Global Smoothies Market Size, Share, Trends & Growth Forecast Report By Product (Fruit-based, Dairy-based and Others), Distribution Channel, Region, and Industry Analysis from 2026 to 2034

Global Smoothies Market Summary

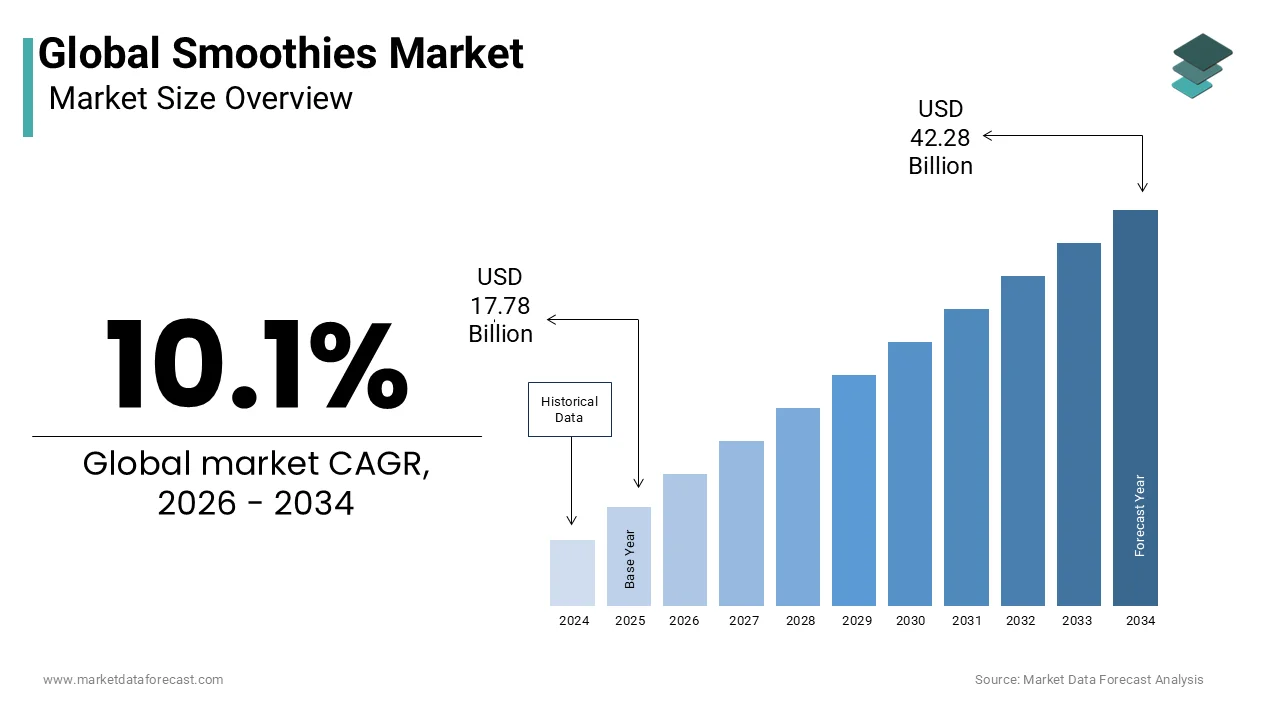

The global smoothies market was valued at USD 17.78 billion in 2025 and is projected to grow to USD 19.58 billion in 2026 and further reach USD 42.28 billion by 2034, expanding at a CAGR of 10.1% during the forecast period. The increasing consumer demand for healthy, convenient, and nutrient-rich beverages, alongside the rising popularity of plant-based and functional food trends are contributing to the growth of the global smoothies market.

Key Market Trends

- Rising consumer adoption of health and wellness beverages as meal replacements.

- Strong growth of plant-based and dairy-free smoothies in vegan and lactose-intolerant populations.

- Expansion of ready-to-drink (RTD) smoothie products through retail and online channels.

- Increasing penetration of functional ingredients like proteins, probiotics, and superfoods in smoothies.

