Global Generic Drugs Market Size, Share, Trends & Growth Analysis Report By Type (Pure Generic Drugs, Branded Generic Drugs), Application (Central Nervous System (CNS), Cardiovascular, Dermatology, Oncology, Respiratory and Others) and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa), Industry Analysis From 2025 to 2033

Global Generic Drugs Market Summary

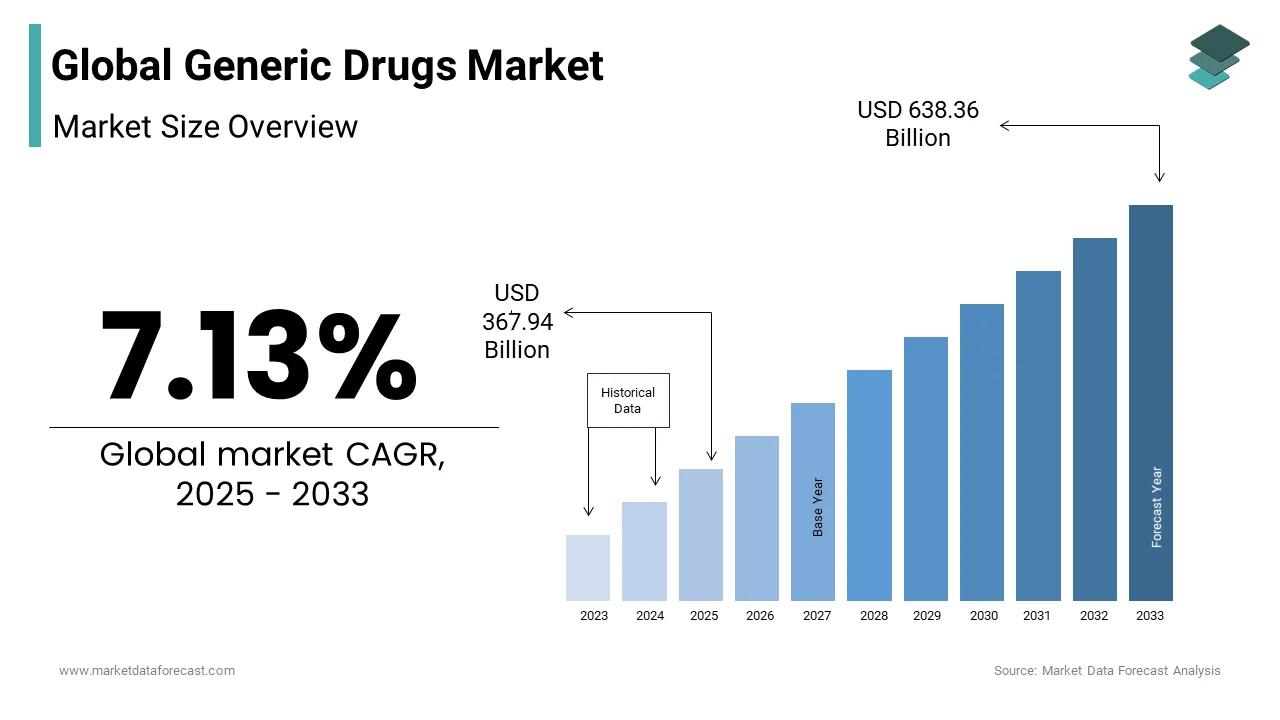

The global generic drugs market was valued at USD 343.45 billion in 2024 and is projected to reach USD 638.36 billion by 2033, growing at a CAGR of 7.13% during the forecast period. The market growth is fueled by the rising need for cost-effective treatments, patent expirations of blockbuster drugs, and the increasing prevalence of chronic diseases globally.

Key Market Trends

- Growing adoption of branded generics in emerging markets due to affordability and quality assurance.

- Expiration of patents for leading drugs, creating opportunities for generic alternatives.

