Europe Sports Tourism Market Size, Share, Trends & Growth Forecast Report, Segmented By Sports Type (Soccer/Football, Cricket, Basketball, Tennis), Tourism Type, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe) - Industry Analysis From (2026 To 2034)

Europe Sports Tourism Market Report Summary

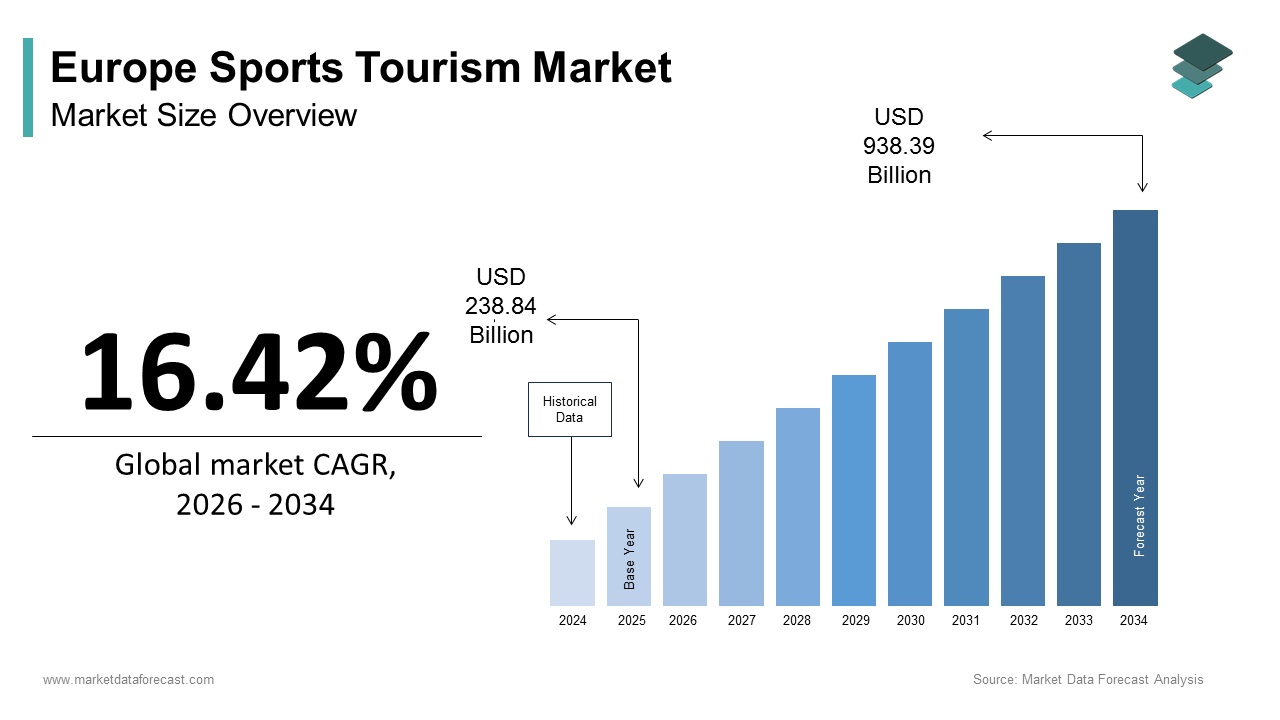

The Europe sports tourism market was valued at USD 238.84 billion in 2025 and is projected to reach USD 938.39 billion by 2034, growing from USD 278.07 billion in 2026 at a CAGR of 16.42% during the forecast period. Market growth is driven by Europe’s deep-rooted sports culture, frequent hosting of international tournaments, and rising demand for live sporting experiences combined with travel. Increasing disposable incomes, expansion of stadium infrastructure, and strong cross-border mobility within Europe are further accelerating sports-related travel. The growing popularity of bundled matchday experiences, fan tourism, and premium hospitality offerings continues to strengthen the region’s sports tourism ecosystem.

Key Market Trends

- Strong demand for football-centric travel experiences driven by major European leagues and tournaments

- The rising popularity of passive sports tourism is focused on live event attendance and fan engagement.