Segmental Insights

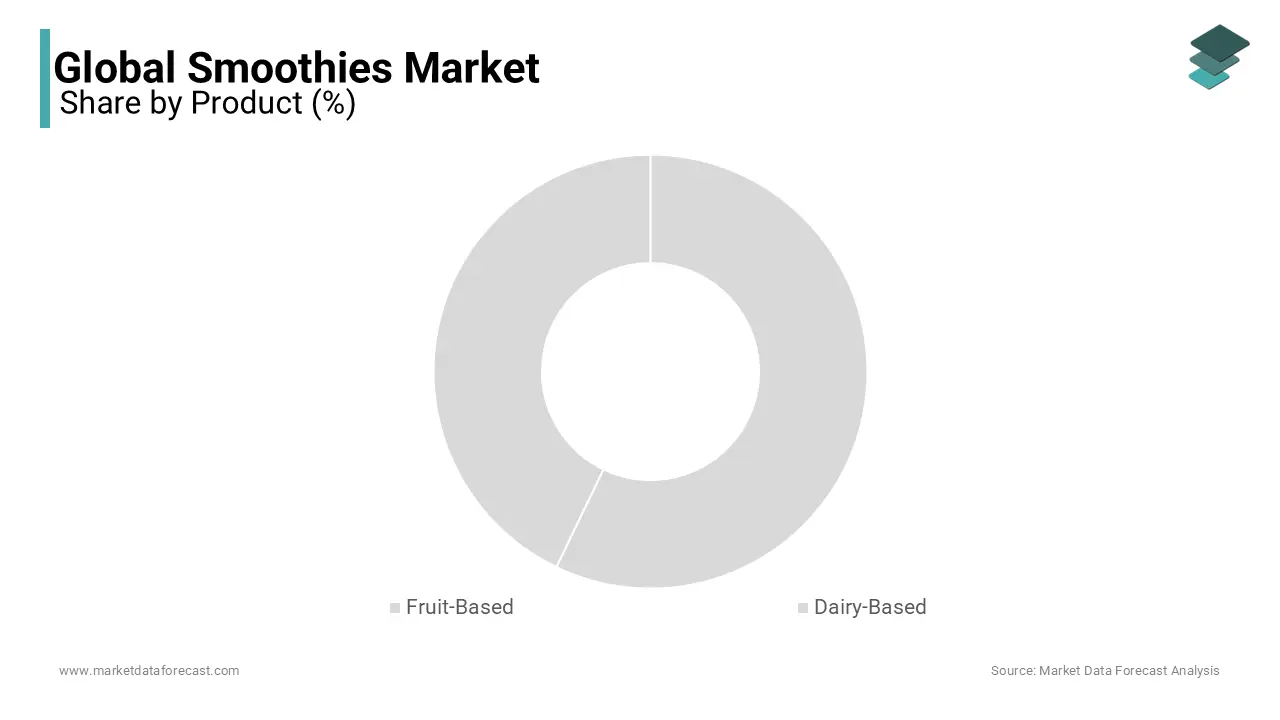

- Based on product, the fruit-based smoothies segment dominated the global market with 58.3% share in 2025, supported by strong demand for natural flavors and health-focused formulations.

- Based on distribution channel, supermarkets accounted for the largest share at 47.5% in 2025, benefiting from wide accessibility, strong retail presence, and diverse product offerings.