- Expanding healthcare access in developing economies, boosting demand for low-cost medicines.

- Strategic collaborations and acquisitions among pharmaceutical companies to strengthen generic drug portfolios.

Segmental Insights

- Based on type, the branded generic drugs segment dominated the market in 2024, supported by higher physician trust and patient adoption compared to unbranded generics.

- Based on application, the cardiovascular drugs segment accounted for 24.7% of the global generic drugs market share in 2024, driven by the growing prevalence of heart-related disorders and the need for affordable long-term medication.

Regional Insights

- North America was the leading regional market, capturing 41.3% of the global market share in 2024, owing to favorable healthcare policies, widespread insurance coverage, and high chronic disease prevalence.

- Asia-Pacific is projected to witness the fastest growth over the forecast period, driven by expanding healthcare access, supportive government initiatives, and rising generic manufacturing capacities.

- Europe held a substantial share, supported by strong regulatory frameworks and increasing adoption of cost-effective drugs across national healthcare systems.

- Latin America shows promising growth potential, driven by government efforts to expand generic drug penetration in public healthcare.

- Middle East & Africa are experiencing gradual growth, supported by rising awareness of affordable medicines and improving healthcare infrastructure.

Competitive Landscape

Key players operating in the global generic drugs market include Ranbaxy Laboratories Ltd, Actavis, Viatris, Dr. Reddy’s Laboratories, Par Pharmaceutical Inc., Sandoz International GmbH, Hospira Inc., Apotex Inc., Pfizer Inc., and Teva Pharmaceutical.

Global Generic Drugs Market Size

In 2024, the global generic drugs market was valued at USD 343.45 billion, and it is expected to reach USD 638.36 billion by 2033 from USD 367.94 billion in 2025, growing at a CAGR of 7.13% during the forecast period.

The Generic Drugs are pharmaceutical products that are bioequivalent to innovator (brand-name) drugs in dosage form, strength, route of administration, quality, performance characteristics, and intended use. These medications emerge post-patent expiry of original compounds, enabling alternative manufacturers to produce therapeutically equivalent versions at significantly reduced costs. The foundation of this market lies in regulatory frameworks that mandate rigorous testing for bioequivalence, ensuring patient safety and efficacy parity. As per the U.S. Food and Drug Administration, generic drugs must demonstrate 80% to 125% bioequivalence to their branded counterparts under strict pharmacokinetic parameters. Similarly, in low- and middle-income countries, generics constitute more than 80% of total medicine consumption, according to the International Generic Medicines Council.

MARKET DRIVERS

Rising Prevalence of Chronic Diseases and Aging Populations

The escalating global burden of non-communicable diseases (NCDs) such as diabetes, cardiovascular disorders, and cancer is majorly propelling the growth of the Generic Drugs Market. As populations age, particularly in developed and emerging economies, the need for long-term pharmacological management intensifies, which is necessitating cost-effective treatment options. The United Nations estimates that by 2030, the number of people aged 60 years or older will reach 1.4 billion, nearly double the 2019 figure of 962 million. For instance, the International Diabetes Federation reports that in 2023, approximately 537 million adults worldwide were living with diabetes, a figure projected to rise to 643 million by 2030. Managing such conditions often requires lifelong medication by making affordability paramount. Generic versions of statins, antihypertensives, and insulin analogs have become indispensable in public health strategies.

Expanding Healthcare Access in Low- and Middle-Income Countries

The push for equitable healthcare access across developing nations has positioned generic drugs as a cornerstone of national health strategies is also driving the growth of the Generic Drugs Market. In regions where public health infrastructure is underfunded and out-of-pocket expenditures remain high, affordable medicines are essential for treatment adherence and disease control. According to the World Bank, nearly 400 million people in sub-Saharan Africa and South Asia lack access to essential medicines due to cost barriers. Generic manufacturers, particularly in India and China, have emerged as global suppliers of low-cost therapeutics by fulfilling over 60% of global demand for generic medicines, as stated by the World Health Organization.