- Increasing integration of hospitality, entertainment, and cultural tourism with sporting events

- Growth in premium seating, VIP packages, and experiential sports travel offerings

- Expansion of digital booking platforms and personalized sports travel packages

Segmental Insights

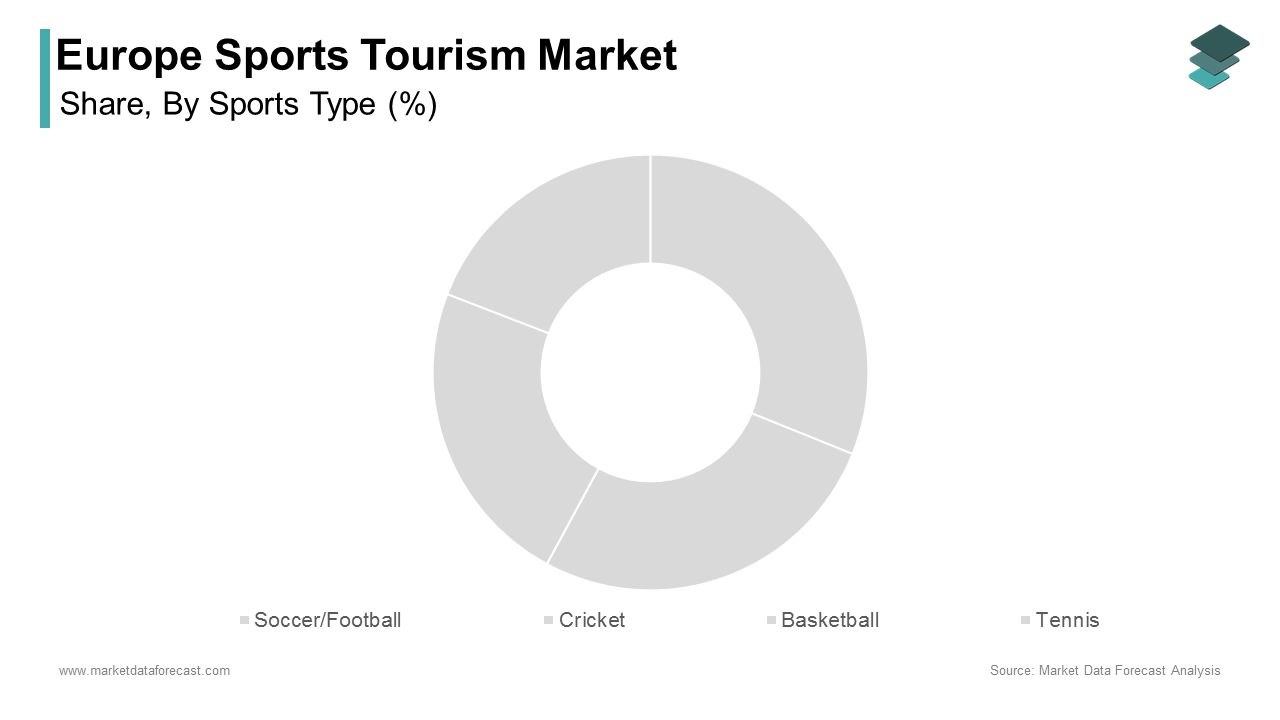

Based on sports type, the soccer or football segment dominated the Europe sports tourism market in 2025 by holding 60.6% of the regional market share, supported by Europe’s globally followed leagues, iconic clubs, and high-frequency international competitions.

Based on tourism type, the passive tourism segment led the market in 2025 by capturing 55.8% of the regional market share, driven by strong demand for spectating experiences, stadium tours, and event-based travel.

Regional Insights

- United Kingdom led the Europe sports tourism market in 2025 by holding 20.9% of the total market share, supported by globally popular football leagues, historic venues, and a mature sports hospitality ecosystem.

- Spain ranked second in 2025, driven by international football tourism, iconic clubs, and strong inbound tourist flow.s

- France is expected to grow at a promising CAGR during the forecast period, supported by mega-event hosting, world-class infrastructure, and strategic use of sports for territorial development.

- Germany is anticipated to account for a notable market share due to its strong fan culture, engineering precision in stadium operations, and decentralized event hosting model.

- Italy is projected to register healthy growth, driven by the fusion of sporting passion, historical attractions, and regional tourism diversity.

Competitive Landscape

The Europe sports tourism market is highly fragmented and experience-driven, with tour operators and travel specialists focusing on exclusive access, matchday hospitality, and customized fan packages. Companies are strengthening partnerships with clubs, leagues, and event organizers while expanding digital platforms to enhance customer engagement and booking convenience.

Prominent players in the Europe sports tourism market include TUI Group, Thomas Cook Sports, Sports Tours International, Gulliver's Sports Travel, Keith Prowse Travel, Matchday International, Champions Travel, Eventeam Group, Gulliver's Travel Group, P1 Travel, Sportsnet Holidays, Travel Counsellors Sports, Inspire Sport, EuroSport Travel, and World Soccer Travel.