Regional Insights

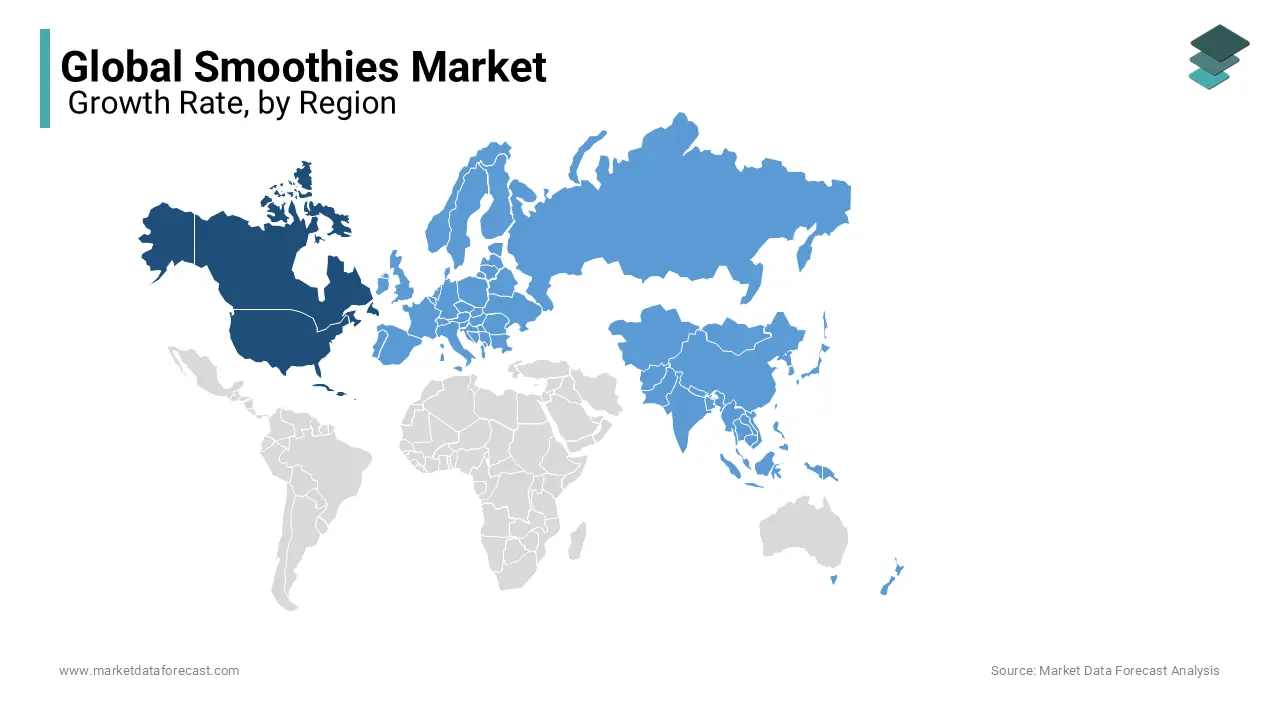

- North America was the largest contributor, capturing 42.3% of the global smoothies market in 2025, driven by health-conscious consumers, well-established smoothie chains, and innovative product launches.

- Europe held a substantial share, supported by rising demand for organic beverages and premium functional drinks.

- Asia-Pacific is forecasted to be the fastest-growing region, fueled by urbanization, growing disposable incomes, and increasing adoption of Western dietary habits.

- Latin America shows notable growth potential, backed by strong consumption of fruit-based beverages and local ingredient availability.

- The Middle East & Africa are experiencing steady growth, with consumers increasingly opting for nutritious and convenient beverage options.

Competitive Landscape

Key players in the global smoothies market include PepsiCo, Inc., Smoothie King, Maui Wowi Hawaiian Coffees & Smoothies, Suja Juice, Innocent Drinks, Bolthouse Farms, Jamba Juice Company, Ella’s Kitchen Ltd, Barfresh Food Group, Tropical Smoothie Cafe, and others.

Global Smoothies Market Size

The size of the global smoothies market was valued at USD 17.78 billion in 2025, and the global smoothies market size is expected to reach USD 42.28 billion by 2034 from USD 19.58 billion in 2026. The market's promising CAGR for the predicted period is 10.1%.

MARKET DRIVERS

Rising Consumer Focus on Preventive Health and Nutritional Supplementation

The growing consumer emphasis on preventive healthcare and daily nutritional optimization is driving the growth of the smoothies market. In an era marked by increasing awareness of diet-related chronic diseases, individuals are proactively seeking food and beverage options that support long-term well-being. According to the Centers for Disease Control and Prevention, more than 60% of U.S. adults live with at least one chronic disease such as obesity, type 2 diabetes, or cardiovascular conditions many of which are linked to poor dietary habits. Smoothies, particularly those formulated with whole fruits, leafy greens, and fortified ingredients, are perceived as an effective means of bridging nutritional deficiencies. The National Institutes of Health reports that only 12% of U.S. adults meet the recommended daily fiber intake, a shortfall that smoothies help address due to their retention of insoluble fiber from blended produce. The Council for Responsible Nutrition notes that 77% of American adults take dietary supplements, but many prefer obtaining nutrients through food-based formats, which smoothies provide in a more palatable and socially acceptable form. Brands like Suja, Bolthouse Farms, and Daily Harvest have capitalized on this trend by offering clinically backed formulations with transparent labeling.