MARKET RESTRAINTS

Stringent Regulatory Hurdles and Divergent Approval Pathways

The generic drugs face significant regulatory complexities that are impeding the growth of the market. Each country maintains distinct bioequivalence requirements, documentation standards, and inspection protocols, creating a fragmented approval landscape. The U.S. Food and Drug Administration requires an average of 38 months for generic drug approval, with over 4,000 applications pending as of 2023, according to the Generic Pharmaceutical Association. In contrast, the European Medicines Agency mandates centralized, decentralized, or national authorization routes, leading to inconsistent approval timelines across member states. Moreover, post-approval surveillance requirements, such as Good Manufacturing Practice (GMP) audits, have intensified following incidents like the 2022 WHO alert on contaminated cough syrups from India and Indonesia, which led to stricter inspections across South Asia. This disparity forces manufacturers to undergo redundant testing and compliance procedures across jurisdictions, increasing development costs and delaying patient access.

Persistent Physician and Consumer Skepticism Toward Efficacy

The healthcare providers and patients continue to question the therapeutic equivalence of generic drugs in high-stakes treatment, which also limits the growth of the Generic Drugs Market. This perception gap stems from historical incidents, brand loyalty, and limited awareness, especially in regions with underdeveloped pharmacovigilance systems. A 2022 survey by the European Federation of Pharmaceutical Industries and Associations revealed that 42% of physicians in Germany and France expressed reservations about substituting originator biologics with biosimilars, citing concerns over immunogenicity and long-term outcomes. Additionally, packaging differences, inactive ingredients, and color variations in generics contribute to patient confusion and non-adherence. The World Health Organization acknowledges that misinformation and lack of provider education significantly undermine generic acceptance, particularly in Eastern Europe and parts of Latin America.

MARKET OPPORTUNITIES

Strategic Expansion into the Emerging Biosimilars Market

The expiration of patents on high-cost biologic drugs, which combine the principles of generic equivalence with advanced biotechnology, is leveraging new opportunities for the growth of the Generic Drugs Market. Companies like Sandoz, Biocon, and Celltrion are already capitalizing on this shift, with biosimilar versions of drugs like adalimumab and trastuzumab gaining regulatory approval in multiple jurisdictions. The U.S. Food and Drug Administration has approved over 40 biosimilars as of 2023, leading to average savings of 30% per treatment course, as reported by the Congressional Budget Office. Emerging markets are also advancing; South Korea’s Ministry of Food and Drug Safety approved 18 biosimilars between 2020 and 2023, fostering domestic production. Additionally, India’s biopharma sector has invested over $2.5 billion in biosimilar R&D since 2020, as stated by the Department of Biotechnology.

Digitalization and AI-Driven Drug Development

The integration of artificial intelligence and digital technologies into generic drug development is revolutionizing efficiency, accuracy, and time-to-market, which is amplifying the growth of the Generic Drugs Market. Traditional generic development involves extensive bioequivalence studies, formulation optimization, and regulatory documentation, often spanning years. However, AI-powered platforms are now enabling predictive modeling of drug dissolution, stability, and pharmacokinetics, drastically reducing trial-and-error experimentation. As per a 2023 report by McKinsey & Company, pharmaceutical companies leveraging machine learning in formulation design have reduced development timelines by up to 40%. For instance, companies like Teva and Dr. Reddy’s are deploying AI algorithms to simulate in vivo performance from in vitro data, accelerating ANDA (Abbreviated New Drug Application) submissions. Digital twin technology, used by firms such as Sun Pharma, allows virtual testing of manufacturing processes, minimizing batch failures and ensuring regulatory compliance. Furthermore, blockchain-based supply chain tracking is enhancing transparency, particularly in global distribution networks.