Europe Sports Tourism Market Size

The Europe sports tourism market size was calculated to be USD 238.84 billion in 2025 and is anticipated to be worth USD 938.39 billion by 2034, growing from USD 278.07 billion in 2026 at a CAGR of 16.42% during the forecast period.

Sports tourism encompasses travel activities centred around participation in or spectating of sporting events, ranging from elite competitions like the UEFA Champions League and Tour de France to participatory experiences such as alpine skiing, marathon running, and football training camps. This segment merges athletic engagement with cultural exploration, leveraging Europe’s dense network of historic stadiums, world-class infrastructure, and diverse natural landscapes from the Pyrenees to the Adriatic coast. Unlike generic leisure travel, sports tourism generates higher per capita spending, longer stays, and off-season visitation, which is making it a strategic pillar of regional economic development. According to Eurostat, international tourist arrivals in the European Union exceeded 670 million in 2023, with event-driven travel accounting for a growing share. Furthermore, as per the European Travel Commission, a significant proportion of European travellers aged 18 to 45 participated in sports-related trips in recent years, which reflects a cultural shift toward experiential and active vacations. As per the European Commission’s Sustainable Tourism Strategy, sports events are increasingly integrated into destination management plans to distribute visitor flows beyond urban hotspots and support rural economies. This convergence of passion, place, and policy positions sports tourism not as a niche segment but as a dynamic engine of inclusive and resilient tourism across Europe.

MARKET DRIVERS

Hosting of Major International Sporting Events Drives Destination Visibility

Europe’s consistent selection as host for global sporting spectacles serves as a primary catalyst for sports tourism by generating massive visitor influxes, media exposure, and long-term destination branding, which is one of the major factors driving the growth of the European sports tourism market. As per UEFA, millions of international fans travelled to Germany for the UEFA Euro 2024, with extended stays and higher daily expenditures documented by the German National Tourist Office. Similarly, the Tour de France attracts millions of roadside spectators annually, including hundreds of thousands of international visitors who follow stages across multiple regions, injecting billions of euros into local economies as per Atout France. These events function as live advertisements. As per the European Travel Commission, host cities experience a notable increase in leisure bookings in the months following major tournaments due to heightened global awareness. Moreover, legacy infrastructure continues to draw visitors for tours and smaller events long after the main competition ends. With Europe slated to host the 2028 UEFA Euro in the UK and Ireland and the 2030 Winter Olympics potentially in the Pyrenees, this cyclical momentum ensures sustained demand and investment in sports-oriented hospitality and transport networks.

Rise of Active and Wellness-Oriented Travel Among Urban Populations

The growing emphasis on health, personal achievement, and experiential consumption among Europe’s urban middle class has intensified demand for participatory sports tourism that blends physical activity with cultural immersion, which is fuelling the sports tourism market expansion in Europe. As per the World Health Organisation, a majority of adults in high-income EU countries report insufficient physical activity, prompting many to seek structured fitness experiences during vacations. This trend fuels events like the Berlin Marathon and cycling gran fondos in Tuscany or the Alps that combine athletic challenge with gastronomy and scenery. As per the European Health and Fitness Association, wellness and active holidays grew significantly in 2023, which is outpacing traditional sun and sea packages. Destinations respond by developing certified routes, as Spain’s Camino de Santiago now offers sportive variants with GPS tracking and recovery zones, while Austria’s Tirol region markets guided ski touring weeks with physiotherapy support. As per Eurobarometer, many Europeans aged 25 to 45 consider physical activity an essential part of holiday planning. As burnout and sedentary lifestyles rise post pandemic, sports tourism evolves from leisure to therapeutic necessity, which is transforming destinations into open-air wellness clinics where movement and culture converge.

MARKET RESTRAINTS

Seasonal Concentration and Infrastructure Overload During Peak Events

Despite its economic benefits, sports tourism in Europe often suffers from acute seasonality and temporary infrastructure saturation that degrade visitor experience and strain local resources, which is hampering the European sports tourism market growth. Major events like the Tour de France, Wimbledon, or Oktoberfest concentrate millions of visitors into narrow time windows, overwhelming transport, lodging, and waste management systems. As per the French Ministry of Ecological Transition, traffic congestion in Alpine regions during winter sports peaks increases CO2 emissions compared to baseline levels, while municipal water consumption also spikes. Similarly, the city of Munich reported that public transport capacity was exceeded during the UEFA Champions League final, leading to safety concerns and service disruptions. As per a study by the University of Barcelona, resident satisfaction in event host neighbourhoods drops during peak tournaments due to noise, crowding, and price inflation. Without coordinated crowd management, sustainable mobility plans, and off-season programming, these short-term booms risk long-term resident backlash and environmental degradation, undermining the very authenticity that attracts sports tourists in the first place.