Expansion of Ready-to-Drink (RTD) Distribution and Retail Accessibility

The proliferation of ready-to-drink (RTD) smoothies across mainstream retail and convenience channels has significantly broadened consumer access and consumption frequency are also propelling the growth of the smoothies market. According to the Food Marketing Institute, smoothies are now stocked in over 68% of U.S. supermarkets, including major chains like Kroger, Walmart, and Whole Foods, often positioned in refrigerated wellness or functional beverage sections. The U.S. Department of Agriculture confirms that chilled functional beverages experienced a 19% increase in retail square footage allocation between 2020 and 2023, reflecting retailer confidence in sustained demand. Additionally, convenience stores and gas stations have begun carrying premium smoothie brands, with Casey’s General Stores and Sheetz introducing smoothie coolers in over 2,000 locations by 2023, as reported by the National Association of Convenience Stores. E-commerce platforms have further amplified accessibility; Amazon Fresh and Instacart reported a 33% year-over-year increase in smoothie sales volume during 2023. The integration of cold-chain logistics and high-pressure processing (HPP) has enabled extended shelf life without preservatives, making national distribution feasible. Furthermore, partnerships with gyms, yoga studios, and corporate cafeterias have embedded smoothies into daily wellness routines. This omnichannel availability has transformed smoothies from occasional health treats into routine dietary staples, fueling consistent market growth.

MARKET RESTRAINTS

High Production and Cold-Chain Logistics Costs

The high operational costs associated with sourcing fresh ingredients, maintaining cold-chain integrity, and utilizing specialized processing technologies is hindering the growth of the smoothies market. Unlike shelf-stable beverages, smoothies require continuous refrigeration from production to point of sale, necessitating temperature-controlled facilities, refrigerated transport, and in-store cooling units. According to the U.S. Energy Information Administration, refrigerated warehouse electricity consumption is 2.5 times higher than ambient storage, which is significantly increasing overhead for manufacturers and distributors. Additionally, the reliance on perishable raw materials such as organic berries, spinach, and avocado exposes producers to seasonal price volatility. The U.S. Department of Agriculture reports that wholesale prices for key smoothie ingredients like strawberries and kale fluctuated by up to 40% between 2021 and 2023 due to climate disruptions and supply shortages. These cost pressures limit profit margins, particularly for smaller brands, and are often passed on to consumers, making premium smoothies less accessible to price-sensitive demographics.

Consumer Skepticism Regarding Ingredient Transparency and Sugar Content

The growing concern over sugar content and perceived lack of ingredient authenticity, which undermines consumer trust is hindering the growth of the smoothies market. Many commercial smoothies, particularly those marketed as "natural" or "organic," contain high levels of intrinsic sugars from fruit concentrates and added sweeteners, blurring the line between nutritious beverage and sugary indulgence. According to the U.S. Food and Drug Administration, the average ready-to-drink smoothie contains 35 to 50 grams of sugar per 16-ounce serving, exceeding the American Heart Association’s recommended daily limit of 25 grams for women and 36 grams for men. The Pew Research Center found that 64% of consumers in 2023 actively check nutrition labels for sugar content before purchasing beverages, with smoothies ranking among the most scrutinized categories. Environmental Working Group reports that 48% of smoothie products examined in 2023 lacked full disclosure of sourcing or processing methods.