MARKET CHALLENGES

Intensifying Price Erosion Due to Hypercompetition

The generic pharmaceutical sector is increasingly characterized by aggressive price competition in saturated markets where multiple manufacturers target the same off-patent molecules is restricting the growth of the Generic Drugs Market. Once a drug loses exclusivity, the entry of numerous generic producers often triggers a rapid decline in pricing, sometimes exceeding 90% within the first year of launch. According to the U.S. Federal Trade Commission, the average price of a generic drug drops by 70% upon the entry of the second competitor and by over 90% when five or more firms enter the market. In India, the National Pharmaceutical Pricing Authority reported that prices of 100 key generic formulations fell by an average of 58% between 2019 and 2023 due to oversupply and bidding wars in government tenders. Similarly, in the European Union, public procurement systems based on lowest-price bidding have driven profit margins below 10% for many manufacturers, as noted by the European Generic Medicines Association. This pricing pressure is exacerbated by consolidation among pharmacy chains and group purchasing organizations, which wield significant negotiating power.

Supply Chain Vulnerabilities and Raw Material Dependence

The heavy reliance on a concentrated supply of active pharmaceutical ingredients (APIs) is likely to hinder the growth of the Generic Drugs Market. As per the U.S. Food and Drug Administration, over 80% of API manufacturing facilities for generic drugs sold in the United States are located in these two countries. This dependency was starkly exposed during the COVID-19 pandemic when lockdowns in China disrupted the supply of antibiotics and antihypertensives, leading to shortages in over 20 countries, according to the World Health Organization. India, despite being the largest exporter of finished generic doses, imports nearly 68% of its APIs from China, as stated by the Indian Drug Manufacturers’ Association. Geopolitical tensions, trade restrictions, and environmental regulations further amplify these risks. In 2023, China’s environmental crackdown on chemical manufacturers in Zhejiang province led to a 40% spike in the price of certain beta-lactam intermediates, affecting global amoxicillin production. Additionally, the European Commission identified 120 essential medicines as being at high risk of shortage due to single-source API dependency.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Analysed | By Type, Application, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Analysed | North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

| Market Leaders Profiled | Ranbaxy Laboratories, Ltd, Actavis, Viatris, Dr. Reddy’s Laboratories, Par Pharmaceutical, Inc., Sandoz International GmbH, Hospira, Inc., Apotex, Inc., Pfizer Inc., and Teva Pharmaceuticals. |

SEGMENTAL ANALYSIS

By Type Insights

The branded generic drugs segment accounted in holding a dominant share of the Generic Drugs Market in 2024, with its strategic positioning as a hybrid model by offering cost advantages over originator brands while maintaining brand equity through differentiated packaging, marketing, and perceived quality assurance. A 2022 survey conducted by the Indian Medical Association revealed that 74% of physicians in India prefer prescribing branded generics due to confidence in the manufacturer’s reputation and consistent product quality. Companies such as Dr. Reddy’s, Cipla, and Sun Pharma have built robust brand equity over decades, enabling them to command premium pricing within the generic segment. In Indonesia, branded generics occupy over 70% of retail pharmacy shelves, as noted by the Indonesian Pharmaceutical Association, largely because prescribers associate them with reliable efficacy and safety. Moreover, in countries like Egypt and Nigeria, where counterfeit medicines constitute up to 30% of the market according to the World Health Organization, branded generics serve as a trusted alternative.

The branded generic manufacturers leverage sophisticated marketing strategies and expansive distribution infrastructures, is also hinders the growth of the Generic Drugs Market. Unlike pure generics, which rely on tender-based procurement and price competition, branded generics benefit from direct engagement with healthcare providers, detailing teams, and promotional campaigns. Additionally, in Eastern Europe, companies like KRKA and Polpharma utilize established hospital supply networks to ensure consistent product placement.