Geopolitical Instability and Security Concerns Deter International Attendance

The rising security threats and political volatility in certain European regions create significant barriers to international sports tourism despite robust event calendars, which further inhibit the European sports tourism market expansion. As per Europol, numerous major sporting events in Europe required enhanced security protocols in 2023 due to terrorism, hooliganism, or civil unrest risks. Reduced attendance at matches in Eastern European cities reflects traveller caution. As per the European Travel Commission, international bookings to host cities in conflict-adjacent regions fell in 2023 even when events proceeded as planned. Insurance costs have also surged; event organisers in France and Belgium reported increases in security premiums between 2021 and 2023 following stadium perimeter breaches and drone incursions. Moreover, visa restrictions and border controls delay entry for non-EU participants and spectators. A survey by the International Federation of Football History & Statistics revealed that overseas fans often cite safety concerns as a primary reason for skipping European matches. Until harmonised threat assessment and rapid response frameworks are implemented across Schengen states, perceived insecurity will continue to suppress demand regardless of event prestige.

MARKET OPPORTUNITIES

Development of Rural and Off-the-Beaten-Path Sports Trails

Europe presents a high-value opportunity in decentralising sports tourism through certified multi-day trails and adventure circuits that revitalise depopulated regions and reduce pressure on urban hotspots. As per the European Commission’s Sustainable Tourism Strategy, initiatives under the “Cultural Routes” and “Green Lanes” programs support rural economies and biodiversity conservation. Spain’s Via Verde network attracted over a million visitors in 2023, with many staying in local guesthouses as per the Spanish Institute for Tourism. Similarly, Norway’s Trolltunga and Preikestolen hikes generate year-round trekking tourism in fjord communities that previously relied on seasonal fishing. The Alpine Pearls cooperative markets guided ski mountaineering and trail running weeks with zero-emission transport links, achieving strong repeat visitor rates according to the Austrian tourism boards. As per the OECD, rural sports tourism generates significantly more local employment per euro spent than urban mass tourism due to higher use of family-run services. As travellers seek authenticity and solitude, these curated experiences transform remote landscapes into resilient economic assets aligned with EU cohesion and climate goals.

Integration of Esports and Hybrid Fan Experiences

The convergence of physical and digital sports fandom opens new avenues for tourism through hybrid events that blend live attendance with immersive technology, which is another major opportunity in the European sports tourism market. As per the European Esports Federation, millions of Europeans attended hybrid gaming tournaments in 2023, where fans watched professional matches in arenas while participating in VR challenges or meet and greets with streamers. Cities like Paris and Berlin now host “fan zones” during traditional events that feature augmented reality player stats, interactive skill games, and digital merchandise booths. The UEFA Champions League Final 2023 in Istanbul included a dedicated esports pavilion where attendees played FIFA simulations against real athletes, extending dwell time as measured by Turkish tourism authorities. Moreover, national federations partner with travel agencies to offer “behind the scenes” packages that leverage athlete influence to drive bookings. As per Deloitte, hybrid sports tourists spend considerably more than passive spectators due to premium add-ons. As Generation Z blurs the line between virtual and physical engagement, these integrated experiences position Europe at the forefront of next-generation sports tourism innovation.

MARKET CHALLENGES

Overtourism in Iconic Sports Destinations Erodes Local Support

The concentration of sports tourism in a handful of globally recognised venues has triggered resident fatigue and policy backlash that threaten long term viability, which is a major challenge to the growth of the European sports tourism market. As per the Barcelona City Council, match days at FC Barcelona’s stadium generate large surges in visitors, overwhelming public transport and inflating rental prices in the Les Corts district. Similar tensions exist in Munich, where Oktoberfest and Bayern Munich matches coincide, straining emergency services and waste collection. As per a survey by the European Urban Knowledge Network, many residents in iconic sports neighbourhoods support caps on event attendance to preserve the quality of life. Some cities have responded with measures like Amsterdam’s ban on large group tours to Ajax matches or Rome’s restrictions on Champions League fan gatherings near historic sites. Without equitable benefit sharing, community engagement, and visitor dispersion strategies, the very popularity of these destinations risks triggering regulatory clampdowns that could curtail event hosting rights and diminish Europe’s competitive edge in global sports tourism.