MARKET OPPORTUNITIES

Integration of Functional and Cognitive-Enhancing Ingredients

The incorporation of nootropic, adaptogenic, and gut-health-promoting compounds into smoothie formulations is set to create huge opportunities for the growth of the smoothies market . Consumers are increasingly seeking beverages that support mental clarity, stress resilience, and emotional balance functions traditionally associated with supplements rather than food. According to the Global Organization for EPA and DHA Omega-3s (GOED), sales of omega-3 fortified foods and beverages grew by 27% between 2020 and 2023, reflecting demand for brain-supportive nutrients. Smoothies are uniquely suited to deliver such ingredients due to their viscous matrix, which enhances the solubility and bioavailability of lipophilic compounds like curcumin, ashwagandha, and phosphatidylserine. According to the American Psychological Association, 78% of adults report experiencing stress-related cognitive fatigue, creating a receptive market for "smart smoothies" that combine protein, healthy fats, and nootropics. Brands like Rebbl and Zola have introduced adaptogen-infused blends featuring reishi mushroom and rhodiola, reporting a 40% increase in repeat purchases, as documented by NielsenIQ.

Expansion into Meal Replacement and Weight Management Applications

The repurposing of smoothies as structured meal replacements in response to rising obesity rates and demand for convenient, portion-controlled nutrition are also to elevate the growth of the smoothies market. With the Centers for Disease Control and Prevention reporting that 41.9% of U.S. adults are obese, there is increasing interest in clinically validated, calorie-controlled dietary solutions. The Academy of Nutrition and Dietetics states that structured meal replacement programs can lead to 2.5 times greater weight loss than standard dieting, making smoothies a strategic tool in weight management. Companies like Soylent and Huel have demonstrated the viability of liquid nutrition models, while traditional smoothie brands are reformulating to meet medical and fitness community standards. Additionally, corporate wellness programs are incorporating smoothie-based plans; Johnson & Johnson’s employee health initiative reported a 22% improvement in metabolic markers among participants using smoothie regimens.

MARKET CHALLENGES

Regulatory Scrutiny Over Health Claims and Labeling Accuracy

The increasing vulnerable to regulatory intervention due to the prevalence of unsubstantiated health claims and inconsistent labeling practices are to impede the growth of the smoothies market. As products are marketed with assertions such as "boosts immunity," "detoxifies the body," or "supports metabolism," they attract scrutiny from federal agencies tasked with protecting consumer health. According to the Federal Trade Commission, over 120 warning letters were issued to food and beverage companies in 2023 for misleading wellness claims, with smoothie and functional drink brands representing 28% of cases. The lack of standardized definitions for terms like "cold-pressed," "raw," or "superfood" allows for interpretive marketing that can mislead consumers. The Government Accountability Office found that 44% of smoothie products examined in a 2022 review lacked clarity on ingredient sourcing or processing methods. Furthermore, the FDA’s updated Nutrition Facts labeling rules now require added sugars to be declared, exposing formulations with high fruit concentrate content.

Seasonal Ingredient Volatility and Supply Chain Fragility

The reliance on fresh, perishable produce makes the smoothies market highly susceptible to climatic disruptions, geopolitical tensions, and agricultural instability is also to restrict the growth of the smoothies market. Key ingredients such as bananas, berries, spinach, and avocados are vulnerable to extreme weather, pests, and trade restrictions, leading to supply shortages and price spikes. According to the U.S. Department of Agriculture, avocado production in California declined by 30% in 2023 due to prolonged drought, forcing manufacturers to reformulate or increase prices. These disruptions are compounded by the limited shelf life of raw materials; once harvested, leafy greens and berries must be processed within 48 to 72 hours to maintain quality, leaving little room for inventory buffering. The Institute for Supply Management reports that 68% of food and beverage producers experienced at least one major ingredient delay in 2023 due to climate or logistical issues.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 10.1% |

| Segments Covered | By Product, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | PepsiCo, Inc, Smoothie King, Maui Wowi Hawaiian Coffees & Smoothies, Suja Juice, Innocent Drinks, Bolthouse Farms, Jamba Juice Company, Ella’s Kitchen Ltd, Barfresh Food Group, Tropical Smoothie Cafe and Others. |