The pure segment is likely to grow with expected to grow with a CAGR of 9.3% from 2025 to 2033. The surge in pure generic adoption is largely propelled by national health systems prioritizing fiscal efficiency through mandatory generic substitution and bulk purchasing. In the United States, the Veterans Health Administration achieved a 94% generic dispensing rate in 2023 by exclusively procuring pure generics through competitive bidding, resulting in annual savings exceeding $10 billion, as reported by the U.S. Department of Veterans Affairs. In China, the National Reimbursement Drug List now mandates the use of pure generics in public hospitals for over 300 off-patent molecules, contributing to a 40% reduction in outpatient drug spending between 2020 and 2023, as stated by the National Healthcare Security Administration. These policy-driven shifts diminish the influence of branding and elevate price and bioequivalence as primary selection criteria, creating fertile ground for pure generic manufacturers.

By Application Insights

The cardiovascular drugs segment in the generic pharmaceutical market by capture 24.7% of share in 2024. Cardiovascular conditions affect over 520 million people globally, with hypertension alone impacting 1.3 billion individuals, according to the World Heart Federation. Generic statins such as atorvastatin and simvastatin, along with ACE inhibitors like lisinopril, dominate prescription volumes. In the United States, generic versions of atorvastatin account for 92% of all statin prescriptions, saving the healthcare system an estimated $200 billion since 2012, as reported by the FDA. In Japan, where 40% of adults over 40 suffer from hypertension, the government’s aggressive generic promotion policy has driven the cardiovascular generic penetration rate to 86.4% in 2023, according to the Pharmaceuticals and Medical Devices Agency. Similarly, in Brazil, the Ministry of Health distributed over 1.1 billion units of generic antihypertensives in 2022 through its Farmácia Popular program, ensuring widespread access.

The oncology segment is projected to grow at a CAGR of 10.8% from 2025 to 2033. The oncology pipeline is witnessing a wave of biosimilar launches following the patent expiry of blockbuster biologics. Roche’s Rituxan (rituximab), Herceptin (trastuzumab), and Avastin (bevacizumab) collectively generated over $25 billion in global sales in 2022, but all have lost exclusivity in major markets. As of 2023, the U.S. FDA has approved 12 oncology biosimilars, including six versions of trastuzumab, leading to price reductions of up to 40%, according to the RAND Corporation. In Europe, biosimilar trastuzumab captured 85% of the market in Germany and 78% in the UK within three years of launch, as reported by the European Commission. India’s Biocon and South Korea’s Celltrion have become key global suppliers, with Biocon’s trastuzumab biosimilar reaching 70 countries by 2023.

REGIONAL ANALYSIS

North America Generic Drugs Market Insights

North America was the largest contributor in the global generic drugs market with 41.3% of the share in 2024. The United States has a highly structured healthcare system that emphasizes cost efficiency and regulatory rigor. The U.S. generic dispensing rate reached 92.6% in 2023, the highest globally, according to the Association for Accessible Medicines. This is supported by a robust Abbreviated New Drug Application (ANDA) pathway managed by the FDA, which approved over 800 generic drugs in 2023 alone. Medicare Part D and private insurers incentivize generic use through tiered copayment structures by ensuring patient adherence.

Europe Generic Drugs Market Insights

Europe was positioned second by accounting for 26.8% of the global generic drugs market in 2024. The region exhibits a dichotomy between Western and Eastern Europe in terms of generic adoption. Countries like Germany, the UK, and France have well-established generic frameworks, with Germany achieving an 84% generic dispensing rate in 2023, as reported by the German Federal Statistical Office. The EU’s centralized approval system via the EMA has streamlined market access, while national policies such as France’s “100% Santé” initiative mandate generic substitution at the pharmacy level. However, in Southern and Eastern Europe, economic constraints and fragmented healthcare systems limit uptake. Greece and Portugal rely heavily on generics due to austerity measures, whereas Poland and Romania face supply chain inefficiencies. The European Commission’s Pharmaceutical Strategy for Europe, launched in 2023 that aims to reduce dependency on third-country API suppliers and accelerate biosimilar adoption, which is positioning the region for moderate but steady growth.