Fragmented Visa and Entry Requirements Across Schengen and Non-Schengen States

Despite the Schengen Area’s open borders, inconsistent visa policies and documentation demands for non-EU sports tourists create friction that suppresses attendance at transnational events, which is further challenging the European sports tourism market growth. As per the International Air Transport Association, travellers attending multi-country tournaments like the Tour de France or UEFA Euro must navigate divergent entry rules if routes cross Schengen and non-Schengen territories. For instance, fans travelling from the UK to France for Euro 2024 faced no visa requirements, but those continuing to Ireland needed separate authorisation, which is a complexity that deterred some potential attendees as per VisitBritain data. Moreover, processing delays persist; applicants from key growth markets such as India and Brazil reported average visa wait times of several weeks in 2023, conflicting with last-minute ticket purchases common in sports tourism. As per the European Travel Commission, non-EU sports tourists cite entry complexity as one of the most common barriers after cost, reducing conversion rates from interest to actual travel. While the upcoming ETIAS system aims to streamline pre-clearance, its implementation delays and fee structures may further discourage spontaneous attendance. Until Europe adopts unified event-specific fast-track protocols for verified ticket holders, administrative hurdles will continue to limit the full global reach of its premier sporting calendar.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 16.42% |

| Segments Covered | By Sports Type, Tourism Type, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | TUI Group, Thomas Cook Sports, Sports Tours International, Gullivers Sports Travel, Keith Prowse Travel, Matchday International, Champions Travel, Eventeam Group, Gullivers Travel Group, P1 Travel, Sportsnet Holidays, Travel Counsellors Sports, Inspire Sport, EuroSport Travel, World Soccer Travel |

SEGMENTAL ANALYSIS

By Sports Type Insights

The soccer/football segment dominated the sports tourism market in Europe in 2025 by holding 60.6% of the regional market share. The dominance of the soccer/football segment in the European market is attributed to the sport’s deep cultural entrenchment, continent‑wide supporter bases, and dense calendar of elite club and international competitions that draw global audiences. One key driver is the unparalleled scale and frequency of high-profile football events across Europe. As per UEFA, millions of international fans travelled to attend domestic league matches in the “Big Five” leagues in 2023, with average per-trip spending exceeding 1,200 euros according to national tourism boards. Iconic stadiums like Camp Nou, Old Trafford, and Allianz Arena operate year-round stadium tours and museum visits, attracting millions of visitors annually as per Deloitte’s Football Money League. Major tournaments amplify this effect; the 2024 UEFA Euro in Germany drew millions of overseas spectators, many of whom extended their stays to explore host cities. Furthermore, football’s emotional resonance drives repeat visitation. As per the European Travel Commission, a majority of international football tourists plan return trips to follow their team’s away fixtures. With over 500 professional clubs across top-tier leagues and fixtures every week for nine months of the year, football provides unmatched consistency and passion in the European context.

The tennis segment is the fastest-growing and is anticipated to exhibit a CAGR of 10.4% over the forecast period, owing to the sport’s premium positioning, global star power, and integration into luxury travel experiences beyond match viewing. A major factor is the rise of experiential packages centred around Grand Slam and ATP/WTA tournaments that blend world-class competition with high-end hospitality. As per Atout France, the French Open at Roland Garros generated hundreds of thousands of international visitor nights in Paris during May 2023, with many bookings of premium packages including player meet and greets, court-side clinics, and fashion collaborations. Similarly, Wimbledon’s reputation for tradition and exclusivity drives demand for ticket lotteries and bespoke London itineraries. VisitBritain reports that Wimbledon fortnight accounts for a notable share of June luxury hotel bookings in the capital. The sport’s demographic appeal—skewing affluent, educated, and female—aligns with high-value tourism segments. Moreover, tennis federations actively promote training camps; the Spanish Tennis Federation hosts thousands of international juniors annually at its academies in Barcelona and Valencia, combining coaching with cultural immersion. As per the International Tennis Federation, tennis tourists spend significantly more per day than average leisure travellers due to premium accommodation, dining, and retail. As destinations leverage tennis’ elegance and global reach, the segment transitions from spectator event to lifestyle destination anchor across Europe.

By Tourism Type Insights

The passive tourism segment commanded the highest share of 55.8% of the regional market in 2025. The dominance of the passive tourism segment in the European market is driven by the massive global audience drawn to spectate elite competitions without direct participation, leveraging Europe’s concentration of world-class stadiums, leagues, and historic rivalries. A primary driver is the emotional and cultural magnetism of watching live football, rugby, and tennis in iconic venues where history unfolds in real time. As per the European Travel Commission, millions of international visitors attended spectator sports events in Europe in 2023, with football accounting for the majority of volumes. Events like the UEFA Champions League final, El Clásico, or the Six Nations rugby championship generate intense demand for tickets, hospitality suites, and city breaks centred entirely around match day experience. National tourism agencies capitalise on this. As per Spain’s Turespaña, match day tourism contributed billions of euros to the economy in 2023, with visitors spending heavily on hotels, restaurants, and merchandise. The social nature of passive tourism also fuels group travel. As per Amadeus, most sports event bookings involve parties of three or more, amplifying economic impact. With Europe hosting more top-tier leagues and annual tournaments than any other region, passive spectating remains the bedrock of sports tourism volume and revenue across the continent.