SEGMENTAL ANALYSIS

By Product Insights

The fruit-based smoothies segment dominated the global smoothies market by capturing 58.3% of share in 2025. The fruit-based smoothies align with innate human taste preferences for sweetness and vibrant flavor profiles, which is making them highly accessible across age groups and cultural backgrounds. According to the Monell Chemical Senses Center, humans are biologically predisposed to favor sweet tastes from an early age, a trait that influences beverage choices throughout life. The American Heart Association notes that while excessive added sugar is discouraged, naturally occurring sugars in fruits are perceived as healthier and more acceptable, enabling brands to market fruit-based blends as wholesome and guilt-free. The National Health and Nutrition Examination Survey (NHANES) data from 2021–2022 indicates that fruit consumption remains the most common dietary supplement strategy among U.S. adults, with 68% reporting daily intake of fruit-derived products, including juices and smoothies.

The Others segment is esteemed to witness a CAGR of 9.6% from 2026 to 2034 with the rise of specialized diets such as vegan, keto, paleo, and allergen-free regimens has created demand for smoothies that transcend traditional formulations. Consumers following plant-based lifestyles avoid dairy entirely, while those on ketogenic diets seek low-sugar, high-fat options incompatible with conventional fruit-heavy blends. The Academy of Nutrition and Dietetics notes that keto-friendly functional beverages grew by 31% in sales between 2021 and 2023, with smoothie brands like Territory and Ketology leading the niche. Companies are experimenting with spirulina, chlorella, and aquafaba to boost protein content while maintaining clean labels. Additionally, fermentation technology is being used to improve digestibility and flavor in plant-based blends. These innovations appeal to environmentally conscious and health-literate consumers, transforming smoothies into cutting-edge vehicles for next-generation nutrition.

By Distribution Channel Insights

The supermarkets channel segment accounted in holding 47.5% of the smoothies market share in 2025. The supermarkets offer unparalleled geographic and demographic reach, which is serving as the primary grocery destination for over 80% of American households, according to the U.S. Bureau of Labor Statistics. Their extensive refrigerated sections now feature dedicated functional beverage zones, where smoothies are positioned alongside yogurts, plant milks, and health shots, reinforcing their perception as nutritious staples. The National Grocers Association reports that 68% of supermarket chains have expanded chilled wellness product offerings since 2020, with smoothies occupying premium shelf space due to high-margin potential. Consumers benefit from price transparency, promotional discounts, and brand variety, enabling comparison shopping.

The smoothie bars channel segment is to witness a CAGR of 8.9% from 2026 to 2034. The smoothie bars have evolved from simple juice kiosks into immersive wellness destinations that emphasize transparency, customization, and lifestyle branding. Consumers increasingly value the ability to witness their smoothie being made in real time, selecting base ingredients, add-ons, and portion sizes. According to the National Restaurant Association, 63% of diners in 2023 preferred establishments that offered build-your-own options, a trend leveraged by chains like Jamba, Smoothie King, and Nékter. These venues often display sourcing information, nutritional data, and allergen warnings prominently, catering to health-literate and medically supervised consumers.

REGIONAL ANALYSIS

North America Smoothies Market Analysis

North America was the largest contributor of the global smoothies market by accounting for 42.3% of share in 2025, with the high consumer awareness of functional nutrition, robust retail infrastructure, and a culture of fitness and preventive health. The proliferation of health-focused retail chains like Whole Foods and Sprouts, alongside mainstream adoption in Walmart and Target, has normalized smoothie consumption across income levels. Additionally, the presence of major brands such as Bolthouse Farms, Suja, and Daily Harvest drives innovation in formulation and packaging. The rise of HPP (high-pressure processing) technology in North America, used by over 60% of premium RTD smoothie producers, as per the Institute of Food Technologists,ensures product safety and shelf stability without preservatives.

Europe Smoothies Market Analysis

Europe was positioned next by holding 18.2% of the share in 2025. The region’s market is characterized by stringent food regulations, high environmental consciousness, and a preference for clean-label, organic products. Countries like Germany, the UK, and Sweden lead in organic smoothie adoption, with organic fruit production increasing by 17% between 2020 and 2023, according to Eurostat. Additionally, the Nordic region has embraced smoothies as part of the “New Nordic Diet,” which emphasizes local, seasonal, and sustainable ingredients. The Danish Veterinary and Food Administration notes that fortified functional beverages must comply with strict health claim regulations, ensuring product credibility.