Asia-Pacific Generic Drugs Market Insights

The Asia-Pacific generic market is lucratively growing with a prominent CAGR in the coming years. India alone produces over 20% of the world’s generic drug volume, exporting to more than 200 countries, according to the Indian Brand Equity Foundation. The region benefits from low manufacturing costs, a skilled workforce, and supportive government policies such as India’s Production Linked Incentive (PLI) scheme, which allocated $2 billion to boost API and formulation production. China’s 14th Five-Year Plan prioritizes self-reliance in pharmaceuticals, reducing API imports by 15% between 2021 and 2023, as reported by the National Medical Products Administration. Additionally, rising domestic healthcare spending in Indonesia, Vietnam, and Thailand is expanding local markets. However, regulatory heterogeneity and quality concerns persist, particularly in Southeast Asia, requiring sustained investment in compliance and innovation.

Latin America Generic Drugs Market Insights

Latin America's generic drugs market is anticipated to grow in the coming years, with Brazil’s government distributing over 1.5 billion generic drug units annually through its public health network, as noted by the Brazilian Health Regulatory Agency (ANVISA). Mexico’s 2022 healthcare reform mandated the use of generics in public hospitals, increasing their market share to 58% by volume. However, economic volatility, import dependencies, and weak intellectual property enforcement hinder growth.

Middle East and Africa Generic Drugs Market Insights

Middle East and Africa global generic market is likely to have steady growth opportunities during the forecast period. Egypt’s Ministry of Health procured $1.2 billion worth of generic drugs in 2023 to combat hepatitis C and diabetes, achieving a 75% reduction in treatment costs. South Africa’s Medicines Control Council approved 300 generic dossiers in 2022, focusing on HIV and TB therapies. However, infrastructure gaps, political instability, and reliance on imports from India and China constrain scalability. The African Union’s Agenda 2063 includes pharmaceutical self-sufficiency as a strategic goal, with countries like Kenya and Rwanda investing in local manufacturing.

COMPETITIVE LANDSCAPE

Key Market Participants

A few of the notable market participants operating in the global generic drugs market profiled in the report include

-

Ranbaxy Laboratories, Ltd

-

Actavis

-

Viatris

-

Dr. Reddy’s Laboratories

-

Par Pharmaceutical, Inc.

-

Sandoz International GmbH

-

Hospira, Inc.

-

Apotex, Inc.

-

Pfizer Inc.

-

Teva Pharmaceutical

-

Others

TOP LEADING PLAYERS IN THE GENERIC DRUGS MARKET

Teva Pharmaceutical Industries Ltd.

Teva stands as a pioneering force in the global generic pharmaceutical landscape, renowned for its extensive portfolio spanning chronic and acute therapeutic areas. The company has built a reputation for operational scale and regulatory compliance, serving markets across North America, Europe, and Asia. Its commitment to expanding access to affordable medicines is reflected in its robust research and development infrastructure, which focuses on complex generics and specialty formulations. Teva’s integration of biosimilars into its core offerings has positioned it at the forefront of next-generation generic therapeutics. The company maintains strong relationships with healthcare systems and payers, enabling widespread distribution through both public and private channels. Its strategic emphasis on supply chain resilience and quality assurance has solidified its role as a trusted provider in highly regulated environments.

Sandoz International GmbH

Sandoz, a wholly owned subsidiary of Novartis, operates as a dedicated global leader in generics and biosimilars, distinguished by its scientific rigor and innovation-driven approach. The company has consistently advanced the development of high-barrier-to-entry products, including sterile injectables, inhalation therapies, and biosimilar monoclonal antibodies. Sandoz emphasizes sustainability and ethical manufacturing, aligning its operations with global health priorities. Its presence across diverse geographies allows it to respond effectively to regional healthcare demands while maintaining adherence to international quality standards. The company actively collaborates with regulatory bodies and healthcare providers to promote confidence in generic medicines. Following its planned spin-off from Novartis, Sandoz aims to function as an independent entity with enhanced agility by focusing on long-term growth through technological advancement and therapeutic differentiation.