The active tourism segment is projected to grow at a CAGR of 12.2% over the forecast period due to the rising health consciousness, experiential travel trends, and the proliferation of organised participatory events that blend athleticism with cultural discovery. Marathons, cycling gran fondos, and amateur football tournaments now serve as primary travel motivators for millions of Europeans and international visitors alike. The Berlin Marathon attracted tens of thousands of runners from over 100 countries in 2023, with most accompanied by friends or family who also stayed multiple nights, as per Berlin Tourism Office data. Similarly, the Maratona delle Dolomites in Italy draws thousands of cyclists annually through a lottery system, generating tens of thousands of visitor nights in South Tyrol during a single weekend. Destinations actively develop certified routes; France’s La Loire à Vélo cycling path spans hundreds of kilometres and hosted hundreds of thousands of active tourists in 2023, many of whom were international, as documented by Atout France. As per the European Health and Fitness Association, active holiday participants report higher satisfaction scores than passive tourists due to personal achievement and deeper local engagement. As wellness and purpose-driven travel intensify, active sports tourism evolves from a niche pursuit to a mainstream driver of sustainable off-season visitation across rural and urban Europe.

REGIONAL ANALYSIS

United Kingdom Sports Tourism Market Analysis

The United Kingdom held 20.9% of the European market share in 2025. The dominance of the UK in the European market is attributed to its concentration of globally revered football clubs, elite tennis and rugby institutions, and robust event infrastructure. As per VisitBritain, millions of international visitors attended English Premier League matches in 2023, with average per-trip spending exceeding 1,400 euros. Wimbledon generates hundreds of thousands of high-value tourist nights annually in London, while Twickenham Stadium hosts Six Nations matches that fill hotels across southwest England. The UK’s strength lies in year-round programming to ensure consistent demand. Heritage also plays a key role; stadium tours at Old Trafford, Anfield, and Wembley drew millions of visitors in 2023, many combining sport with cultural sightseeing. Despite Brexit, the UK maintains strong air connectivity and visa-free access for most key markets, ensuring continued global appeal as Europe’s premier destination for both passive spectating and active participation in world-class sporting environments.

Spain Sports Tourism Market Analysis

Spain had the second-largest share of the European sports tourism market in 2025. The growth of Spain in the European sports tourism market can be credited to its football supremacy, diverse climate, and integration of sport with the Mediterranean lifestyle. As per Spain’s National Institute of Statistics, millions of international fans attended La Liga matches in 2023, with Camp Nou tours alone attracting over a million visitors. Beyond football, Spain excels in active tourism as the Vuelta a España cycling race traverses multiple regions annually, while marathons in Valencia and Seville rank among Europe’s fastest-growing. The Spanish Tennis Federation’s academies in Barcelona host thousands of junior athletes yearly, fostering long-term engagement. Spain also leverages sport for seasonal balance; ski resorts in the Pyrenees and Andalusian golf courses attract winter sports tourists, offsetting summer beach dependency. As per Turespaña, sports tourists stay longer than average leisure visitors and spend significantly more on local services. With universal appeal across age demographics and seamless blending of competition, culture, and climate, Spain maintains exceptional depth and resilience in sports tourism demand.

France Sports Tourism Market Analysis

France is projected to grow at a promising CAGR in the European sports tourism market during the forecast period, owing to its hosting of mega events, world-class infrastructure, and strategic use of sport for territorial development. The 2024 UEFA Euro brought millions of international visitors, with matches staged in multiple cities dispersing economic benefits widely. Roland Garros contributes significantly; as per Atout France, the French Open generated hundreds of thousands of tourist nights in Paris in May 2023 with strong luxury spending. France also leads in active tourism through the Tour de France, which draws hundreds of thousands of international spectators annually along its extensive route. The government’s “Sport Tourism Plan” allocates funding to develop regional circuits like Alpine ski trails and Provence running paths, ensuring year-round activity. As per the French Ministry of Sports, sports tourism supports significant employment nationwide, with many jobs located in rural areas. With institutional coordination between tourism, sport, and transport ministries, France exemplifies how strategic event policy can transform sport into a tool for inclusive economic regeneration across urban and peripheral territories.