Asia Pacific Smoothies Market Analysis

Asia Pacific is emerging as a high-potential region due to rising urbanization and health awareness. China’s ready-to-drink health beverage market grew by 22% annually between 2020 and 2023, reaching $12.4 billion in sales, according to the China Beverage Association. Indian consumers are adopting smoothies as alternatives to traditional sugary drinks like lassi and sugarcane juice, with urban fitness centers increasingly offering customized blends. Japan has integrated smoothies into its preventive healthcare initiatives, with the Ministry of Health, Labour and Welfare promoting fruit and vegetable intake to combat aging-related diseases. However, taste preferences for less sweet or icy textures require product adaptation.

Latin America Smoothies Market

Latin America is expected to have a significant growth opportunities in the next coming years. Countries like Brazil, Mexico, and Colombia are major producers of acai, mango, and papaya key ingredients in commercial smoothies. In urban centers, smoothie bars and juice kiosks are gaining popularity among young professionals and fitness enthusiasts. However, limited refrigeration infrastructure and lower consumer spending power constrain widespread adoption of premium RTD products.

Middle East & Africa Smoothies Market Analysis

The Middle East and Africa are growing steadily in the next coming years. Dubai’s Department of Economy and Tourism reports that health-focused F&B outlets increased by 28% between 2021 and 2023, with smoothie bars appearing in malls and fitness centers. Saudi Arabia’s Vision 2030 includes investments in preventive healthcare, creating opportunities for functional beverages. In Africa, South Africa leads in processed smoothie adoption, with Pick n Pay and Woolworths offering chilled organic options. However, in most Sub-Saharan countries, smoothies remain informal products sold in markets or as street food.

COMPETITIVE LANDSCAPE

Key Market Participants

Some of the notable players in the global smoothies market include

- PepsiCo, Inc.

- Smoothie King

- Maui Wowi Hawaiian Coffees & Smoothies

- Suja Juice

- Innocent Drinks

- Bolthouse Farms

- Jamba Juice Company

- Ella’s Kitchen Ltd

- Barfresh Food Group

- Tropical Smoothie Cafe

- Others

The competitive landscape of the smoothies market is defined by a tension between authenticity and scalability, where brands must balance artisanal quality with mass-market accessibility. While large-scale producers leverage distribution power and retail dominance, niche players differentiate through ingredient transparency, functional innovation, and lifestyle branding. Competition extends beyond flavor and nutrition to encompass sourcing ethics, environmental impact, and consumer education, with brands increasingly judged on their commitment to regenerative agriculture, plastic reduction, and social equity. The rise of private-label offerings from major retailers has intensified price pressure, forcing premium brands to justify their value through clinical validation and sensory excellence. At the same time, the blurring lines between smoothies, meal replacements, and pharmaceutical-grade nutrition have invited crossover competition from supplement and medical food companies. Digital engagement has become a critical battleground, with social media, influencer partnerships, and mobile apps shaping brand perception and purchase behavior. Innovation cycles are accelerating, driven by advances in preservation technology, plant-based science, and personalization algorithms. Ultimately, the most resilient competitors are those that treat the smoothie not merely as a beverage but as a vehicle for holistic well-being, which is embedding purpose, science, and trust into every aspect of their offering.

TOP PLAYERS IN THE MARKET

Bolthouse Farms

Bolthouse Farms has emerged as a pioneering force in the premium smoothies market by seamlessly integrating agriculture, nutrition science, and consumer branding. Bolthouse’s innovation in high-pressure processing (HPP) technology has set industry benchmarks for shelf life and nutrient retention without preservatives. The brand’s presence in major retail and foodservice channels has made it a household name in North America, while its commitment to sustainability in farming and packaging resonates with eco-conscious consumers.