Sun Pharmaceutical Industries Ltd.

Sun Pharma has emerged as a dominant player from the emerging markets, leveraging its strong R&D capabilities and global footprint to deliver high-quality generic medicines. The company excels in developing complex dosage forms and niche therapeutics, particularly in dermatology and specialty care. Its vertically integrated model ensures control over the value chain, from active pharmaceutical ingredients to finished formulations. Sun Pharma’s strategic acquisitions have expanded its presence in regulated markets by allowing it to compete effectively with Western counterparts.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One major strategy employed by leading generic drug manufacturers is the pursuit of complex and high-barrier-to-entry products. By focusing on difficult-to-manufacture formulations such as sterile injectables, transdermal patches, and inhalation systems, companies differentiate themselves from competitors engaged in price-driven commoditization. These products require advanced technical expertise, specialized facilities, and rigorous regulatory validation, limiting competition and enabling sustainable margins. Firms invest heavily in formulation science and process engineering to overcome bioequivalence challenges and ensure consistent product performance. This approach not only reduces exposure to hypercompetitive markets but also aligns with healthcare systems seeking reliable alternatives to branded specialty drugs. The emphasis on complexity allows companies to secure long-term supply contracts and establish themselves as preferred vendors in regulated environments.

Another key strategy is vertical integration across the pharmaceutical value chain. Leading players are increasingly acquiring or developing capabilities in active pharmaceutical ingredient (API) manufacturing, formulation development, and packaging to reduce dependency on external suppliers. This integration enhances control over quality, supply continuity, and cost efficiency, particularly in times of geopolitical or logistical disruptions. Furthermore, vertical integration strengthens resilience against raw material shortages and enables faster scale-up of new products. This holistic control over production fosters trust among healthcare providers and strengthens competitive positioning in both mature and emerging markets.

Another strategic focus is geographic diversification and market expansion into underserved regions. Companies are intensifying efforts to penetrate low- and middle-income countries where access to affordable medicines remains a challenge. This expansion is supported by tailored product portfolios that address region-specific disease burdens such as infectious diseases, cardiovascular conditions, and diabetes. Additionally, participation in global health initiatives and tenders from multilateral organizations enhances visibility and credibility. Entering new markets also mitigates risks associated with regulatory changes or pricing pressures in mature regions.

COMPETITION OVERVIEW

The competitive landscape of the generic drugs market is characterized by a blend of strategic sophistication and relentless pressure. While the sector is inherently price-sensitive, leading players are shifting away from pure cost competition toward differentiation through innovation, quality, and specialization. The market features a mix of large multinational corporations, regional powerhouses, and nimble specialty-focused firms, each vying for dominance in distinct therapeutic and geographic niches. Intense rivalry persists in saturated markets where multiple manufacturers target the same off-patent molecules, often resulting in aggressive pricing and margin compression. However, a growing number of companies are carving out sustainable advantages by focusing on complex generics, biosimilars, and difficult-to-manufacture formulations that require advanced technical capabilities. Regulatory compliance and supply chain reliability have become differentiators, especially in regions with stringent oversight. Companies that maintain consistent quality, adhere to international standards, and demonstrate transparency in manufacturing practices gain preferential access to public tenders and private contracts. Strategic mergers, acquisitions, and partnerships are increasingly common by enabling firms to expand portfolios, enter new markets, and enhance R&D capabilities.

RECENT MARKET DEVELOPMENTS

- In January 2024, Sandoz announced the completion of its separation from Novartis, establishing itself as an independent publicly traded company focused exclusively on generics and biosimilars. This strategic move is anticipated to enhance operational agility and allow Sandoz to pursue targeted investments in high-growth therapeutic areas.