Germany Sports Tourism Market Analysis

Germany is anticipated to account for a notable share of the European sports tourism market during the forecast period owing to its engineering precision, fan culture, and decentralised event hosting model. The Bundesliga is renowned for affordable tickets, passionate supporters, and stadium accessibility, as these are the factors that drew millions of international visitors in 2023, as per the German National Tourist Office. The 2024 UEFA Euro further amplified visibility with matches in Berlin, Munich, and Dortmund showcasing Germany’s logistical excellence. Beyond football, Germany excels in winter sports tourism; the Bavarian Alps host FIS World Cup events that attract skiers and spectators from across Europe. The country’s federal structure ensures broad distribution, as even mid-sized cities like Leipzig and Stuttgart host international athletics and handball tournaments that fill hotels and restaurants. As per the German Sports Confederation, most sports tourists combine event attendance with cultural visits, enhancing overall economic impact. With strong rail connectivity, environmental awareness, and emphasis on fan experience rather than commercialisation, Germany offers an authentic, accessible model that resonates deeply with European and global visitors seeking genuine sporting immersion.

Italy Sports Tourism Market Analysis

Italy is expected to register a healthy CAGR in the European sports tourism market during the forecast period, owing to its fusion of sporting passion, historical grandeur, and regional diversity. Serie A clubs Juventus, AC Milan, and Inter draw hundreds of thousands of international fans annually, while the San Siro stadium tour remains a Milan must-do. Italy’s true strength lies in active and niche sports tourism; the Maratona delle Dolomites cycling event fills South Tyrol with thousands of riders and supporters each July. Historic motorsport also drives demand—the Monza Formula 1 Grand Prix and Mille Miglia classic car rally attract global enthusiasts willing to pay premium prices. The Italian National Olympic Committee promotes “sport and culture” packages linking events to UNESCO sites. As per ENIT, sports tourists in Italy often combine event attendance with cultural sightseeing, visiting multiple attractions per trip. Moreover, Italy leverages its coastline and mountains for sailing, skiing, and hiking tourism tied to local festivals. With unmatched aesthetic appeal, emotional intensity, and regional authenticity, Italy transforms every sports journey into a multisensory narrative where competition and heritage intertwine seamlessly.

COMPETITION OVERVIEW

Competition in the Europe sports tourism market is characterised by a dual structure comprising premium hospitality specialists and grassroots tour operators serving distinct but complementary segments. Incumbent leaders leverage exclusive rights with UEFA, FIFA and national federations to dominate high-value spectating experiences for elite events, benefiting from brand trust and operational scale. Meanwhile, agile niche players thrive in participatory tourism by offering authentic local immersion training camps and youth tournaments that foster emotional loyalty. The market is not price-driven but defined by access quality and experiential depth—factors that create high barriers for generic travel agencies lacking sport-specific networks. New entrants face challenges in securing official accreditation, managing logistics during peak events and ensuring safety compliance for minors. Consolidation is limited, yet collaboration with DMOs, airlines and hotels is rising to enhance package value. Ultimately, leadership is determined by the ability to blend sporting passion with seamless travel execution while contributing to sustainable destination development across Europe’s diverse cultural and geographic landscape.

KEY MARKET PLAYERS

A few major players of the Europe sports tourism market include

- TUI Group

- Thomas Cook Sports

- Sports Tours International

- Gulliver's Sports Travel

- Keith Prowse Travel

- Matchday International

- Champions Travel

- Eventeam Group

- Gulliver's Travel Group

- P1 Travel

- Sportsnet Holidays

- Travel Counsellors Sports

- Inspire Sport

- EuroSport Travel

- World Soccer Travel

Top Strategies Used by the Key Market Participants

Key players in the Europe sports tourism market pursue strategies centred on exclusivity, personalisation, and sustainability. Companies secure official partnerships with governing bodies to offer privileged access to tickets, hospitality and behind-the-scenes content that cannot be replicated by generic travel agencies. Product innovation focuses on experiential bundles that integrate sport with culture, wellness and gastronomy to increase dwell time and spending. Digital platforms enable real-time itinerary management, multilingual support, and AI-driven recommendations, enhancing convenience for international visitors. Sustainability is embedded through carbon offsetting, local sourcing and community benefit sharing to align with EU tourism guidelines. Youth and grassroots engagement build long-term loyalty by fostering early emotional connections to destinations through sport. These approaches collectively transform sports tourism from transactional event attendance to immersive lifestyle experiences that drive economic resilience and social value across Europe.