Suja Life LLC

Suja Life has positioned itself at the forefront of the organic and cold-pressed beverage revolution, which is transforming the smoothies market with a focus on purity, probiotics, and holistic wellness. The company’s philosophy centers on delivering raw, unpasteurized products that preserve live enzymes and beneficial microbes, appealing to health-focused and immunocompromised consumers. Suja’s formulations often include adaptogens, plant-based proteins, and fermented ingredients, aligning with emerging trends in gut health and cognitive wellness. Its success lies in bridging the gap between clinical-grade nutrition and consumer accessibility, offering products that are both scientifically grounded and sensorially appealing.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

- A primary strategy among leading smoothie brands is vertical integration of the supply chain, from farm sourcing to final packaging, ensuring control over ingredient quality, sustainability, and traceability. Companies can guarantee freshness, reduce contamination risks, and promote regenerative agricultural practices by enhancing both product integrity and brand trust.

- Another key approach is the development of science-backed formulations that align with clinical nutrition principles, incorporating functional ingredients such as probiotics, adaptogens, and plant proteins. Brands are increasingly collaborating with dietitians, nutrition scientists, and medical advisors to formulate products that support specific health outcomes, which is transforming smoothies from casual refreshments into credible wellness tools.

- Also, leveraging digital platforms and subscription models to deepen customer relationships and ensure recurring revenue. Direct-to-consumer channels allow for personalized offerings, data-driven insights, and rapid product iteration based on user feedback by enabling brands to stay agile in a fast-evolving market while building community and loyalty around health-centric lifestyles.

RECENT HAPPENINGS IN THE MARKET

- In March 2025, Bolthouse Farms launched a new line of protein-fortified, keto-friendly smoothies made with avocado and MCT oil by targeting fitness enthusiasts and low-carb diet followers across North American retail chains.

- In July 2023, Suja Life partnered with a microbiome research institute to develop a next-generation probiotic smoothie series clinically tested for gut-brain axis support by enhancing its scientific credibility and premium positioning.

- In November 2023, Daily Harvest introduced a regeneratively sourced frozen smoothie cup line, certified by a third-party soil health organization, which is reinforcing its commitment to sustainable agriculture and climate-positive practices.

- In January 2025, Nestlé Health Science acquired a minority stake in a functional smoothie startup specializing in medical nutrition for aging population by signaling expansion into clinically supported dietary solutions.

- In May 2025, Smoothie King opened its 1,000th store in Nashville, Tennessee, featuring an enhanced digital ordering system and recovery-focused formulations developed in collaboration with sports nutritionists.

MARKET SEGMENTATION

This research report on the global smoothies market has been segmented and sub-segmented based on product, distribution channel, and region.

By Product

- Fruit-Based

- Organic

- Inorganic

- Dairy-Based

By Distribution Channel

- Restaurants

- Supermarkets

- Convenience Stores

- Smoothie Bars

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is the size of the global smoothies market in 2025?

The global smoothies market is expected to be valued at USD 17.78 billion in 2025.

2. What is the projected CAGR of the global smoothies market?

The market is forecasted to grow at a CAGR of 10.1% from 2026 to 2034.

3. What factors are driving the growth of the smoothies market?

Increasing health awareness and demand for nutritious, on-the-go beverages are key growth drivers.

4. Which regions are leading in the global smoothies market?

North America and Europe are the dominant regions due to high health-conscious consumer bases.

5. What types of smoothies are popular in the market?

Fruit-based, dairy-based, and green smoothies are among the most popular segments.

6. Is plant-based smoothie demand increasing?

Yes, demand for plant-based and vegan smoothies is rising with the shift toward plant-based diets.

7. Who are the major players in the global smoothies market?

Key players include Jamba Juice, Smoothie King, Bolthouse Farms, and PepsiCo’s Naked Juice.

8. What consumer trends are shaping the smoothies market?

Preferences for clean-label, organic, low-sugar, and functional ingredients are shaping the market.

9. How are e-commerce and delivery apps influencing the market?

Online platforms and delivery apps are expanding smoothie accessibility and boosting market growth.

10. What challenges does the smoothies market face?

High prices, shelf-life limitations, and sugar content concerns are key challenges.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com