plays a crucial role, with brands like Ferrari and Fiat requiring precise and aesthetically pleasing latches for vehicle interiors. Data from the National Institute of Statistics shows that industrial production in Italy increased by 4%, supported by a recovery in consumer goods manufacturing. The construction industry contributes to market growth through renovation projects that often involve replacing old hardware with modern Push-Pull systems. Additionally, the packaging industry in Italy utilizes specialized latches for reusable containers and luxury boxes, adding to the diverse demand.

Spain Push-Pull Market Analysis

Spain's push-pull latch market growth is likely to grow steadily in the coming years, with its growing automotive and construction sectors. The country has become a major manufacturing hub for European automakers, with companies like SEAT and Ford operating large production facilities that require extensive interior components. The construction industry also supports market growth with ongoing infrastructure projects and residential developments requiring hardware for doors, windows, and cabinetry. The tourism industry further contributes to demand through the hospitality sector, which frequently renovates hotels and resorts using modern furniture with Push-Pull latches. Additionally, the renewable energy sector is expanding with investments in solar and wind projects that require secure enclosures for electrical equipment.

COMPETITIVE LANDSCAPE

The competition in the Europe push pull market is characterized by a mix of established global leaders and specialized regional manufacturers who vie for dominance through innovation and quality. Major players distinguish themselves by offering advanced mechanical and electronic solutions that cater to the growing demand for minimalist and handle-less interiors. The market sees intense rivalry in terms of product durability, aesthetic appeal, and integration with smart home technologies. Companies frequently launch new variants with improved corrosion resistance and smoother operation to attract discerning consumers. Price competition remains relevant, particularly in the mid-range segment where cost-sensitive buyers seek value for money. However, premium brands focus on superior engineering and brand reputation to justify higher price points. Strategic collaborations with furniture makers and architects are common tactics to secure specification advantages. The presence of low-cost imports from Asia adds pressure on local manufacturers to optimize production efficiency.

KEY MARKET PLAYERS

The leading companies operating in the Europe push pull market include:

- Häfele Group

- Hettich Group

- Blum

- Sugatsune Kogyo Co., Ltd.

- Southco Inc.

- ASSA ABLOY AB

- Allegion plc

- DIRAK GmbH

- Essentra plc

- Godrej & Boyce Manufacturing Company

TOP PLAYERS IN THE MARKET

- Hettich is a leading global manufacturer of furniture fittings with a strong presence in the European push-pull market. The company specializes in innovative mechanical and electronic opening systems that cater to modern minimalist designs. Hettich contributes significantly to the global market by exporting high-quality hardware solutions to over 120 countries. Recent actions include the launch of advanced Push to Open mechanisms that integrate seamlessly with smart home technologies. The company has invested heavily in research and development to enhance the durability and aesthetic appeal of its products. Hettich also focuses on sustainability by using recyclable materials in its production processes. Their commitment to quality and innovation strengthens their position as a preferred supplier for both residential and commercial projects across Europe.

- Blum is an Austrian manufacturer renowned for its high-quality motion technologies and fitting systems, including push-pull mechanisms. The company plays a pivotal role in the global market by setting benchmarks for functionality and ease of use. Blum recently expanded its product portfolio with the introduction of Servo Drive electrical opening support systems. These innovations allow for touchless operation, which enhances hygiene and convenience in kitchens and bathrooms. The company has strengthened its market position by establishing new training centers in major European cities to educate designers and craftsmen. Blum emphasizes ergonomic design and long-term reliability, which appeals to premium segment consumers. Their strategic partnerships with furniture manufacturers ensure widespread adoption of their technologies in custom and modular furniture solutions throughout the continent.

- Häfele is a prominent international partner for furniture and architectural hardware with a significant footprint in the Europe push pull market. The company offers a diverse range of mechanical and electronic latches that meet varying customer needs. Häfele contributes to the global market through its extensive distribution network and comprehensive product catalog. Recent initiatives include the development of compact push-pull latches designed for slim-profile furniture applications. The company has enhanced its digital platforms to provide easier access to product information and installation guides for professionals. Häfele focuses on providing holistic solutions by integrating push-pull systems with lighting and connectivity features. Their emphasis on customer service and technical support helps maintain strong relationships with architects and interior designers. This approach ensures that Hafele remains a key player in delivering innovative and reliable hardware solutions across European markets.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe push pull market primarily focus on product innovation and technological integration to maintain a competitive advantage. Companies invest heavily in research and development to create smart and electronic opening systems that align with modern home automation trends. Strategic partnerships with furniture manufacturers and interior designers help embed these components into new collections early in the design phase. Expansion of distribution networks ensures broader market reach and faster delivery times to customers across diverse regions. Sustainability initiatives are also central to corporate strategies as firms adopt eco-friendly materials and energy-efficient production methods to comply with stringent European regulations. Training programs for installers and architects enhance product adoption by ensuring proper usage and highlighting functional benefits. These combined efforts enable companies to differentiate their offerings and respond effectively to evolving consumer preferences for minimalism and convenience in interior design applications.

MARKET SEGMENTATION

This research report on the Europe push pull market has been segmented and sub-segmented into the following categories.

By Component

- Mechanical

- Electronic

By Application

- Residential

- Commercial

By Material

- Stainless Steel

- Zinc Alloy

- Plastic

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe push-pull market?

The Europe push-pull market covers connectors and closures that enable easy connect/disconnect functionality in electronics, packaging, and industrial applications.

How does the Europe push-pull market function?

The Europe push-pull market functions through mechanical designs that allow secure mating and quick release without twisting, used across multiple industries.

What drives growth in the Europe push-pull market?

The Europe push-pull market grows due to demand for user-friendly packaging, reliable industrial connectors, and automation needs in manufacturing sectors.

Which countries lead the Europe push-pull market?

The Europe push-pull market is led by Germany, France, and the UK, where electronics manufacturing and packaging industries drive strong component demand.

What applications shape the Europe push-pull market?

The Europe push-pull market serves electronics, medical devices, beverage packaging, industrial automation, and consumer goods packaging applications.

What types define the Europe push-pull market?

The Europe push-pull market includes circular connectors, plastic closures, metal connectors, tamper-evident designs, and waterproof variants for diverse uses.

How does packaging influence the Europe push-pull market?

The Europe push-pull market benefits from packaging because push-pull closures offer convenience, child resistance, and tamper evidence for beverages and consumer goods.

What trends affect the Europe push-pull market?

The Europe push-pull market sees growth in sustainable materials, miniaturization, higher reliability standards, and smart packaging integration.

What challenges face the Europe push-pull market?

The Europe push-pull market faces material cost pressures, regulatory compliance for food contact, and competition from alternative closure technologies.

How do connectors fit the Europe push-pull market?

The Europe push-pull market relies on connectors for industrial, medical, and electronics applications needing secure, vibration-resistant connections.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com