Leading Players in the Europe Sports Tourism Market

- Match Hospitality is a Swiss-based global leader in premium sports hospitality with deep integration across Europe’s elite football and tennis circuits. The company holds official hospitality rights for UEFA Champions League, UEFA Euro, and Roland Garros, offering curated experiences including match tickets, gourmet dining and player interactions. Match leverages its partnerships with national federations and stadium operators to deliver seamless end-to-end itineraries that blend sport with luxury travel. Recently, the company launched dynamic pricing algorithms and AI-driven personalisation for Euro 2024 packages, allowing real-time customisation based on fan preferences and team progression. It also expanded its sustainability program by offsetting carbon emissions for all client travel and using locally sourced catering at event venues. Through exclusive access, high service standards and data-driven engagement, Match Hospitality sets the benchmark for premium sports tourism across Europe.

- STH is a UK-headquartered specialist in end-to-end sports travel solutions serving federations, clubs and individual fans across football, rugby and tennis. The company operates official travel programs for over 30 European clubs, including Liverpool FC and Borussia Dortmund, providing ticketing, accommodation and guided tours. STH differentiates through hyperlocal expertise and community integration—offering behind the scenes acces,s such as training ground visits and academy tours that foster emotional connection. In recent years, STH enhanced its digital platform with real-time itinerary management and multilingual concierge services supporting fans from emerging markets like India and the United States. It also partnered with VisitBritain and Atout France to co-develop off-season sports heritage trails linking stadiums, museums and fan zones. By combining authenticity, operational excellence and destination storytelling, STH strengthens long-term loyalty in Europe’s experience-driven sports tourism landscape.

- Gulliver's Sports Travel is a Netherlands-based pioneer in group and youth sports tourism with a strong footprint in amateur football, basketball and volleyball across Europe. The company organises over 1 500 tournaments and training camps annually, hosting teams from more than 60 countries at its dedicated facilities in Spain, Portugal and the Netherlands. Gullivers emphasizes educational value and cultural exchange by integrating language workshops, local sightseeing, and community matches into its programs. Recently, the company launched a carbon-neutral certification for all youth tours and introduced hybrid events where virtual coaching sessions precede in-person tournaments. It also collaborated with UEFA Foundation for Children to fund participation for underprivileged teams. Through its focus on grassroots development, safe environments, and inclusive experiences, Gulliver's cultivates lifelong sports tourism habits while supporting social cohesion across European communities.

MARKET SEGMENTATION

This research report on the Europe sports tourism market has been segmented and sub-segmented based on sports type, tourism type and region.

By Sports Type

- Soccer/Football

- Cricket

- Basketball

- Tennis

By Tourism Type

- Active

- Passive

- Nostalgia

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is driving the growth of the Europe sports tourism market?

The market is driven by Europe’s strong sports culture, frequent international sporting events, advanced infrastructure, and increasing disposable income among travelers.

2. What types of sports tourism are most popular in Europe?

Event-based tourism (football, Formula 1, tennis), active sports tourism (cycling, skiing, marathons), and adventure sports tourism are the most popular.

3. Which sport contributes the highest revenue in Europe sports tourism?

Football contributes the highest revenue due to major leagues, international tournaments, and strong fan travel across countries.

4. How does mega sporting events impact the market?

Mega events such as the UEFA Championships, Olympics, and Grand Slam tournaments significantly boost inbound tourism, hotel occupancy, and local economies.

5. What role do travel agencies play in sports tourism?

Travel agencies provide bundled services including tickets, accommodation, transport, and hospitality, simplifying travel for sports fans and participants.

6. How is digitalization influencing sports tourism in Europe?

Online booking platforms, mobile apps, virtual ticketing, and digital marketing have improved accessibility, customer engagement, and trip personalization.

7. What are the key challenges faced by the Europe sports tourism market?

High travel costs, seasonality, visa restrictions, crowd management, and dependence on event schedules are major challenges.

8. What opportunities exist in the Europe sports tourism market?

Growth opportunities include niche sports tourism, sustainable travel packages, women’s sports events, and emerging adventure sports destinations.

9. How does sustainability impact sports tourism in Europe?

Eco-friendly venues, green transport, and sustainable event planning are increasingly influencing traveler preferences and policy decisions.

10. Who are the primary customers in the sports tourism market?

Sports fans, amateur athletes, professional teams, corporate travelers, and youth sports groups are the main customer segments.

11. How does seasonality affect the market?

Demand peaks during major tournaments and seasonal sports such as winter skiing, while off-season periods show lower activity levels.

12. What is the future outlook for the Europe sports tourism market?

The market is expected to grow steadily due to increasing international events, rising experiential travel demand, and innovation in sports travel services.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com