- In March 2024, Teva Pharmaceutical Industries launched a new digital platform to streamline regulatory submissions and improve supply chain transparency across its global manufacturing network. This initiative is expected to strengthen compliance and accelerate time-to-market for new generic products.

- In February 2024, Sun Pharmaceutical Industries entered into a strategic collaboration with a European biotech firm to co-develop a pipeline of complex generic injectables. This partnership aims to expand Sun Pharma’s presence in the sterile formulations segment and enhance its innovation portfolio.

- In May 2024, Aurobindo Pharma received final approval from a major regulatory authority for a portfolio of respiratory generics, enabling market entry in a highly regulated region. This approval is expected to broaden the company’s therapeutic reach and strengthen its international footprint.

- In April 2024, Dr. Reddy’s Laboratories inaugurated a new advanced manufacturing facility dedicated to biosimilar development in India. This expansion is anticipated to boost production capacity and reinforce the company’s position in the high-growth biosimilars segment.

MARKET SEGMENTATION

This research report on the global generic drugs market has been segmented and sub-segmented based on type, application, and region.

By Type

- Pure Generic Drugs

- Branded Generic Drugs

By Application

- The Central Nervous System (CNS)

- Cardiovascular

- Dermatology

- Oncology

- Respiratory

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What was the value of the global generic drugs market in 2024

The global generic drugs market size was valued at USD 343.45 billion in 2024.

2. Which segment by application held the largest share in the generic drugs market?

Based on the application, the CVD segment led the generic drugs market in 2024.

3. Who are the major players in the generic drugs market?

Ranbaxy Laboratories, Ltd, Actavis, Mylan, Inc., Industries, Ltd., Dr. Reddy’s Laboratories, Par Pharmaceutical, Inc., Sandoz International GmbH, Hospira, Inc., Apotex, Inc., Watson Pharmaceuticals, Ltd., Teva Pharmaceutical are some of the noteworthy players in the global generic drugs market.

4. How do generic drugs in the Global Generic Drugs Market achieve bioequivalence with branded medications?

Generic drugs in the Global Generic Drugs Market match their branded counterparts in active ingredient, strength, dosage form, and route, passing rigorous bioequivalence tests required for regulatory approval.

5. What are the main therapeutic areas targeted by the Global Generic Drugs Market?

Key areas include cardiovascular, oncology, central nervous system, dermatology, and respiratory diseases, accounting for a major share of prescriptions in the Global Generic Drugs Market.

6. How do government policies influence the Global Generic Drugs Market?

Supportive policies, like incentives for generic prescribing and price controls, play a critical role in increasing accessibility, reducing health expenses, and driving volume within the Global Generic Drugs Market.

7. Who are the top players in the Global Generic Drugs Market?

Top players include Teva Pharmaceuticals, Mylan NV, Novartis AG, Pfizer Inc., Sun Pharmaceutical, Lupin, and Hikma Pharmaceuticals, driving innovation and manufacturing scale in the Global Generic Drugs Market.

8. What is the process for a drug to enter the Global Generic Drugs Market after patent expiration?

After a patent expires, generic companies file an ANDA, demonstrating that the product is bioequivalent to the branded version, which allows for legal market entry and fuels competition in the Global Generic Drugs Market.

9. Why are drugs in the Global Generic Drugs Market more affordable than branded drugs?

In the Global Generic Drugs Market, companies save on R&D, marketing, and licensing costs, enabling them to offer medications at substantially lower prices while maintaining quality and effectiveness.

10. How do biosimilars fit into the Global Generic Drugs Market landscape?

Biosimilars, highly similar to original biologic drugs, represent a rapidly growing sub-segment within the Global Generic Drugs Market, especially for complex therapies in oncology and autoimmune diseases.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com